ICU Medical (ICUI)

We’re skeptical of ICU Medical. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think ICU Medical Will Underperform

Founded in 1984 and named for its initial focus on intensive care units, ICU Medical (NASDAQ:ICUI) develops and manufactures medical products for infusion therapy, vascular access, and vital care applications used in hospitals and other healthcare settings.

- Forecasted revenue decline of 1.8% for the upcoming 12 months implies demand will fall off a cliff

- Below-average returns on capital indicate management struggled to find compelling investment opportunities, and its decreasing returns suggest its historical profit centers are aging

- A silver lining is that its solid 12.4% annual revenue growth over the last five years indicates its offering’s solve complex business issues

ICU Medical fails to meet our quality criteria. We see more attractive opportunities in the market.

Why There Are Better Opportunities Than ICU Medical

ICU Medical’s stock price of $125.99 implies a valuation ratio of 15.9x forward P/E. ICU Medical’s valuation may seem like a bargain, especially when stacked up against other healthcare companies. We remind you that you often get what you pay for, though.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. ICU Medical (ICUI) Research Report: Q4 CY2025 Update

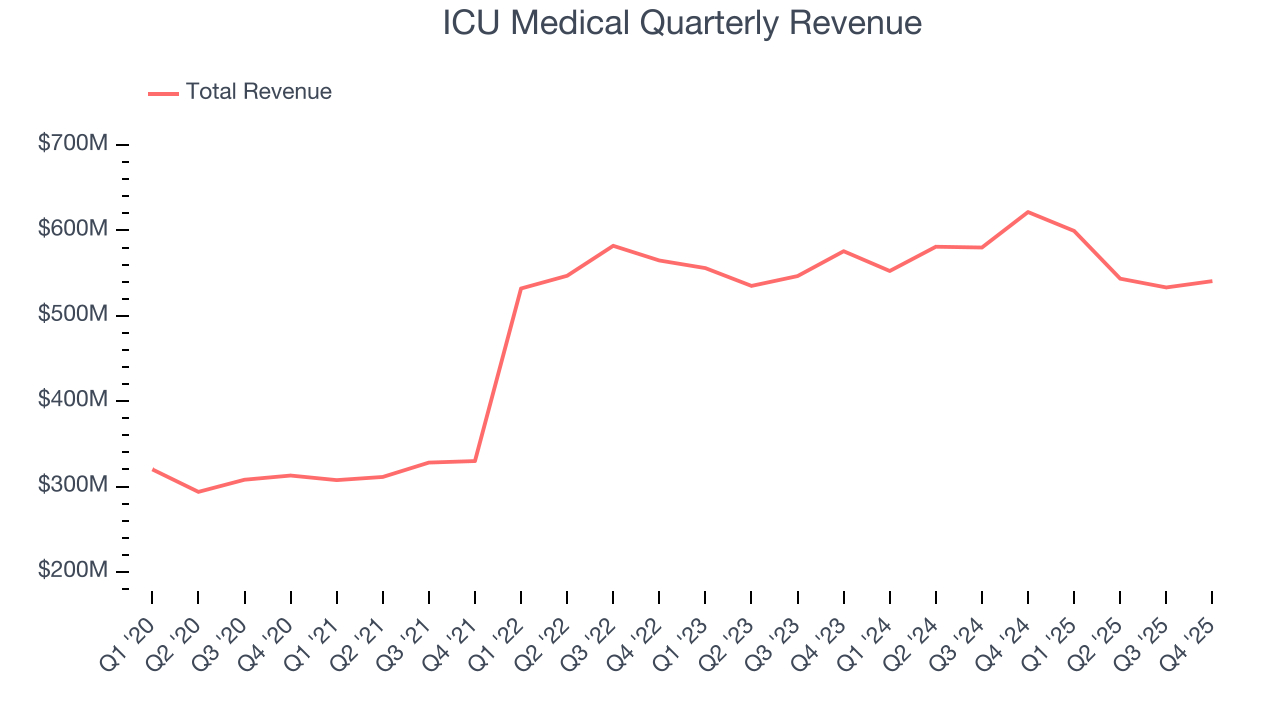

Medical device company ICU Medical (NASDAQ:ICUI) reported Q4 CY2025 results exceeding the market’s revenue expectations, but sales fell by 13% year on year to $540.7 million. Its non-GAAP profit of $1.91 per share was 12.8% above analysts’ consensus estimates.

ICU Medical (ICUI) Q4 CY2025 Highlights:

- Revenue: $540.7 million vs analyst estimates of $530.9 million (13% year-on-year decline, 1.9% beat)

- Adjusted EPS: $1.91 vs analyst estimates of $1.69 (12.8% beat)

- Adjusted EBITDA: $98.19 million vs analyst estimates of $94.75 million (18.2% margin, 3.6% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $8.10 at the midpoint, beating analyst estimates by 1.1%

- EBITDA guidance for the upcoming financial year 2026 is $415 million at the midpoint, in line with analyst expectations

- Operating Margin: 1%, down from 7.4% in the same quarter last year

- Free Cash Flow Margin: 6.6%, up from 2.6% in the same quarter last year

- Market Capitalization: $3.74 billion

Company Overview

Founded in 1984 and named for its initial focus on intensive care units, ICU Medical (NASDAQ:ICUI) develops and manufactures medical products for infusion therapy, vascular access, and vital care applications used in hospitals and other healthcare settings.

ICU Medical's business is organized into three main segments: Consumables, Infusion Systems, and Vital Care. The Consumables division includes products like needlefree connectors, infusion sets, and closed system transfer devices that help healthcare providers safely deliver medications and fluids to patients. These products are designed to reduce the risk of needlestick injuries and prevent exposure to hazardous drugs during preparation and administration.

The Infusion Systems segment features various infusion pumps that precisely control the delivery of medications and fluids. For example, a hospital might use ICU Medical's Plum 360 infusion pump to deliver antibiotics to a patient at an exact rate over a specific time period. This division also includes specialized software that connects with electronic health records to help prevent medication errors.

In the Vital Care segment, ICU Medical offers IV solutions, hemodynamic monitoring systems, and temperature management products. A surgical team might use the company's Level 1 fluid warming system to maintain a patient's body temperature during a lengthy procedure, while critical care nurses might rely on its hemodynamic monitoring systems to track a patient's cardiac output and oxygen delivery.

ICU Medical generates revenue by selling its products to acute care hospitals, ambulatory clinics, and alternate site facilities like home healthcare providers. The company maintains distribution centers across the United States and serves customers in over 100 countries, either through its direct sales force or independent distributors. Beyond simply selling devices, ICU Medical provides implementation and data analytics services to help healthcare facilities optimize their infusion systems.

4. Medical Devices & Supplies - Cardiology, Neurology, Vascular

The medical devices and supplies industry, particularly in the fields of cardiology, neurology, and vascular care, benefits from a business model that balances innovation with relatively predictable revenue streams. These companies focus on developing life-saving devices such as stents, pacemakers, neurostimulation implants, and vascular access tools, which address critical and often chronic conditions. The recurring need for these devices, coupled with growing global demand for advanced treatments, provides stability and opportunities for long-term growth. However, the industry faces hurdles such as high research and development costs, rigorous regulatory approval processes, and reliance on reimbursement from healthcare systems, which can exert downward pressure on pricing. Looking ahead, the industry is positioned to benefit from tailwinds such as aging populations (which tend to have higher rates of disease) and technological advancements like minimally invasive procedures and connected devices that improve patient monitoring and outcomes. Innovations in robotic-assisted surgery and AI-driven diagnostics are also expected to accelerate adoption and expand treatment capabilities. However, potential headwinds include pricing pressures stemming from value-based care models and continued complexity changing from navigating regulatory frameworks that may prioritize further lowering healthcare costs.

ICU Medical's primary competitors include Becton Dickinson (NYSE:BDX), Baxter International (NYSE:BAX), and B. Braun Medical in the consumables and infusion systems markets. In the vital care segment, the company competes with Edwards Lifesciences (NYSE:EW) and Fresenius (ETR:FRE).

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $2.22 billion in revenue over the past 12 months, ICU Medical lacks scale in an industry where it matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, ICU Medical’s 12.4% annualized revenue growth over the last five years was solid. Its growth beat the average healthcare company and shows its offerings resonate with customers.

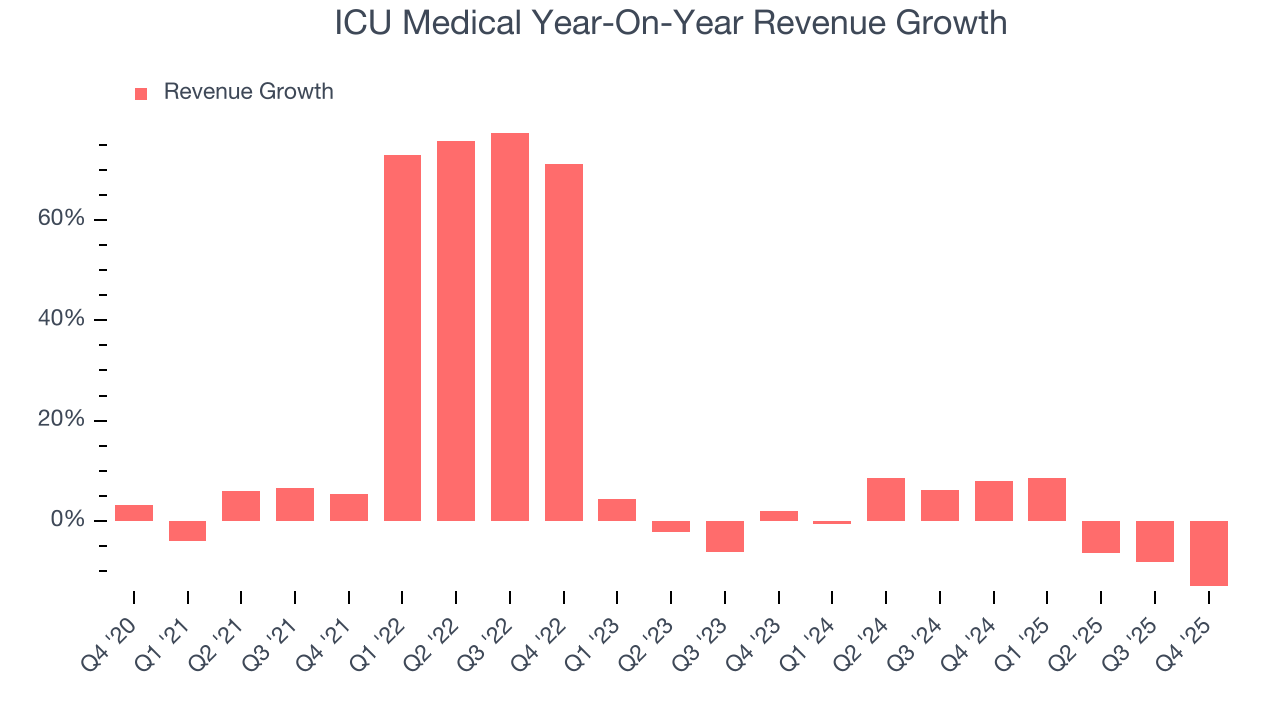

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. ICU Medical’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, ICU Medical’s revenue fell by 13% year on year to $540.7 million but beat Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to decline by 3.4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

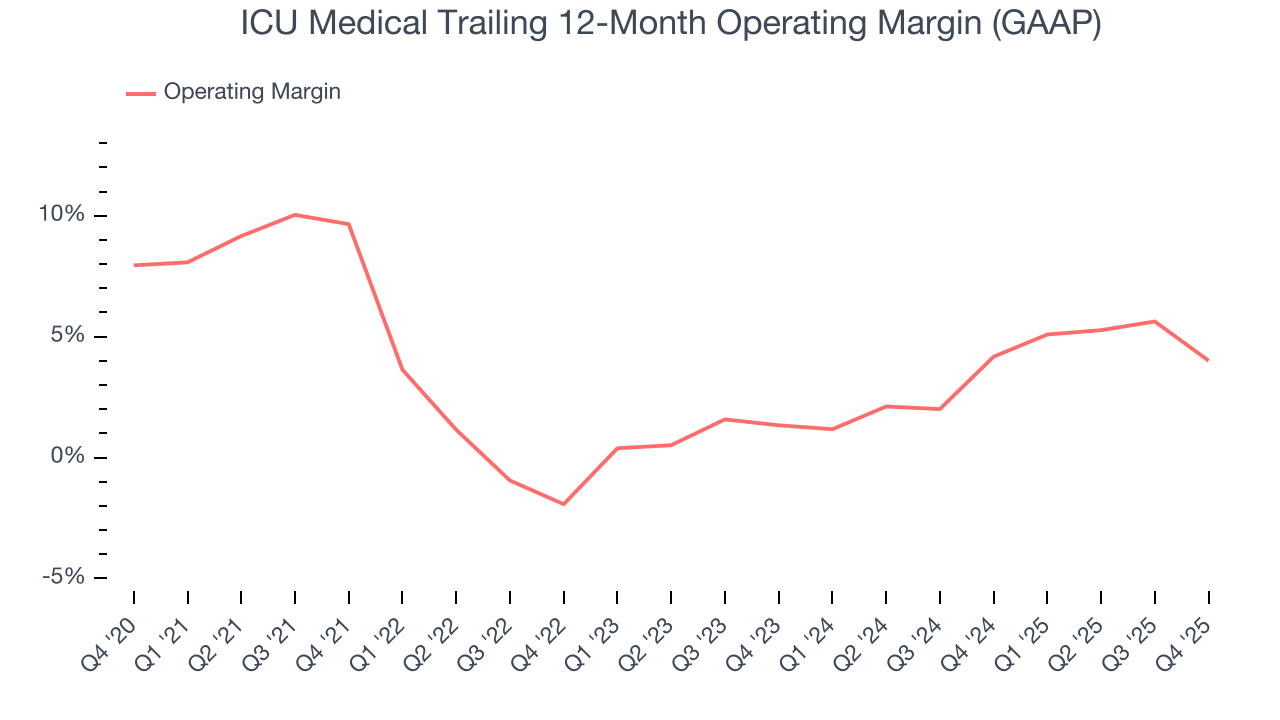

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

ICU Medical was profitable over the last five years but held back by its large cost base. Its average operating margin of 2.9% was weak for a healthcare business.

Analyzing the trend in its profitability, ICU Medical’s operating margin decreased by 5.6 percentage points over the last five years, but it rose by 2.7 percentage points on a two-year basis. Still, shareholders will want to see ICU Medical become more profitable in the future.

This quarter, ICU Medical generated an operating margin profit margin of 1%, down 6.4 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

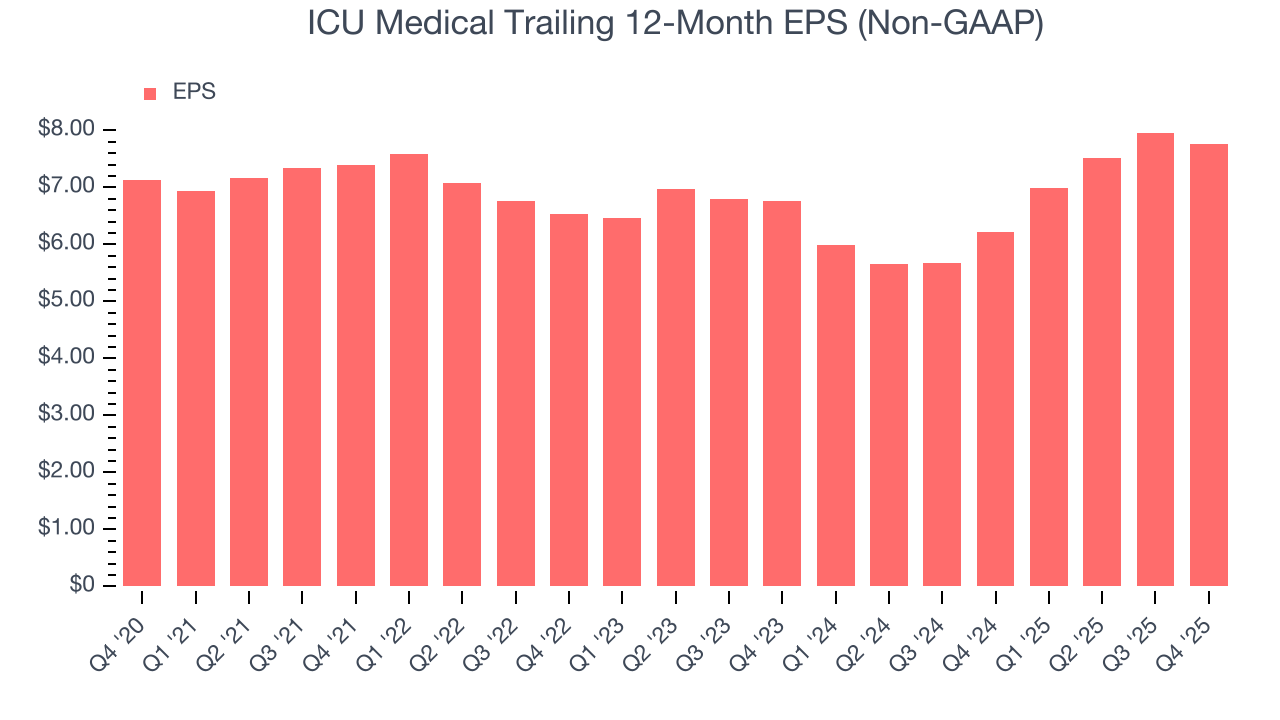

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

ICU Medical’s EPS grew at an unimpressive 1.7% compounded annual growth rate over the last five years, lower than its 12.4% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

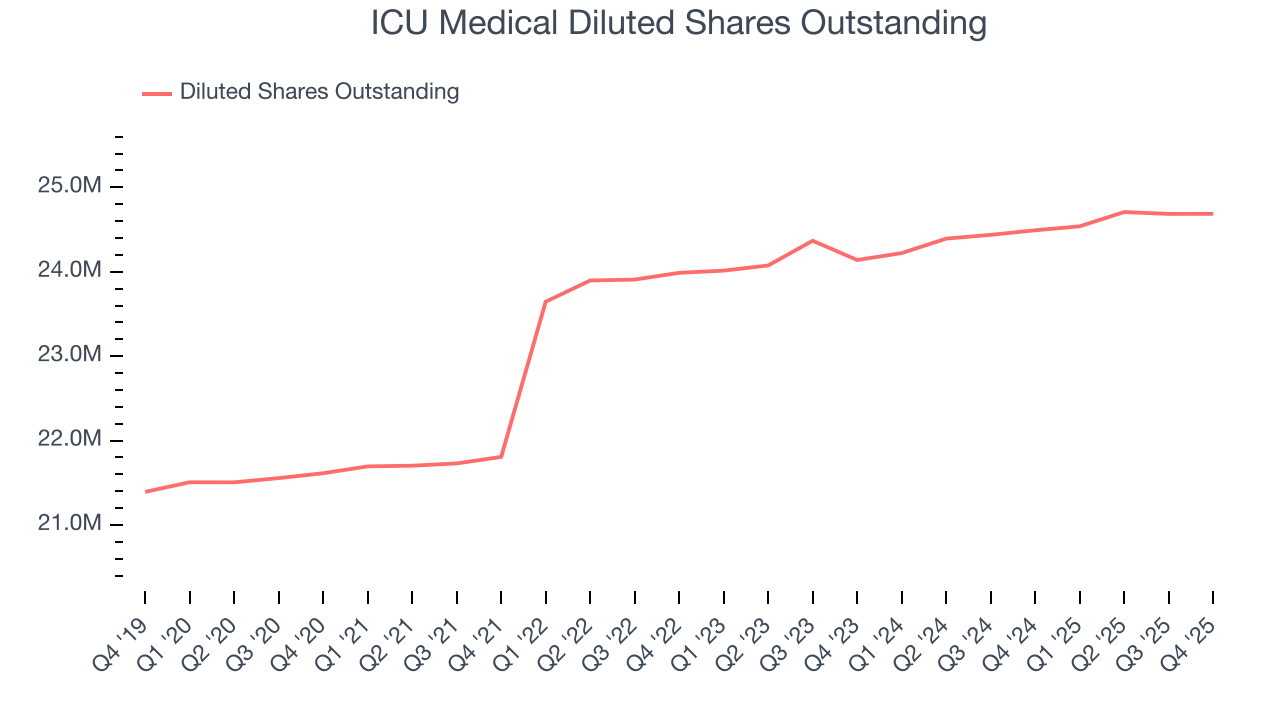

We can take a deeper look into ICU Medical’s earnings to better understand the drivers of its performance. As we mentioned earlier, ICU Medical’s operating margin declined by 5.6 percentage points over the last five years. Its share count also grew by 14.2%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, ICU Medical reported adjusted EPS of $1.91, down from $2.11 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects ICU Medical’s full-year EPS of $7.76 to grow 2.4%.

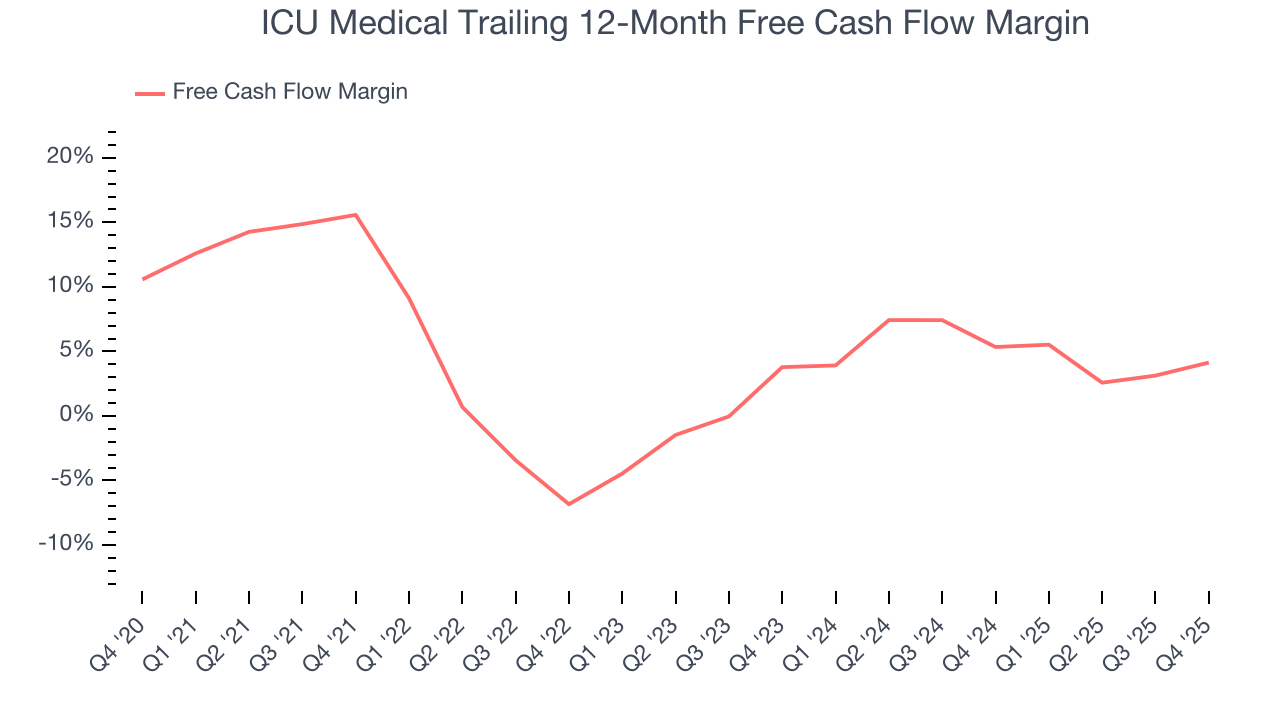

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

ICU Medical has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.4%, subpar for a healthcare business.

Taking a step back, we can see that ICU Medical’s margin dropped by 11.4 percentage points during that time. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s becoming a more capital-intensive business.

ICU Medical’s free cash flow clocked in at $35.95 million in Q4, equivalent to a 6.6% margin. This result was good as its margin was 4.1 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

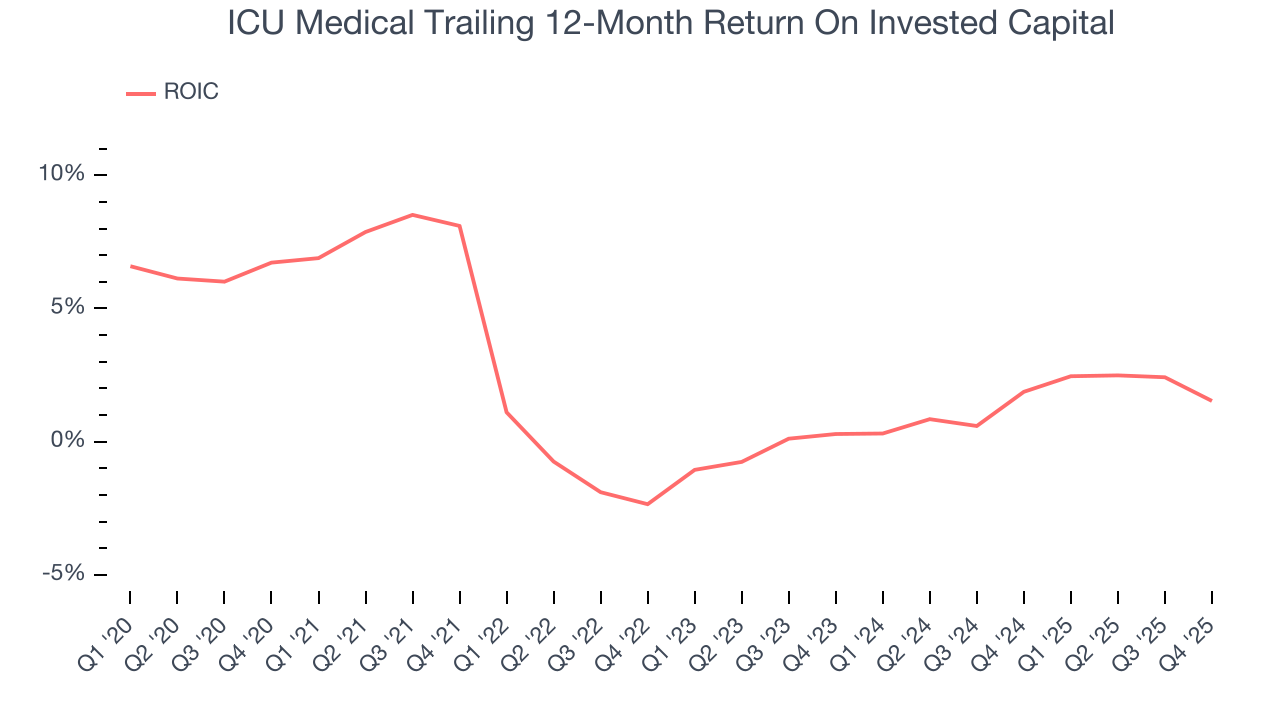

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

ICU Medical historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 1.9%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, ICU Medical’s ROIC averaged 1.2 percentage point decreases each year over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Assessment

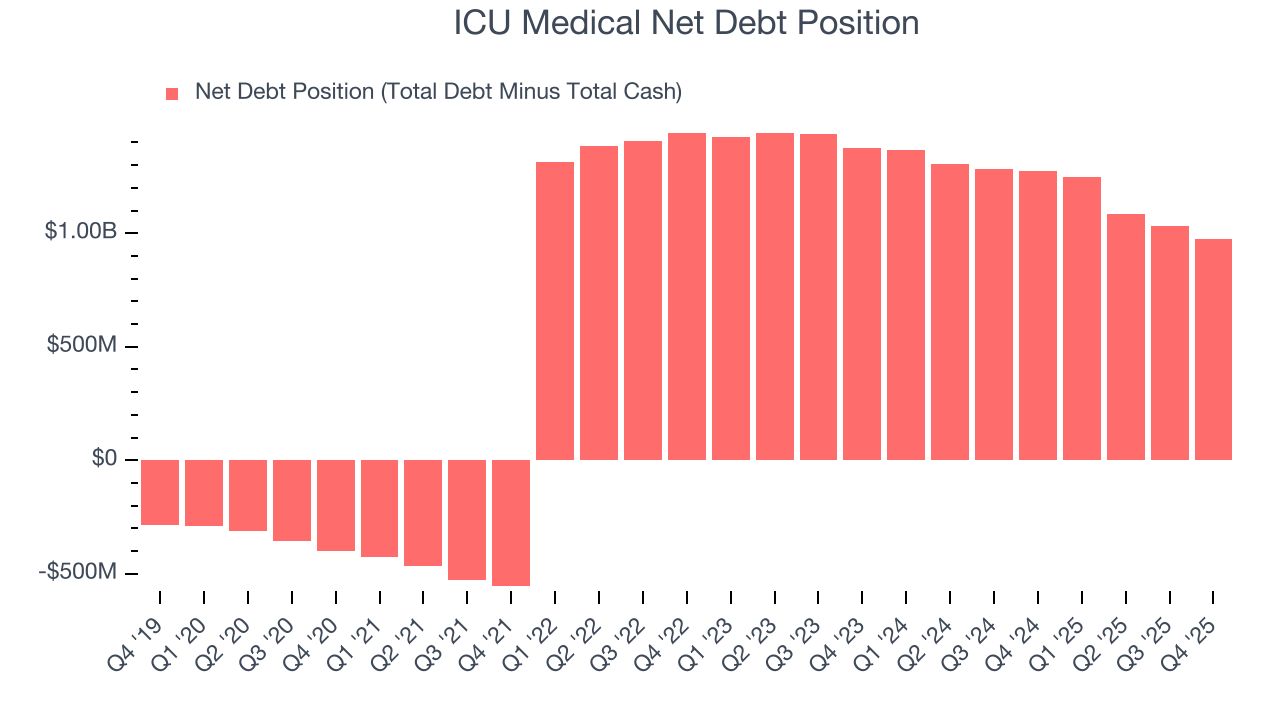

ICU Medical reported $308 million of cash and $1.28 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $403.8 million of EBITDA over the last 12 months, we view ICU Medical’s 2.4× net-debt-to-EBITDA ratio as safe. We also see its $83.03 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from ICU Medical’s Q4 Results

It was good to see ICU Medical beat analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $149.95 immediately following the results.

13. Is Now The Time To Buy ICU Medical?

Updated: March 15, 2026 at 12:00 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in ICU Medical.

ICU Medical isn’t a terrible business, but it doesn’t pass our quality test. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its cash profitability fell over the last five years. And while the company’s operating margins are in line with the overall healthcare sector, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

ICU Medical’s P/E ratio based on the next 12 months is 15.9x. Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $182.67 on the company (compared to the current share price of $125.99).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.