Ulta's (NASDAQ:ULTA) Q2 Sales Top Estimates

Radek Strnad /

August 24, 2023

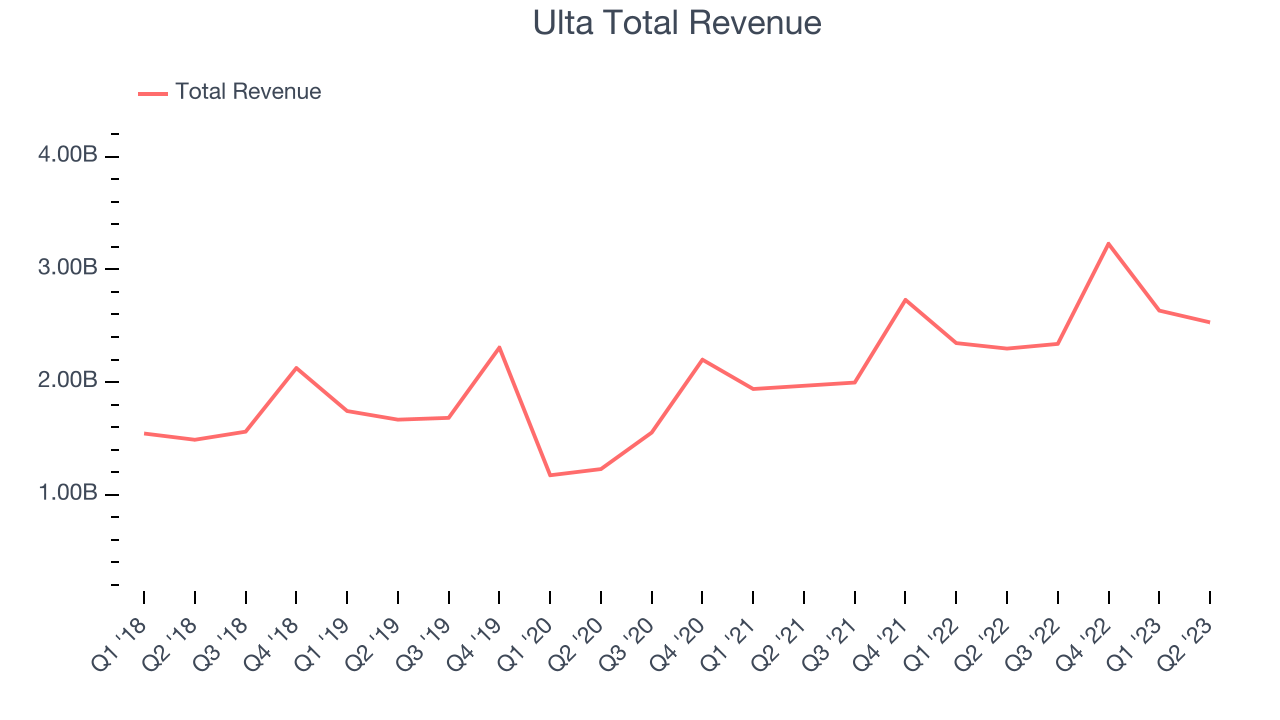

Beauty, cosmetics, and personal care retailer Ulta Beauty (NASDAQ:ULTA) reported Q2 FY2023 results topping analysts' expectations, with revenue up 10.1% year on year to $2.53 billion. The company's outlook for the full year was also close to analysts' estimates with revenue guided to $11.1 billion at the midpoint. Ulta made a GAAP profit of $300.1 million, improving from its profit of $295.7 million in the same quarter last year.

Is now the time to buy Ulta? Find out in our full research available to StockStory Edge members.

Ulta (ULTA) Q2 FY2023 Highlights:

- Revenue: $2.53 billion vs analyst estimates of $2.5 billion (1.28% beat)

- EPS: $6.02 vs analyst estimates of $5.86 (2.7% beat)

- The company reconfirmed revenue guidance for the full year of $11.1 billion at the midpoint

- Free Cash Flow of $28.9 million, down 55.5% from the same quarter last year

- Gross Margin (GAAP): 39.3%, down from 40.4% in the same quarter last year

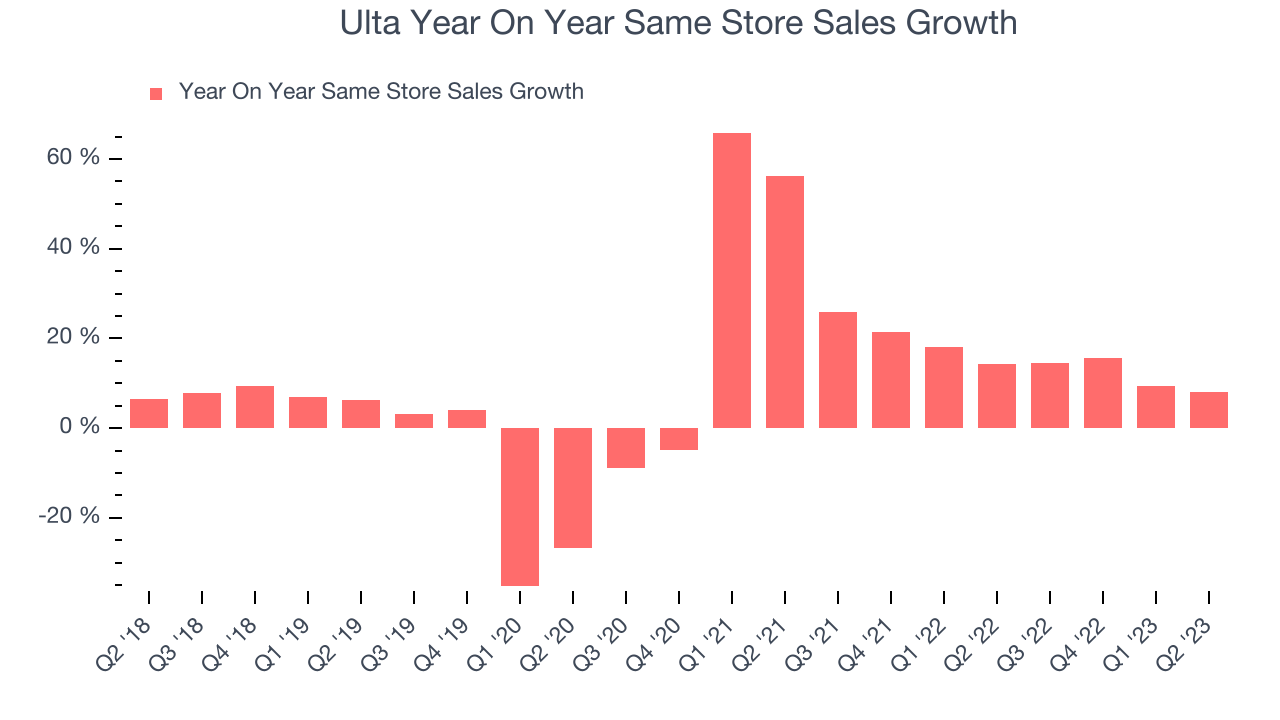

- Same-Store Sales were up 8% year on year

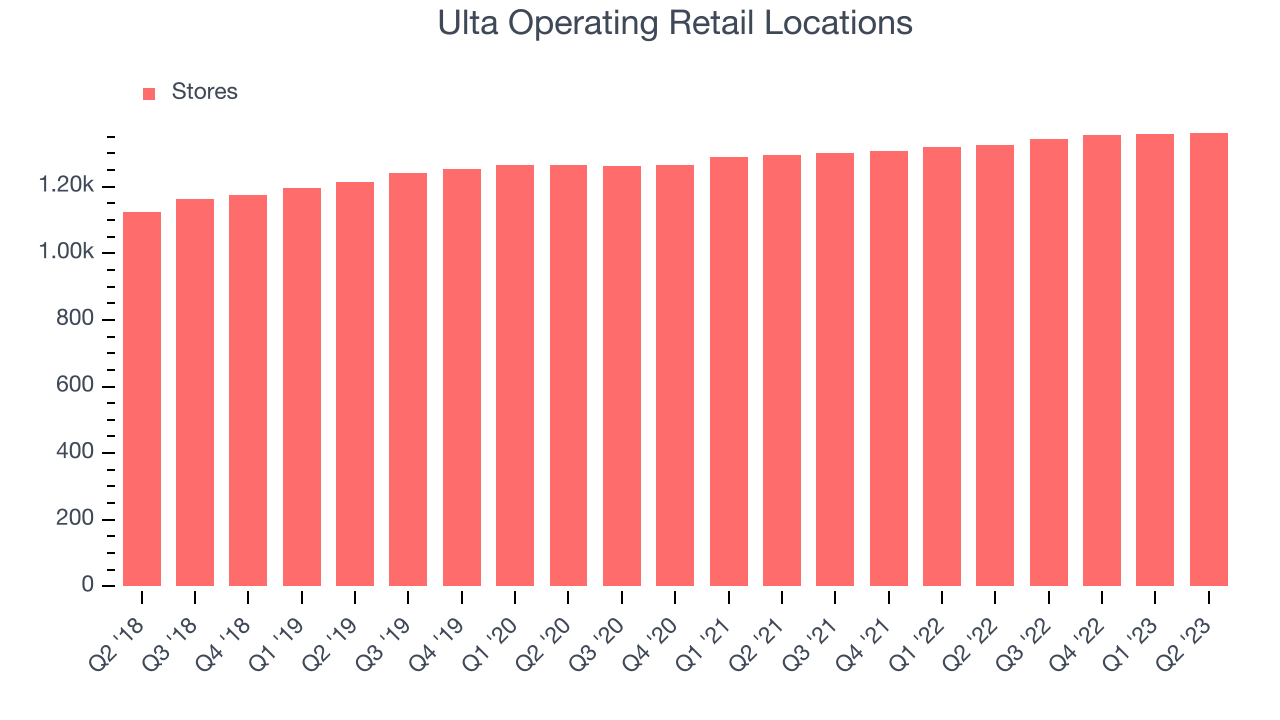

- Store Locations: 1,362 at quarter end, increasing by 37 over the last 12 months

“The Ulta Beauty team delivered another quarter of strong performance, with sales, gross profit, and SG&A expenses all better than our internal expectations. During the quarter, we drove growth across all major categories, increased the number of loyalty members, and strengthened engagement with the Ulta Beauty brand. In addition, our teams achieved important milestones for our multi-year, transformational investment agenda designed to drive efficiencies and support our future growth,” said Dave Kimbell, Chief Executive Officer.

Offering high-end prestige brands as well as lower-priced, mass-market ones, Ulta Beauty (NASDAQ:ULTA) is an American retailer that sells makeup, skincare, haircare, and fragrance products.

Beauty and cosmetics retailers understand that beauty is in the eye of the beholder, but a little lipstick, nail polish, and glowing skin also help the cause. These stores—which mostly cater to consumers but can also garner the attention of salon pros—aim to be a one-stop personal care and beauty products shop with many brands across many categories. E-commerce is changing how consumers buy cosmetics, so these retailers are constantly evolving to meet the customer where and how they want to shop.

Sales Growth

Ulta is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

As you can see below, the company's annualized revenue growth rate of 10.9% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was impressive as it opened new stores and grew sales at existing, established stores.

This quarter, Ulta reported robust year-on-year revenue growth of 10.1% and its revenue of $2.53 billion exceeded analysts' expectations by 1.28%. Looking ahead, the analysts covering the company expect sales to grow 6.56% over the next 12 months.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

A retailer's store count often determines on how much revenue it can generate.

When a retailer like Ulta is opening new stores, it usually means that demand is greater than supply, and in turn, it's investing for growth. Ulta's store count increased by 37 locations, or 2.79%, over the last 12 months to 1,362 total retail locations in the most recently reported quarter.

Taking a step back, the company has generally opened new stores over the last eight quarters, averaging 2.96% annual growth in its physical footprint. This is decent store growth and in line with other retailers. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Same-Store Sales

Ulta's demand has outpaced the broader consumer retail sector over the last eight quarters. On average, the company has grown its same-store sales by a robust 15.9% year on year. This performance suggests that its steady rollout of new stores could be beneficial for shareholders. When a company has strong demand, more locations should help it reach more customers seeking its products.

In the latest quarter, Ulta's same-store sales rose 8% year on year. By the company's standards, this growth was a meaningful deceleration from the 14.4% year-on-year increase it posted 12 months ago. One quarter fluctuations aren't material for the long-term prospects of a business, especially when they're coming off a tough comparison period, but we'll watch Ulta closely to see if it can reaccelerate growth.

Key Takeaways from Ulta's Q2 Results

With a market capitalization of $21.8 billion, a $388.6 million cash balance, and positive free cash flow over the last 12 months, we're confident that Ulta has the resources needed to pursue a high-growth business strategy.

It was good to see Ulta beat analysts' revenue and EPS estimates this quarter, driven by outperformance in same-store sales growth. This was especially encouraging given it was a tough comparison quarter (Ulta was coming off 14.4% same-store sales growth in the same quarter last year) and its competitors, Bath & Body Works and Sally Beauty (to name a few), missed their sales numbers. Furthermore, Ulta extended its hot streak of beating Wall Street's expectations to over two years. Overall, this was a good quarter. The stock is up 2.51% after reporting and currently trades at $433.44 per share.

So should you invest in Ulta right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.