MongoDB (MDB)

MongoDB is intriguing. Its elite ARR growth suggests it not only generates recurring revenue but also is winning market share.― StockStory Analyst Team

1. News

2. Summary

Why MongoDB Is Interesting

Named after "humongous database," reflecting its ability to handle massive data loads, MongoDB (NASDAQ:MDB) provides a flexible document-based database platform that helps developers build, deploy, and maintain modern applications more efficiently.

- ARR trends over the last year show it’s maintaining a steady flow of long-term contracts that contribute positively to its revenue predictability

- Annual revenue growth of 33.1% over the past five years was outstanding, reflecting market share gains

- One pitfall is its operating profits and efficiency rose over the last year as it benefited from some fixed cost leverage

MongoDB shows some promise. If you like the story, the price seems fair.

Why Is Now The Time To Buy MongoDB?

MongoDB’s stock price of $259.55 implies a valuation ratio of 7.3x forward price-to-sales. MongoDB’s valuation is higher than that of many in the software space, sure. However, we still think the valuation is justified given the top-line growth.

It could be a good time to invest if you see something the market doesn’t.

3. MongoDB (MDB) Research Report: Q4 CY2025 Update

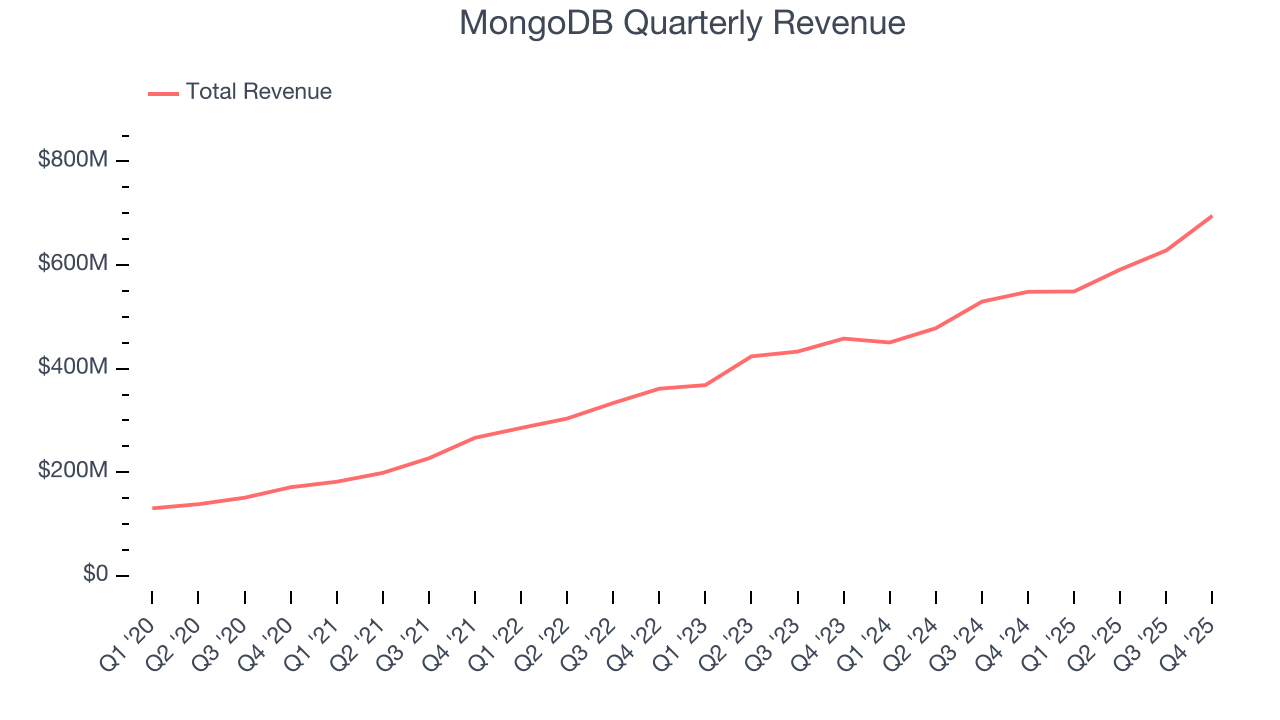

Database platform company MongoDB (NASDAQ:MDB) announced better-than-expected revenue in Q4 CY2025, with sales up 26.7% year on year to $695.1 million. The company expects next quarter’s revenue to be around $661.5 million, close to analysts’ estimates. Its non-GAAP profit of $1.65 per share was 12.1% above analysts’ consensus estimates.

MongoDB (MDB) Q4 CY2025 Highlights:

- Revenue: $695.1 million vs analyst estimates of $670.3 million (26.7% year-on-year growth, 3.7% beat)

- Adjusted EPS: $1.65 vs analyst estimates of $1.47 (12.1% beat)

- Adjusted Operating Income: $158.8 million vs analyst estimates of $142.6 million (22.8% margin, 11.3% beat)

- Revenue Guidance for Q1 CY2026 is $661.5 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2027 is $5.84 at the midpoint, beating analyst estimates by 2.4%

- Operating Margin: 0%, up from -3.4% in the same quarter last year

- Free Cash Flow Margin: 25.4%, up from 22.3% in the previous quarter

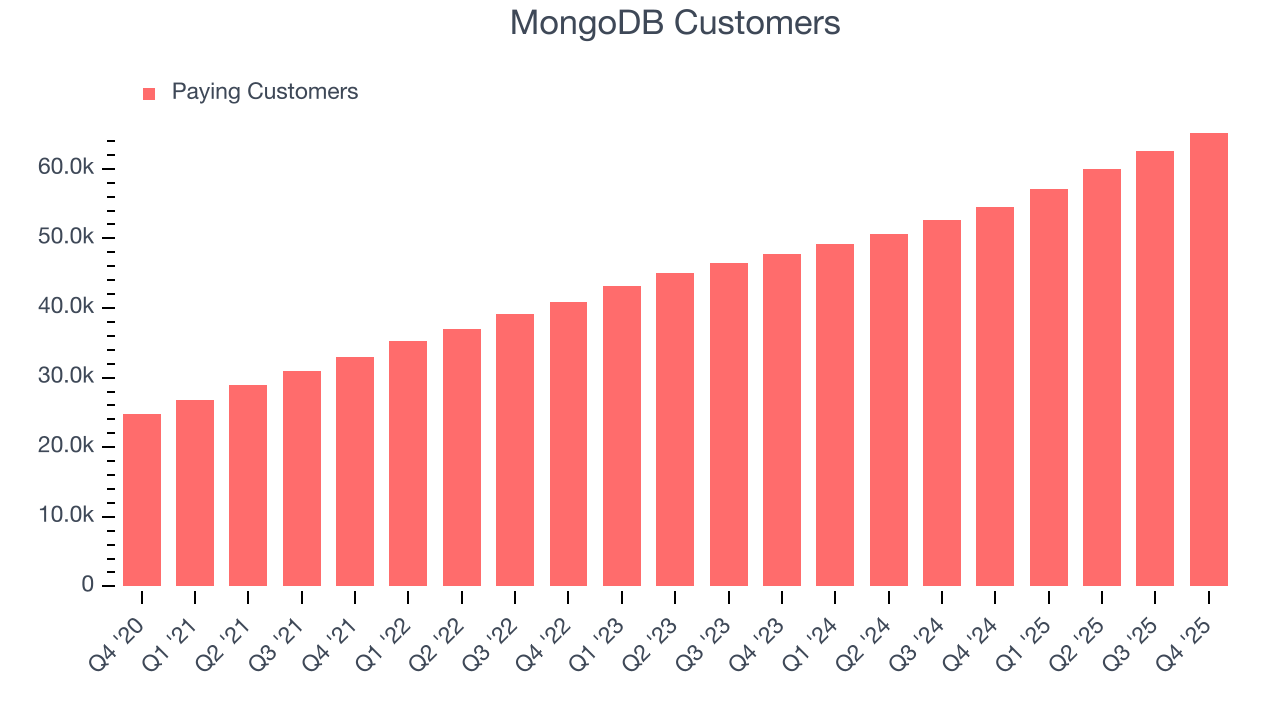

- Customers: 65,200, up from 62,500 in the previous quarter

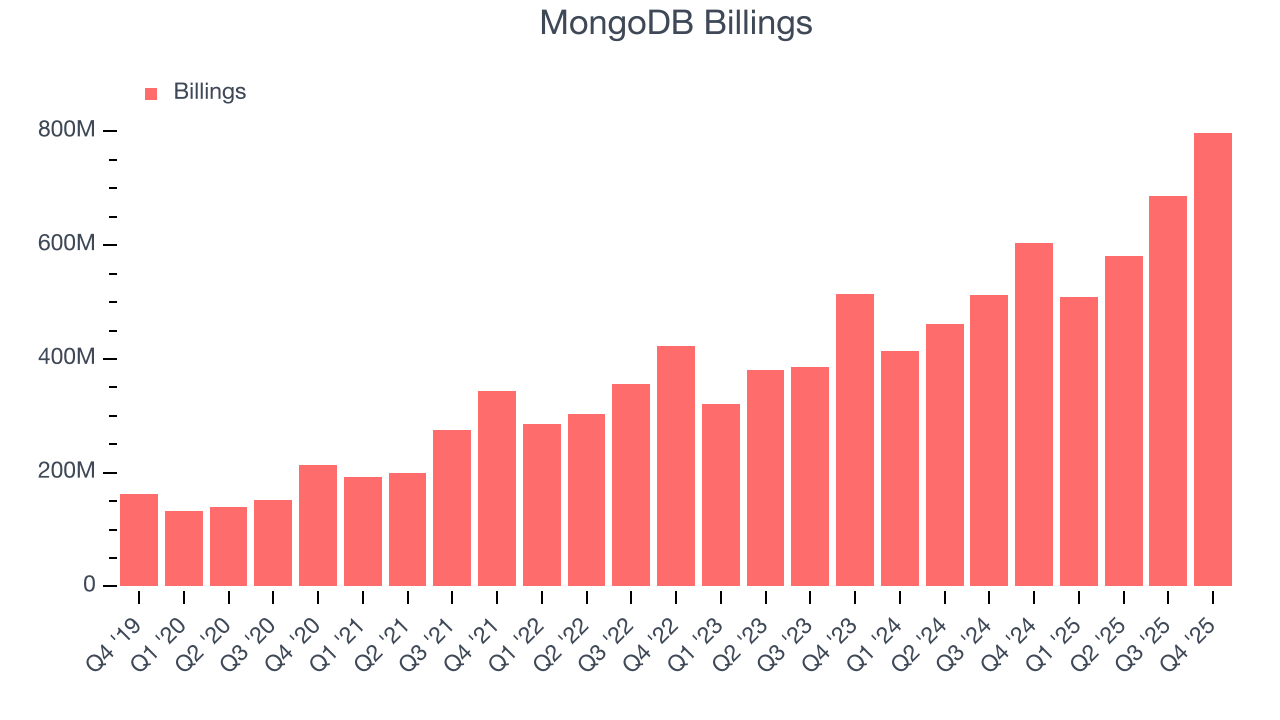

- Billings: $798 million at quarter end, up 32.3% year on year

- Market Capitalization: $26.73 billion

Company Overview

Named after "humongous database," reflecting its ability to handle massive data loads, MongoDB (NASDAQ:MDB) provides a flexible document-based database platform that helps developers build, deploy, and maintain modern applications more efficiently.

MongoDB's platform bridges the gap between traditional relational databases and newer non-relational approaches, offering the flexibility developers need for modern applications while maintaining the reliability businesses demand. Its document-based architecture allows information to be stored in JSON-like formats that more naturally align with how developers work with data in their code.

Customers can deploy MongoDB in multiple ways: as a fully-managed cloud service (MongoDB Atlas), which MongoDB operates across major cloud providers like AWS, Google Cloud, and Microsoft Azure, or as self-managed software (MongoDB Enterprise Advanced) that organizations can run themselves in the cloud or on-premises.

The company has expanded beyond its core database functionality to offer an integrated developer data platform with capabilities for search, vector search for AI applications, time series data processing, data lifecycle management, and edge computing. This comprehensive approach allows organizations to reduce the number of specialized data technologies they need to maintain.

A typical MongoDB customer might be a retail company using the platform to power its e-commerce application, storing product information, customer profiles, and transaction data while leveraging Atlas Vector Search to enable AI-powered product recommendations based on customer behavior patterns.

4. Data Storage

Data is the lifeblood of the internet and software in general, and the amount of data created is accelerating. As a result, the importance of storing the data in scalable and efficient formats continues to rise, especially as its diversity and associated use cases expand from analyzing simple, structured datasets to high-scale processing of unstructured data such as images, audio, and video.

MongoDB competes with established legacy database providers like Oracle (NYSE:ORCL), Microsoft (NASDAQ:MSFT), and IBM (NYSE:IBM), as well as cloud providers offering database services including Amazon Web Services (NASDAQ:AMZN), Google Cloud (NASDAQ:GOOGL), and Microsoft Azure. Other competitors include specialized database vendors like Couchbase (NASDAQ:BASE) and Redis (NASDAQ:REDI).

5. Revenue Growth

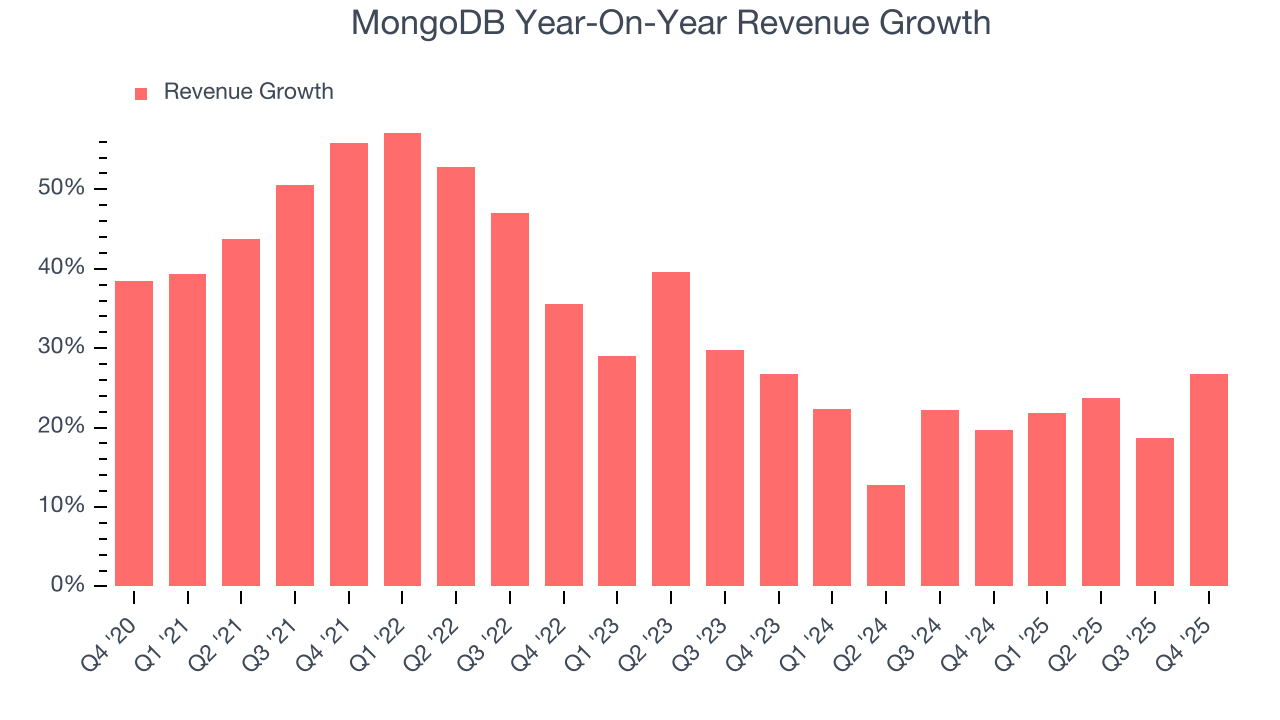

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, MongoDB’s 33.1% annualized revenue growth over the last five years was excellent. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. MongoDB’s annualized revenue growth of 21% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, MongoDB reported robust year-on-year revenue growth of 26.7%, and its $695.1 million of revenue topped Wall Street estimates by 3.7%. Company management is currently guiding for a 20.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 17.4% over the next 12 months, a deceleration versus the last two years. Still, this projection is admirable and implies the market is forecasting success for its products and services.

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

MongoDB’s billings punched in at $798 million in Q4, and over the last four quarters, its growth was fantastic as it averaged 28.9% year-on-year increases. This alternate topline metric grew faster than total sales, meaning the company collects cash upfront and then recognizes the revenue over the length of its contracts - a boost for its liquidity and future revenue prospects.

7. Customer Base

MongoDB reported 65,200 customers at the end of the quarter, a sequential increase of 2,700. That’s roughly in line with what we’ve observed over the last year, confirming that the company is maintaining its sales momentum.

8. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for MongoDB to acquire new customers as its CAC payback period checked in at 378.8 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a competitive market. A silver lining is that once it acquires its customers, they typically don’t leave and increase their spending - a sign of high switching costs.

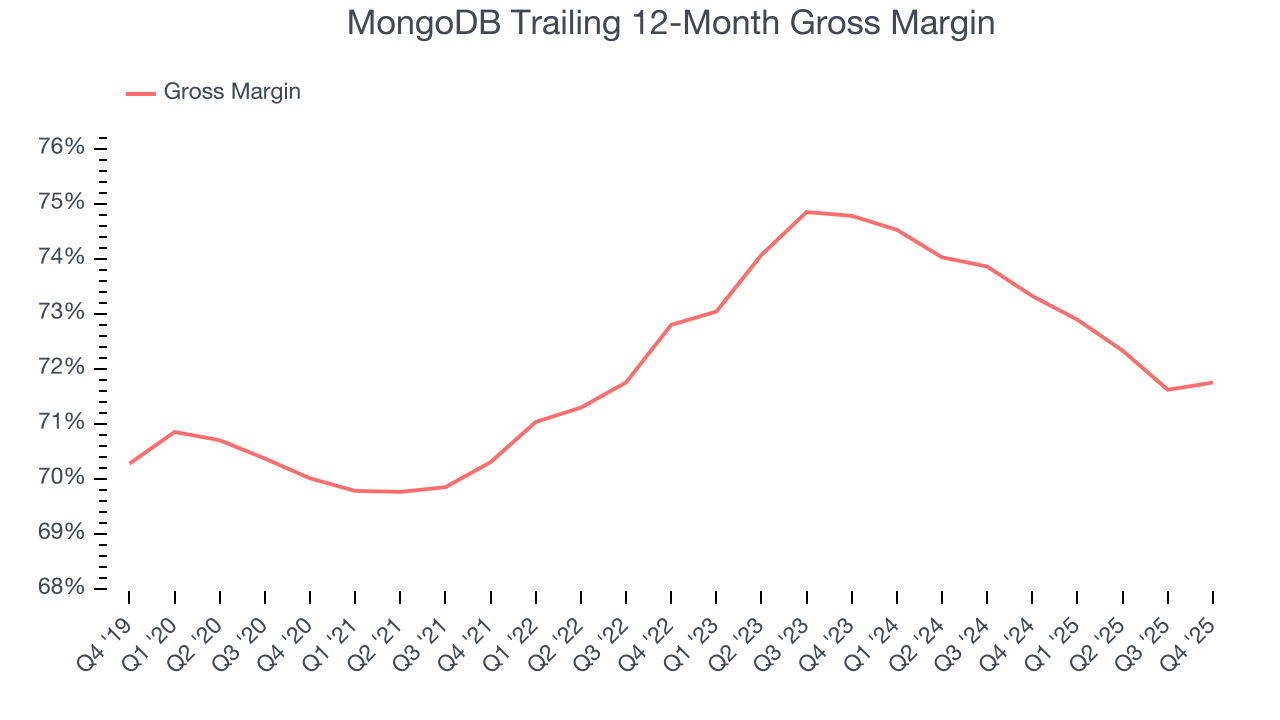

9. Gross Margin & Pricing Power

For software companies like MongoDB, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

MongoDB’s gross margin is slightly below the average software company, giving it less room than its competitors to invest in areas such as product and sales. As you can see below, it averaged a 71.7% gross margin over the last year. Said differently, MongoDB had to pay a chunky $28.25 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. MongoDB has seen gross margins decline by 3 percentage points over the last 2 year, which is among the worst in the software space.

MongoDB produced a 73% gross profit margin in Q4, in line with the same quarter last year. Zooming out, MongoDB’s full-year margin has been trending down over the past 12 months, decreasing by 1.6 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs.

10. Operating Margin

Although MongoDB broke even this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 5.6% over the last year. Unprofitable, high-growth software companies require extra attention because they spend heaps of money to capture market share. This happened because the company spent loads of money to capture market share. As seen in its fast revenue growth, the aggressive strategy has paid off so far, and Wall Street’s estimates suggest the party will continue. We tend to agree and believe the business has a good chance of reaching profitability upon scale.

Over the last two years, MongoDB’s expanding sales gave it operating leverage as its margin rose by 5.2 percentage points. Still, it will take much more for the company to reach long-term profitability.

In Q4, MongoDB’s breakeven margin was 0%, up 3.4 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

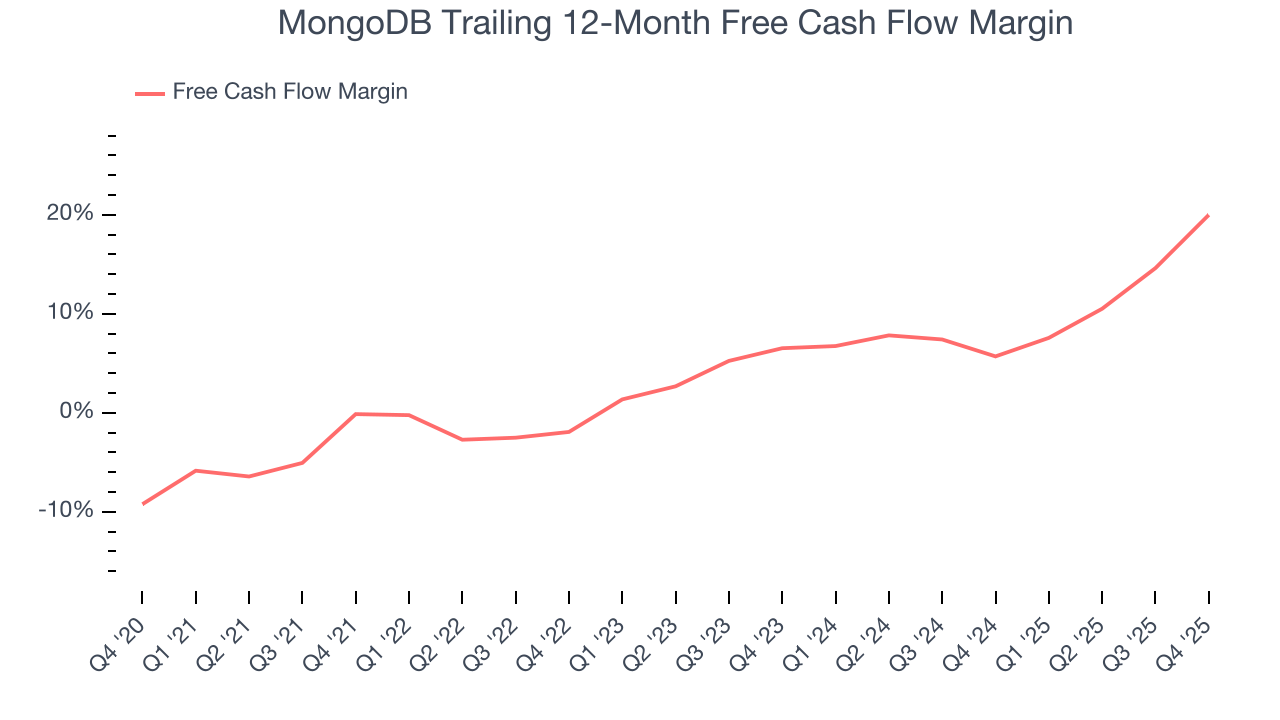

11. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

MongoDB has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 20% over the last year, better than the broader software sector. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

MongoDB’s free cash flow clocked in at $176.7 million in Q4, equivalent to a 25.4% margin. This result was good as its margin was 21.2 percentage points higher than in the same quarter last year. Its cash profitability was also above its one-year level, and we hope the company can build on this trend.

Over the next year, analysts predict MongoDB’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 20% for the last 12 months will decrease to 15%.

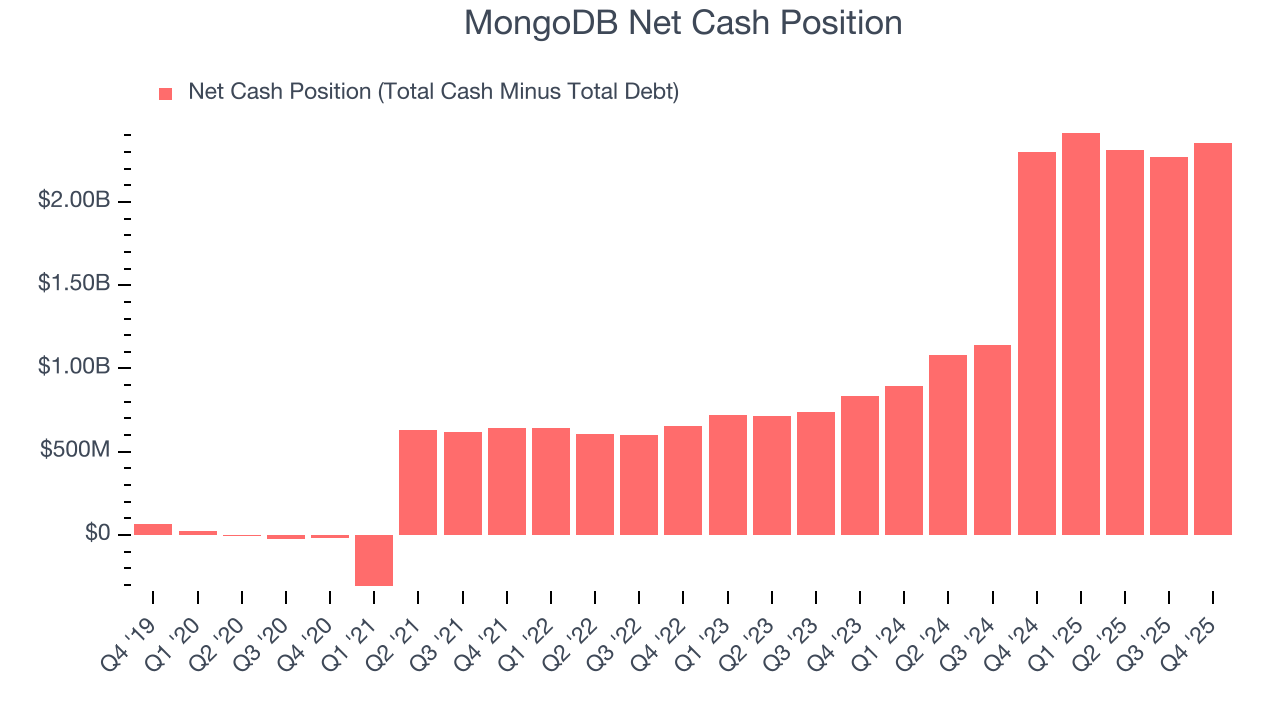

12. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

MongoDB is a well-capitalized company with $2.39 billion of cash and $32.86 million of debt on its balance sheet. This $2.35 billion net cash position is 11.8% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from MongoDB’s Q4 Results

We were impressed by how significantly MongoDB blew past analysts’ billings expectations this quarter. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The market seemed to be hoping for more, and the stock traded down 23.5% to $250.73 immediately following the results.

14. Is Now The Time To Buy MongoDB?

Updated: March 14, 2026 at 10:02 PM EDT

Before deciding whether to buy MongoDB or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

There are definitely a lot of things to like about MongoDB. To kick things off, its revenue growth was impressive over the last five years. And while its expanding operating margin shows it’s becoming more efficient at building and selling its software, its surging ARR shows its fundamentals and revenue predictability are improving. On top of that, its strong free cash flow generation gives it reinvestment options.

MongoDB’s price-to-sales ratio based on the next 12 months is 7.3x. When scanning the software space, MongoDB trades at a fair valuation. For those confident in the business and its management team, this is a good time to invest.

Wall Street analysts have a consensus one-year price target of $356.41 on the company (compared to the current share price of $259.55), implying they see 37.3% upside in buying MongoDB in the short term.