EverQuote (EVER)

We aren’t fans of EverQuote. Its projected EPS for the next year is underwhelming, which doesn’t bode well for its share price.― StockStory Analyst Team

1. News

2. Summary

Why EverQuote Is Not Exciting

Aiming to simplify a once complicated process, EverQuote (NASDAQ:EVER) is an online insurance marketplace where consumers can compare and purchase various types of insurance from different providers

- Excessive marketing spend signals little organic demand and traction for its platform

- A positive is that its platform is difficult to replicate at scale and leads to a best-in-class gross margin of 96.6%

EverQuote falls short of our expectations. Our attention is focused on better businesses.

Why There Are Better Opportunities Than EverQuote

EverQuote is trading at $16.09 per share, or 3.9x forward EV/EBITDA. EverQuote’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. EverQuote (EVER) Research Report: Q4 CY2025 Update

Online insurance comparison site EverQuote (NASDAQ:EVER) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 32.5% year on year to $195.3 million. On the other hand, next quarter’s revenue guidance of $180 million was less impressive, coming in 7% below analysts’ estimates. Its GAAP profit of $1.54 per share was significantly above analysts’ consensus estimates.

EverQuote (EVER) Q4 CY2025 Highlights:

- Revenue: $195.3 million vs analyst estimates of $176.9 million (32.5% year-on-year growth, 10.4% beat)

- EPS (GAAP): $1.54 vs analyst estimates of $0.36 (significant beat)

- Adjusted EBITDA: $25.06 million vs analyst estimates of $21.92 million (12.8% margin, 14.4% beat)

- Revenue Guidance for Q1 CY2026 is $180 million at the midpoint, below analyst estimates of $193.6 million

- EBITDA guidance for Q1 CY2026 is $25 million at the midpoint, below analyst estimates of $26.87 million

- Operating Margin: 9.5%, up from 8.2% in the same quarter last year

- Free Cash Flow Margin: 13.2%, up from 10.6% in the previous quarter

- Market Capitalization: $557 million

Company Overview

Aiming to simplify a once complicated process, EverQuote (NASDAQ:EVER) is an online insurance marketplace where consumers can compare and purchase various types of insurance from different providers

EverQuote is an online insurance marketplace founded in 2011 by Seth Birnbaum and Tomas Revesz, with the aim of revolutionizing the way people shop for and compare insurance policies. EverQuote's primary product is an online platform that allows users to compare and purchase auto, home, renters, and life insurance policies from different insurance companies. The platform uses proprietary analytics and algorithms to match users with insurance providers that offer the best coverage and prices based on their specific needs and budget.

The service provided by EverQuote is essential for customers because shopping for insurance can be a daunting and confusing process, especially for those who are not familiar with the intricacies of insurance policies. With EverQuote, customers can easily and quickly compare policies from different providers and choose the one that suits them best.

EverQuote makes money by charging insurance companies a fee for every lead generated through its platform. This fee is based on the type of insurance policy, the lead's quality, and the competition in the market.

4. Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Competitors offering an insurance marketplace include Progressive (NYSE:PGR) as well as private companies Farmer’s Insurance and Liberty Mutual.

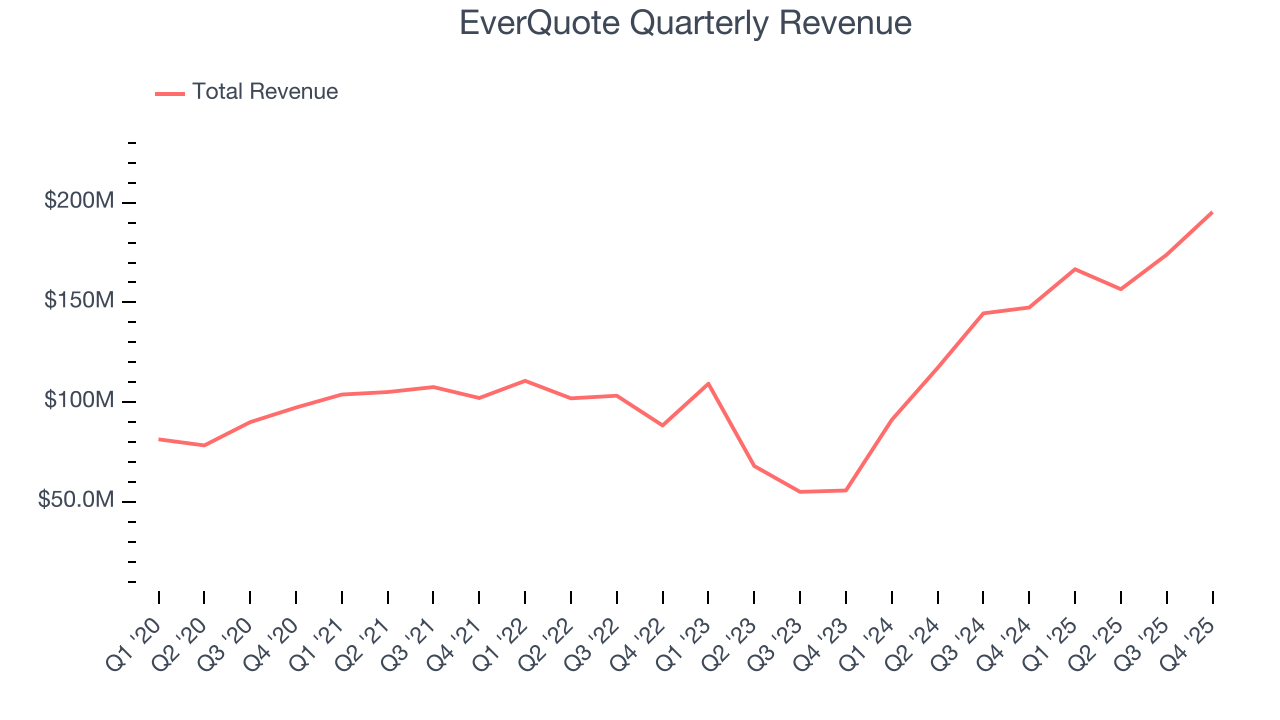

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, EverQuote grew its sales at an impressive 19.7% compounded annual growth rate. Its growth beat the average consumer internet company and shows its offerings resonate with customers.

This quarter, EverQuote reported wonderful year-on-year revenue growth of 32.5%, and its $195.3 million of revenue exceeded Wall Street’s estimates by 10.4%. Company management is currently guiding for a 8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.8% over the next 12 months, a deceleration versus the last three years. Still, this projection is above average for the sector and indicates the market is forecasting some success for its newer products and services.

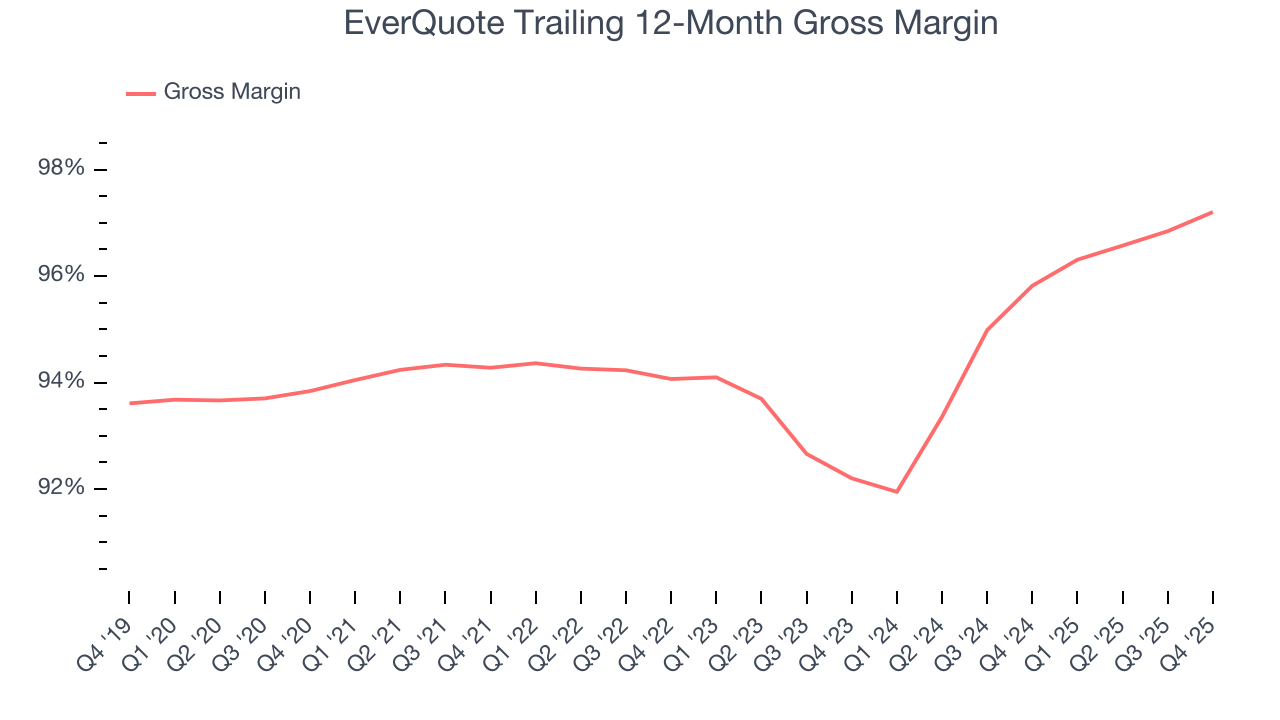

6. Gross Margin & Pricing Power

For online marketplaces like EverQuote, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification.

EverQuote’s gross margin is one of the highest in the consumer internet sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in product and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 96.6% gross margin over the last two years. Said differently, roughly $96.62 was left to spend on selling, marketing, and R&D for every $100 in revenue.

This quarter, EverQuote’s gross profit margin was 97.7% , marking a 1.4 percentage point increase from 96.3% in the same quarter last year. EverQuote’s full-year margin has also been trending up over the past 12 months, increasing by 1.4 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

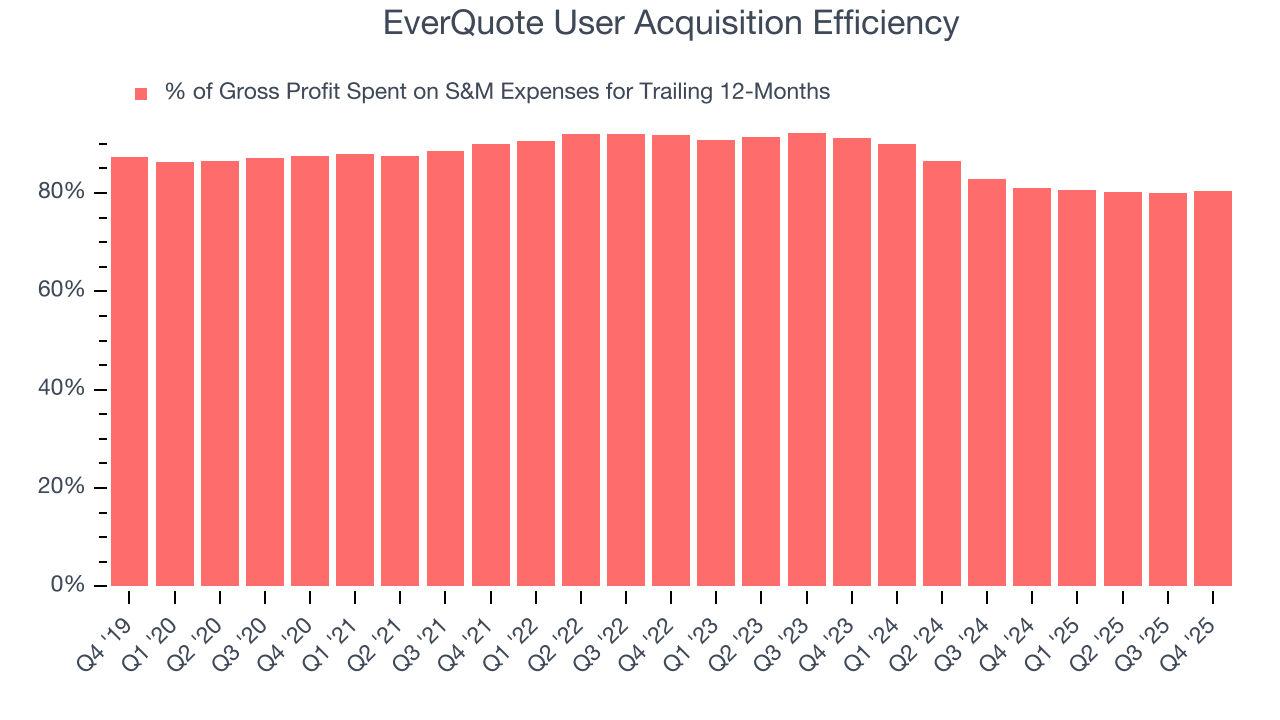

7. User Acquisition Efficiency

Consumer internet businesses like EverQuote grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

It’s very expensive for EverQuote to acquire new users as the company has spent 80.3% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates a highly competitive environment with little differentiation between EverQuote and its peers.

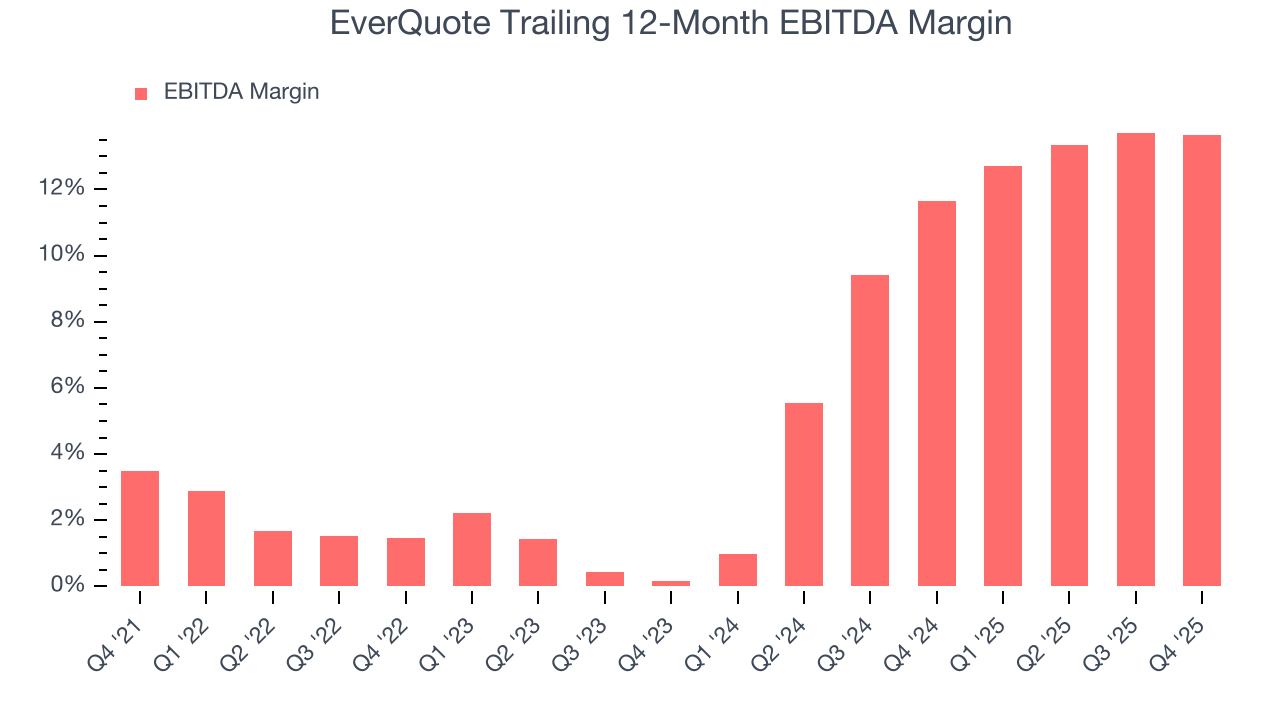

8. EBITDA

EBITDA is a good way of judging operating profitability for consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a more standardized view of the business’s profit potential.

EverQuote has been an efficient company over the last two years. It was one of the more profitable businesses in the consumer internet sector, boasting an average EBITDA margin of 12.8%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, EverQuote’s EBITDA margin rose by 12.2 percentage points over the last few years, as its sales growth gave it operating leverage.

This quarter, EverQuote generated an EBITDA margin profit margin of 12.8%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

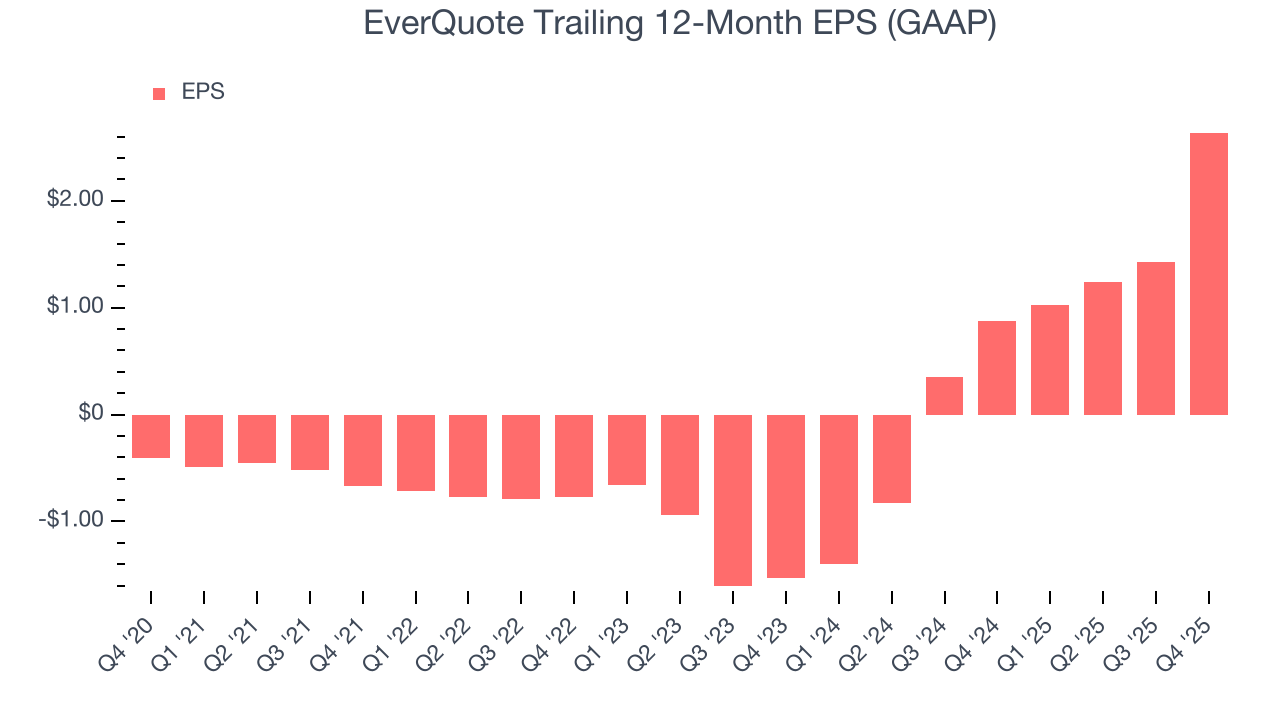

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

EverQuote’s full-year EPS flipped from negative to positive over the last three years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, EverQuote reported EPS of $1.54, up from $0.33 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects EverQuote’s full-year EPS of $2.64 to shrink by 32.6%.

10. Cash Is King

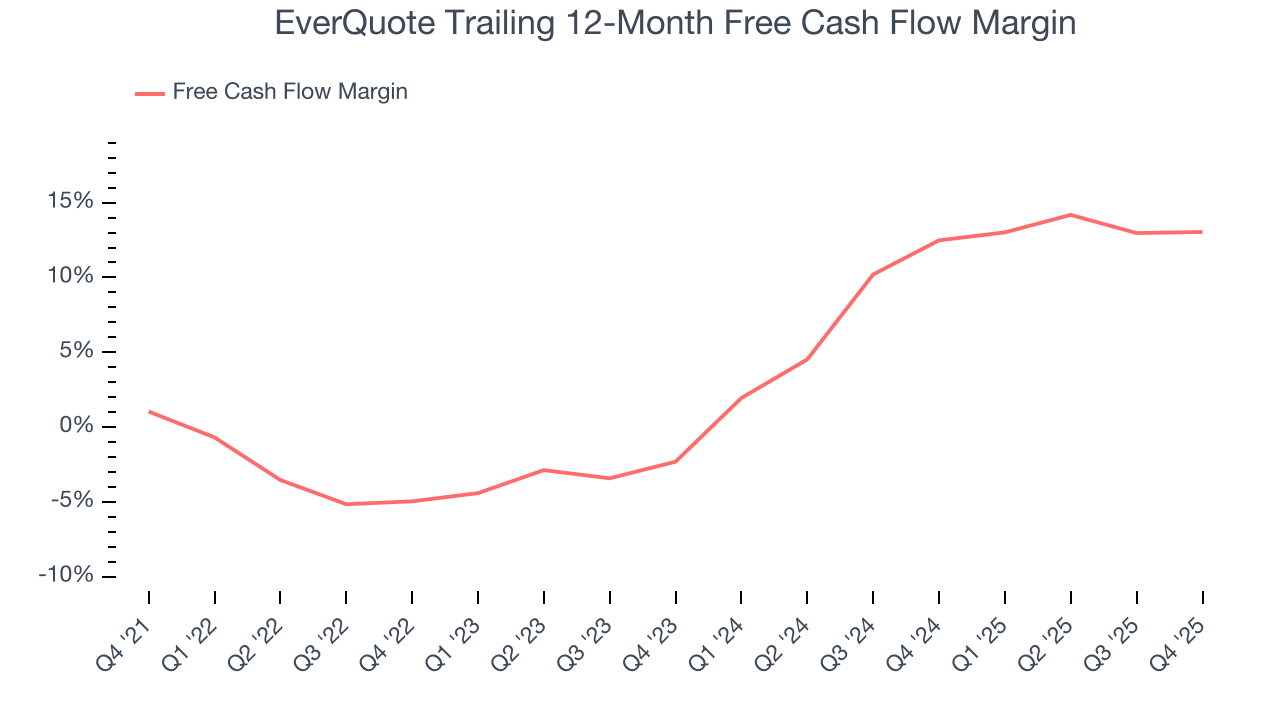

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

EverQuote has shown impressive cash profitability, driven by its attractive business model that gives it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 12.8% over the last two years, better than the broader consumer internet sector.

Taking a step back, we can see that EverQuote’s margin expanded by 18 percentage points over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

EverQuote’s free cash flow clocked in at $25.85 million in Q4, equivalent to a 13.2% margin. This cash profitability was in line with the comparable period last year and its two-year average.

11. Balance Sheet Assessment

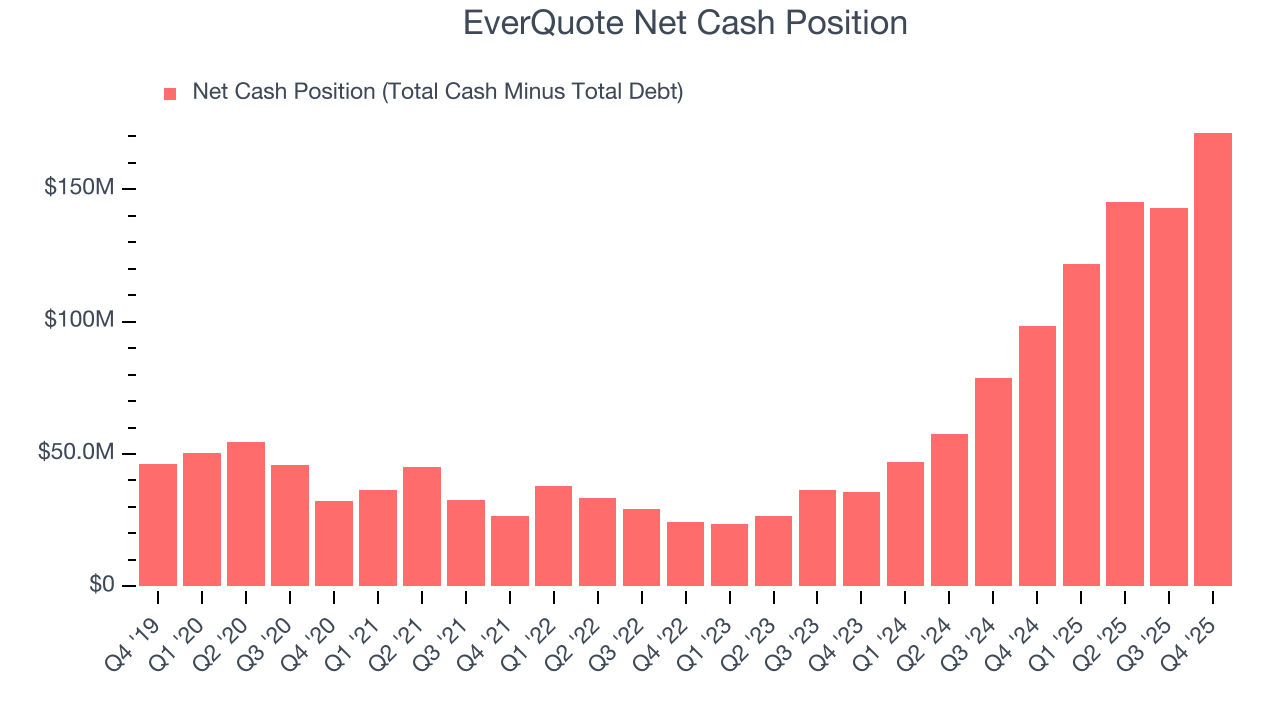

Businesses that maintain a cash surplus face reduced bankruptcy risk.

EverQuote is a profitable, well-capitalized company with $171.4 million of cash and no debt. This position is 30.8% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from EverQuote’s Q4 Results

We were impressed by how significantly EverQuote blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its revenue guidance for next quarter missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 8.3% to $14.05 immediately following the results.

13. Is Now The Time To Buy EverQuote?

Updated: March 15, 2026 at 10:31 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own EverQuote, you should also grasp the company’s longer-term business quality and valuation.

EverQuote isn’t a terrible business, but it doesn’t pass our bar. Although its revenue growth was impressive over the last three years, it’s expected to deteriorate over the next 12 months and its sales and marketing spend is very high compared to other consumer internet businesses. And while the company’s admirable gross margins are a wonderful starting point for the overall profitability of the business, the downside is its projected EPS for the next year is lacking.

EverQuote’s EV/EBITDA ratio based on the next 12 months is 3.9x. This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $24.17 on the company (compared to the current share price of $16.09).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.