ACV Auctions (ACVA)

ACV Auctions doesn’t excite us. It not only barely produces cash but also has been less efficient lately, as seen by its falling margins.― StockStory Analyst Team

1. News

2. Summary

Why ACV Auctions Is Not Exciting

Founded in 2014, ACV Auctions (NASDAQ:ACVA) is an online auction marketplace for car dealers and wholesalers to buy and sell used cars.

- High servicing costs result in an inferior gross margin of 27.1% that must be offset through higher volumes

- Excessive marketing spend signals little organic demand and traction for its platform

- A positive is that its marketplace Units have grown by 17.3% annually, allowing for more profitable cross-selling opportunities if it can build complementary products and features

ACV Auctions’s quality is insufficient. We see more lucrative opportunities elsewhere.

Why There Are Better Opportunities Than ACV Auctions

ACV Auctions is trading at $4.85 per share, or 10.2x forward EV/EBITDA. This multiple rich for the business quality. Not a great combination.

Paying a premium for high-quality companies with strong long-term earnings potential is preferable to owning challenged businesses with questionable prospects. That helps the prudent investor sleep well at night.

3. ACV Auctions (ACVA) Research Report: Q4 CY2025 Update

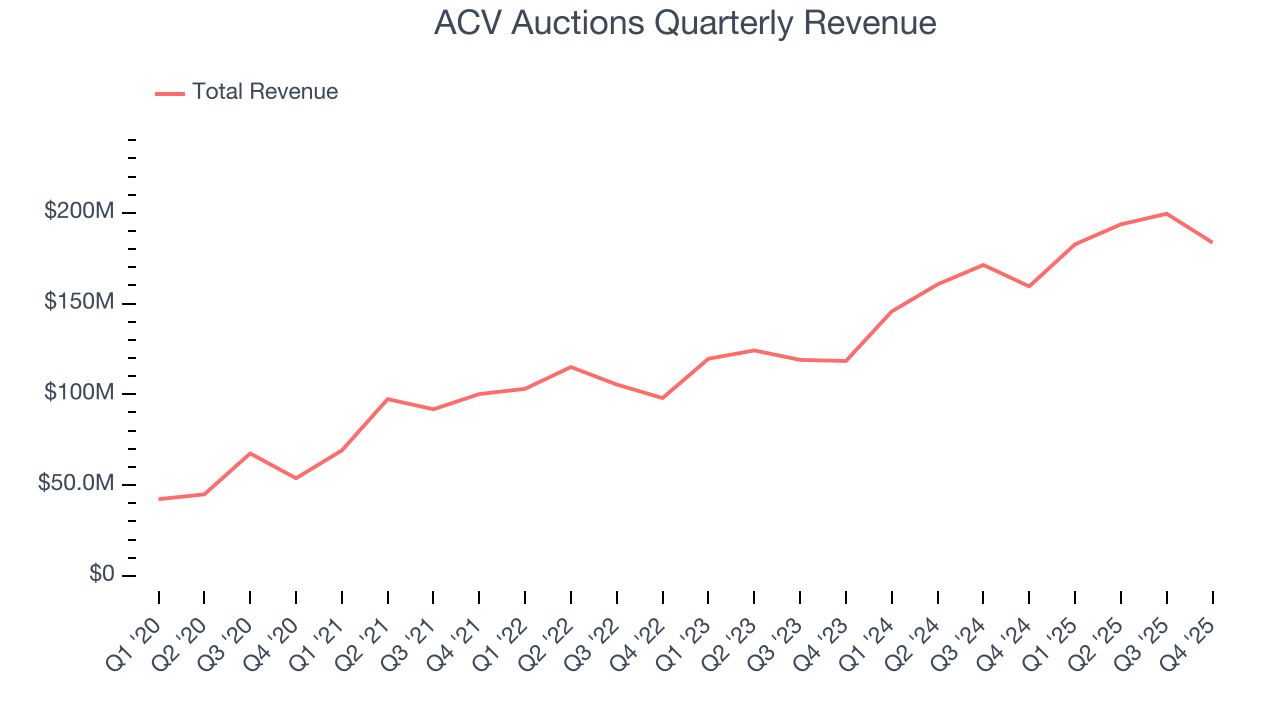

Online used car auction platform ACV Auctions (NASDAQ:ACVA) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 15.1% year on year to $183.6 million. On the other hand, next quarter’s revenue guidance of $202 million was less impressive, coming in 0.9% below analysts’ estimates. Its GAAP loss of $0.11 per share was in line with analysts’ consensus estimates.

ACV Auctions (ACVA) Q4 CY2025 Highlights:

- Revenue: $183.6 million vs analyst estimates of $182 million (15.1% year-on-year growth, 0.9% beat)

- EPS (GAAP): -$0.11 vs analyst estimates of -$0.12 (in line)

- Adjusted EBITDA: $7.62 million vs analyst estimates of $5.88 million (4.1% margin, 29.7% beat)

- Revenue Guidance for Q1 CY2026 is $202 million at the midpoint, below analyst estimates of $203.7 million

- EBITDA guidance for the upcoming financial year 2026 is $75 million at the midpoint, below analyst estimates of $78.13 million

- Operating Margin: -9.7%, up from -16.2% in the same quarter last year

- Free Cash Flow was -$23.37 million compared to -$1.25 million in the previous quarter

- Market Capitalization: $1.15 billion

Company Overview

Founded in 2014, ACV Auctions (NASDAQ:ACVA) is an online auction marketplace for car dealers and wholesalers to buy and sell used cars.

The company's mission is to provide an efficient platform for buying and selling used cars in virtual auction settings. By digitizing the process, ACV Auctions reduces the time and costs associated with attending physical auctions and broadens the pool of buyers and sellers. Additionally, the company provides a range of services that includes vehicle inspections, financing, and transportation to make the platform a one-stop shop.

The customers of ACV Auctions are car dealers and wholesalers who are looking for a reliable and convenient way to buy and sell used cars. The platform is especially popular among smaller dealerships that don’t have the resources to attend physical auctions. ACV Auctions generates revenue by charging a fee for each transaction on its platform.

For example, a car dealer in Texas wants to purchase ten used cars from a Florida seller. Without a digital marketplace, that Texas dealer may not have found the Florida cars. Even if those cars were discovered, the dealer likely would have had to travel to Florida to attend a physical auction. With ACV Auctions, the dealer can participate in the auction virtually and bid real-time. After purchasing, the dealer can arrange transportation of the cars on the platform.

4. Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Competitors offering marketplaces for used car sales include Carvana, (NYSE:CVNA), KAR Auction Services (NYSE:KAR), and private company Manheim.

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, ACV Auctions grew its sales at an impressive 21.7% compounded annual growth rate. Its growth beat the average consumer internet company and shows its offerings resonate with customers.

This quarter, ACV Auctions reported year-on-year revenue growth of 15.1%, and its $183.6 million of revenue exceeded Wall Street’s estimates by 0.9%. Company management is currently guiding for a 10.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.4% over the next 12 months, a deceleration versus the last three years. Still, this projection is noteworthy and suggests the market is baking in success for its products and services.

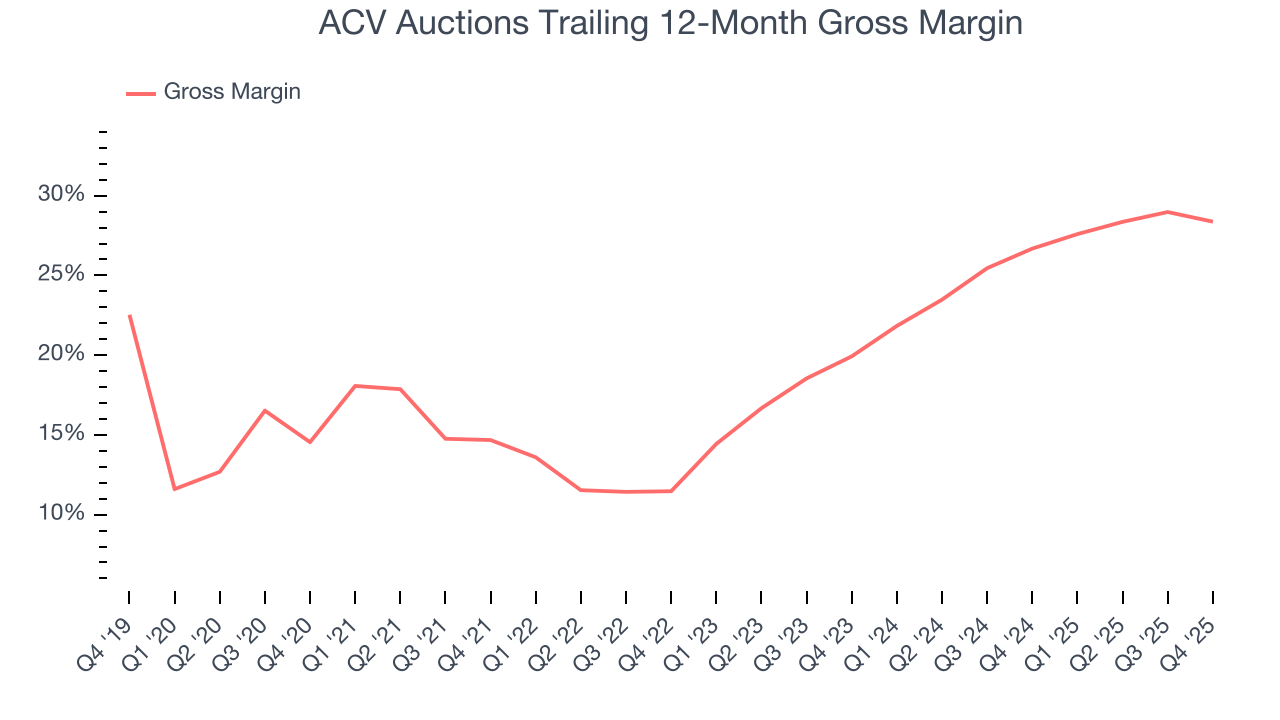

6. Gross Margin & Pricing Power

For online marketplaces like ACV Auctions, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification.

ACV Auctions’s unit economics are far below other consumer internet companies, signaling it operates in a competitive market and must pay many third parties a slice of its sales to distribute its products and services. As you can see below, it averaged a 27.6% gross margin over the last two years. Said differently, ACV Auctions had to pay a chunky $72.40 to its service providers for every $100 in revenue.

ACV Auctions produced a 23.8% gross profit margin in Q4 , marking a 2.1 percentage point decrease from 25.8% in the same quarter last year. Zooming out, however, ACV Auctions’s full-year margin has been trending up over the past 12 months, increasing by 1.7 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

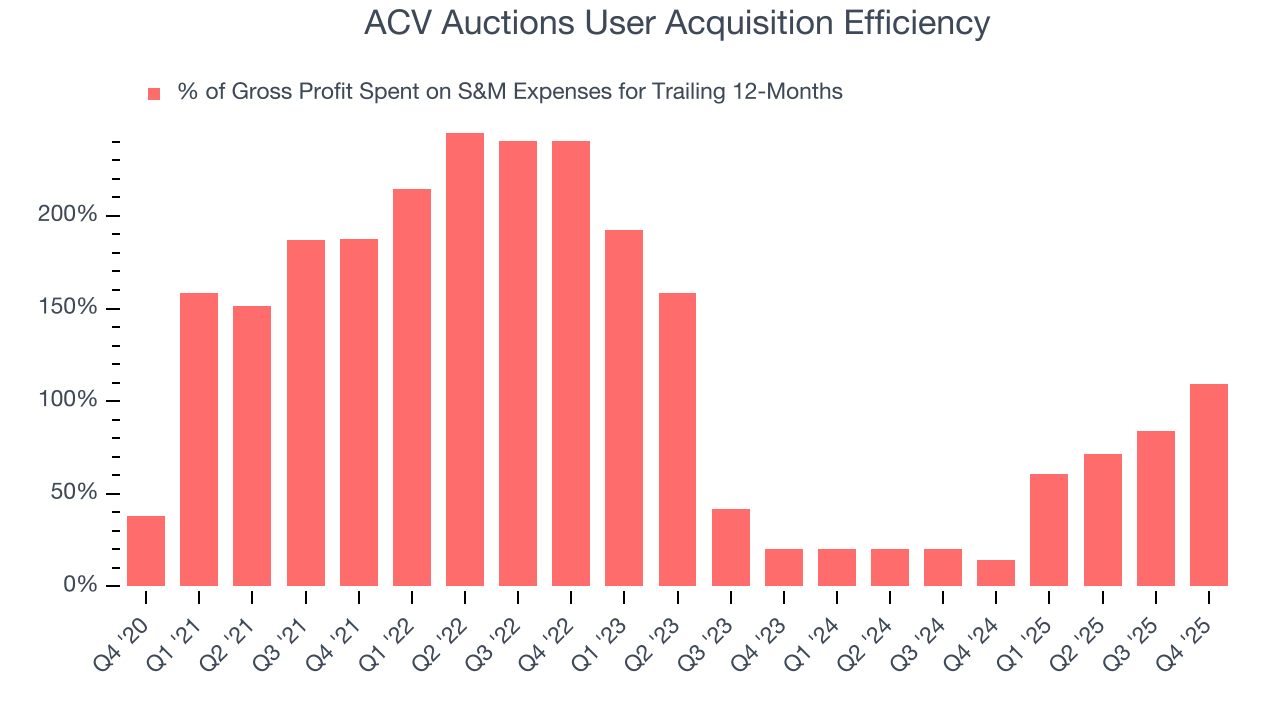

7. User Acquisition Efficiency

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like ACV Auctions grow from a combination of product virality, paid advertisement, and incentives.

It’s very expensive for ACV Auctions to acquire new users as the company has spent 109% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates a highly competitive environment with little differentiation between ACV Auctions and its peers.

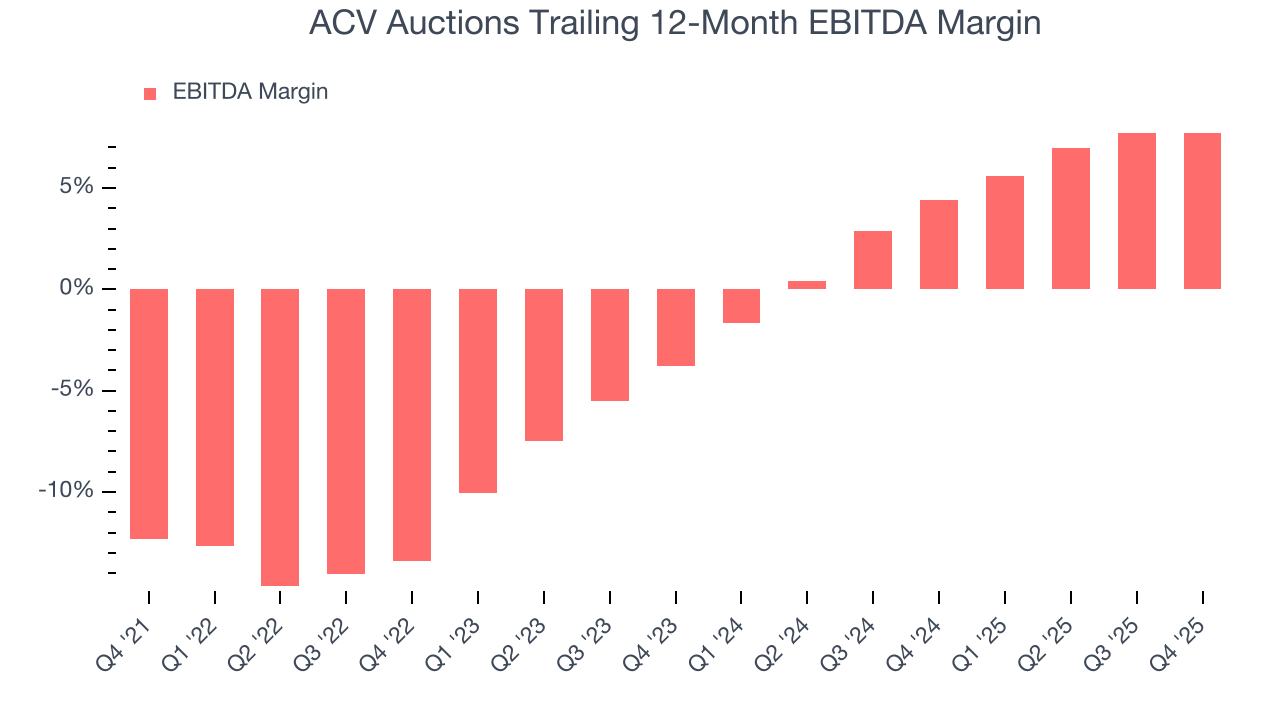

8. EBITDA

ACV Auctions has managed its cost base well over the last two years. It demonstrated solid profitability for a consumer internet business, producing an average EBITDA margin of 6.2%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, ACV Auctions’s EBITDA margin rose by 21.1 percentage points over the last few years, as its sales growth gave it immense operating leverage.

In Q4, ACV Auctions generated an EBITDA margin profit margin of 4.1%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

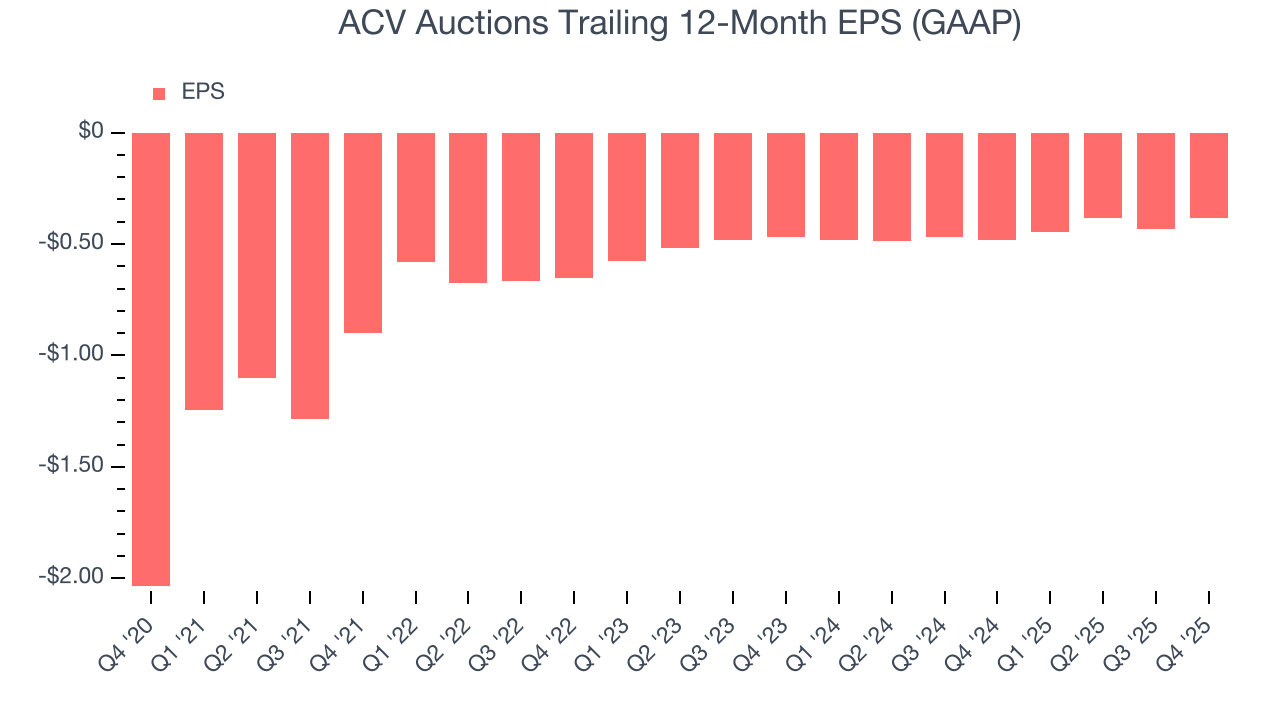

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although ACV Auctions’s full-year earnings are still negative, it reduced its losses and improved its EPS by 16.2% annually over the last three years. The next few quarters will be critical for assessing its long-term profitability.

In Q4, ACV Auctions reported EPS of negative $0.11, up from negative $0.16 in the same quarter last year. This print beat analysts’ estimates by 8%. Over the next 12 months, Wall Street expects ACV Auctions to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.38 will advance to negative $0.21.

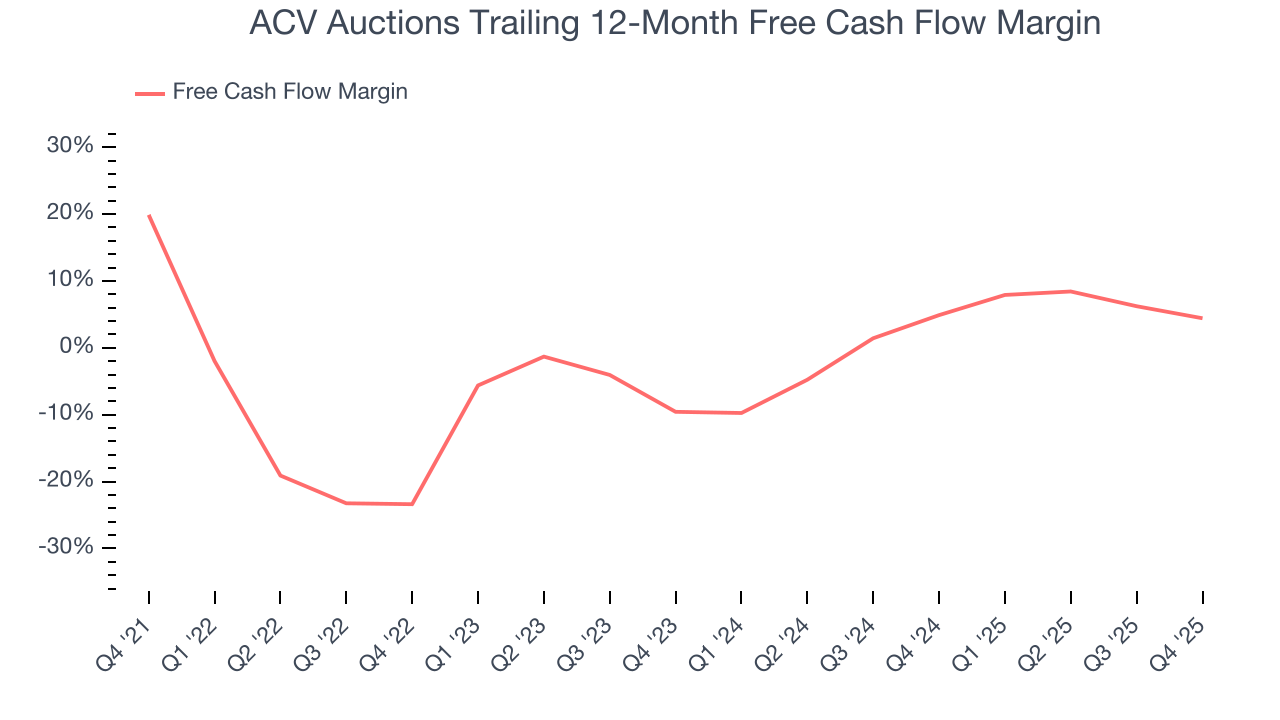

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

ACV Auctions has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.6%, subpar for a consumer internet business.

Taking a step back, an encouraging sign is that ACV Auctions’s margin expanded by 27.8 percentage points over the last few years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

ACV Auctions burned through $23.37 million of cash in Q4, equivalent to a negative 12.7% margin. The company’s cash burn was similar to its $11.19 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business.

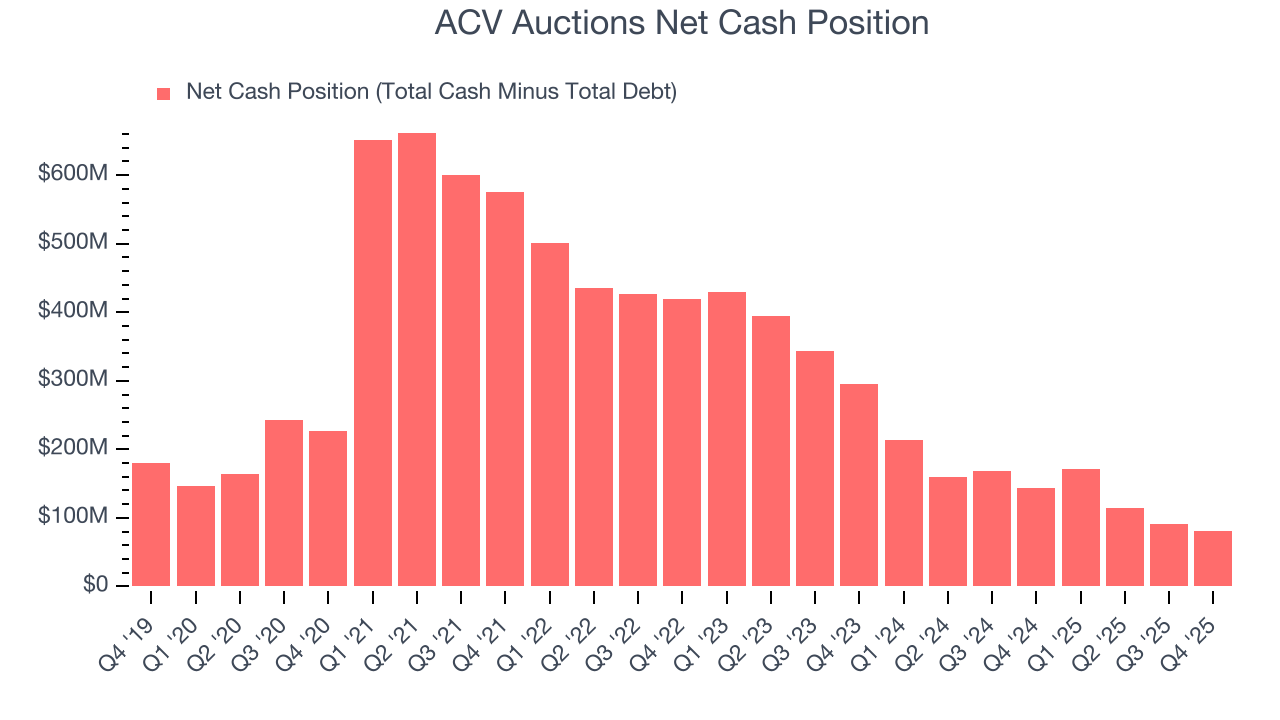

11. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

ACV Auctions is a well-capitalized company with $271.5 million of cash and $190 million of debt on its balance sheet. This $81.5 million net cash position is 7.1% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from ACV Auctions’s Q4 Results

We were impressed by how significantly ACV Auctions blew past analysts’ EBITDA expectations this quarter. On the other hand, its full-year EBITDA guidance missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded up 9% to $6.19 immediately after reporting.

13. Is Now The Time To Buy ACV Auctions?

Updated: March 14, 2026 at 10:36 PM EDT

When considering an investment in ACV Auctions, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

ACV Auctions isn’t a terrible business, but it doesn’t pass our quality test. Although its revenue growth was impressive over the last three years, it’s expected to deteriorate over the next 12 months and its sales and marketing spend is very high compared to other consumer internet businesses. And while the company’s rising cash profitability gives it more optionality, the downside is its gross margins make it extremely difficult to reach positive operating profits compared to other consumer internet businesses.

ACV Auctions’s EV/EBITDA ratio based on the next 12 months is 10.2x. Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $9.12 on the company (compared to the current share price of $4.85).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.