Flowers Foods (FLO)

We wouldn’t recommend Flowers Foods. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Flowers Foods Will Underperform

With Wonder Bread as its premier brand, Flower Foods (NYSE:FLO) is a packaged foods company that focuses on bakery products such as breads, buns, and cakes.

- Performance over the past three years shows its incremental sales were much less profitable, as its earnings per share fell by 21% annually

- Organic sales performance over the past two years indicates the company may need to make strategic adjustments or rely on M&A to catalyze faster growth

- Estimated sales decline of 1.3% for the next 12 months implies a challenging demand environment

Flowers Foods’s quality is insufficient. We see more favorable opportunities in the market.

Why There Are Better Opportunities Than Flowers Foods

Flowers Foods’s stock price of $8.24 implies a valuation ratio of 10x forward P/E. Flowers Foods’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Flowers Foods (FLO) Research Report: Q4 CY2025 Update

Packaged bakery food company Flower Foods (NYSE:FLO) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 11% year on year to $1.23 billion. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $5.22 billion at the midpoint. Its non-GAAP profit of $0.22 per share was 45.6% above analysts’ consensus estimates.

Flowers Foods (FLO) Q4 CY2025 Highlights:

- Revenue: $1.23 billion vs analyst estimates of $1.23 billion (11% year-on-year growth, in line)

- Adjusted EPS: $0.22 vs analyst estimates of $0.15 (45.6% beat)

- Adjusted EBITDA: $117.4 million vs analyst estimates of $100.4 million (9.5% margin, 16.9% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.85 at the midpoint, missing analyst estimates by 12.4%

- EBITDA guidance for the upcoming financial year 2026 is $480 million at the midpoint, below analyst estimates of $503.8 million

- Operating Margin: -5.8%, down from 5.9% in the same quarter last year

- Free Cash Flow Margin: 6.4%, down from 7.6% in the same quarter last year

- Sales Volumes fell 2.2% year on year, in line with the same quarter last year

- Market Capitalization: $2.47 billion

Company Overview

With Wonder Bread as its premier brand, Flower Foods (NYSE:FLO) is a packaged foods company that focuses on bakery products such as breads, buns, and cakes.

The company traces its roots back to 1919, when brothers William Howard and Joseph Hampton Flowers commenced their operations with a single bakery and initially sold fresh bread directly to customers from a horse-drawn wagon. The company subsequently grew through organic means as well as through acquisitions, with the 2013 acquisition of Wonder Bread from Hostess as a notable one

Today, some notable products include Nature’s Own Whole Wheat and Honey Wheat Bread, Dave’s Killer Bread, Tastykake cupcakes and donuts, and Mrs. Freshley’s brownies and cakes. Flowers Foods’ core customer is the everyday American household. From the parent packing school lunches to the college student looking for a quick snack, their products have widespread appeal. Recognizing the evolving dietary needs and preferences of consumers, Flowers Foods has diversified its product range, including healthier bread options and organic choices.

The company’s baked goods can be found in many locations selling food and snacks. Wonder Bread and Flower Foods’ other brands are available in supermarkets, convenience stores, and mass retailers. Additionally, a significant portion of their products are sold to foodservice and vending companies.

4. Perishable Food

The perishable food industry is diverse, encompassing large-scale producers and distributors to specialty and artisanal brands. These companies sell produce, dairy products, meats, and baked goods and have become integral to serving modern American consumers who prioritize freshness, quality, and nutritional value. Investing in perishable food stocks presents both opportunities and challenges. While the perishable nature of products can introduce risks related to supply chain management and shelf life, it also creates a constant demand driven by the necessity for fresh food. Companies that can efficiently manage inventory, distribution, and quality control are well-positioned to thrive in this competitive market. Navigating the perishable food industry requires adherence to strict food safety standards, regulations, and labeling requirements.

Competitors in packaged bakery goods include Grupo Bimbo (BMV:BIMBO A), Hostess Brands, acquired by J.M. Smucker (NYSE:SJM), and Pepperidge Farm, a subsidiary of Campbell Soup (NYSE:CPB).

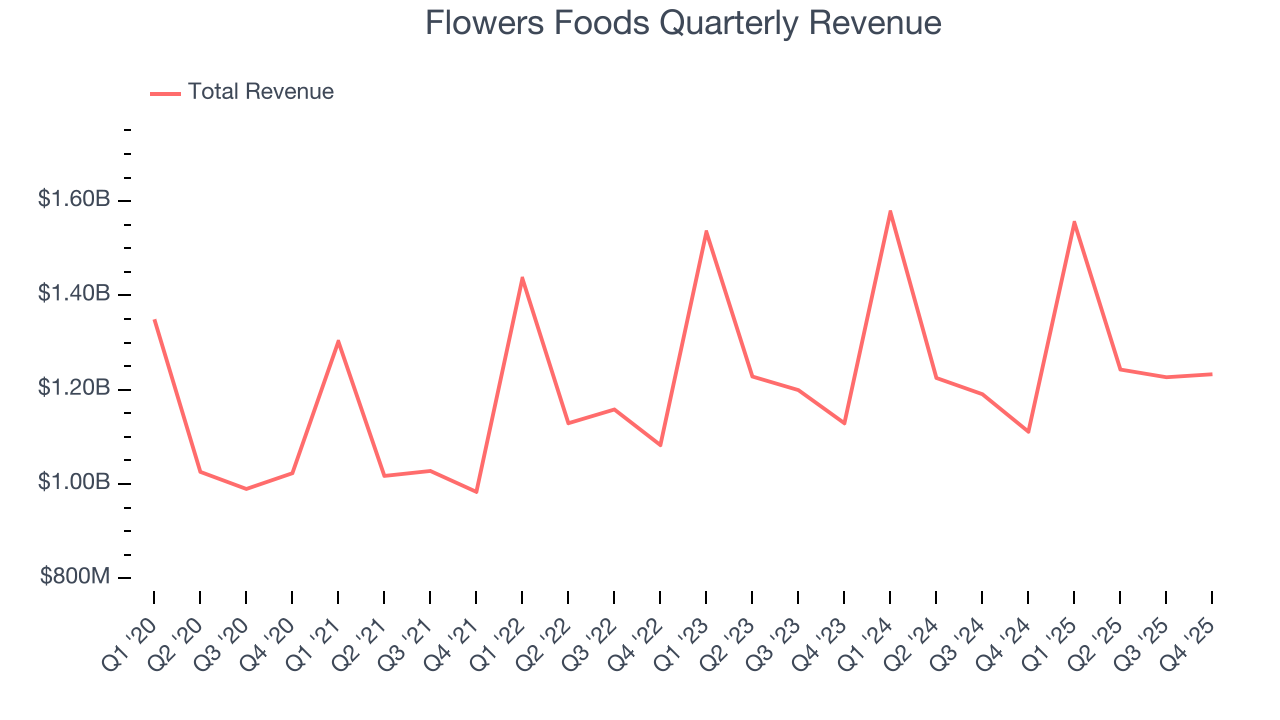

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $5.26 billion in revenue over the past 12 months, Flowers Foods carries some recognizable products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, Flowers Foods grew its sales at a sluggish 3% compounded annual growth rate over the last three years as consumers bought less of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, Flowers Foods’s year-on-year revenue growth was 11%, and its $1.23 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and implies its products will see some demand headwinds.

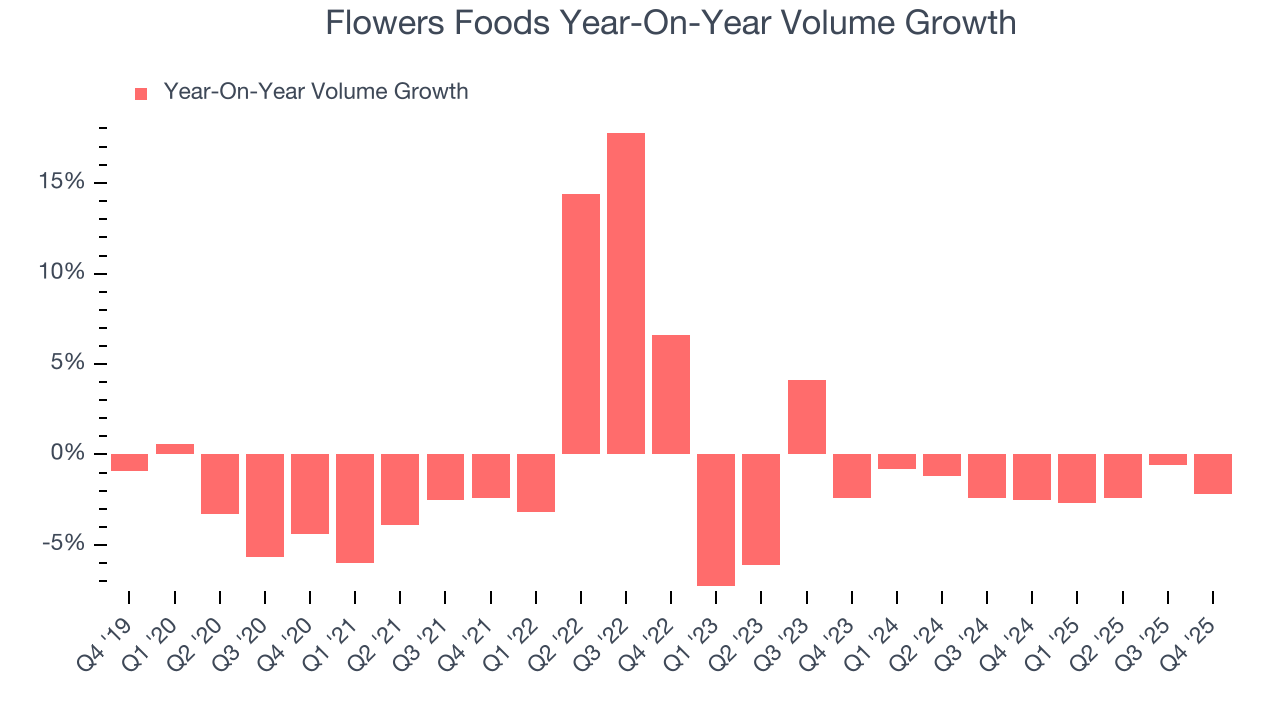

6. Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Flowers Foods’s average quarterly sales volumes have shrunk by 1.9% over the last two years. This decrease isn’t ideal because the quantity demanded for consumer staples products is typically stable.

In Flowers Foods’s Q4 2025, sales volumes dropped 2.2% year on year. This result represents a further deceleration from its historical levels, showing the business is struggling to move its products.

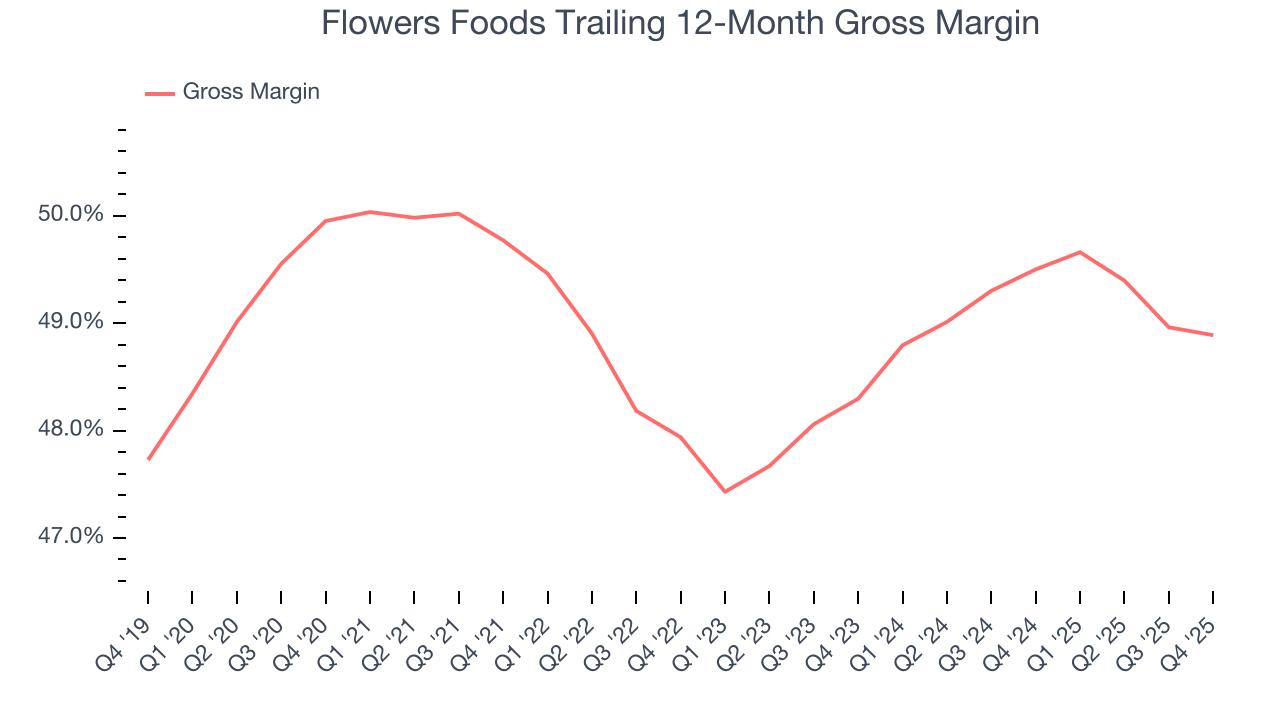

7. Gross Margin & Pricing Power

Flowers Foods has great unit economics for a consumer staples company, giving it ample room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an excellent 49.2% gross margin over the last two years. That means for every $100 in revenue, only $50.81 went towards paying for raw materials, production of goods, transportation, and distribution.

This quarter, Flowers Foods’s gross profit margin was 48.5%, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

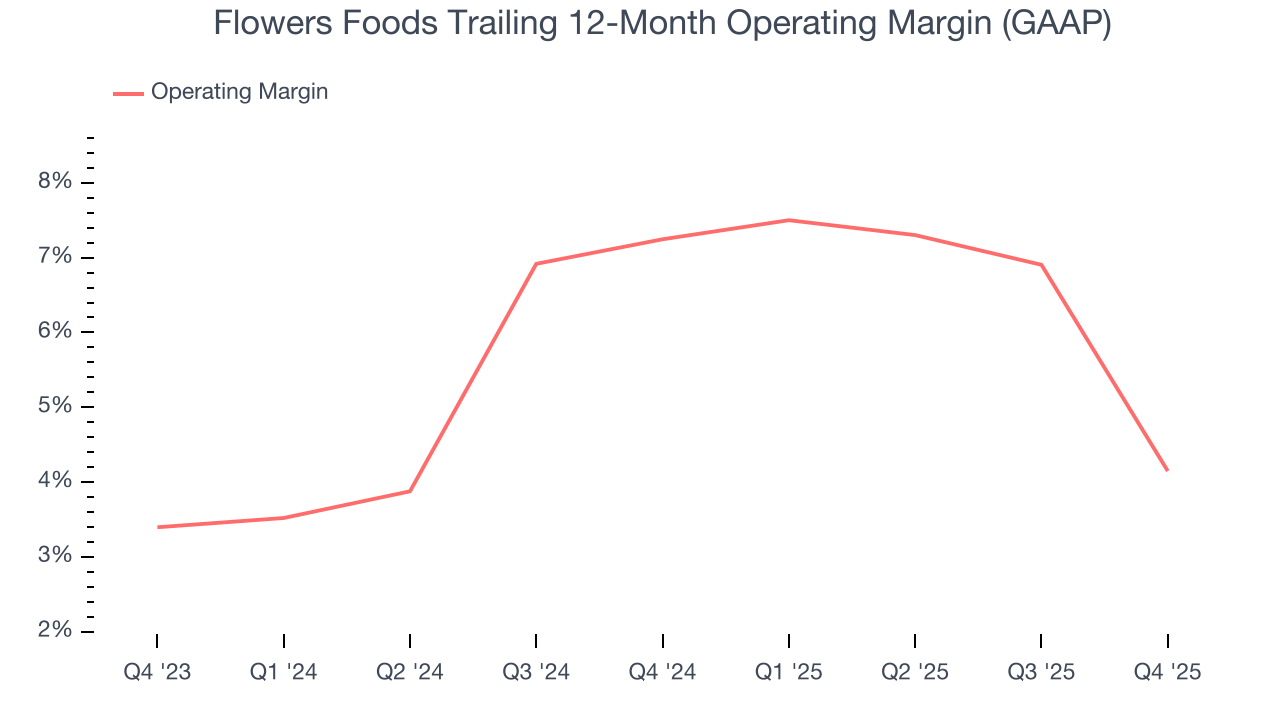

8. Operating Margin

Flowers Foods was profitable over the last two years but held back by its large cost base. Its average operating margin of 5.7% was weak for a consumer staples business. This result is surprising given its high gross margin as a starting point.

Analyzing the trend in its profitability, Flowers Foods’s operating margin decreased by 3.1 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Flowers Foods’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Flowers Foods generated an operating margin profit margin of negative 5.8%, down 11.7 percentage points year on year. Since Flowers Foods’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, and administrative overhead increased.

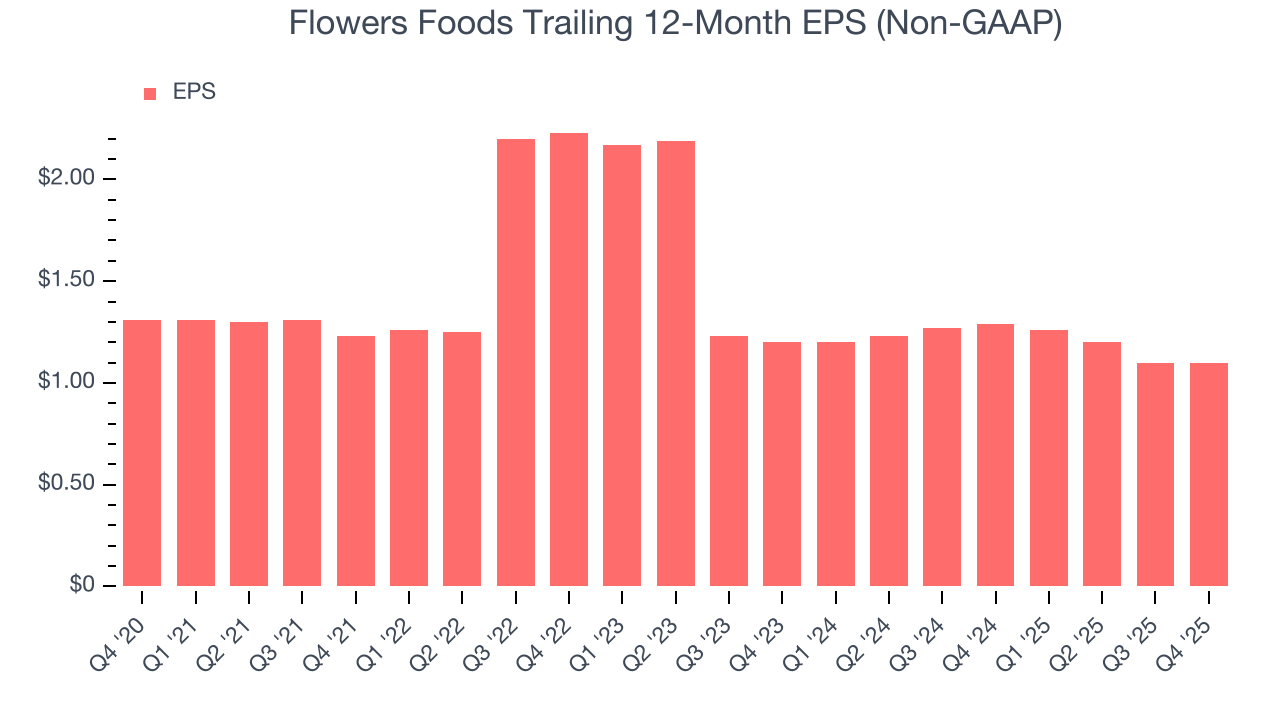

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Flowers Foods, its EPS declined by 21% annually over the last three years while its revenue grew by 3%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Flowers Foods reported adjusted EPS of $0.22, in line with the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Flowers Foods’s full-year EPS of $1.10 to shrink by 11.7%.

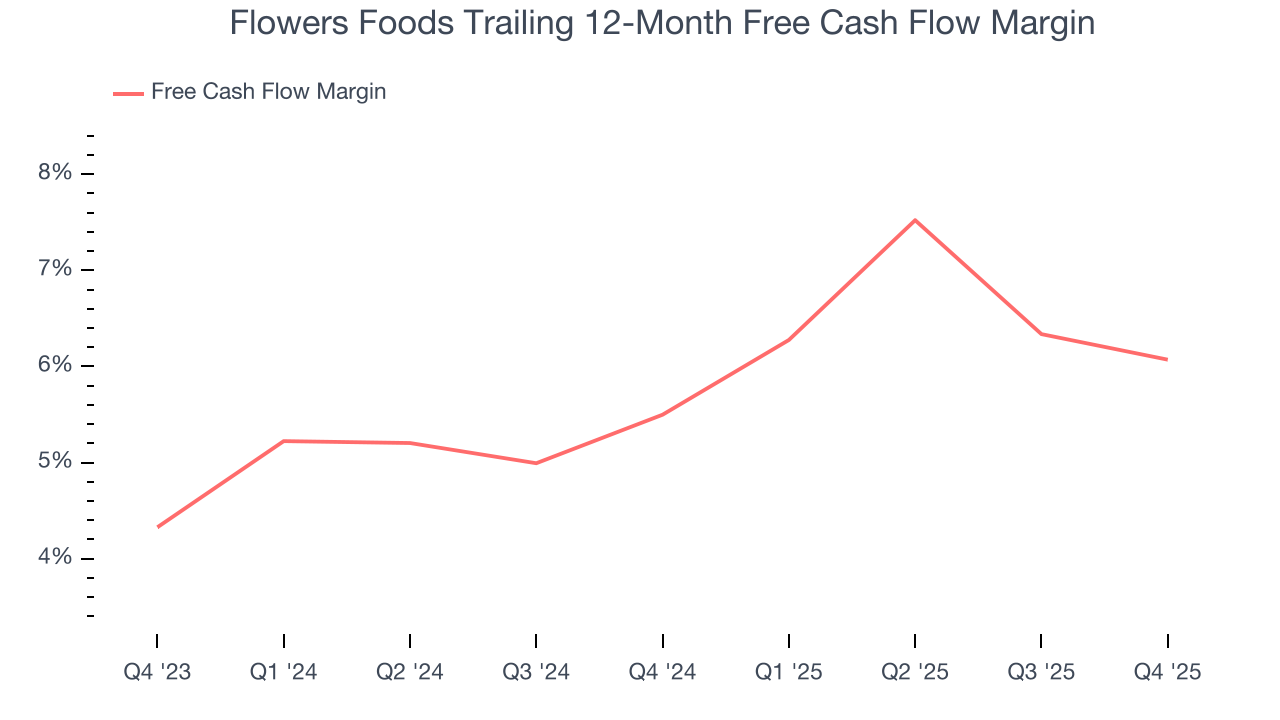

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Flowers Foods has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.8% over the last two years, slightly better than the broader consumer staples sector.

Flowers Foods’s free cash flow clocked in at $78.57 million in Q4, equivalent to a 6.4% margin. The company’s cash profitability regressed as it was 1.3 percentage points lower than in the same quarter last year. This warrants extra attention because consumer staples companies typically produce more consistent and defensive performance.

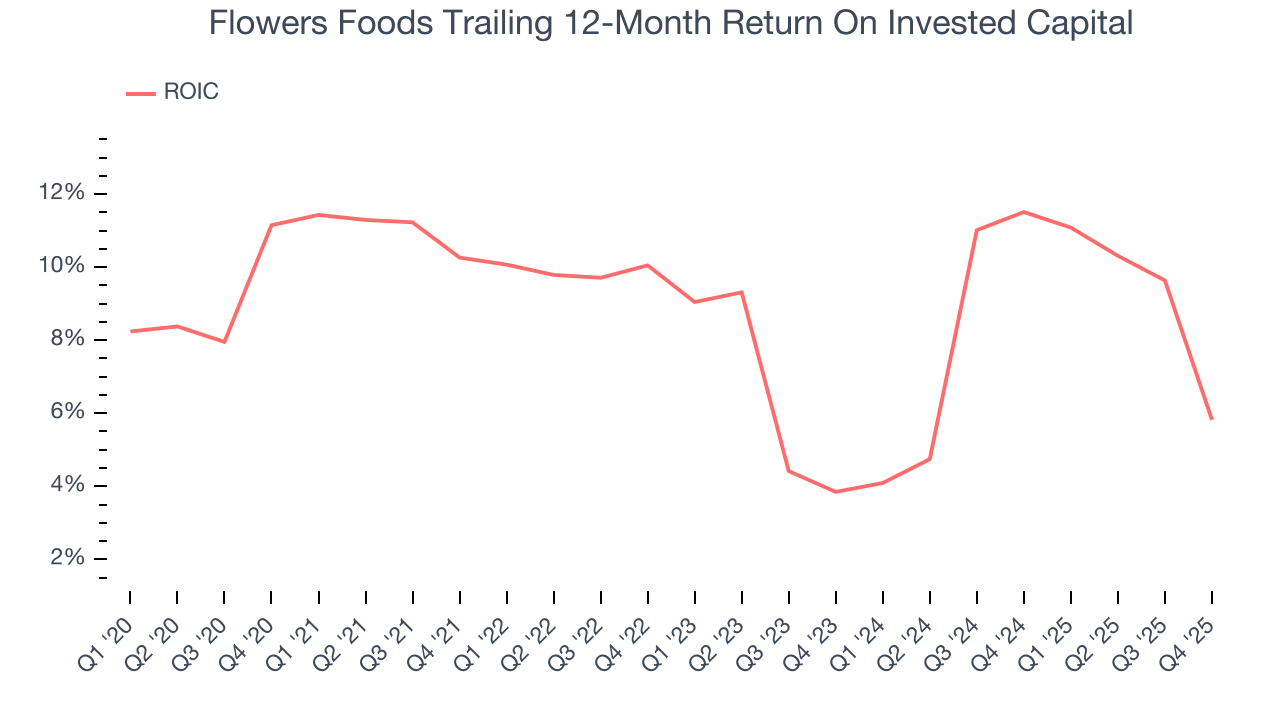

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Flowers Foods historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.3%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+.

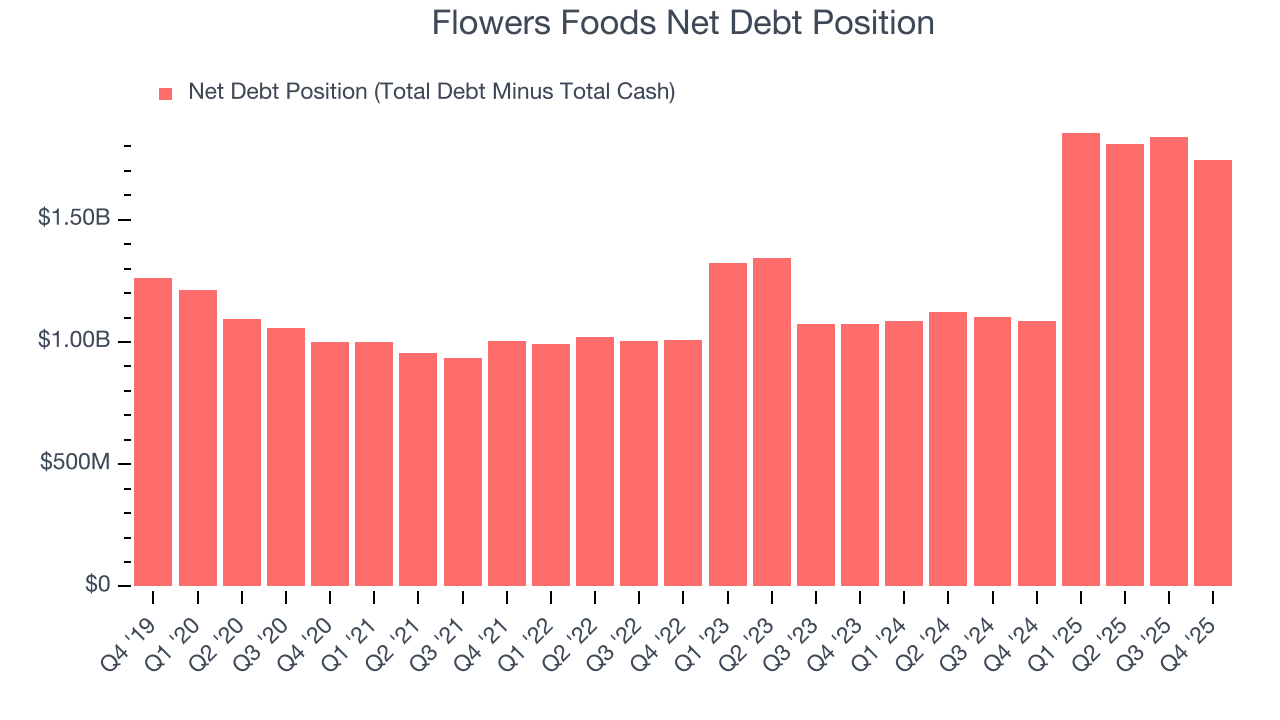

12. Balance Sheet Assessment

Flowers Foods reported $12.1 million of cash and $1.76 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $535.2 million of EBITDA over the last 12 months, we view Flowers Foods’s 3.3× net-debt-to-EBITDA ratio as safe. We also see its $27.78 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Flowers Foods’s Q4 Results

It was good to see Flowers Foods beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EBITDA guidance missed. Overall, this print had some key positives. The market seemed to be hoping for more, and the stock traded down 7.4% to $10.51 immediately following the results.

14. Is Now The Time To Buy Flowers Foods?

Updated: March 22, 2026 at 10:41 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Flowers Foods.

We cheer for all companies serving everyday consumers, but in the case of Flowers Foods, we’ll be cheering from the sidelines. First off, its revenue growth was uninspiring over the last three years, and analysts expect its demand to deteriorate over the next 12 months. While its gross margins are a strong starting point for the overall profitability of the business, the downside is its declining EPS over the last three years makes it a less attractive asset to the public markets. On top of that, its projected EPS for the next year is lacking.

Flowers Foods’s P/E ratio based on the next 12 months is 10x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $11.33 on the company (compared to the current share price of $8.24).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.