Zscaler (NASDAQ:ZS) Posts Better-Than-Expected Q1 But Stock Drops

Petr Huřťák /

November 27, 2023

Cloud security platform Zscaler (NASDAQ:ZS) reported Q1 FY2024 results topping analysts' expectations, with revenue up 39.7% year on year to $496.7 million. Guidance for next quarter's revenue was also better than expected at $506 million at the midpoint, 1.7% above analysts' estimates. It made a non-GAAP profit of $0.67 per share, improving from its profit of $0.29 per share in the same quarter last year.

Is now the time to buy Zscaler? Find out in our full research report.

Zscaler (ZS) Q1 FY2024 Highlights:

- Revenue: $496.7 million vs analyst estimates of $473.4 million (4.9% beat

- Billings: $456.6 million vs. analyst estimates of $442.1 million (3.3% beat)

- EPS (non-GAAP): $0.67 vs analyst estimates of $0.49 (36.9% beat)

- Revenue Guidance for Q2 2024 is $506 million at the midpoint, above analyst estimates of $497.3 million

- The company lifted its revenue guidance for the full year from $2.06 billion to $2.10 billion at the midpoint, a 1.8% increase (non-GAAP income from operations guidance also raised, although billings guidance maintained)

- Free Cash Flow of $224.7 million, up 122% from the previous quarter (beat)

- Gross Margin (GAAP): 77.6%, down from 78.5% in the same quarter last year (miss)

“We had a strong start to our fiscal year with all key metrics coming above our guidance. We are enabling enterprises to move forward with their key transformative initiatives - Zero Trust and AI - which is driving demand for our Zero Trust Exchange,” said Jay Chaudhry, Chairman and CEO of Zscaler.

After successfully selling all four of his previous cybersecurity companies, Jay Chaudhry's fifth venture, Zscaler (NASDAQ:ZS) offers software-as-a-service that helps companies securely connect to applications and networks in the cloud.

Network Security

Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks. The migration of businesses to the cloud and employees working remotely in insecure environments is increasing demand modern cloud-based network security software, which offers better performance at lower cost than maintaining the traditional on-premise solutions, such as expensive specialized firewall hardware.

Sales Growth

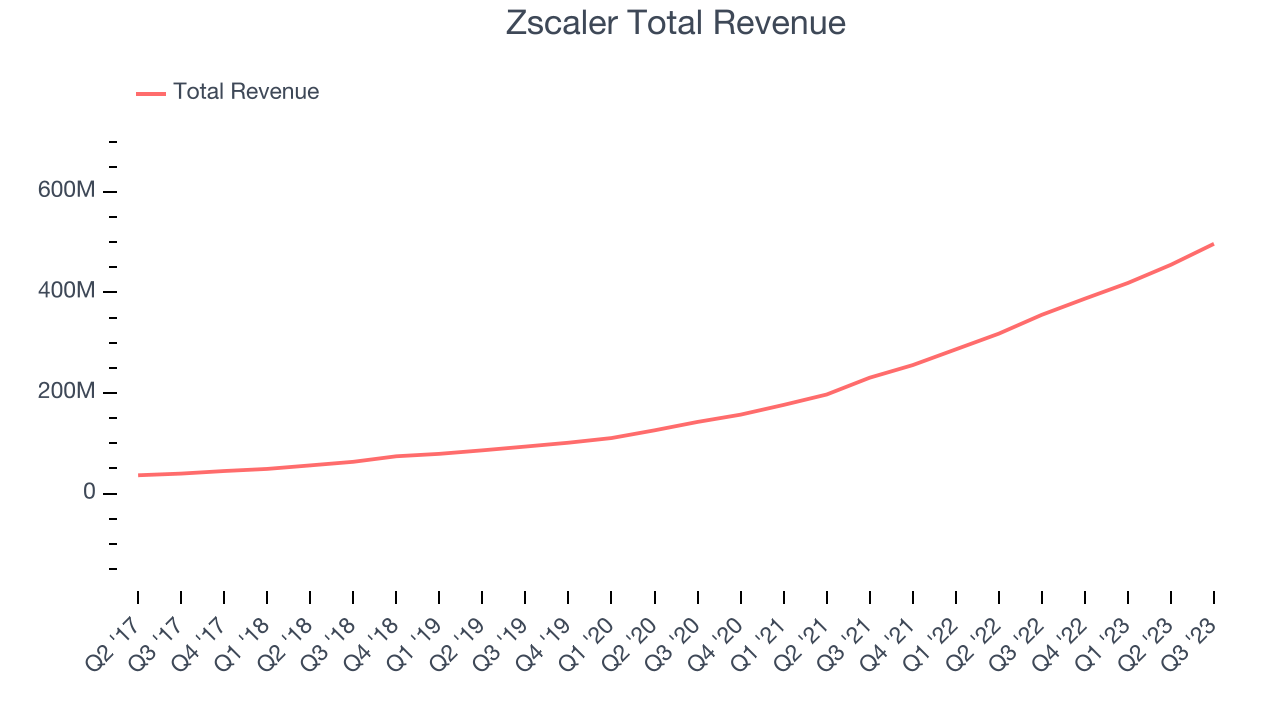

As you can see below, Zscaler's revenue growth has been exceptional over the last two years, growing from $230.5 million in Q1 FY2022 to $496.7 million this quarter.

Unsurprisingly, this was another great quarter for Zscaler with revenue up 39.7% year on year. On top of that, its revenue increased $41.7 million quarter on quarter, a solid improvement from the $36.21 million increase in Q4 2023. This is a sign of slight re-acceleration of growth.

Next quarter, Zscaler is guiding for a 23.4% year-on-year revenue decline to $506 million, a further deceleration from the 51.7% year-on-year decrease it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 24.2% over the next 12 months before the earnings results announcement.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. See it here.

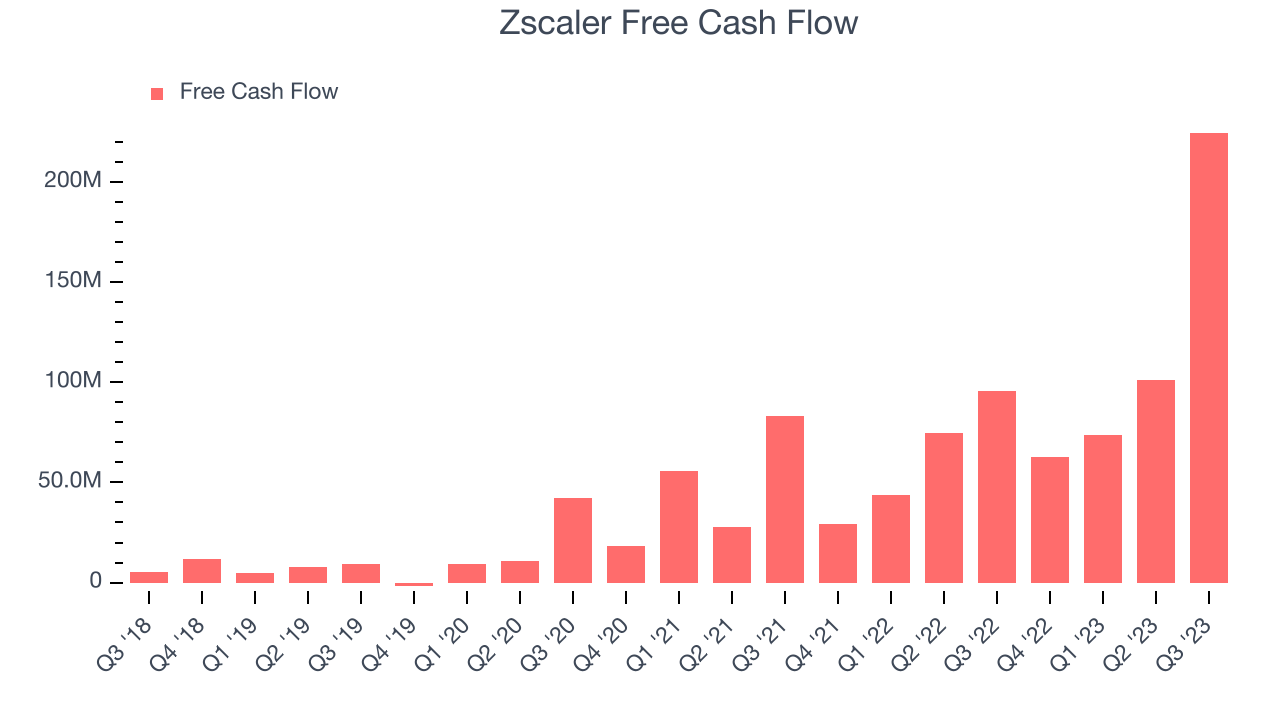

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Zscaler's free cash flow came in at $224.7 million in Q1, up 135% year on year.

Zscaler has generated $462.7 million in free cash flow over the last 12 months, an impressive 25.3% of revenue. This high FCF margin stems from its asset-lite business model and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a cash cushion.

Key Takeaways from Zscaler's Q1 Results

Sporting a market capitalization of $28.64 billion, more than $2.32 billion in cash on hand, and positive free cash flow over the last 12 months, we believe that Zscaler is attractively positioned to invest in growth.

It was good to see Zscaler beat analysts' billings, revenue, and non-GAAP operating profit expectations this quarter. We were also glad next quarter's revenue guidance came in higher than Wall Street's estimates. Lastly, it was a major positive that Zscaler raised its full year revenue and non-GAAP operating profit guidance. Overall, we think this was a strong quarter that should satisfy most shareholders. The market was likely expecting more, however, and the stock is down 6.8% after reporting, trading at $178.83 per share. This could be due to some combination of a gross margin miss (and decline year on year), comments that the company plans on "scaling our go-to-market and R&D organizations" (which could hurt near-term margins), and high expectations.

So should you invest in Zscaler right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.