DXP (DXPE)

We admire DXP. Its revenue is growing quickly while its profitability is rising, giving it multiple ways to win.― StockStory Analyst Team

1. News

2. Summary

Why We Like DXP

Founded during the emergence of Big Oil in Texas, DXP (NASDAQ:DXPE) provides pumps, valves, and other industrial components.

- Earnings growth has massively outpaced its peers over the last five years as its EPS has compounded at 47.4% annually

- Market share has increased this cycle as its 14.9% annual revenue growth over the last five years was exceptional

- Forecasted revenue growth of 10.2% for the next 12 months indicates its momentum over the last two years is sustainable

We expect great things from DXP. The valuation looks fair based on its quality, so this could be a good time to invest in some shares.

Why Is Now The Time To Buy DXP?

DXP is trading at $130.67 per share, or 21.4x forward P/E. This multiple is lower than most industrials companies, and we think the stock is a deal when considering its quality characteristics.

By definition, where you buy a stock impacts returns. Compared to entry price, business quality matters much more for long-term market outperformance. Buying in at a great price helps, nevertheless.

3. DXP (DXPE) Research Report: Q4 CY2025 Update

Industrial distributor DXP Enterprises (NASDAQ:DXPE) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 12% year on year to $527.4 million. Its non-GAAP profit of $1.39 per share was 6.9% above analysts’ consensus estimates.

DXP (DXPE) Q4 CY2025 Highlights:

- Revenue: $527.4 million vs analyst estimates of $499 million (12% year-on-year growth, 5.7% beat)

- Adjusted EPS: $1.39 vs analyst estimates of $1.30 (6.9% beat)

- Adjusted EBITDA: $58.97 million vs analyst estimates of $55 million (11.2% margin, 7.2% beat)

- Operating Margin: 8.8%, in line with the same quarter last year

- Free Cash Flow Margin: 6.5%, up from 4.8% in the same quarter last year

- Market Capitalization: $2.50 billion

Company Overview

Founded during the emergence of Big Oil in Texas, DXP (NASDAQ:DXPE) provides pumps, valves, and other industrial components.

In 1908 Charles A. Levins founded what was formerly known as Southern Engine and Pump Company to deliver water, help steamships operate, and for irrigation purposes. The company made various acquisitions as it sought to provide customers with a single point of contact for a broad category of products and services.

The company has made 40+ acquisitions since the 2000s, targeting smaller companies that complement its existing portfolio or operate independently. For example, it acquired Florida Valve and Alliance Pump & Mechanical in 2023 which, respectively, expanded its offerings of pumps and valves.

DXP provides various pumps including centrifugal pumps (uses a spinning wheel to push liquid outward and create flow) and rotary gear pumps (uses rotating parts to trap and push liquid through the pump) ideal for handling lubricating oils and other liquids. It also offers all kinds of bearings and power transmissions which are used for reducing friction and transferring power in machinery and equipment.

Its selection also spans different industrial components from abrasives and lubricants to hand tools and welding equipment. Additionally, DXP is a source for safety products such as eye protection, first aid kits, and respiratory gear, as well as safety through services. Some of the services it offers include H2S gas protection and fire safety solutions.

DXP primarily engages in long term contracts with businesses which typically last 3 to 5 years. It also offers volume discounts, providing customers with lower prices when they purchase larger quantities of products.

4. Maintenance and Repair Distributors

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Maintenance and repair distributors that boast reliable selection and quickly deliver products to customers can benefit from this theme. While e-commerce hasn’t disrupted industrial distribution as much as consumer retail, it is still a real threat, forcing investment in omnichannel capabilities to serve customers everywhere. Additionally, maintenance and repair distributors are at the whim of economic cycles that impact the capital spending and construction projects that can juice demand.

Competitors offering similar products include Grainger (NYSE:GWW), MSC (NYSE:MSM), and Fastenal (NASDAQ:FAST).

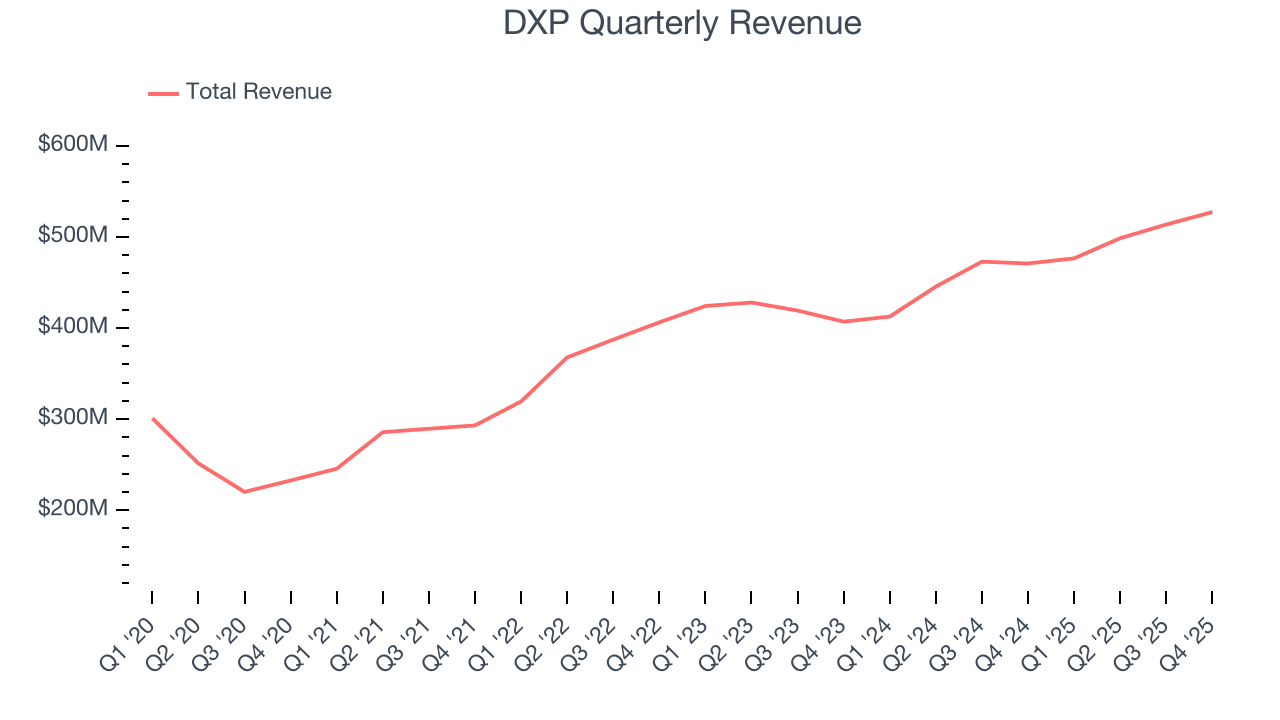

5. Revenue Growth

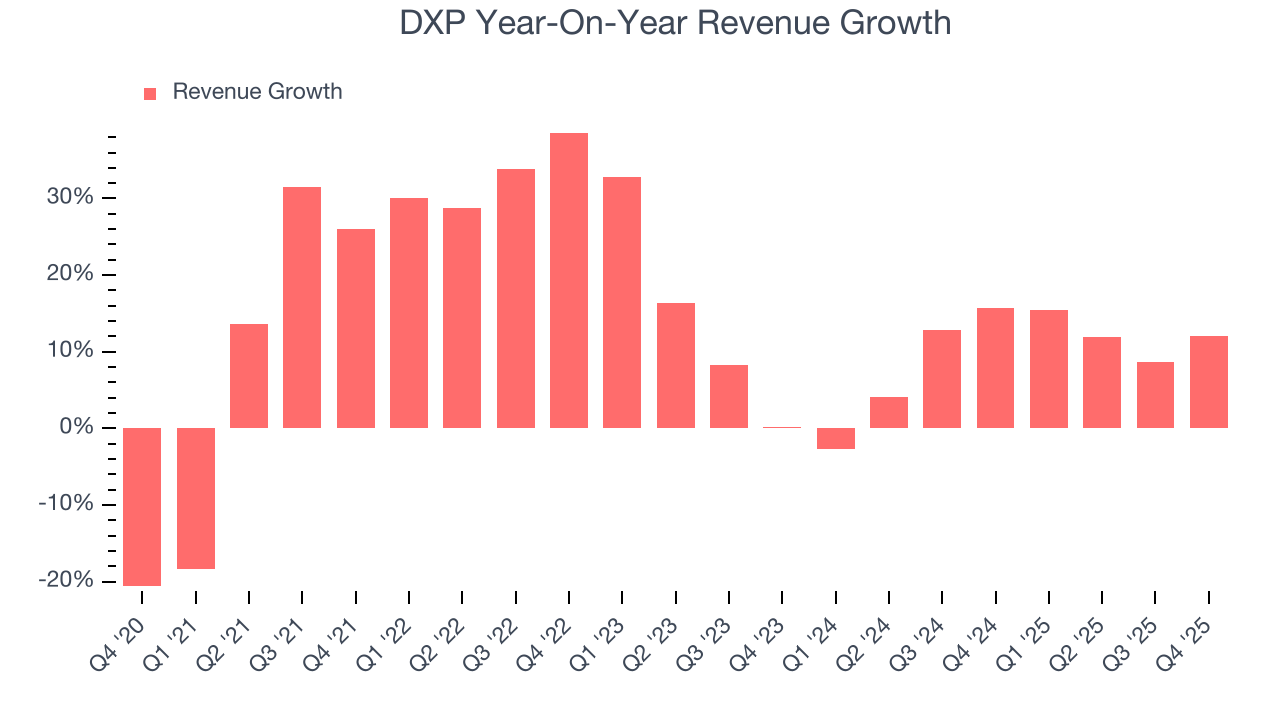

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, DXP grew its sales at an exceptional 14.9% compounded annual growth rate. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. DXP’s annualized revenue growth of 9.6% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, DXP reported year-on-year revenue growth of 12%, and its $527.4 million of revenue exceeded Wall Street’s estimates by 5.7%.

Looking ahead, sell-side analysts expect revenue to grow 3.8% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

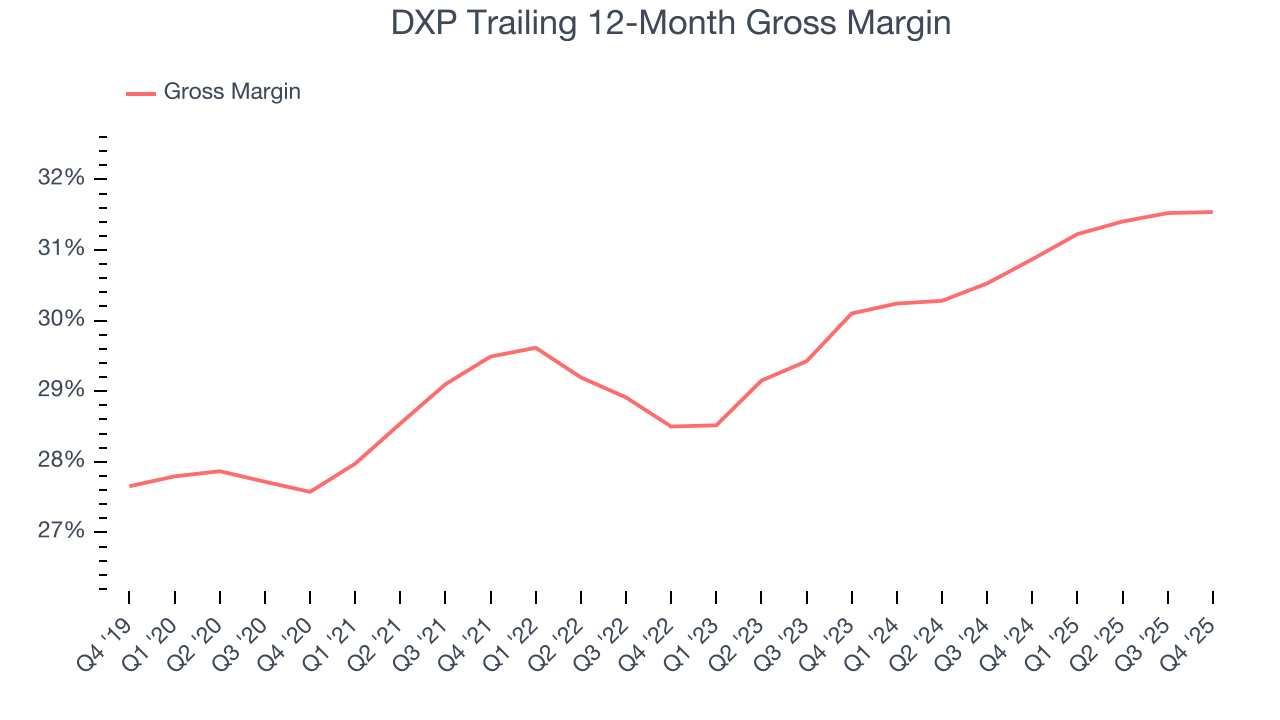

6. Gross Margin & Pricing Power

DXP’s unit economics are better than the typical industrials business, signaling its products are somewhat differentiated through quality or brand.As you can see below, it averaged a decent 30.3% gross margin over the last five years. That means for every $100 in revenue, roughly $30.25 was left to spend on selling, marketing, R&D, and general administrative overhead.

DXP’s gross profit margin came in at 31.6% this quarter, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

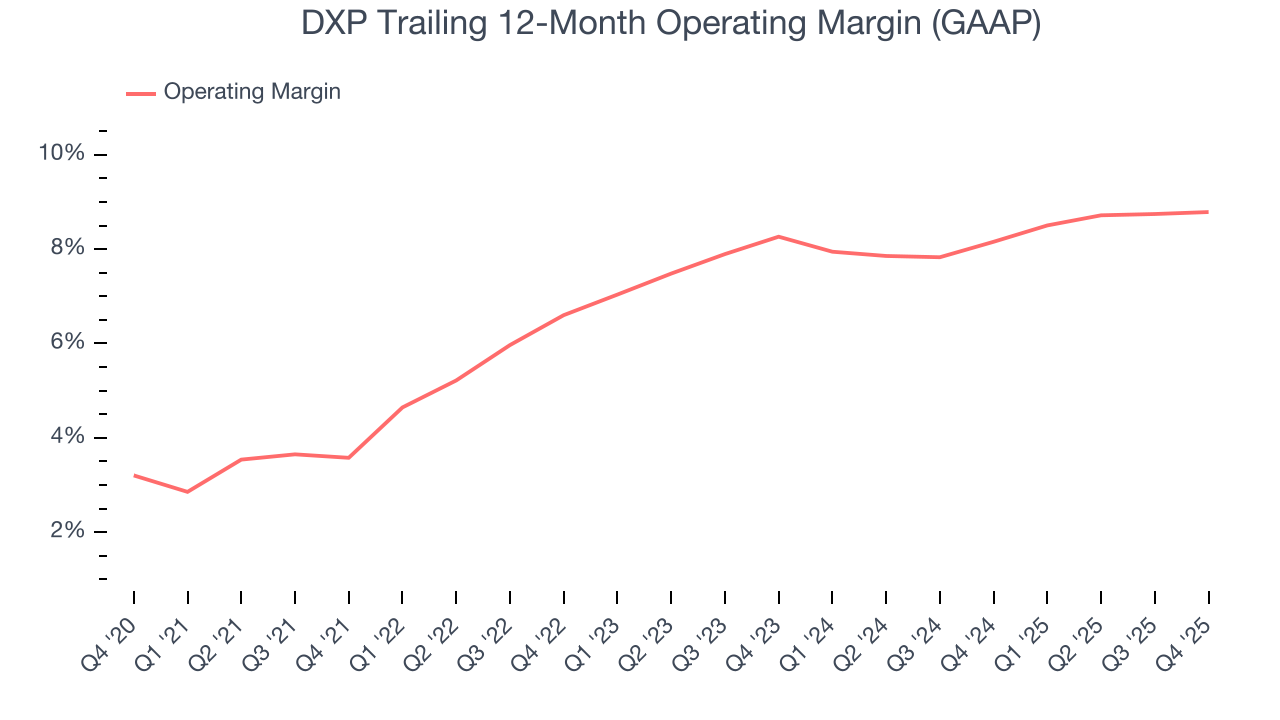

7. Operating Margin

DXP was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.4% was weak for an industrials business.

On the plus side, DXP’s operating margin rose by 5.2 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q4, DXP generated an operating margin profit margin of 8.8%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

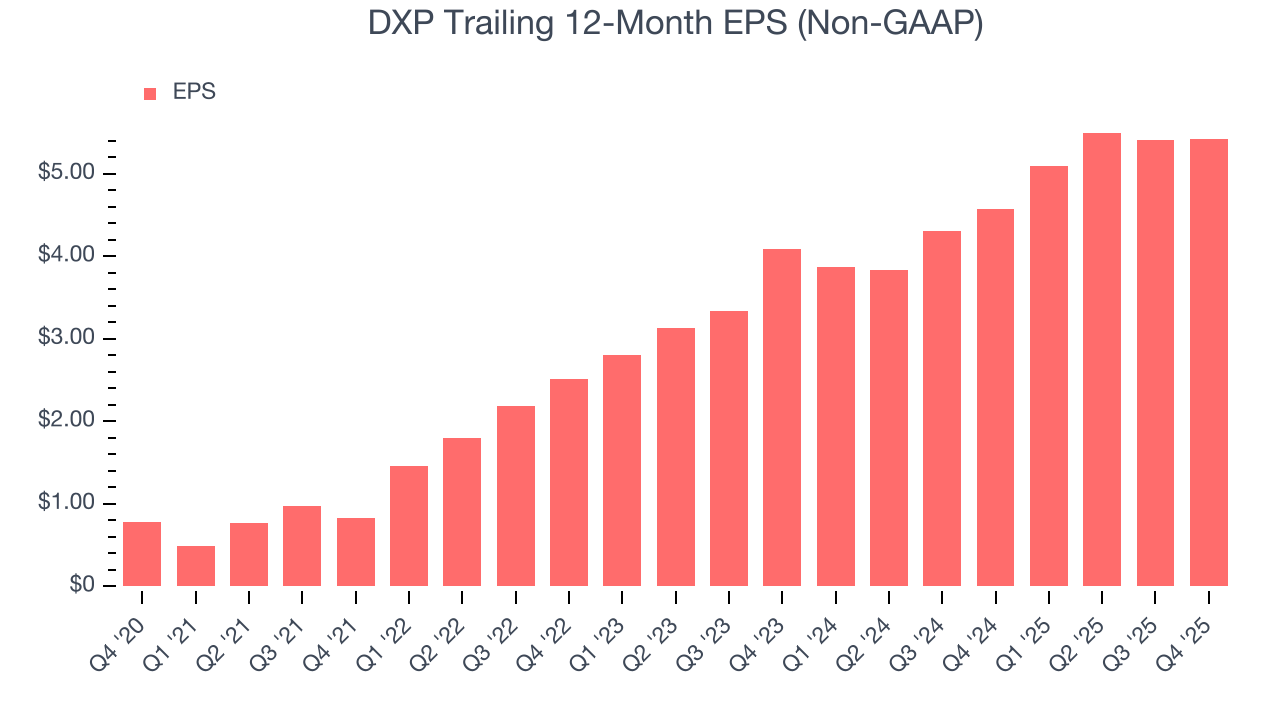

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

DXP’s EPS grew at an astounding 47.4% compounded annual growth rate over the last five years, higher than its 14.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

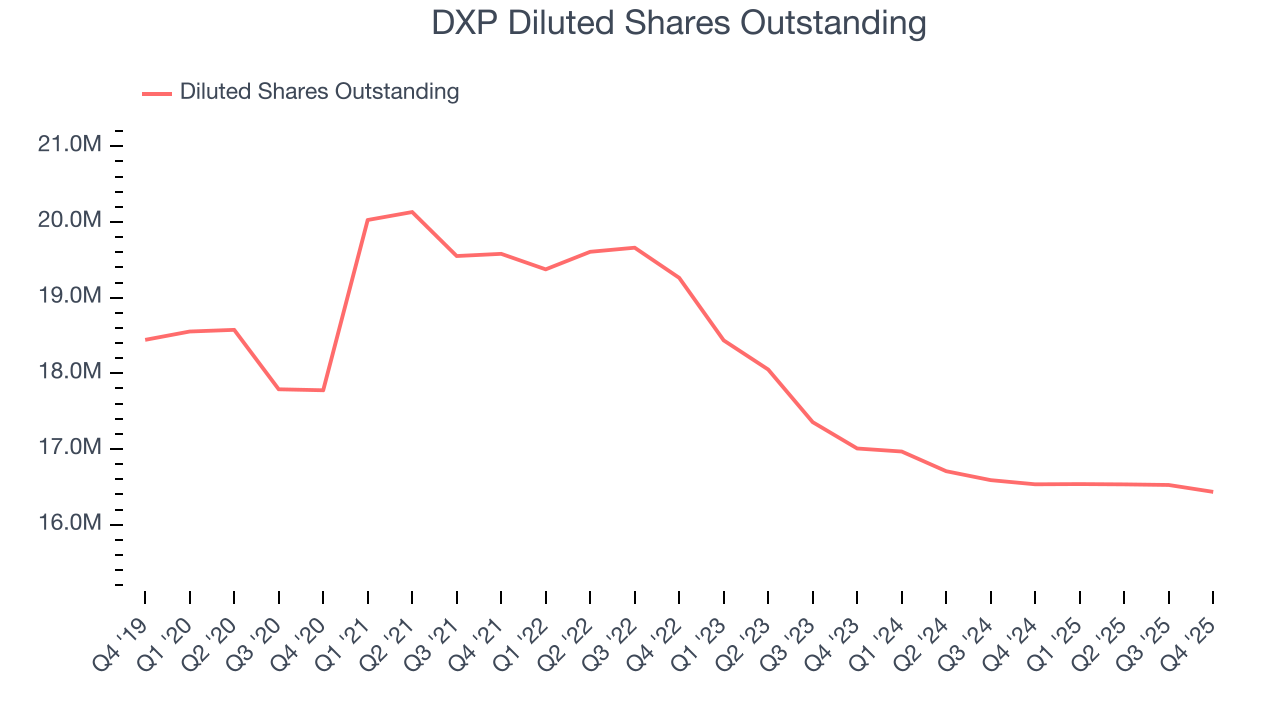

Diving into the nuances of DXP’s earnings can give us a better understanding of its performance. As we mentioned earlier, DXP’s operating margin was flat this quarter but expanded by 5.2 percentage points over the last five years. On top of that, its share count shrank by 7.5%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For DXP, its two-year annual EPS growth of 15.2% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, DXP reported adjusted EPS of $1.39, up from $1.38 in the same quarter last year. This print beat analysts’ estimates by 6.9%. Over the next 12 months, Wall Street expects DXP’s full-year EPS of $5.42 to grow 18.6%.

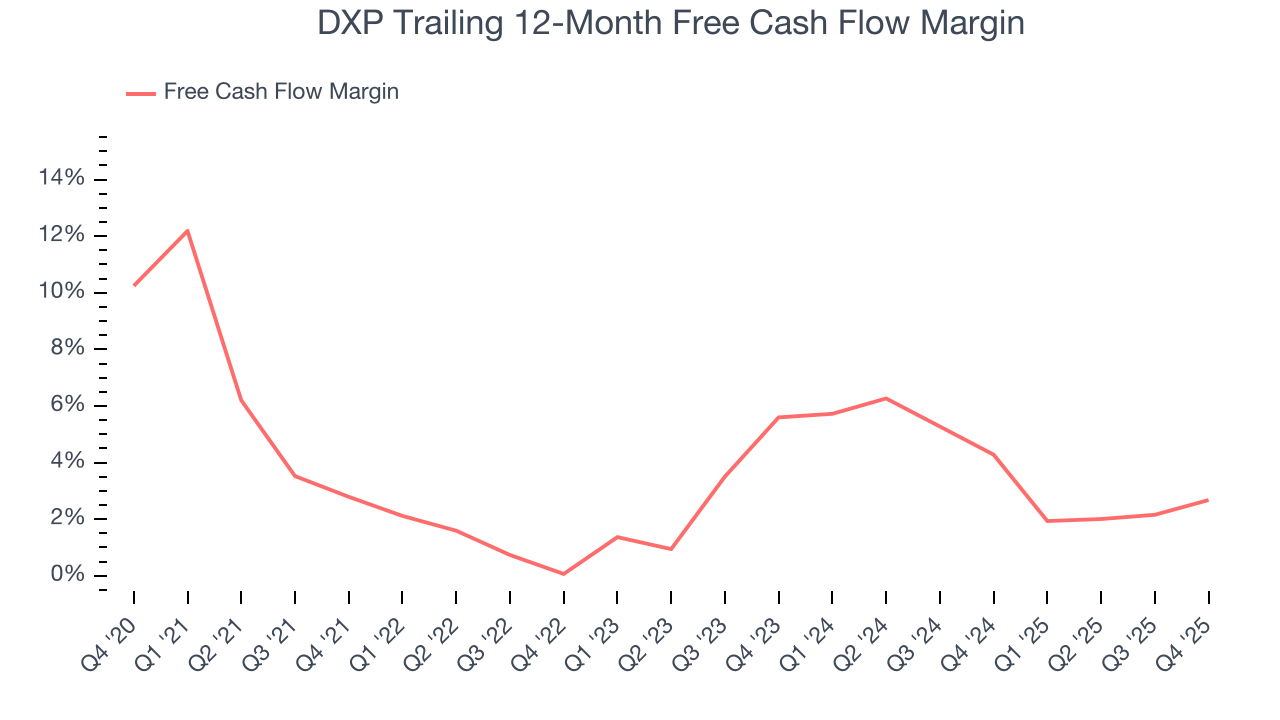

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

DXP has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.2%, subpar for an industrials business.

DXP’s free cash flow clocked in at $34.47 million in Q4, equivalent to a 6.5% margin. This result was good as its margin was 1.7 percentage points higher than in the same quarter last year. Its cash profitability was also above its five-year level, and we hope the company can build on this trend.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

DXP’s five-year average ROIC was 12.4%, higher than most industrials businesses. This illustrates its management team’s ability to invest in profitable growth opportunities and generate value for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, DXP’s has increased over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

11. Balance Sheet Assessment

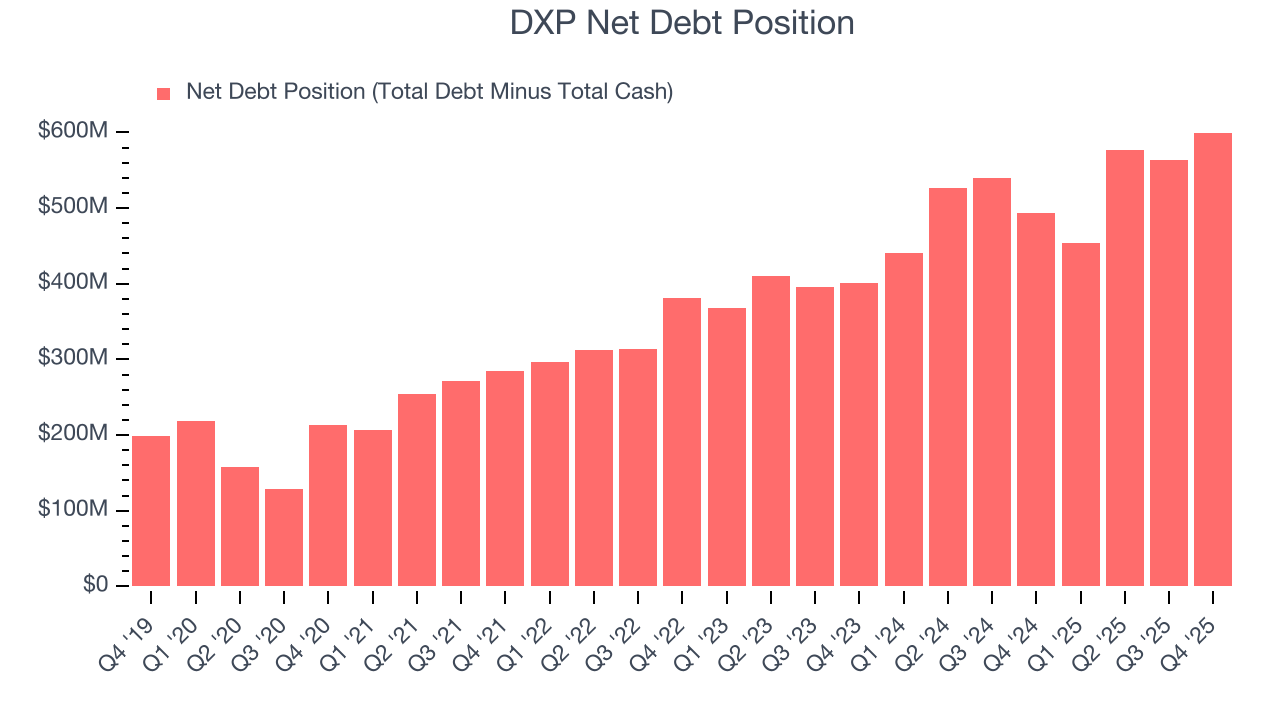

DXP reported $303.9 million of cash and $903.6 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $225.3 million of EBITDA over the last 12 months, we view DXP’s 2.7× net-debt-to-EBITDA ratio as safe. We also see its $25.5 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from DXP’s Q4 Results

We were impressed by how significantly DXP blew past analysts’ revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $155.36 immediately after reporting.

13. Is Now The Time To Buy DXP?

Updated: March 14, 2026 at 11:22 PM EDT

Before deciding whether to buy DXP or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

DXP is a rock-solid business worth owning. For starters, its revenue growth was exceptional over the last five years. And while its low free cash flow margins give it little breathing room, its expanding operating margin shows the business has become more efficient. Additionally, DXP’s astounding EPS growth over the last five years shows its profits are trickling down to shareholders.

DXP’s P/E ratio based on the next 12 months is 21.4x. Looking at the industrials landscape today, DXP’s fundamentals really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $139.50 on the company (compared to the current share price of $130.67), implying they see 6.8% upside in buying DXP in the short term.