Zeta Global (ZETA)

We admire Zeta Global. Its efficient sales engine has led to first-class growth, showing it can win market share organically.― StockStory Analyst Team

1. News

2. Summary

Why We Like Zeta Global

Powered by an AI engine that processes over one trillion consumer signals monthly, Zeta Global (NYSE:ZETA) operates a data-driven cloud platform that helps companies target, connect, and engage with consumers through personalized marketing across channels like email, social media, and video.

- Billings growth has averaged 31.5% over the last year, indicating a healthy pipeline of new contracts that should drive future revenue increases

- Notable projected revenue growth of 34.7% for the next 12 months hints at market share gains

- User-friendly software enables clients to ramp up spending quickly, leading to the speedy recovery of customer acquisition costs

Zeta Global is a market leader. The valuation seems reasonable relative to its quality, so this could be an opportune time to buy some shares.

Why Is Now The Time To Buy Zeta Global?

Zeta Global is trading at $17.93 per share, or 2.3x forward price-to-sales. This multiple is cheap, and we think the stock is a bargain considering its quality characteristics.

We jump for joy when high-quality companies trade at bargain prices because shareholders can benefit from both earnings growth and a positive re-rating - a powerful one-two punch.

3. Zeta Global (ZETA) Research Report: Q4 CY2025 Update

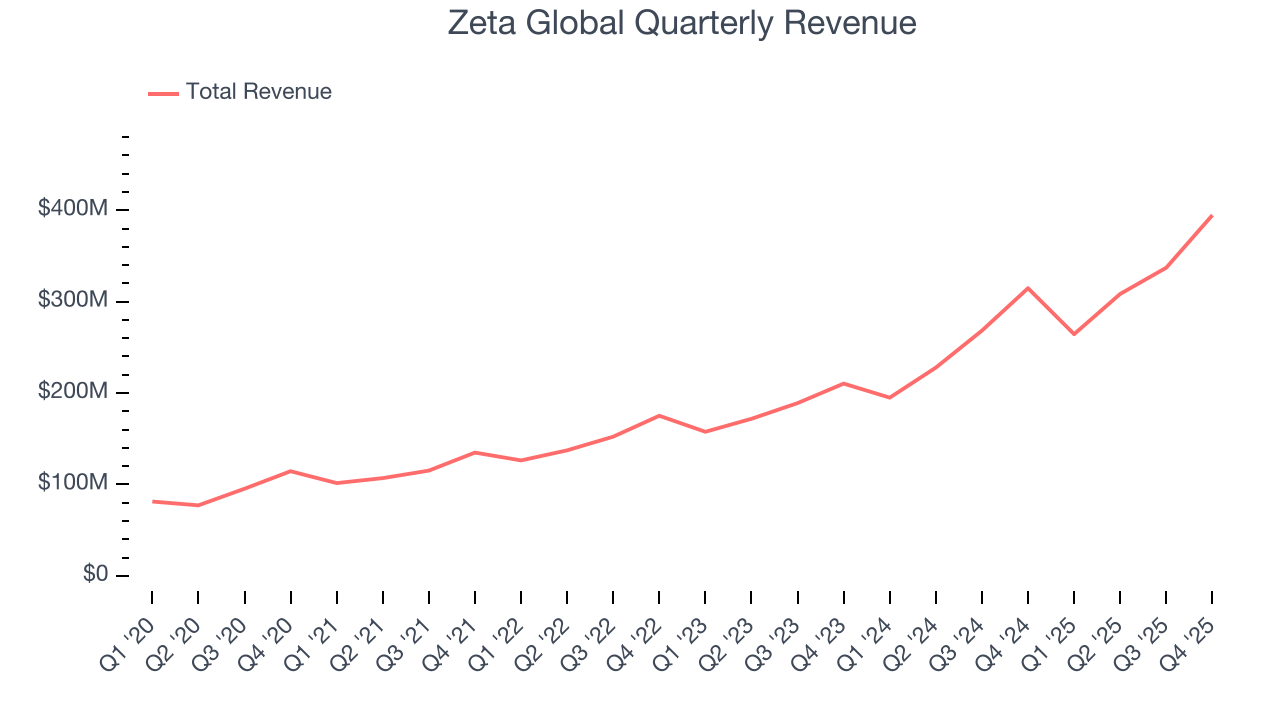

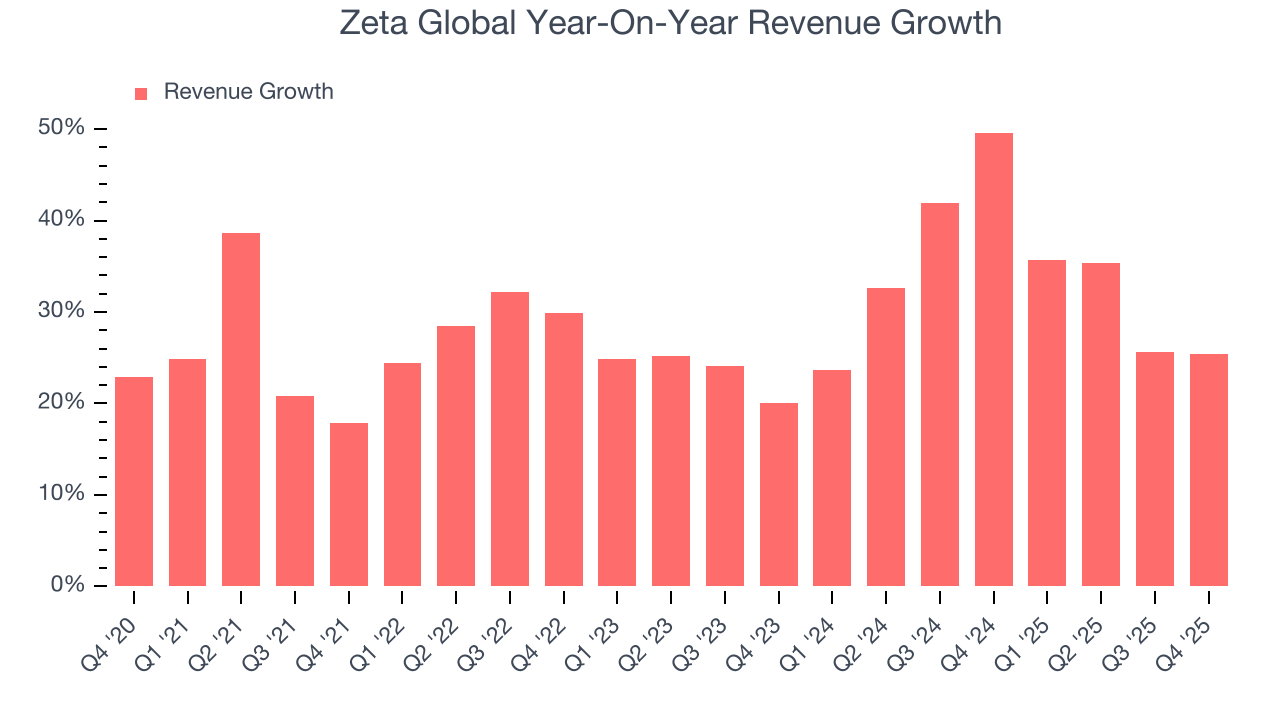

Marketing technology company Zeta Global (NYSE:ZETA) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 25.4% year on year to $394.6 million. Guidance for next quarter’s revenue was optimistic at $370 million at the midpoint, 2.1% above analysts’ estimates.

Zeta Global (ZETA) Q4 CY2025 Highlights:

- Revenue: $394.6 million vs analyst estimates of $380.6 million (25.4% year-on-year growth, 3.7% beat)

- Adjusted EBITDA: $95.13 million vs analyst estimates of $91.17 million (24.1% margin, 4.3% beat)

- Revenue Guidance for Q1 CY2026 is $370 million at the midpoint, above analyst estimates of $362.3 million

- EBITDA guidance for the upcoming financial year 2026 is $391 million at the midpoint, above analyst estimates of $382.8 million

- Operating Margin: 4.5%, up from 2.2% in the same quarter last year

- Free Cash Flow Margin: 14.2%, similar to the previous quarter

- Market Capitalization: $3.68 billion

Company Overview

Powered by an AI engine that processes over one trillion consumer signals monthly, Zeta Global (NYSE:ZETA) operates a data-driven cloud platform that helps companies target, connect, and engage with consumers through personalized marketing across channels like email, social media, and video.

The company's core product, the Zeta Marketing Platform (ZMP), combines three integrated components: a Customer Data Platform (CDP) that creates unified consumer profiles, an Email Service Provider (ESP) for messaging campaigns, and a Demand-Side Platform (DSP) for paid media activation. This integrated approach allows enterprises to leverage Zeta's extensive data assets - which include over 240 million opted-in individuals in the U.S. and 535 million globally, with approximately 2,500 attributes per person.

Zeta's proprietary artificial intelligence analyzes this data to identify consumer intent and create highly targeted marketing programs. For example, a retail company might use Zeta's platform to identify consumers showing purchase intent for specific products, deliver personalized email offers, and then retarget those same consumers with complementary products across social media and connected TV channels.

The company generates revenue through subscription-based access to its platform and usage-based fees tied to marketing campaign volume. Zeta serves customers across various industries, with particular strength in consumer retail, telecommunications, financial services, and insurance. The company emphasizes data privacy compliance as a core component of its operations, implementing technical measures to manage user consent parameters in accordance with evolving global regulations.

4. Advertising Software

The digital advertising market is large, growing, and becoming more diverse, both in terms of audiences and media. As a result, there is a growing need for software that enables advertisers to use data to automate and optimize ad placements.

Zeta Global competes with large marketing technology providers like Adobe (NASDAQ:ADBE) with its Experience Cloud, Salesforce (NYSE:CRM) with its Marketing Cloud, and Oracle (NYSE:ORCL) with its Marketing Cloud, as well as specialized marketing platforms like The Trade Desk (NASDAQ:TTD) and Integral Ad Science (NASDAQ:IAS).

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Zeta Global’s 28.8% annualized revenue growth over the last five years was impressive. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Zeta Global’s annualized revenue growth of 33.8% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Zeta Global reported robust year-on-year revenue growth of 25.4%, and its $394.6 million of revenue topped Wall Street estimates by 3.7%. Company management is currently guiding for a 39.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 32.6% over the next 12 months, similar to its two-year rate. Still, this projection is healthy and indicates the market is forecasting success for its products and services.

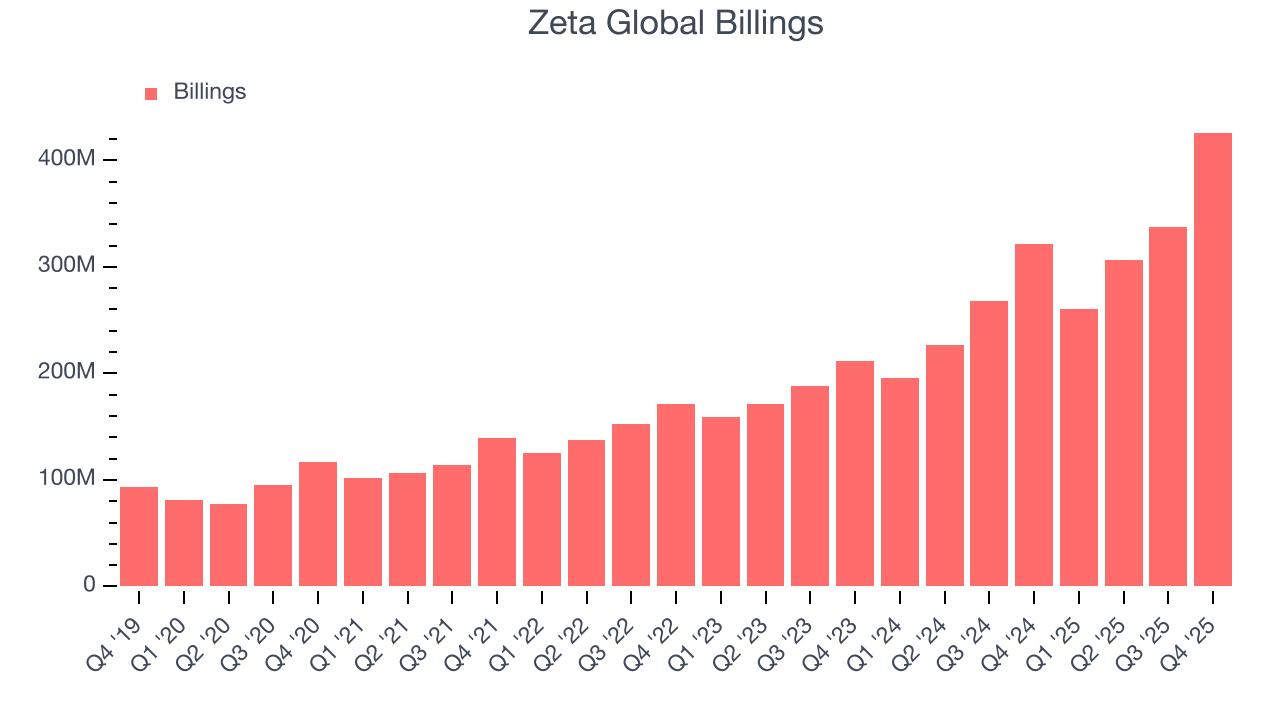

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Zeta Global’s billings punched in at $426 million in Q4, and over the last four quarters, its growth was fantastic as it averaged 31.5% year-on-year increases. This performance aligned with its total sales growth, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Zeta Global is extremely efficient at acquiring new customers, and its CAC payback period checked in at 5.6 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Zeta Global more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

8. Gross Margin & Pricing Power

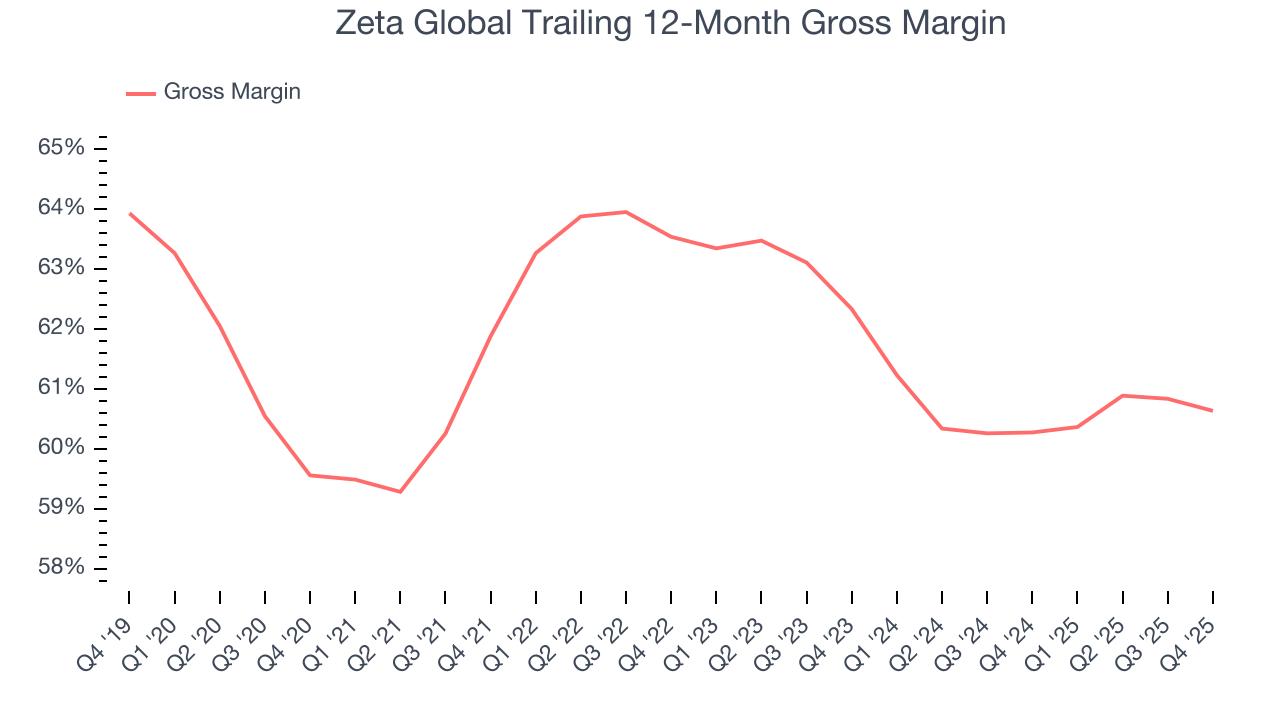

For software companies like Zeta Global, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Zeta Global’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 60.6% gross margin over the last year. Said differently, Zeta Global had to pay a chunky $39.37 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Zeta Global has seen gross margins decline by 1.7 percentage points over the last 2 year, which is poor compared to software peers.

Zeta Global’s gross profit margin came in at 59.5% this quarter, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

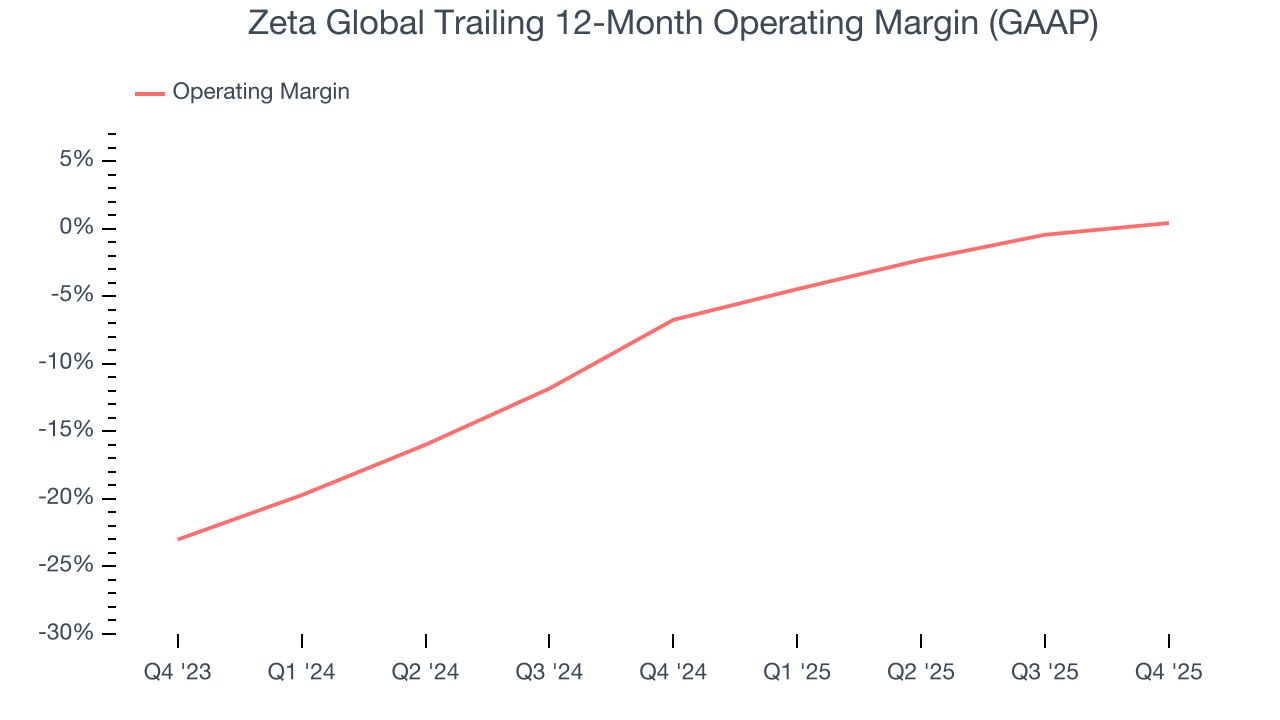

9. Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Zeta Global was roughly breakeven when averaging the last year of quarterly operating profits, decent for a software business.

Analyzing the trend in its profitability, Zeta Global’s operating margin rose by 7.2 percentage points over the last two years, as its sales growth gave it operating leverage.

This quarter, Zeta Global generated an operating margin profit margin of 4.5%, up 2.3 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

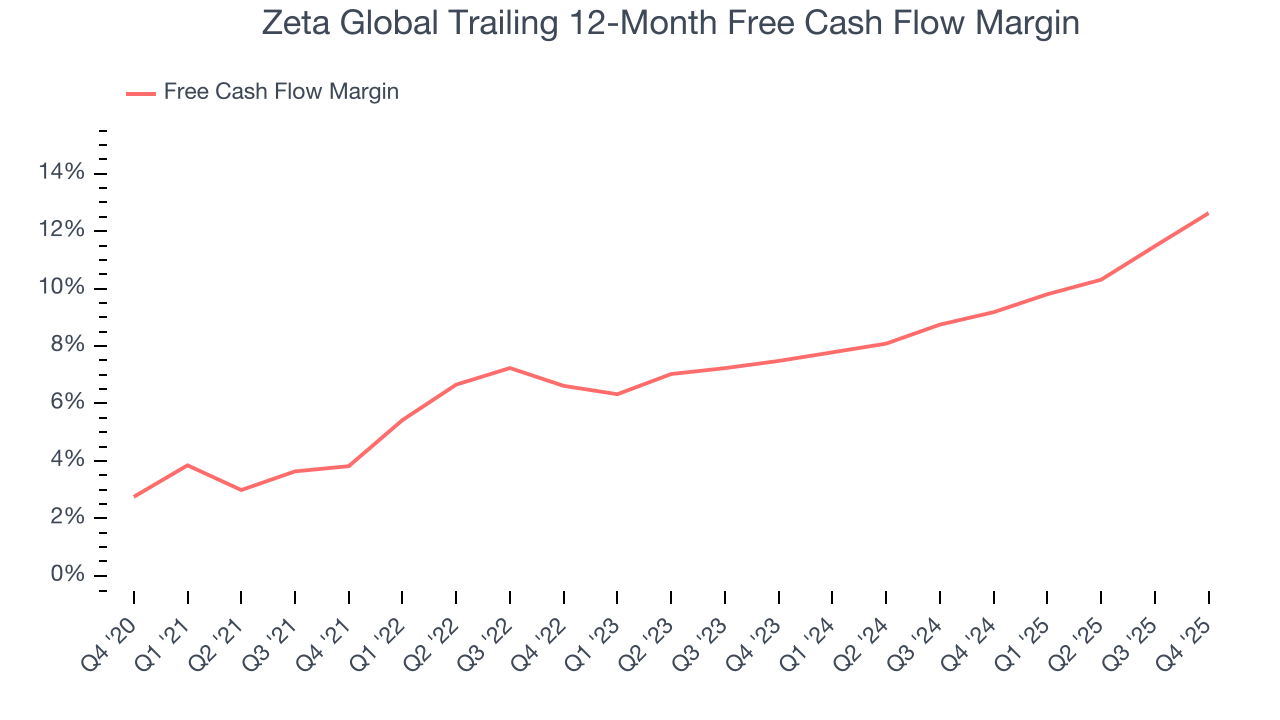

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Zeta Global has shown mediocre cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 12.6%, subpar for a software business.

Zeta Global’s free cash flow clocked in at $55.85 million in Q4, equivalent to a 14.2% margin. This result was good as its margin was 4.1 percentage points higher than in the same quarter last year. Its cash profitability was also above its one-year level, and we hope the company can build on this trend.

Over the next year, analysts’ consensus estimates show they’re expecting Zeta Global’s free cash flow margin of 12.6% for the last 12 months to remain the same.

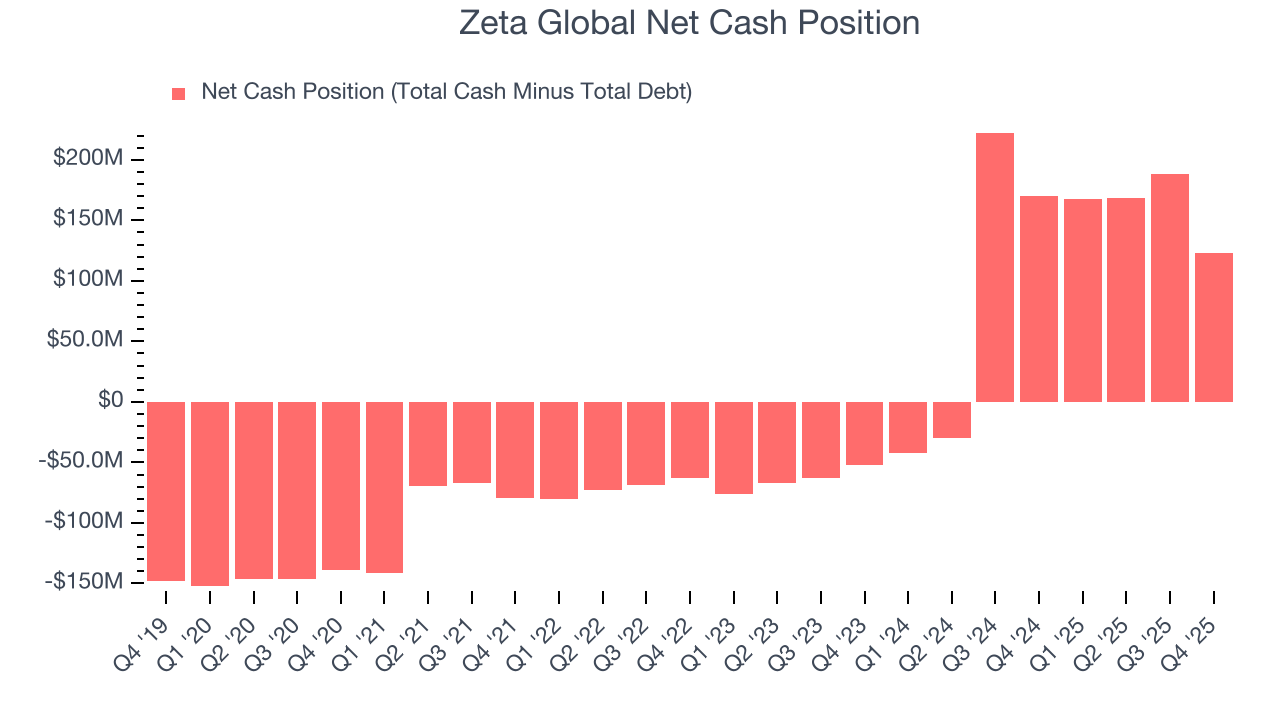

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Zeta Global is a profitable, well-capitalized company with $319.8 million of cash and $197.1 million of debt on its balance sheet. This $122.7 million net cash position is 3.3% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Zeta Global’s Q4 Results

It was great to see Zeta Global expecting revenue growth to accelerate next year. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 1.5% to $17.20 immediately after reporting.

13. Is Now The Time To Buy Zeta Global?

Updated: March 16, 2026 at 10:38 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Zeta Global.

There is a lot to like about Zeta Global. To begin with, its revenue growth was strong over the last five years, and its growth over the next 12 months is expected to accelerate. And while its gross margins show its business model is much less lucrative than other companies, its efficient sales strategy allows it to target and onboard new users at scale.

Zeta Global’s price-to-sales ratio based on the next 12 months is 2.3x. Analyzing the software landscape today, Zeta Global’s positive attributes shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $29.08 on the company (compared to the current share price of $17.93), implying they see 62.2% upside in buying Zeta Global in the short term.