Distribution Solutions (DSGR)

Distribution Solutions is interesting. Its exceptional revenue growth indicates it’s winning market share.― StockStory Analyst Team

1. News

2. Summary

Why Distribution Solutions Is Interesting

Founded in 1952, Distribution Solutions (NASDAQ:DSGR) provides supply chain solutions and distributes industrial, safety, and maintenance products to various industries.

- Annual revenue growth of 39.4% over the last four years was superb and indicates its market share increased during this cycle

- Performance over the past two years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 16.7% outpaced its revenue gains

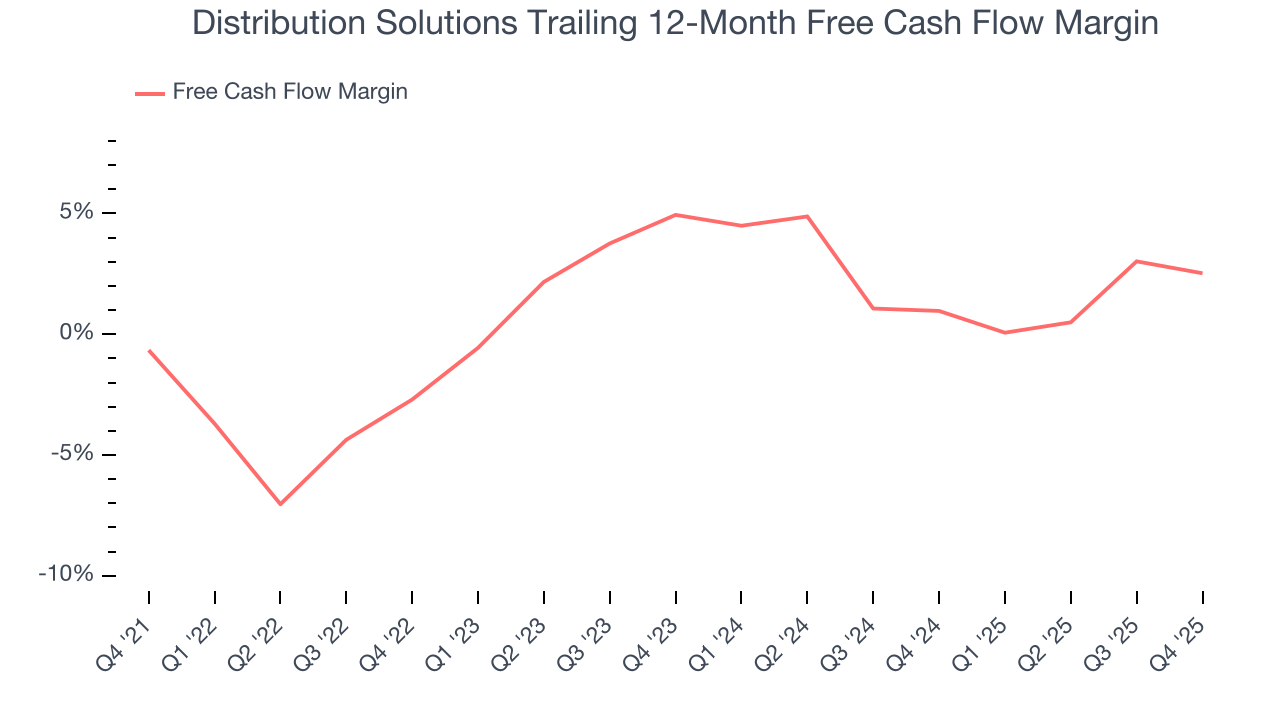

- One risk is its ability to fund investments or reward shareholders with increased buybacks or dividends is restricted by its weak free cash flow margin of 1.5% for the last five years

Distribution Solutions shows some potential. If you’re a believer, the valuation looks fair.

Why Is Now The Time To Buy Distribution Solutions?

Distribution Solutions’s stock price of $19.31 implies a valuation ratio of 13.1x forward P/E. Distribution Solutions’s valuation is lower than that of many in the industrials space. Even so, we think it is justified for the revenue growth characteristics.

This could be a good time to invest if you think there are underappreciated aspects of the business.

3. Distribution Solutions (DSGR) Research Report: Q4 CY2025 Update

Industrial and safety product distributor Distribution Solutions (NASDAQ:DSGR) fell short of the market’s revenue expectations in Q4 CY2025, with sales flat year on year at $481.6 million. Its non-GAAP profit of $0.18 per share was 43.2% below analysts’ consensus estimates.

Distribution Solutions (DSGR) Q4 CY2025 Highlights:

- Revenue: $481.6 million vs analyst estimates of $496.3 million (flat year on year, 3% miss)

- Adjusted EPS: $0.18 vs analyst expectations of $0.32 (43.2% miss)

- Adjusted EBITDA: $35.44 million vs analyst estimates of $43.9 million (7.4% margin, 19.3% miss)

- Operating Margin: 1.6%, down from 4.9% in the same quarter last year

- Free Cash Flow Margin: 2.4%, down from 4.5% in the same quarter last year

- Market Capitalization: $1.37 billion

Company Overview

Founded in 1952, Distribution Solutions (NASDAQ:DSGR) provides supply chain solutions and distributes industrial, safety, and maintenance products to various industries.

Distribution Solutions was established to streamline and enhance the supply chain for industrial and safety products. With a history of addressing product distribution, the company has evolved to offer various solutions.

Today, the company provides industrial supplies, safety equipment, and maintenance products to customers in various industries, ensuring businesses have the necessary tools and materials to maintain operational efficiency and safety. For example, manufacturing firms rely on Distribution Solutions's delivery of essential components to avoid production delays, while construction companies depend on their safety gear to protect workers on-site.

Revenue sources for Distribution Solutions include sales of industrial and safety products, along with value-added services such as inventory management and logistics support. The business model focuses on building customer relationships through direct sales and a distribution network. Recurring revenue is driven by long-term contracts and repeat business from customers for replacement parts.

4. Maintenance and Repair Distributors

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Maintenance and repair distributors that boast reliable selection and quickly deliver products to customers can benefit from this theme. While e-commerce hasn’t disrupted industrial distribution as much as consumer retail, it is still a real threat, forcing investment in omnichannel capabilities to serve customers everywhere. Additionally, maintenance and repair distributors are at the whim of economic cycles that impact the capital spending and construction projects that can juice demand.

Competitors in the industrial products industry include Grainger (NYSE:GWW), Fastenal (NASDAQ:FAST), and MSC Industrial (NYSE:MSM)

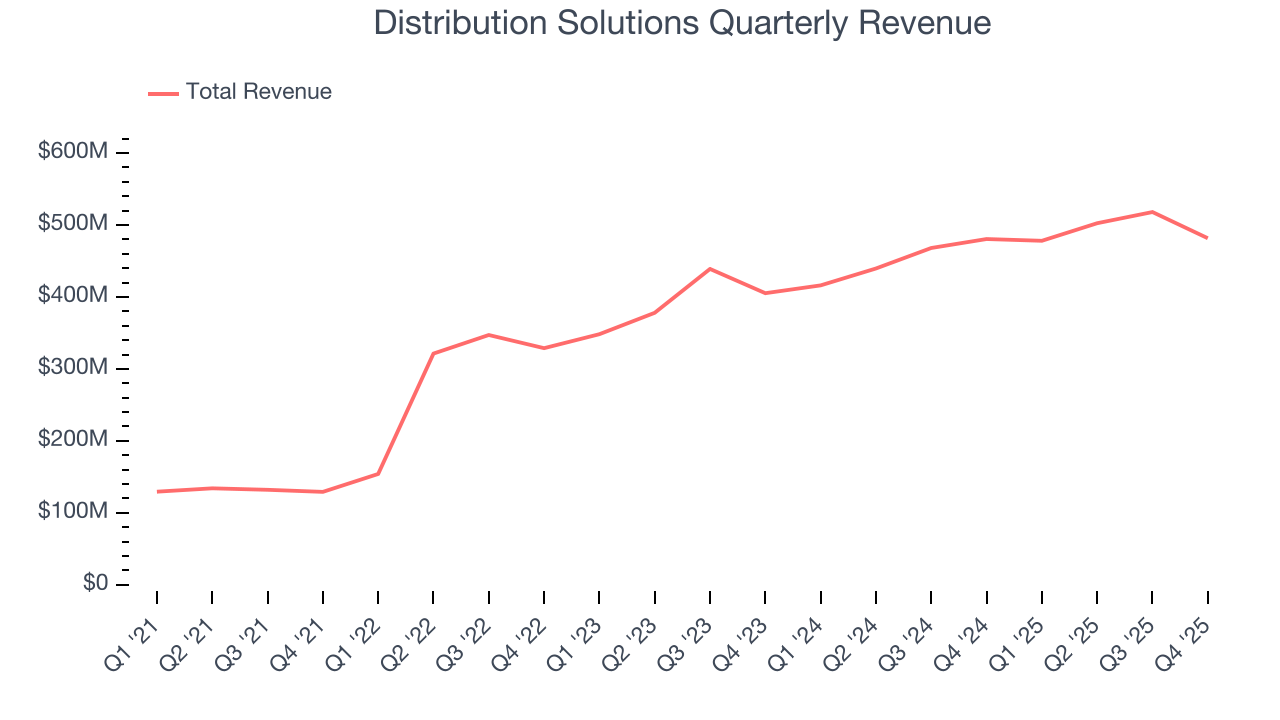

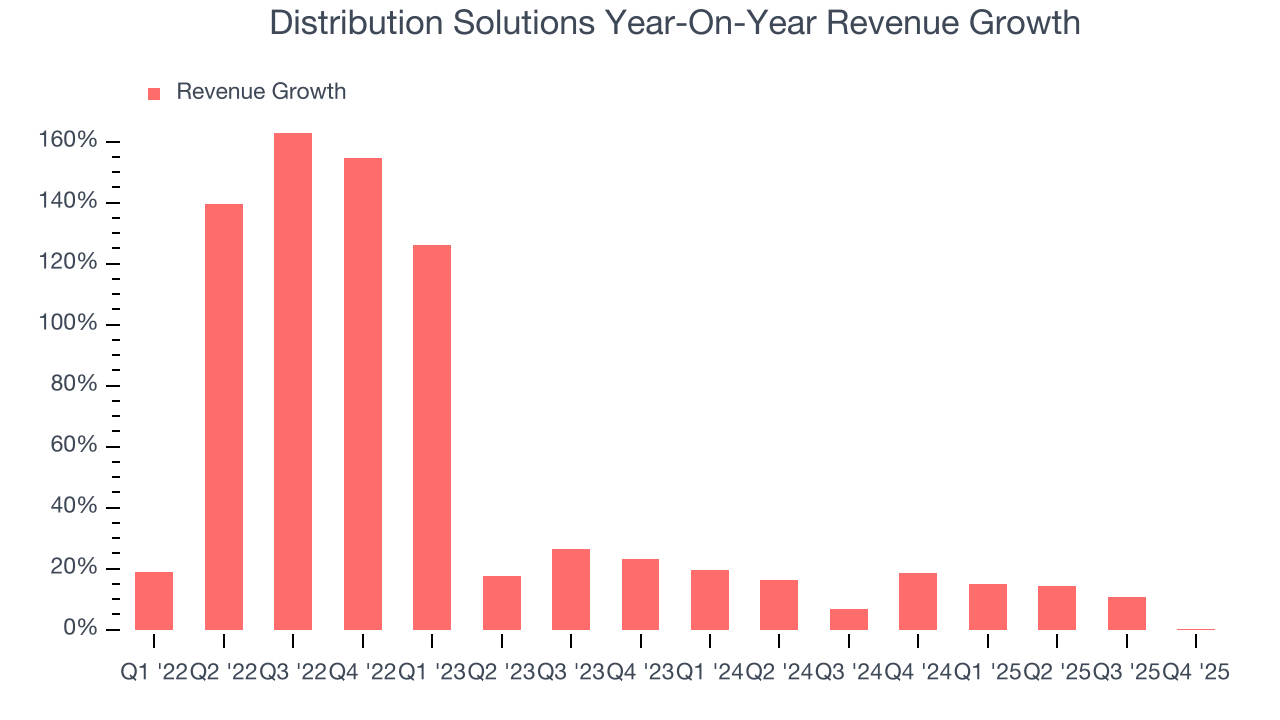

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Distribution Solutions’s 39.4% annualized revenue growth over the last four years was incredible. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Distribution Solutions’s annualized revenue growth of 12.3% over the last two years is below its four-year trend, but we still think the results suggest healthy demand.

This quarter, Distribution Solutions’s $481.6 million of revenue was flat year on year, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

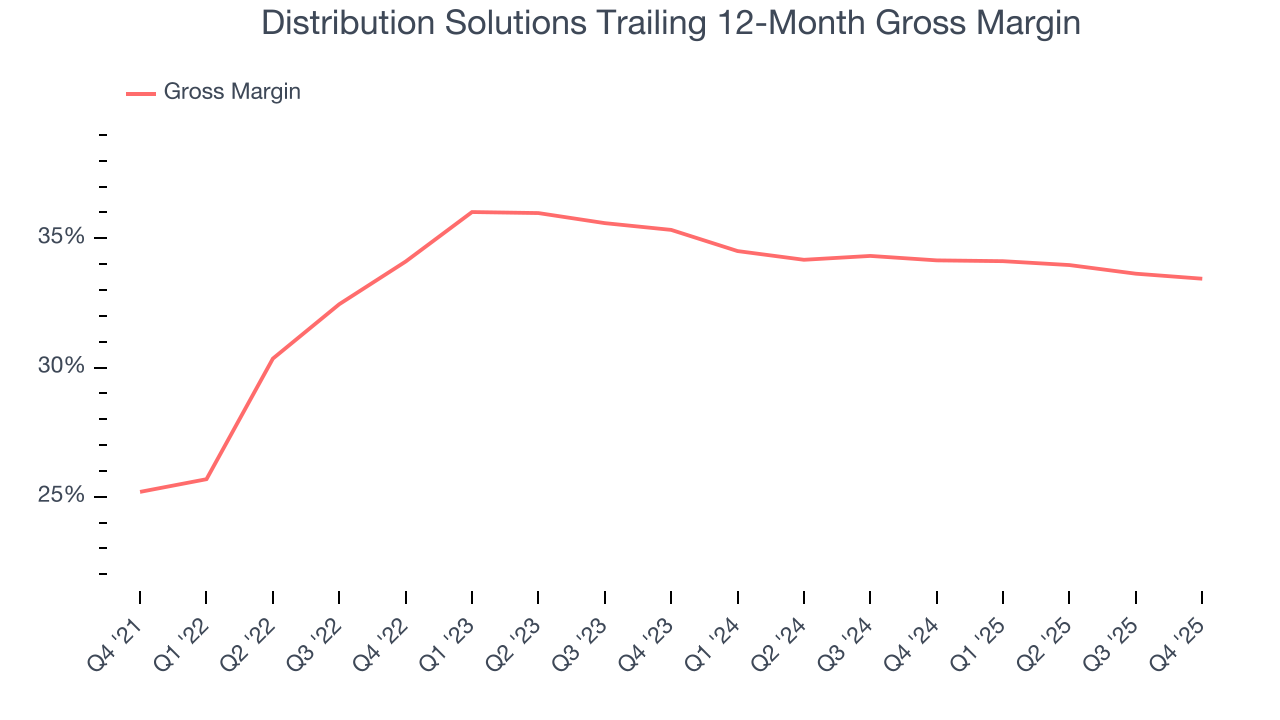

6. Gross Margin & Pricing Power

Distribution Solutions’s gross margin is good compared to other industrials businesses and signals it sells differentiated products, not commodities. As you can see below, it averaged an impressive 33.5% gross margin over the last five years. Said differently, Distribution Solutions paid its suppliers $66.47 for every $100 in revenue.

In Q4, Distribution Solutions produced a 32.7% gross profit margin, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

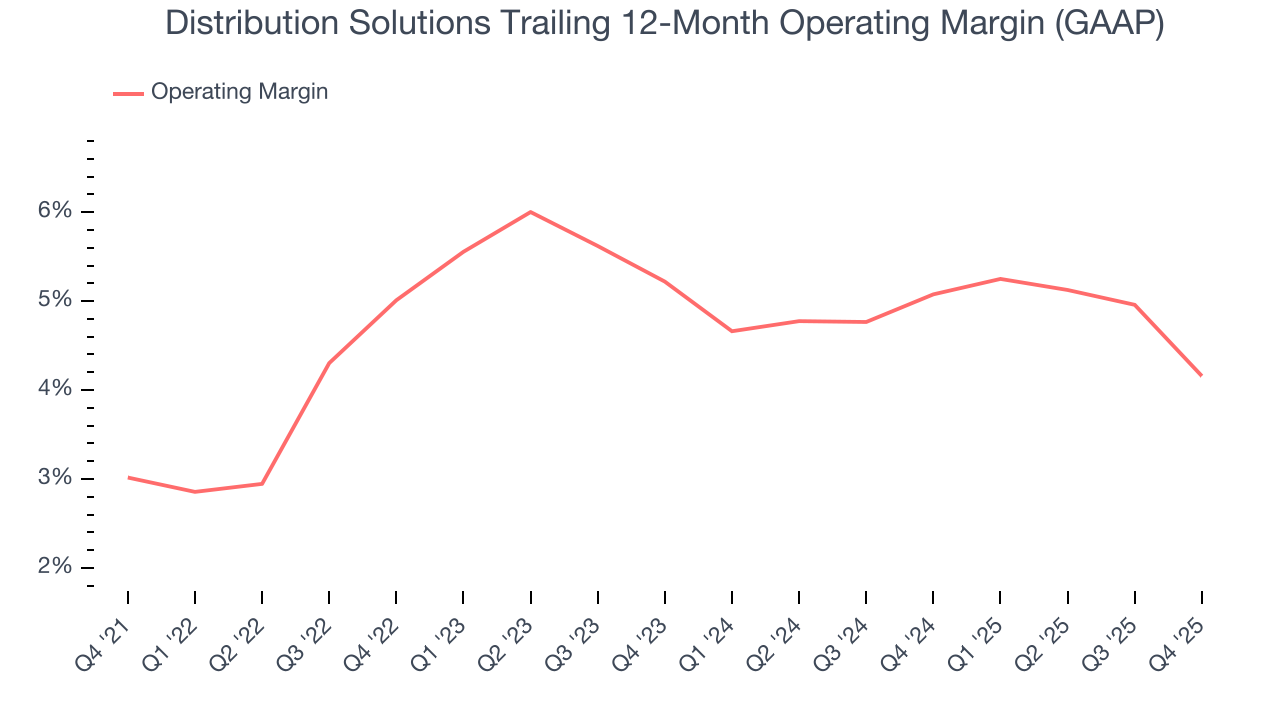

7. Operating Margin

Distribution Solutions was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.7% was weak for an industrials business. This result is surprising given its high gross margin as a starting point.

On the plus side, Distribution Solutions’s operating margin rose by 1.1 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Distribution Solutions generated an operating margin profit margin of 1.6%, down 3.3 percentage points year on year. Since Distribution Solutions’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Distribution Solutions has shown poor cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.6%, below what we’d expect for an industrials business.

Taking a step back, an encouraging sign is that Distribution Solutions’s margin expanded by 3.2 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Distribution Solutions’s free cash flow clocked in at $11.72 million in Q4, equivalent to a 2.4% margin. The company’s cash profitability regressed as it was 2 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

9. Balance Sheet Assessment

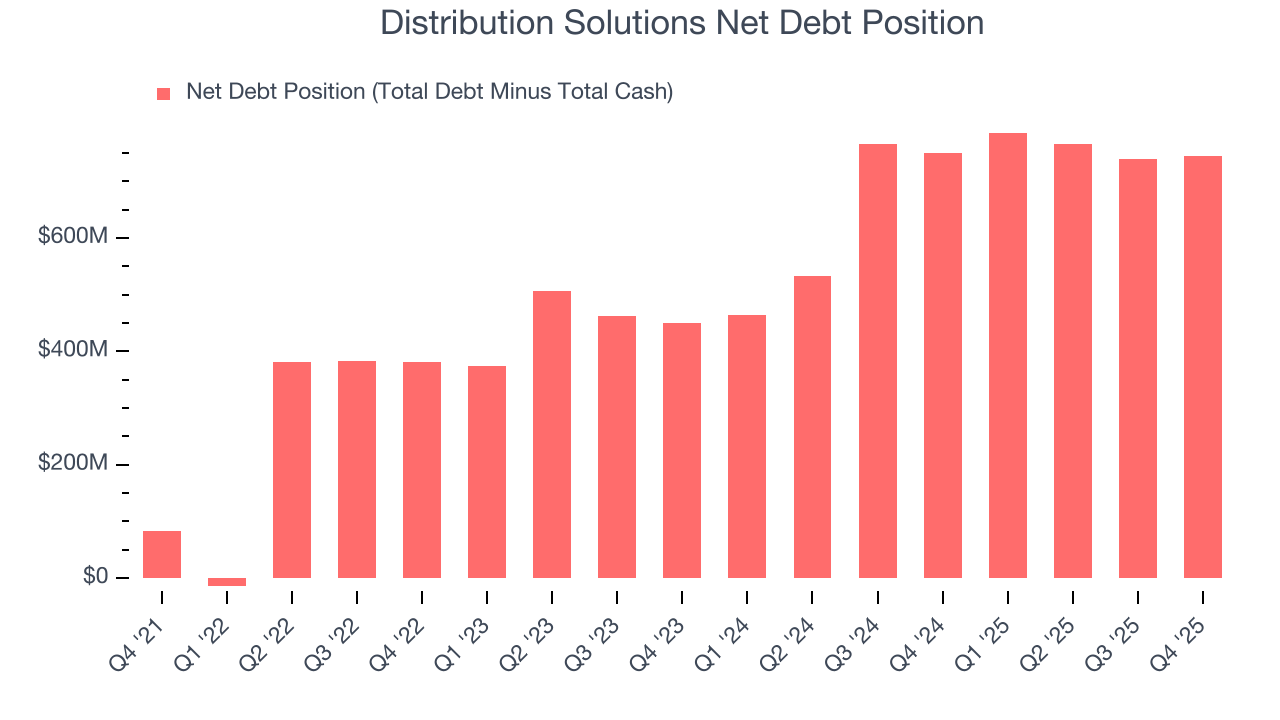

Distribution Solutions reported $75.33 million of cash and $819.1 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $175.2 million of EBITDA over the last 12 months, we view Distribution Solutions’s 4.2× net-debt-to-EBITDA ratio as safe. We also see its $29.46 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

10. Key Takeaways from Distribution Solutions’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 8.3% to $27.25 immediately after reporting.

11. Is Now The Time To Buy Distribution Solutions?

Updated: March 14, 2026 at 11:17 PM EDT

Are you wondering whether to buy Distribution Solutions or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

First of all, the company’s revenue growth was exceptional over the last four years. And while its low free cash flow margins give it little breathing room, its projected EPS for the next year implies the company will generate shareholder value. Additionally, Distribution Solutions’s spectacular EPS growth over the last two years shows its profits are trickling down to shareholders.

Distribution Solutions’s P/E ratio based on the next 12 months is 13.1x. Looking at the industrials landscape right now, Distribution Solutions trades at a pretty interesting price. If you’re a fan of the business and management team, now is a good time to scoop up some shares.

Wall Street analysts have a consensus one-year price target of $35.50 on the company (compared to the current share price of $19.31), implying they see 83.8% upside in buying Distribution Solutions in the short term.