KLA Corporation (KLAC)

We’d invest in KLA Corporation. Its fusion of high growth and profitability makes it an unstoppable force with big upside.― StockStory Analyst Team

1. News

2. Summary

Why We Like KLA Corporation

Formed by the 1997 merger of the two leading semiconductor yield management companies, KLA Corporation (NASDAQ:KLAC) is the leading supplier of equipment used to measure and inspect semiconductor chips.

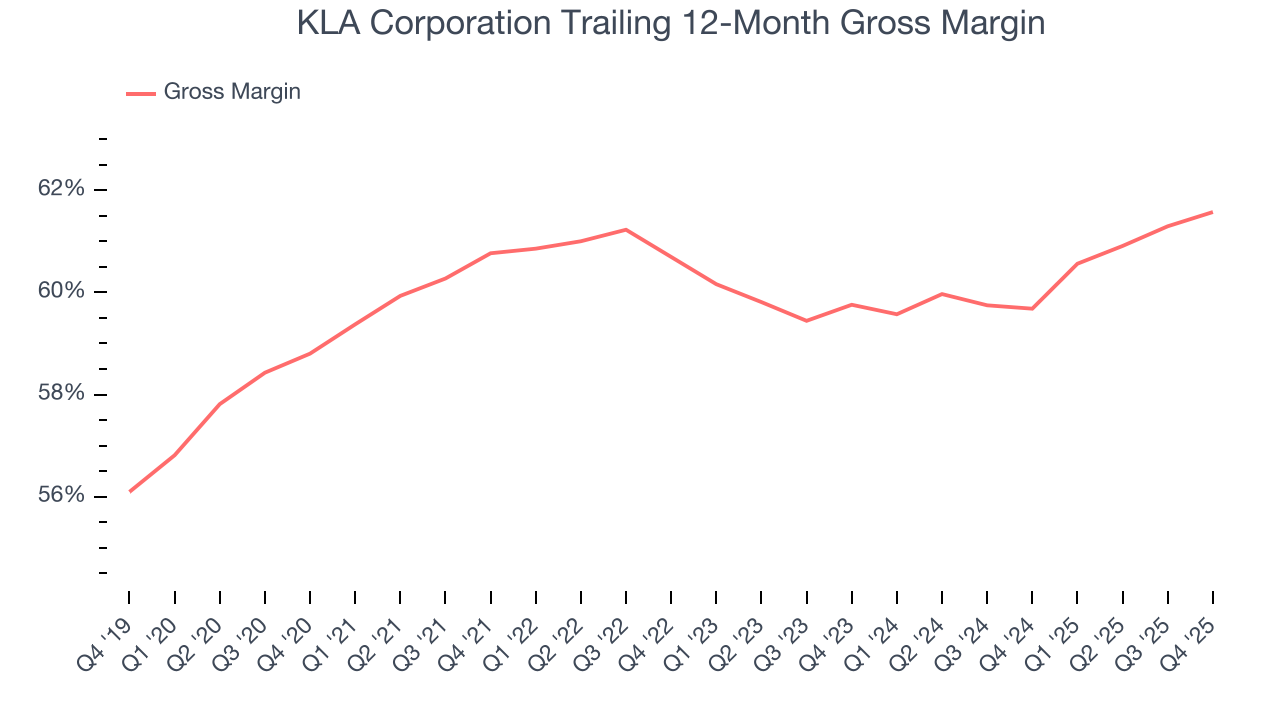

- Offerings are difficult to replicate at scale and result in a best-in-class gross margin of 60.7%

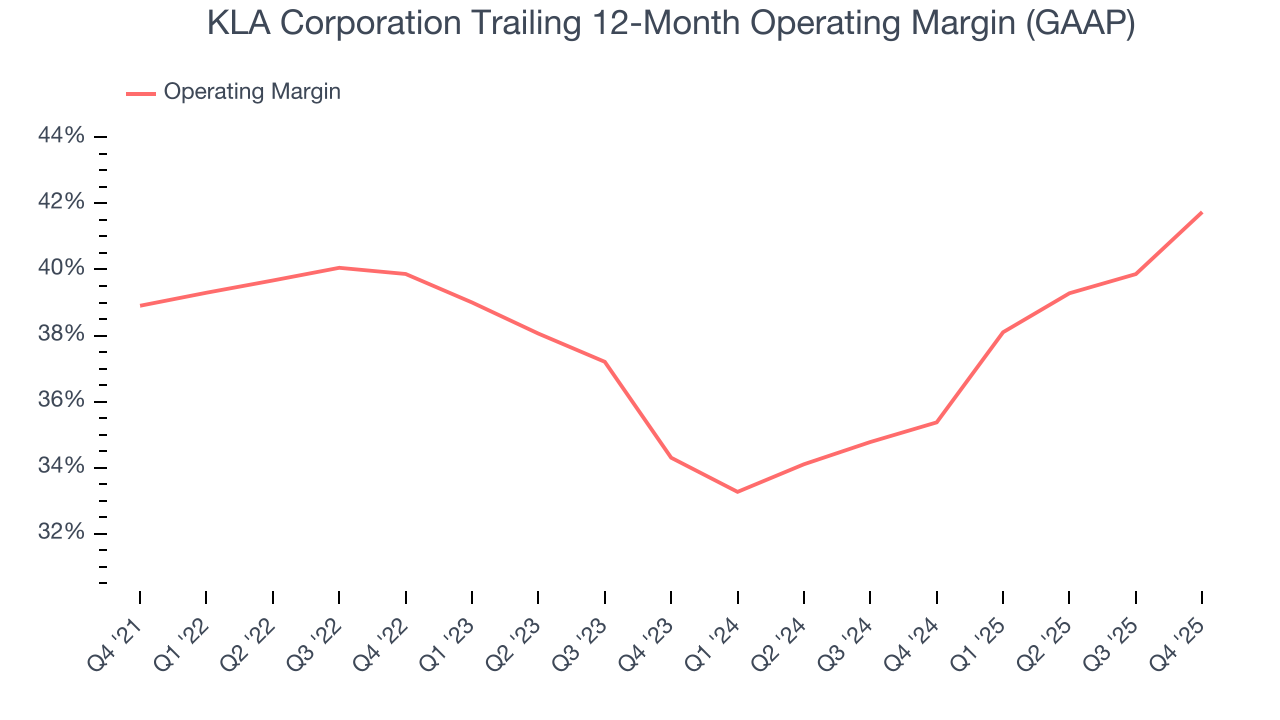

- Excellent operating margin highlights the strength of its business model, and its profits increased over the last five years as it scaled

- Robust free cash flow profile gives it the flexibility to invest in growth initiatives or return capital to shareholders, and its recently improved profitability means it has even more resources to invest or distribute

We’re optimistic about KLA Corporation. The price looks fair relative to its quality, so this might be a favorable time to buy some shares.

Why Is Now The Time To Buy KLA Corporation?

At $1,521 per share, KLA Corporation trades at 37.1x forward P/E. This valuation is fair - even cheap depending on how much you like the story - for the quality you get.

Entry price matters much less than business quality when investing for the long term, but hey, it certainly doesn’t hurt to get in at an attractive price.

3. KLA Corporation (KLAC) Research Report: Q4 CY2025 Update

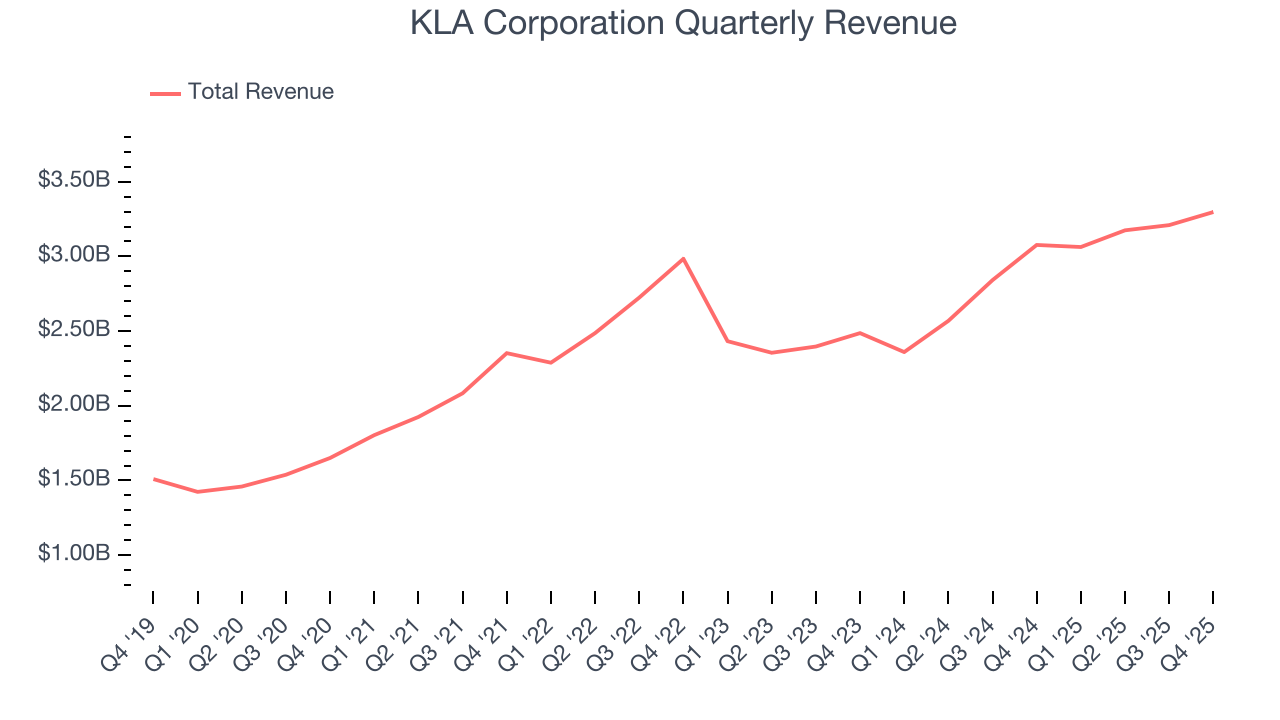

Semiconductor manufacturing equipment maker KLA Corporation (NASDAQ:KLAC) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 7.2% year on year to $3.30 billion. Guidance for next quarter’s revenue was better than expected at $3.35 billion at the midpoint, 1.9% above analysts’ estimates. Its non-GAAP profit of $8.85 per share was 0.6% above analysts’ consensus estimates.

KLA Corporation (KLAC) Q4 CY2025 Highlights:

- Revenue: $3.30 billion vs analyst estimates of $3.26 billion (7.2% year-on-year growth, 1.3% beat)

- Adjusted EPS: $8.85 vs analyst estimates of $8.80 (0.6% beat)

- Adjusted EBITDA: $1.50 billion vs analyst estimates of $1.46 billion (45.6% margin, 3% beat)

- Revenue Guidance for Q1 CY2026 is $3.35 billion at the midpoint, above analyst estimates of $3.29 billion

- Adjusted EPS guidance for Q1 CY2026 is $9.08 at the midpoint, above analyst estimates of $8.98

- Operating Margin: 40.3%, up from 32.6% in the same quarter last year

- Free Cash Flow Margin: 38.3%, up from 24.6% in the same quarter last year

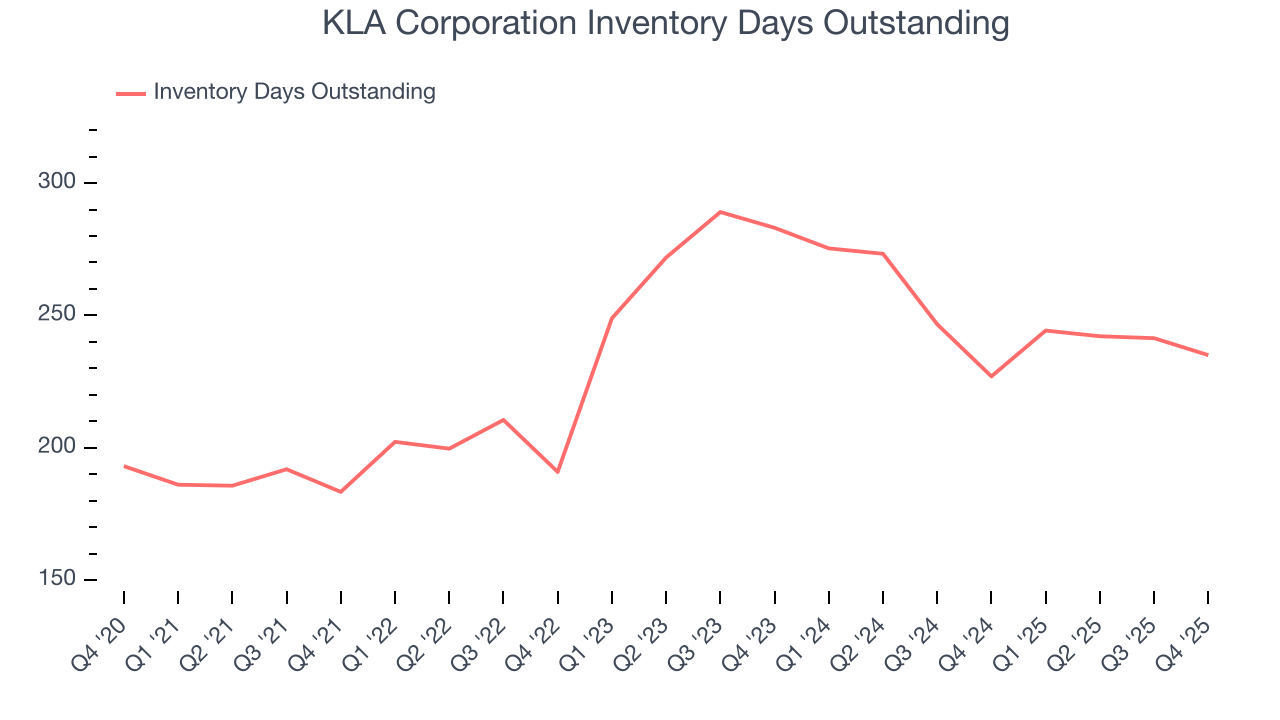

- Inventory Days Outstanding: 235, down from 241 in the previous quarter

- Market Capitalization: $213.8 billion

Company Overview

Formed by the 1997 merger of the two leading semiconductor yield management companies, KLA Corporation (NASDAQ:KLAC) is the leading supplier of equipment used to measure and inspect semiconductor chips.

KLA sells the tools used by semiconductor foundries and memory chip producers to inspect semiconductors and measure their precise dimensions throughout the manufacturing process, from the wafers to patterning to final production. Today, accuracy and defect detection in the semiconductor manufacturing process is becoming even more crucial as chip sizes continue to shrink, making it increasingly difficult to find defects. As the cost to create chips has gone up, even a small irregularity early on in the manufacturing process can render a chip useless, costing companies time and money.

KLA is the dominant provider of process control systems, maintaining around 50% market share for more than a decade, or 4x its closest competitor. It works closely with its customers to develop specific tools for specific semiconductor manufacturing processes. In recent years it has looked to expand its addressable market and the 2019 acquisition of Orbotech extended its business into printed circuit boards and flat panel displays.

KLAC's primary peers and competitors are Applied Materials (NASDAQ:AMAT), ASML (NASDAQ:ASML) Lam Research (NASDA:LCRX), and Tokyo Electron (TSE:8035).

4. Semiconductor Manufacturing

The semiconductor capital (manufacturing) equipment group has become highly concentrated over the past decade. Suppliers have consolidated, and the increasing cost of innovation have made it unaffordable to almost everybody, except the largest companies, to produce leading edge chips. The result of the increased industry concentration has been higher operating margins and free cash generation through the cycle. Despite this structural improvement, the businesses can still be quite volatile, as demand fluctuations for the semiconductor equipment are magnified by the already cyclical nature of underlying semiconductor demand.

5. Revenue Growth

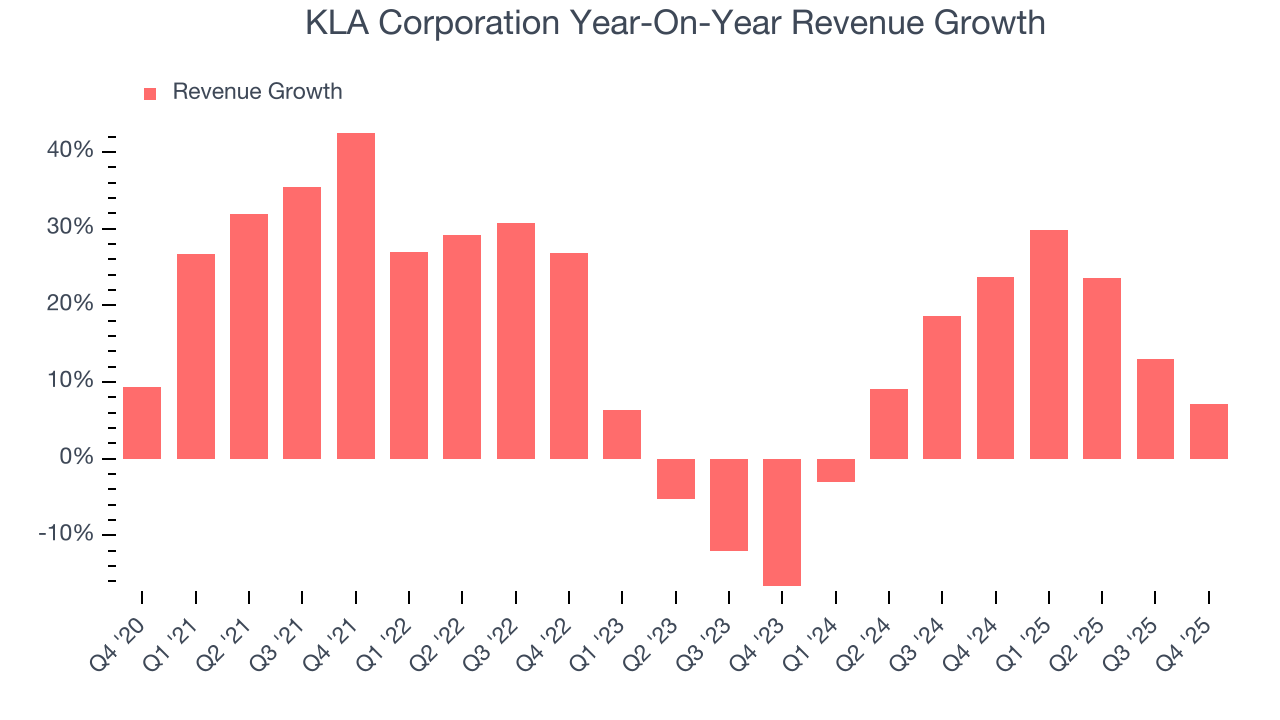

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, KLA Corporation’s sales grew at an impressive 16% compounded annual growth rate over the last five years. Its growth surpassed the average semiconductor company and shows its offerings resonate with customers, a great starting point for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. KLA Corporation’s annualized revenue growth of 14.8% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, KLA Corporation reported year-on-year revenue growth of 7.2%, and its $3.30 billion of revenue exceeded Wall Street’s estimates by 1.3%. Despite the beat, this was its third consecutive quarter of decelerating growth, indicating a potential cyclical downturn. Company management is currently guiding for a 9.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 11.8% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

6. Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, KLA Corporation’s DIO came in at 235, which is 4 days above its five-year average. These numbers suggest that despite the recent decrease, the company’s inventory levels are higher than what we’ve seen in the past.

7. Gross Margin & Pricing Power

Gross profit margin is a key metric to track because it shows how much money a semiconductor company gets to keep after paying for its raw materials, manufacturing, and other input costs.

KLA Corporation’s gross margin is one of the best in the semiconductor sector, and its differentiated products give it strong pricing power. As you can see below, it averaged an elite 60.7% gross margin over the last two years. Said differently, roughly $60.70 was left to spend on selling, marketing, R&D, and general administrative overhead for every $100 in revenue.

KLA Corporation’s gross profit margin came in at 61.4% this quarter, marking a 1.1 percentage point increase from 60.3% in the same quarter last year. KLA Corporation’s full-year margin has also been trending up over the past 12 months, increasing by 1.9 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

8. Operating Margin

KLA Corporation has been a well-oiled machine over the last two years. It demonstrated elite profitability for a semiconductor business, boasting an average operating margin of 38.8%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, KLA Corporation’s operating margin rose by 2.8 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, KLA Corporation generated an operating margin profit margin of 40.3%, up 7.7 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

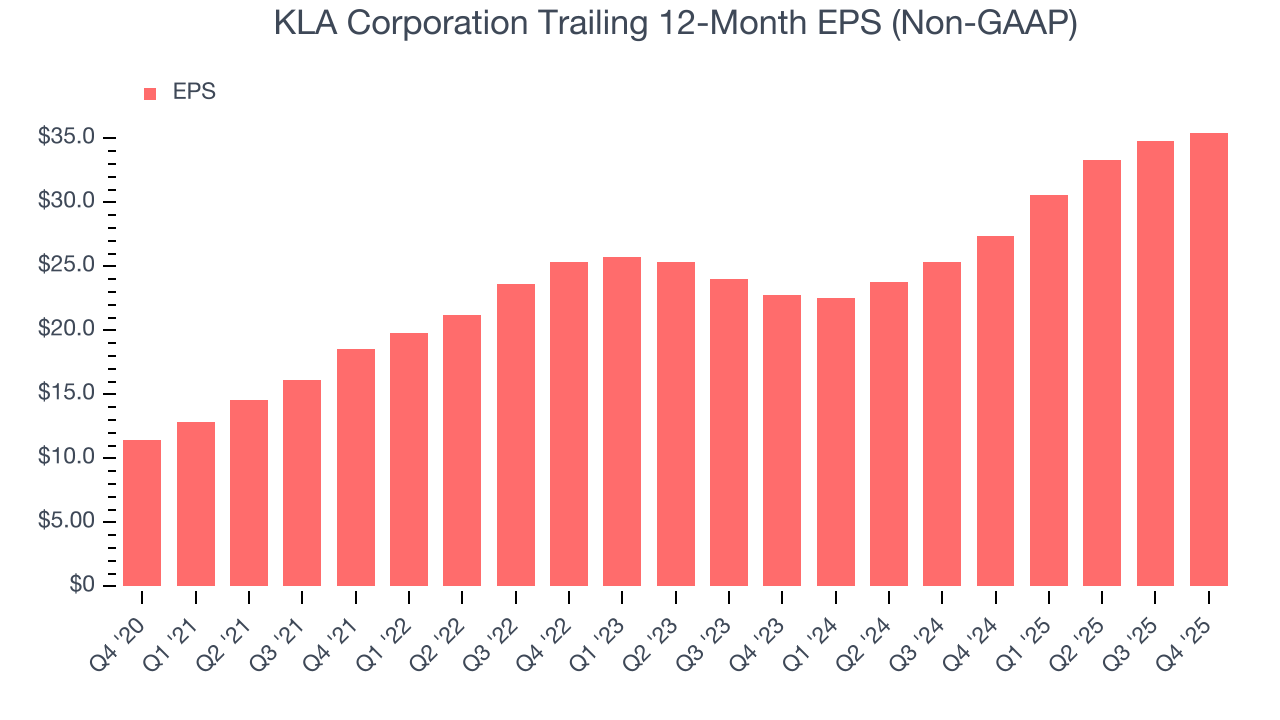

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

KLA Corporation’s EPS grew at a remarkable 25.3% compounded annual growth rate over the last five years, higher than its 16% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

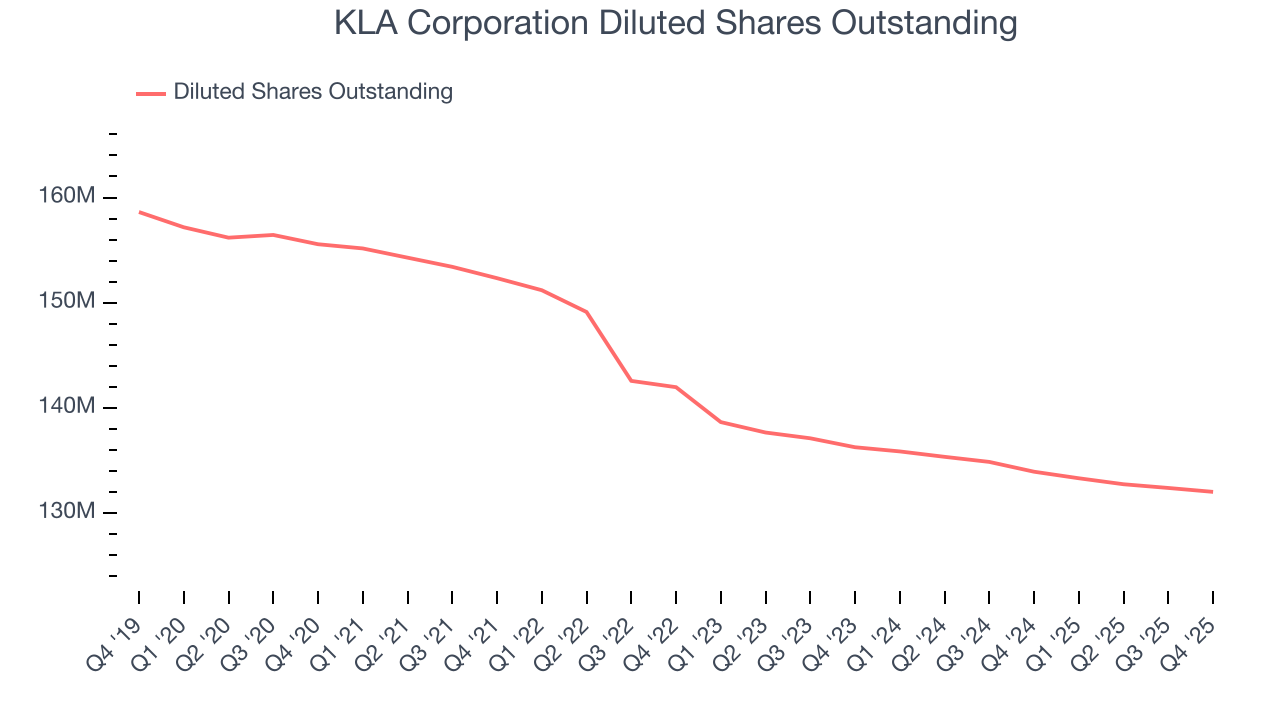

We can take a deeper look into KLA Corporation’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, KLA Corporation’s operating margin expanded by 2.8 percentage points over the last five years. On top of that, its share count shrank by 15.1%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q4, KLA Corporation reported adjusted EPS of $8.85, up from $8.20 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects KLA Corporation’s full-year EPS of $35.45 to grow 14.6%.

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

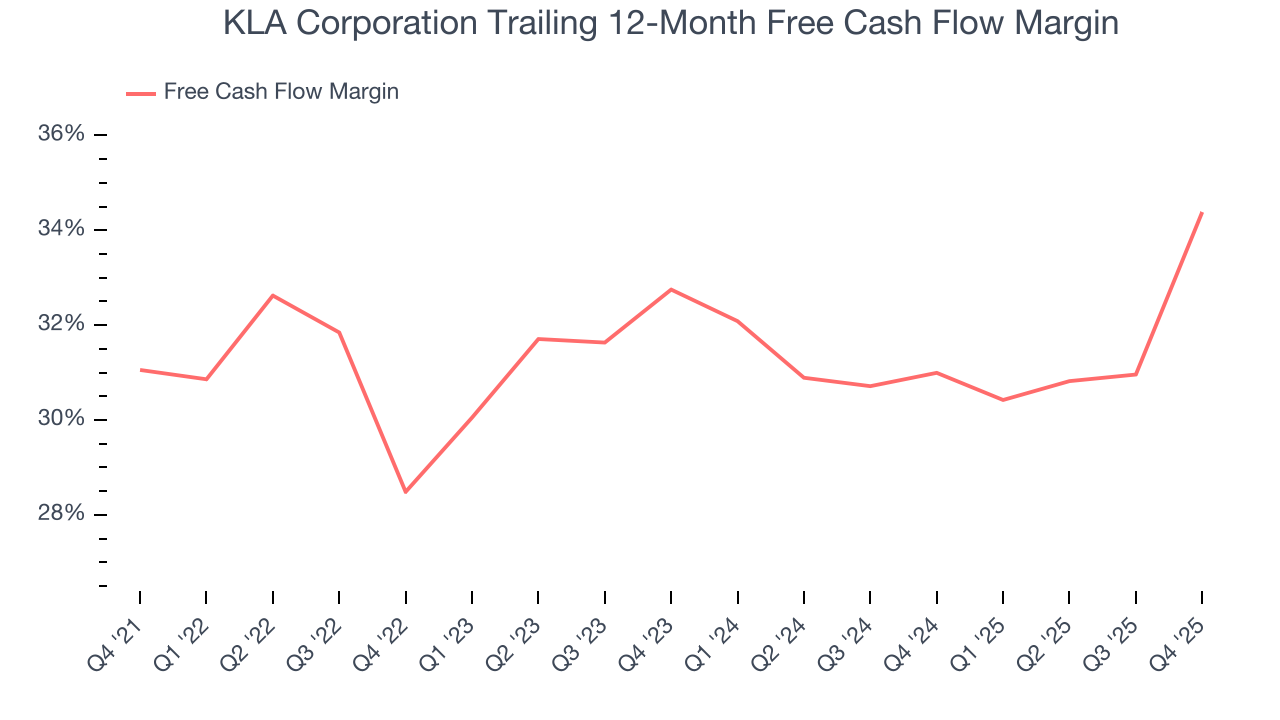

KLA Corporation has shown terrific cash profitability, and if sustainable, puts it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the semiconductor sector, averaging an eye-popping 32.8% over the last two years.

Taking a step back, we can see that KLA Corporation’s margin expanded by 3.3 percentage points over the last five years. This is encouraging because it gives the company more optionality.

KLA Corporation’s free cash flow clocked in at $1.26 billion in Q4, equivalent to a 38.3% margin. This result was good as its margin was 13.7 percentage points higher than in the same quarter last year, building on its favorable historical trend.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

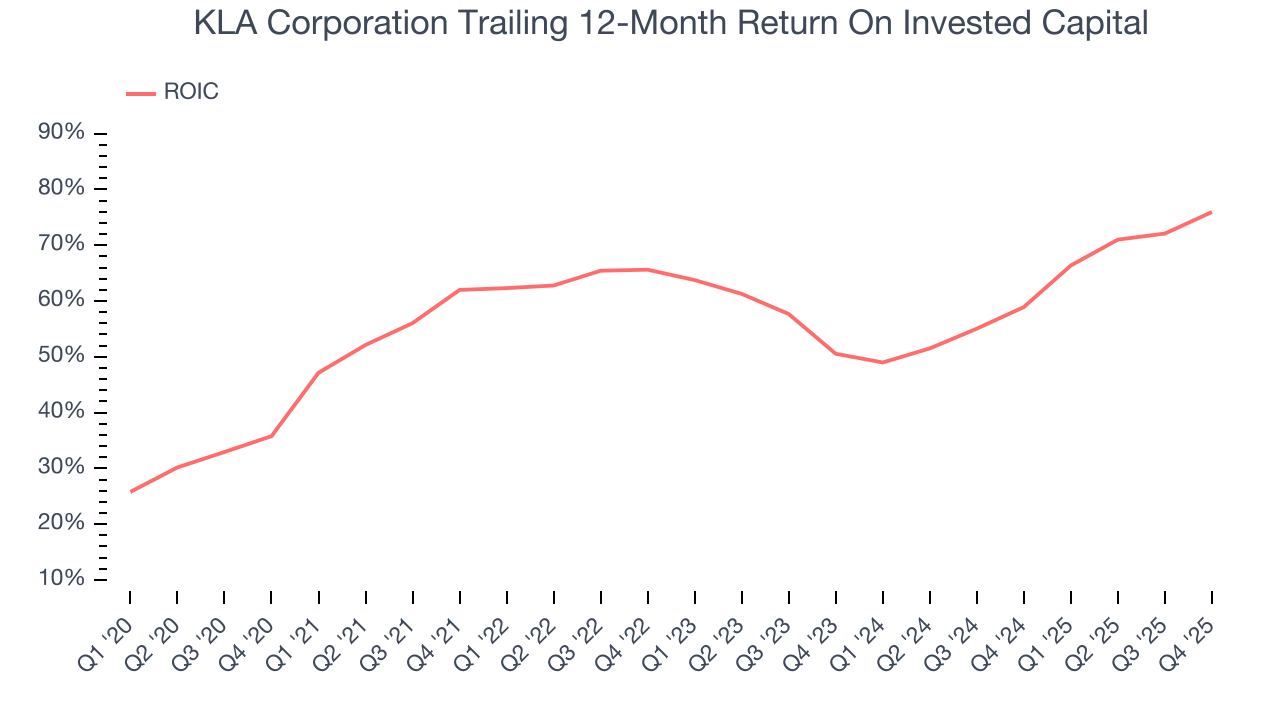

KLA Corporation’s five-year average ROIC was 62.6%, placing it among the best semiconductor companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

12. Balance Sheet Assessment

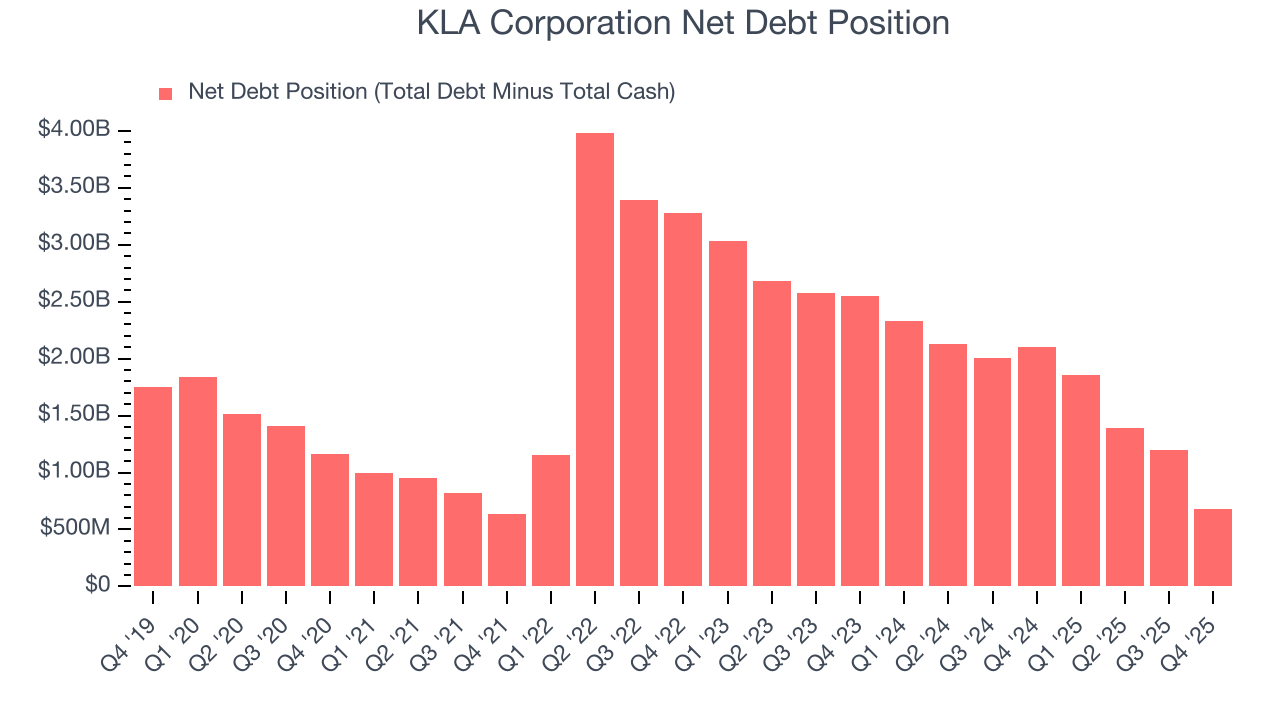

KLA Corporation reported $5.21 billion of cash and $5.89 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $5.91 billion of EBITDA over the last 12 months, we view KLA Corporation’s 0.1× net-debt-to-EBITDA ratio as safe. We also see its $33.86 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from KLA Corporation’s Q4 Results

It was encouraging to see KLA Corporation’s revenue guidance for next quarter beat analysts’ expectations. We were also glad its inventory levels shrunk. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 3.7% to $1,628 immediately following the results.

14. Is Now The Time To Buy KLA Corporation?

Updated: March 1, 2026 at 9:23 PM EST

Before making an investment decision, investors should account for KLA Corporation’s business fundamentals and valuation in addition to what happened in the latest quarter.

KLA Corporation is an amazing business ranking highly on our list. For starters, its revenue growth was impressive over the last five years, and analysts believe it can continue growing at these levels. On top of that, its admirable gross margins indicate robust pricing power, and its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits.

KLA Corporation’s P/E ratio based on the next 12 months is 37.1x. Scanning the semiconductor space today, KLA Corporation’s fundamentals really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $1,667 on the company (compared to the current share price of $1,519), implying they see 9.8% upside in buying KLA Corporation in the short term.