Calavo (CVGW)

Calavo faces an uphill battle. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Calavo Will Underperform

A trailblazer in the avocado industry, Calavo Growers (NASDAQ:CVGW) is a pioneering California-based provider of high-quality avocados and other fresh food products.

- Products have few die-hard fans as sales have declined by 16.3% annually over the last three years

- Sales are projected to tank by 12.5% over the next 12 months as its demand continues evaporating

- Gross margin of 10.4% is an output of its commoditized products

Calavo’s quality doesn’t meet our bar. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than Calavo

At $23.61 per share, Calavo trades at 16.3x forward P/E. Calavo’s valuation may seem like a bargain, especially when stacked up against other consumer staples companies. We remind you that you often get what you pay for, though.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Calavo (CVGW) Research Report: Q4 CY2025 Update

Fresh produce company Calavo Growers (NASDAQ:CVGW) reported Q4 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 20.8% year on year to $122.2 million. Its non-GAAP profit of $0.27 per share was 25.6% above analysts’ consensus estimates.

Calavo (CVGW) Q4 CY2025 Highlights:

- Revenue: $122.2 million vs analyst estimates of $116.4 million (20.8% year-on-year decline, 5% beat)

- Adjusted EPS: $0.27 vs analyst estimates of $0.22 (25.6% beat)

- Adjusted EBITDA: $8.01 million vs analyst estimates of $7.45 million (6.6% margin, 7.5% beat)

- Operating Margin: -1.2%, down from 3.3% in the same quarter last year

- Market Capitalization: $449.7 million

Company Overview

A trailblazer in the avocado industry, Calavo Growers (NASDAQ:CVGW) is a pioneering California-based provider of high-quality avocados and other fresh food products.

The company's story began in 1924 when a group of farmers in the fertile region of Santa Paula, California formed a cooperative to market and distribute avocados. Their goal was to raise awareness and create a thriving market for this then-unfamiliar fruit among Americans.

Through innovative marketing campaigns and efforts to educate the public on the culinary uses and health benefits of avocados, Calavo Growers played a pivotal role in its integration into American cuisine. Today, avocados have become a staple ingredient in countless dishes and are celebrated for their nutritional benefits.

While avocados lie at the heart of Calavo Growers's business, its product portfolio extends far beyond. The company offers a diverse array of fresh foods, including tomatoes, papayas, pineapples, and pre-packaged guacamole. This diversification allows it to serve the evolving needs and tastes of consumers, making it a versatile player in the fresh produce industry.

Calavo Growers operates across North America, Mexico, and other international markets, and its extensive distribution network ensures products are readily available in grocery stores, restaurants, and food service establishments.

4. Perishable Food

The perishable food industry is diverse, encompassing large-scale producers and distributors to specialty and artisanal brands. These companies sell produce, dairy products, meats, and baked goods and have become integral to serving modern American consumers who prioritize freshness, quality, and nutritional value. Investing in perishable food stocks presents both opportunities and challenges. While the perishable nature of products can introduce risks related to supply chain management and shelf life, it also creates a constant demand driven by the necessity for fresh food. Companies that can efficiently manage inventory, distribution, and quality control are well-positioned to thrive in this competitive market. Navigating the perishable food industry requires adherence to strict food safety standards, regulations, and labeling requirements.

Competitors in the fresh produce category include Dole (NYSE:DOLE), Fresh Del Monte (NYSE:FDP), and Mission Produce (NASDAQ:AVO) along with private companies Chiquita Brands International and Sunkist Growers.

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

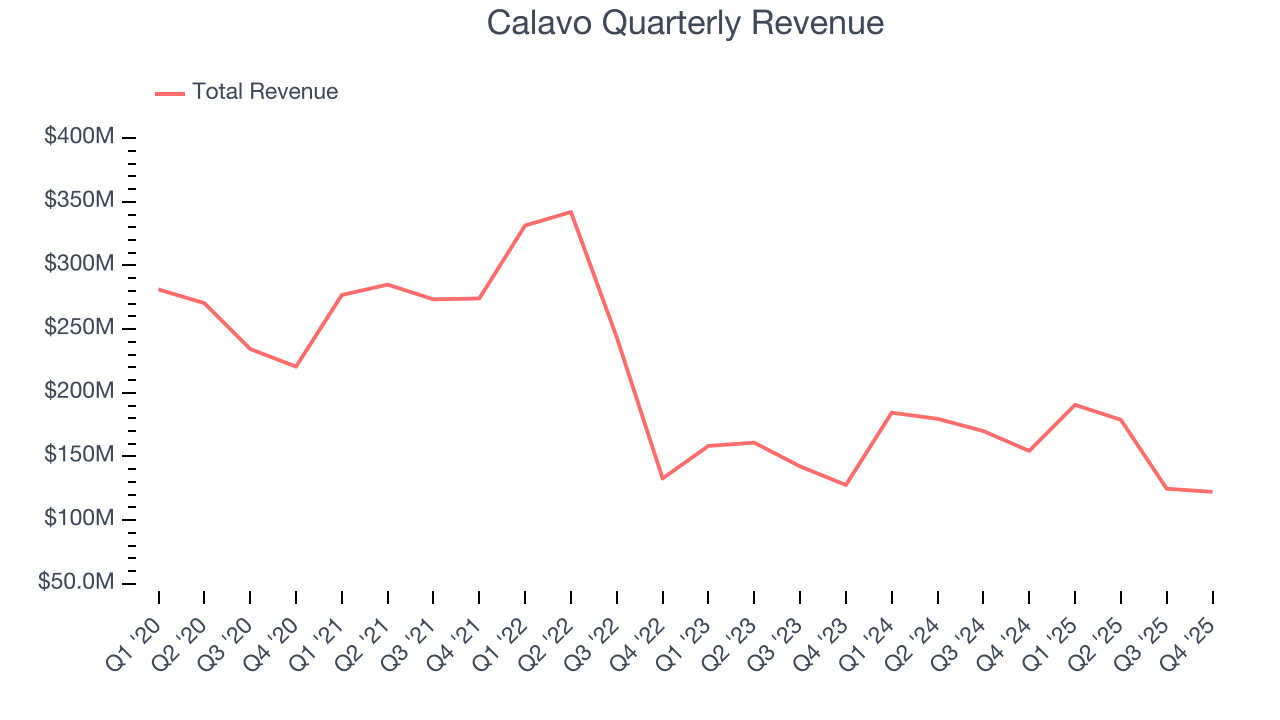

With $616.3 million in revenue over the past 12 months, Calavo is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Calavo’s revenue declined by 16.3% per year over the last three years, a poor baseline for our analysis.

This quarter, Calavo’s revenue fell by 20.8% year on year to $122.2 million but beat Wall Street’s estimates by 5%.

Looking ahead, sell-side analysts expect revenue to decline by 12.5% over the next 12 months. it’s tough to feel optimistic about a company facing demand difficulties.

6. Gross Margin & Pricing Power

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

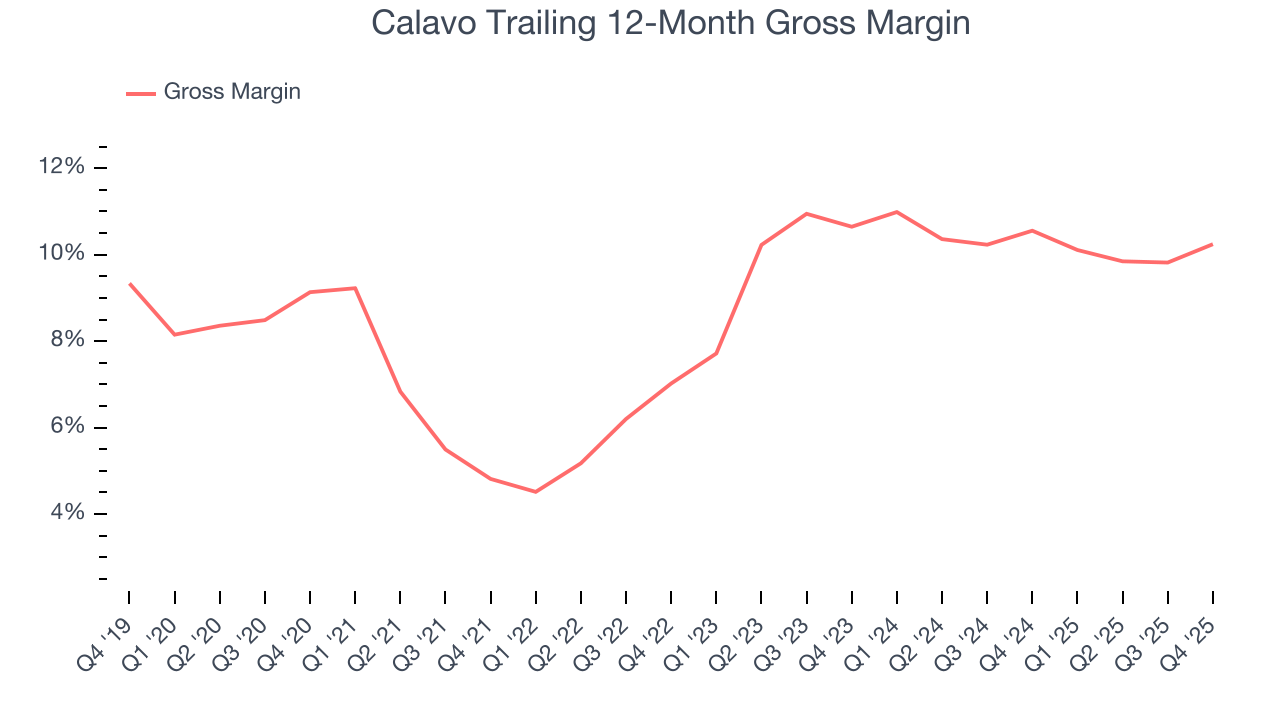

Calavo has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 10.4% gross margin over the last two years. That means Calavo paid its suppliers a lot of money ($89.59 for every $100 in revenue) to run its business.

Calavo’s gross profit margin came in at 12.4% this quarter, up 2.2 percentage points year on year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

7. Operating Margin

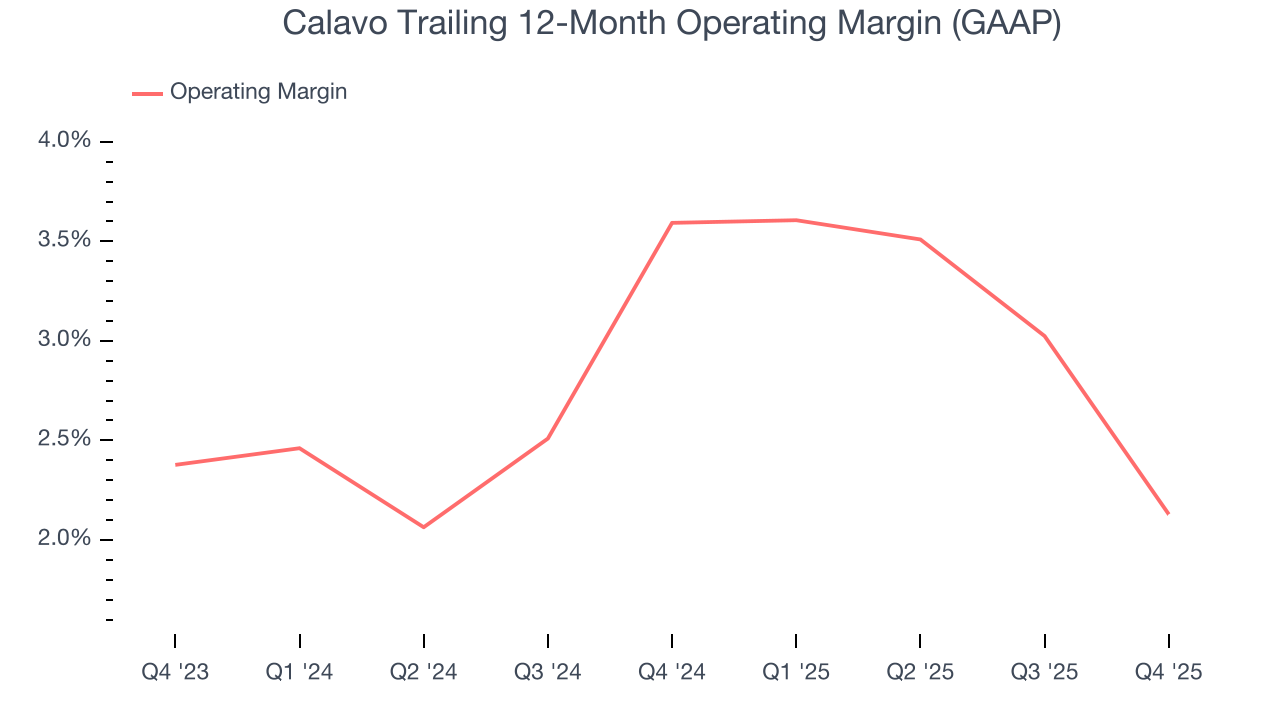

Calavo was profitable over the last two years but held back by its large cost base. Its average operating margin of 2.9% was weak for a consumer staples business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Calavo’s operating margin decreased by 1.5 percentage points over the last year. Calavo’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Calavo generated an operating margin profit margin of negative 1.2%, down 4.5 percentage points year on year. Conversely, its gross margin actually rose, so we can assume its recent inefficiencies were driven by increased operating expenses like marketing, and administrative overhead.

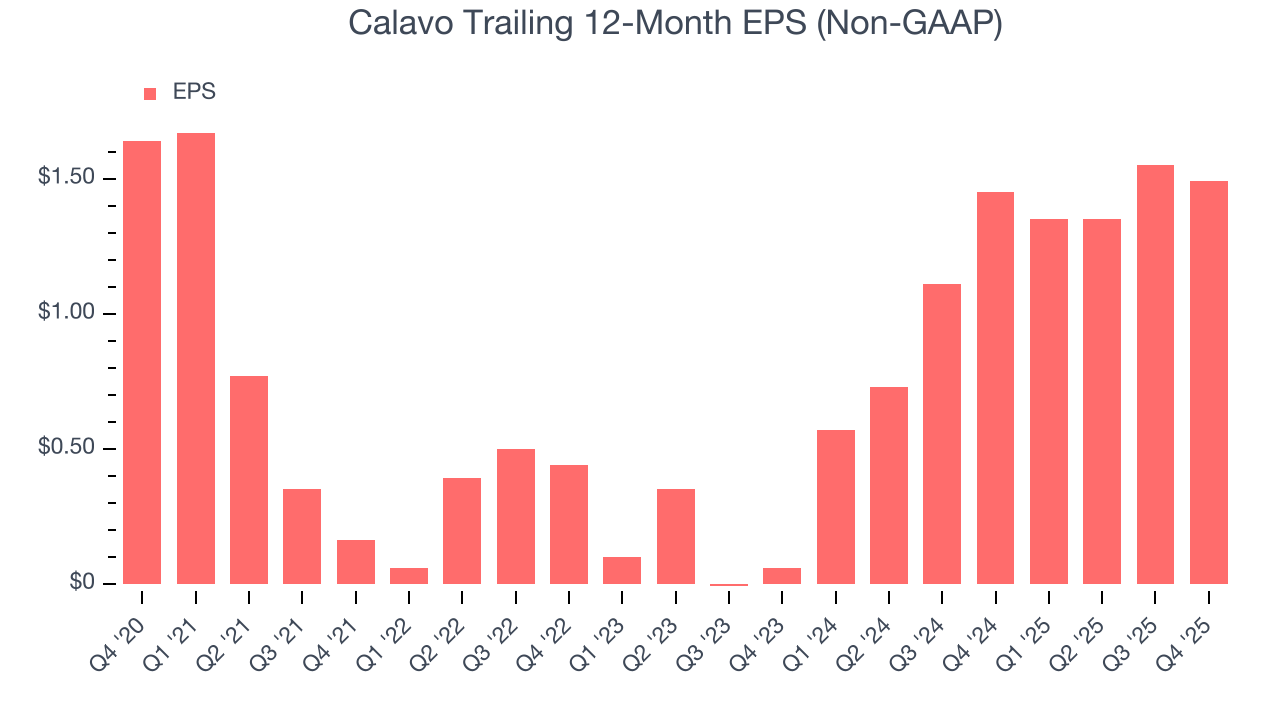

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Calavo’s EPS grew at 50.2% compounded annual growth rate over the last three years, higher than its 16.3% annualized revenue declines. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

In Q4, Calavo reported adjusted EPS of $0.27, down from $0.33 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Calavo’s full-year EPS of $1.49 to grow 2.7%.

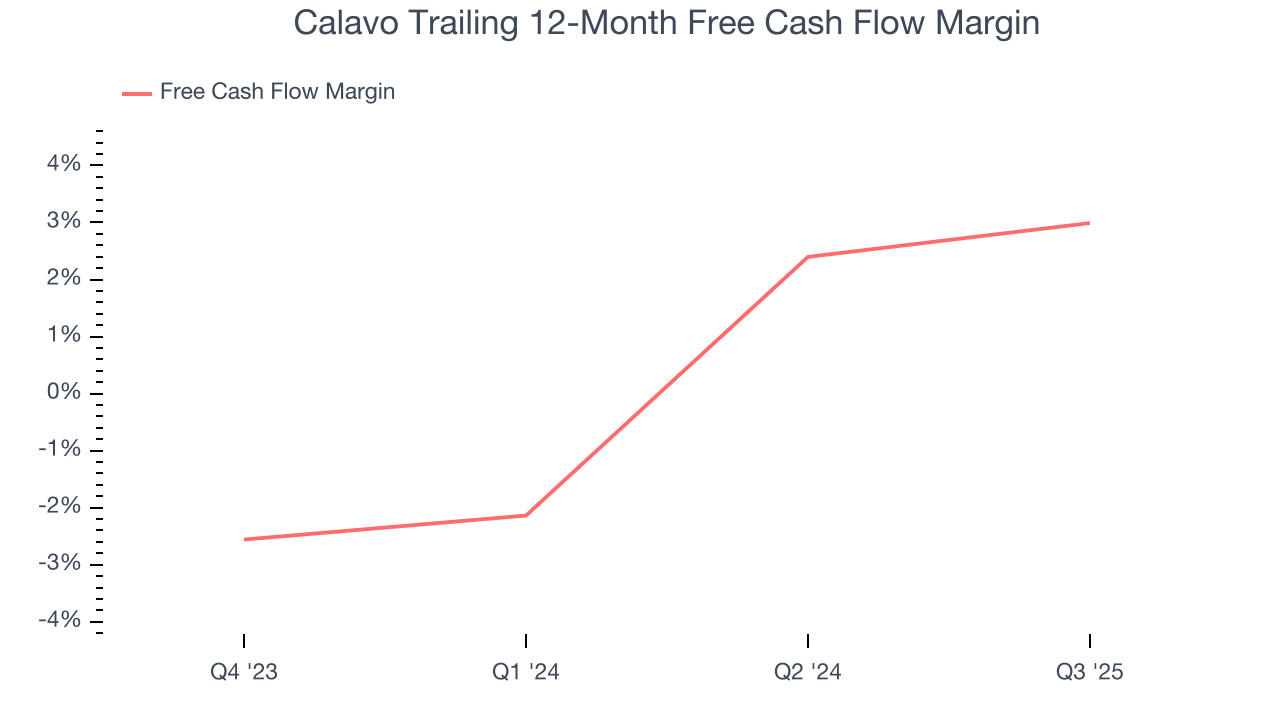

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Calavo has shown mediocre cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 3.1%, below what we’d expect for a consumer staples business.

10. Return on Invested Capital (ROIC)

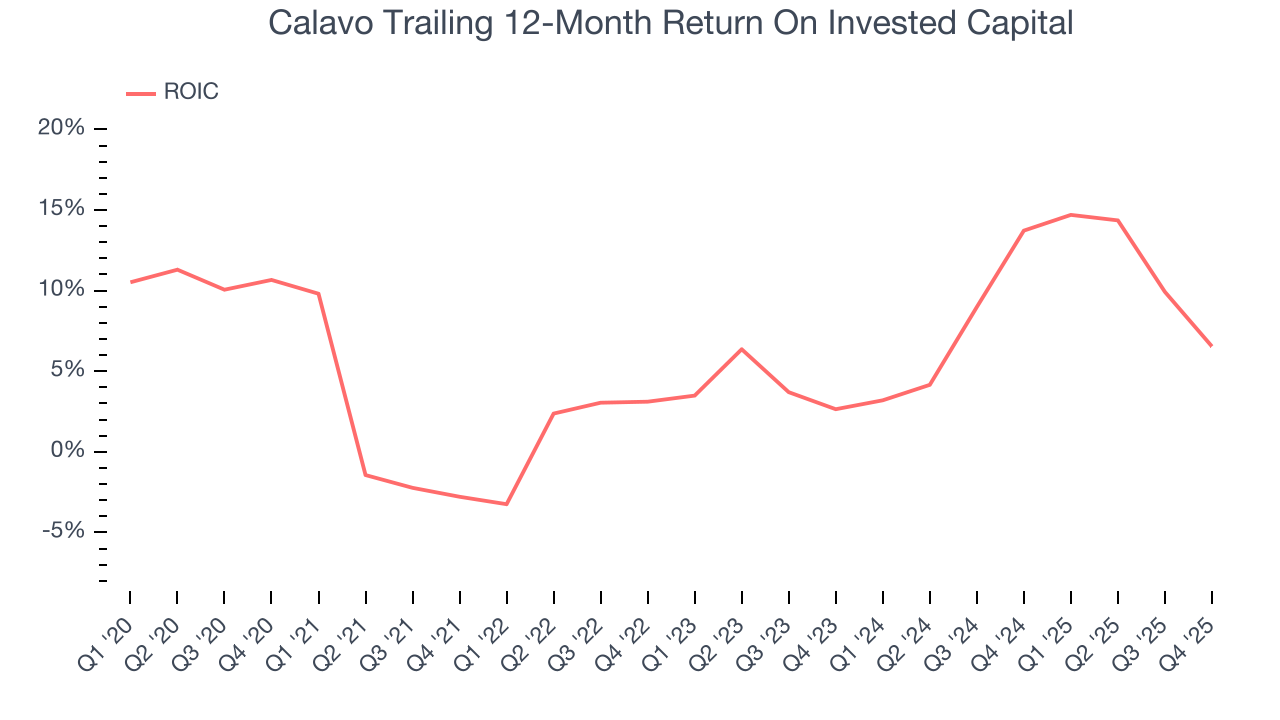

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Calavo historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 4.6%, lower than the typical cost of capital (how much it costs to raise money) for consumer staples companies.

11. Key Takeaways from Calavo’s Q4 Results

We were impressed by how significantly Calavo blew past analysts’ gross margin expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $24.97 immediately following the results.

12. Is Now The Time To Buy Calavo?

Updated: March 13, 2026 at 10:53 PM EDT

Before deciding whether to buy Calavo or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Calavo doesn’t pass our quality test. To kick things off, its revenue has declined over the last three years. While its EPS growth over the last three years has been fantastic, the downside is its gross margins make it more challenging to reach positive operating profits compared to other consumer staples businesses. On top of that, its brand caters to a niche market.

Calavo’s P/E ratio based on the next 12 months is 16.3x. This multiple tells us a lot of good news is priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $27 on the company (compared to the current share price of $23.61).