Maximus (MMS)

Maximus catches our eye. Its eye-popping 16.8% annualized EPS growth over the last five years has significantly outpaced its peers.― StockStory Analyst Team

1. News

2. Summary

Why Maximus Is Interesting

With nearly 50 years of experience translating public policy into operational programs that serve millions of citizens, Maximus (NYSE:MMS) provides operational services, clinical assessments, and technology solutions to government agencies in the U.S. and internationally.

- Earnings per share grew by 16.8% annually over the last five years and trumped its peers

- Economies of scale give it more fixed cost leverage than its smaller competitors

- A drawback is its estimated sales growth of 1.7% for the next 12 months implies demand will slow from its two-year trend

Maximus shows some potential. If you like the stock, the price seems reasonable.

3. Maximus (MMS) Research Report: Q4 CY2025 Update

Government services provider Maximus (NYSE:MMS) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 4.1% year on year to $1.35 billion. The company’s full-year revenue guidance of $5.28 billion at the midpoint came in 3.6% below analysts’ estimates. Its non-GAAP profit of $1.85 per share was 1.6% above analysts’ consensus estimates.

Maximus (MMS) Q4 CY2025 Highlights:

- Revenue: $1.35 billion vs analyst estimates of $1.37 billion (4.1% year-on-year decline, 2.2% miss)

- Adjusted EPS: $1.85 vs analyst estimates of $1.82 (1.6% beat)

- Adjusted EBITDA: $170.4 million vs analyst estimates of $172.4 million (12.7% margin, 1.2% miss)

- The company dropped its revenue guidance for the full year to $5.28 billion at the midpoint from $5.33 billion, a 0.9% decrease

- Management raised its full-year Adjusted EPS guidance to $8.20 at the midpoint, a 1.2% increase

- EBITDA guidance for the full year is $738 million at the midpoint, in line with analyst expectations

- Operating Margin: 10.9%, up from 6.2% in the same quarter last year

- Free Cash Flow was -$250.7 million compared to -$103 million in the same quarter last year

- Market Capitalization: $5.11 billion

Company Overview

With nearly 50 years of experience translating public policy into operational programs that serve millions of citizens, Maximus (NYSE:MMS) provides operational services, clinical assessments, and technology solutions to government agencies in the U.S. and internationally.

Maximus operates through three segments: U.S. Federal Services, U.S. Services, and Outside the U.S. The company manages large-scale government programs including healthcare enrollment, benefits administration, and clinical assessments. About half of its revenue comes from U.S. federal agencies, with state governments accounting for another third.

In its U.S. Federal Services segment, Maximus operates contact centers for Medicare and the federal health insurance marketplace, handles student loan servicing under the Aidvantage brand, and conducts medical disability examinations for veterans. For example, when a veteran needs to have their disability status evaluated, Maximus manages the clinical assessment process on behalf of the Department of Veterans Affairs.

The U.S. Services segment focuses on state-level programs, particularly Medicaid eligibility and enrollment services. The company also performs clinical assessments to determine eligibility for long-term care services and provides employment services that help welfare recipients transition to sustainable employment.

Internationally, Maximus delivers similar services, including employment programs and health assessments in countries like the United Kingdom and Australia. For instance, in the UK, the company conducts functional assessments for disability benefits under contract with the Department for Work and Pensions.

Maximus generates revenue primarily through performance-based contracts where payment depends on transaction volume or achieving specific outcomes. The company has been expanding its technology capabilities, offering services in application development, cybersecurity, and advanced analytics to help government agencies modernize their systems and improve service delivery.

4. Government & Technical Consulting

The sector has historically benefitted from steady government spending on defense, infrastructure, and regulatory compliance, providing firms long-term contract stability. However, the Trump administration is showing more willingness than previous administrations to upend government spending and bloat. Whether or not defense budgets get cut, the rising demand for cybersecurity, AI-driven defense solutions, and sustainability consulting should benefit the sector for years, as agencies and enterprises seek expertise in navigating complex technology and regulations. Additionally, industrial automation and digital engineering are driving efficiency gains in infrastructure and technical consulting projects, which could help profit margins.

Maximus competes with government insourced operations and other service providers including General Dynamics Information Technology, Deloitte, Leidos, Accenture, Booz Allen Hamilton, and Conduent. In international markets, competitors include Serco, Capita, and Atos.

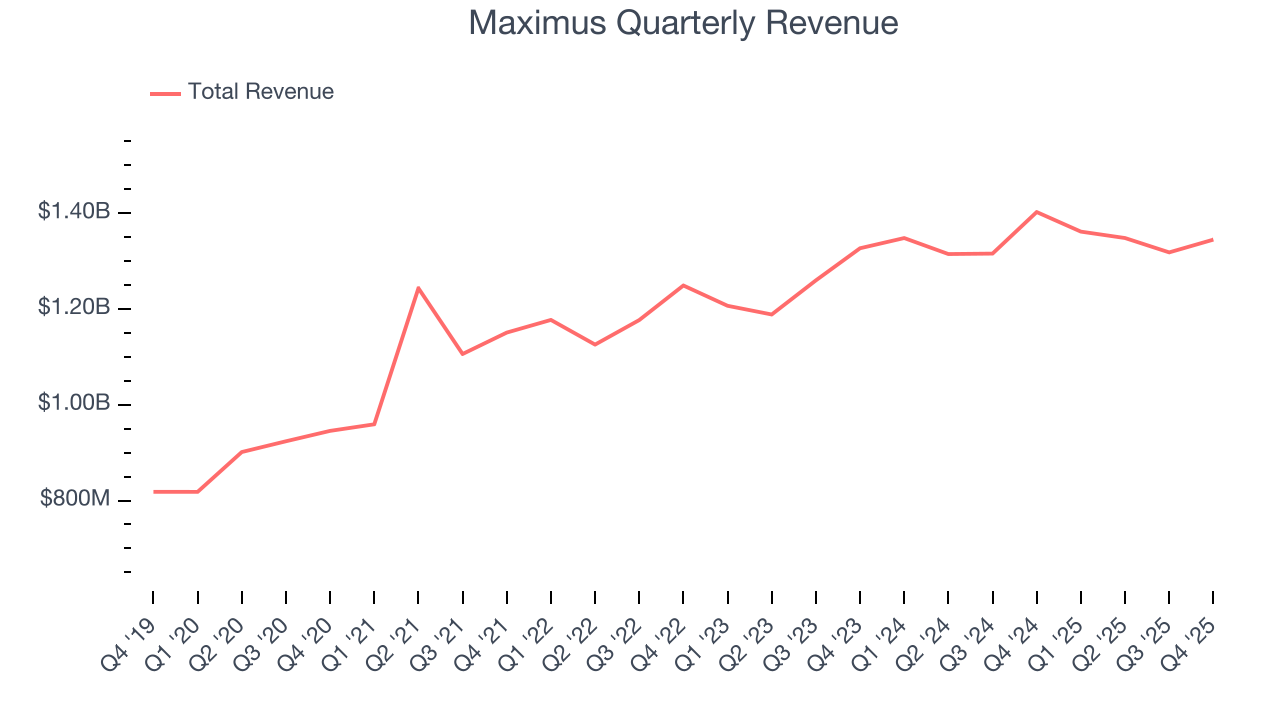

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $5.37 billion in revenue over the past 12 months, Maximus is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

As you can see below, Maximus’s sales grew at a solid 8.4% compounded annual growth rate over the last five years. This is an encouraging starting point for our analysis because it shows Maximus’s demand was higher than many business services companies.

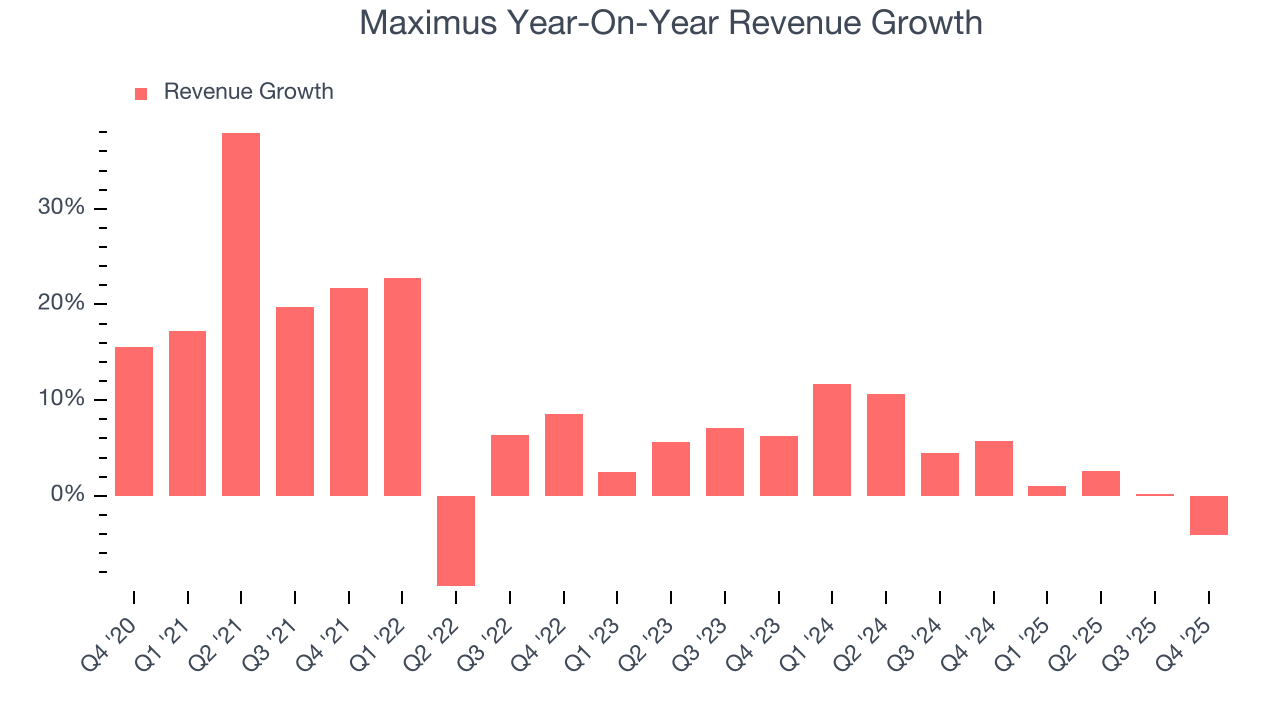

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Maximus’s recent performance shows its demand has slowed as its annualized revenue growth of 3.9% over the last two years was below its five-year trend.

This quarter, Maximus missed Wall Street’s estimates and reported a rather uninspiring 4.1% year-on-year revenue decline, generating $1.35 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.9% over the next 12 months, similar to its two-year rate. This projection is underwhelming and implies its newer products and services will not accelerate its top-line performance yet. At least the company is tracking well in other measures of financial health.

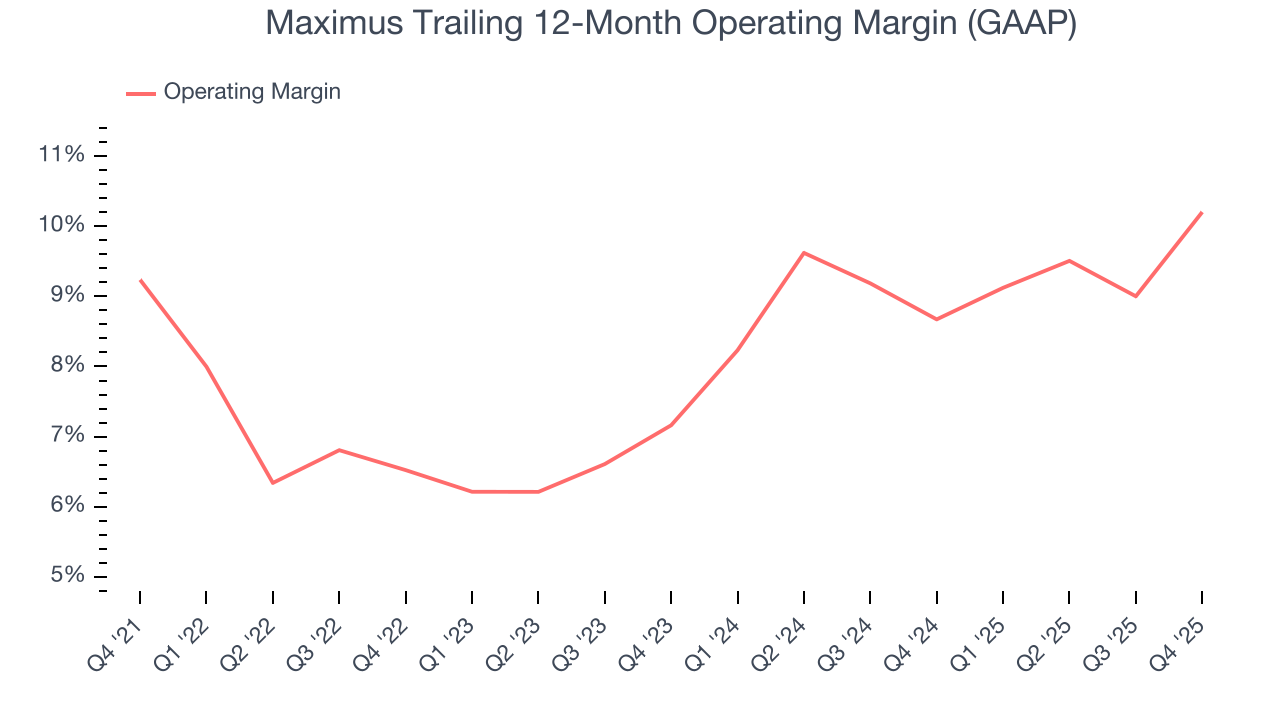

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Maximus’s operating margin has risen over the last 12 months and averaged 8.4% over the last five years. Although its profitability is still mediocre, we can see its solid revenue growth is giving it operating leverage as it scales. This gives it a shot at higher long-term profits if it can keep expanding.

Analyzing the trend in its profitability, Maximus’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Maximus generated an operating margin profit margin of 10.9%, up 4.7 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

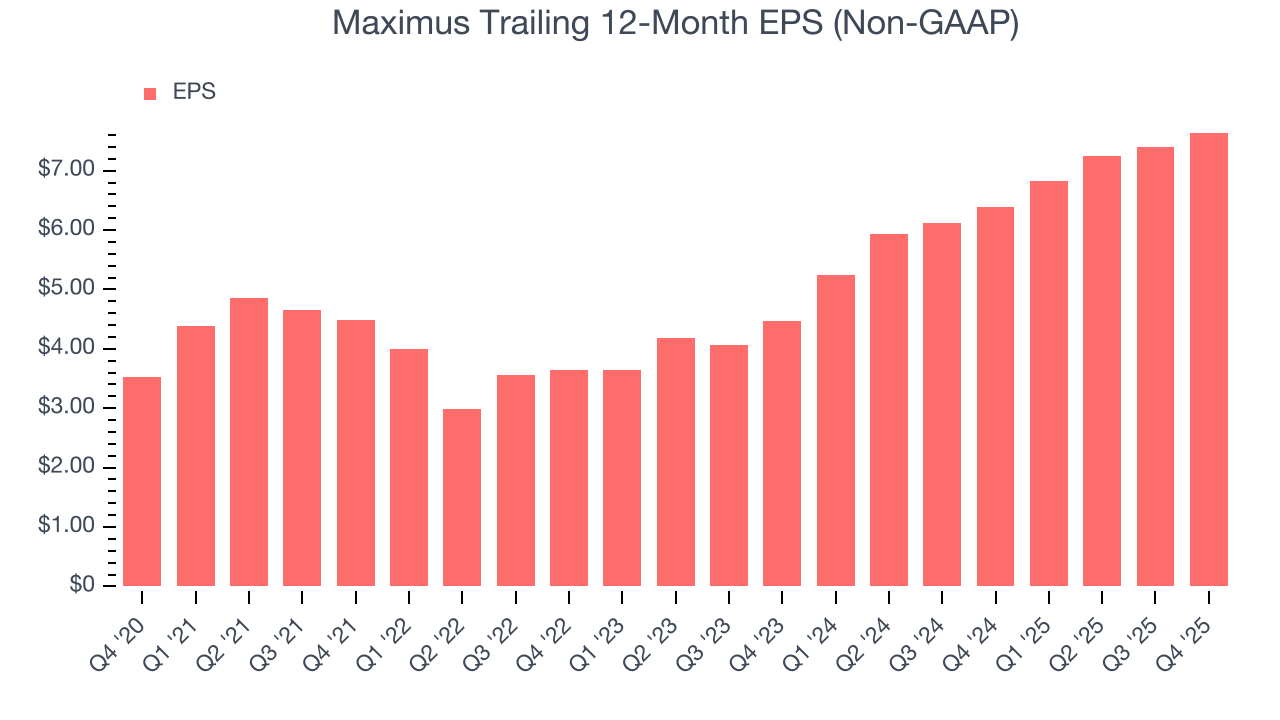

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Maximus’s EPS grew at an astounding 16.8% compounded annual growth rate over the last five years, higher than its 8.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Maximus, its two-year annual EPS growth of 30.7% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Maximus reported adjusted EPS of $1.85, up from $1.61 in the same quarter last year. This print beat analysts’ estimates by 1.6%. Over the next 12 months, Wall Street expects Maximus’s full-year EPS of $7.64 to grow 12%.

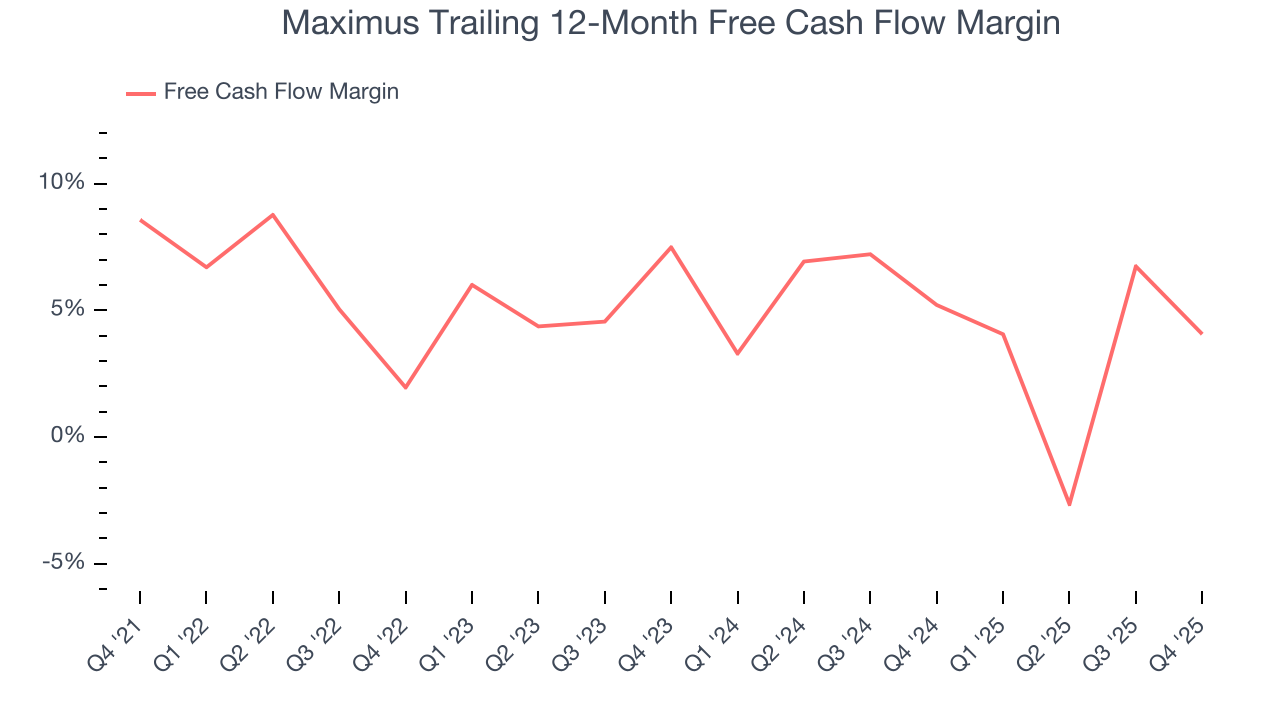

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Maximus has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.4% over the last five years, slightly better than the broader business services sector.

Taking a step back, we can see that Maximus’s margin dropped by 4.5 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Maximus burned through $250.7 million of cash in Q4, equivalent to a negative 18.6% margin. The company’s cash burn increased from $103 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings.

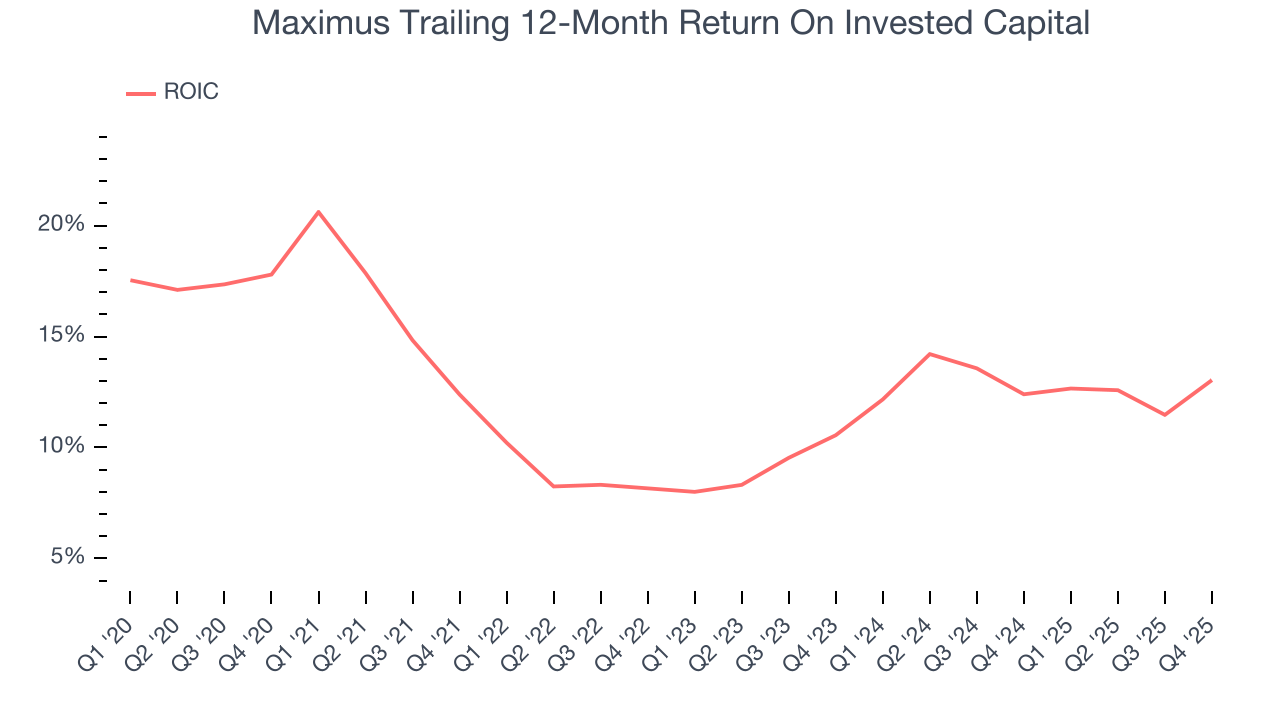

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Maximus’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 11.3%, slightly better than typical business services business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Maximus’s ROIC averaged 2.4 percentage point increases each year. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

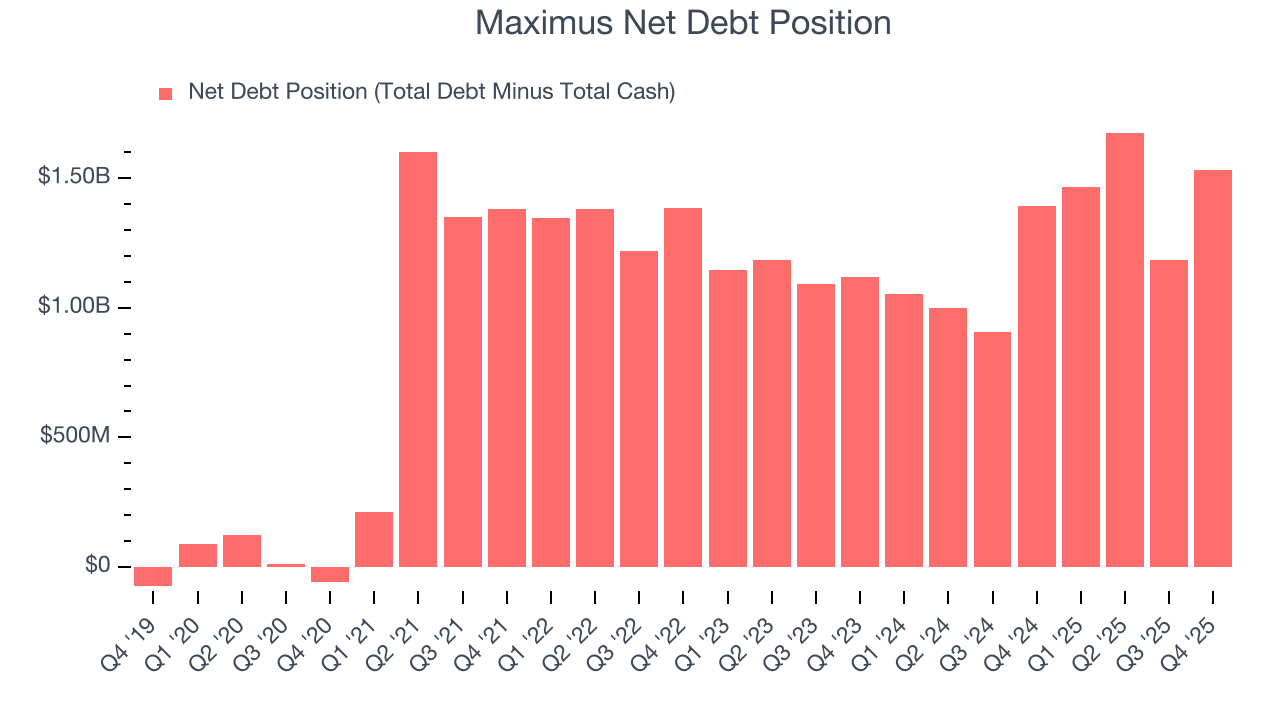

10. Balance Sheet Assessment

Maximus reported $137.6 million of cash and $1.67 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $715.4 million of EBITDA over the last 12 months, we view Maximus’s 2.1× net-debt-to-EBITDA ratio as safe. We also see its $45.74 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Maximus’s Q4 Results

It was good to see Maximus beat analysts’ EPS expectations this quarter. On the other hand, its full-year revenue guidance missed and its revenue fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $93.69 immediately following the results.

12. Is Now The Time To Buy Maximus?

Updated: March 15, 2026 at 12:13 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Maximus, you should also grasp the company’s longer-term business quality and valuation.

There are some positives when it comes to Maximus’s fundamentals. To kick things off, its revenue growth was solid over the last five years. And while its cash profitability fell over the last five years, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders. On top of that, its projected EPS for the next year implies the company’s fundamentals will improve.

Maximus’s P/E ratio based on the next 12 months is 8.1x. Looking at the business services space right now, Maximus trades at a compelling valuation. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $110 on the company (compared to the current share price of $72.42), implying they see 51.9% upside in buying Maximus in the short term.