Arcos Dorados (ARCO)

Arcos Dorados catches our eye. Its demand is skyrocketing, as seen by its rapid growth in same-store sales and number of restaurants.― StockStory Analyst Team

1. News

2. Summary

Why Arcos Dorados Is Interesting

Translating to “Golden Arches” in Spanish, Arcos Dorados (NYSE:ARCO) is the master franchisee of the McDonald's brand in Latin America and the Caribbean, responsible for its operations and growth in over 20 countries.

- Same-store sales growth over the past two years shows it’s successfully drawing diners into its restaurants

- Same-store sales provide a solid foundation for the steady expansion of its restaurants

- A downside is its gross margin of 12.7% reflects the bad unit economics inherent in most restaurant businesses

Arcos Dorados’s quality is inadequate. You should search for better opportunities.

Why There Are Better Opportunities Than Arcos Dorados

At $8.80 per share, Arcos Dorados trades at 13.4x forward P/E. Arcos Dorados’s multiple may seem like a great deal among restaurant peers, but we think there are valid reasons why it’s this cheap.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Arcos Dorados (ARCO) Research Report: Q4 CY2025 Update

Fast-food chain Arcos Dorados (NYSE:ARCO) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 10.7% year on year to $1.27 billion. Its GAAP profit of $0.12 per share was 40.5% below analysts’ consensus estimates.

Arcos Dorados (ARCO) Q4 CY2025 Highlights:

- Revenue: $1.27 billion vs analyst estimates of $1.27 billion (10.7% year-on-year growth, in line)

- EPS (GAAP): $0.12 vs analyst expectations of $0.20 (40.5% miss)

- Adjusted EBITDA: $172.7 million vs analyst estimates of $143.9 million (13.6% margin, 20% beat)

- Operating Margin: 1.1%, down from 9% in the same quarter last year

- Locations: 2,520 at quarter end, up from 2,428 in the same quarter last year

- Same-Store Sales rose 16% year on year (14.3% in the same quarter last year)

- Market Capitalization: $1.62 billion

Company Overview

Translating to “Golden Arches” in Spanish, Arcos Dorados (NYSE:ARCO) is the master franchisee of the McDonald's brand in Latin America and the Caribbean, responsible for its operations and growth in over 20 countries.

McDonald’s is one of the world’s preeminent fast-food chains and its rapid growth has caught the attention of consumers worldwide.

One such person captivated by McDonald’s was Woods Staton, who joined the company in the 1980s and worked his way up to President of its South Latin America division.

In 2007, Staton saw an opportunity to take on an even larger role in the McDonald’s story. The company decided to sell its operations in Latin America because of the volatile economic environment, and Staton (along with other McDonald’s executives) acquired the stranded assets. Thus, Arcos Dorados was born.

As its largest franchisee, Arcos Dorados controls north of 2,300 McDonald’s restaurants and has access to its extensive knowledge and systems. Furthermore, it has more autonomy than typical franchisees as it has the exclusive right to own, operate, and grant franchises in its territories.

Since its establishment, Arcos Dorados has successfully expanded the McDonald's brand across the region, leveraging its deep understanding of local markets, cultures, and tastes. Its McDonald’s restaurants share many similarities to those in the U.S. aside from a few menu differences, such as the Cheddar McMelt in Brazil.

4. Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Fast-food competitors operating in Latin America include Burger King (owned by Restaurant Brands International, NYSE:QSR), Domino’s (NYSE:DPZ), and KFC and Pizza Hut (owned by Yum! Brands, NYSE:YUM).

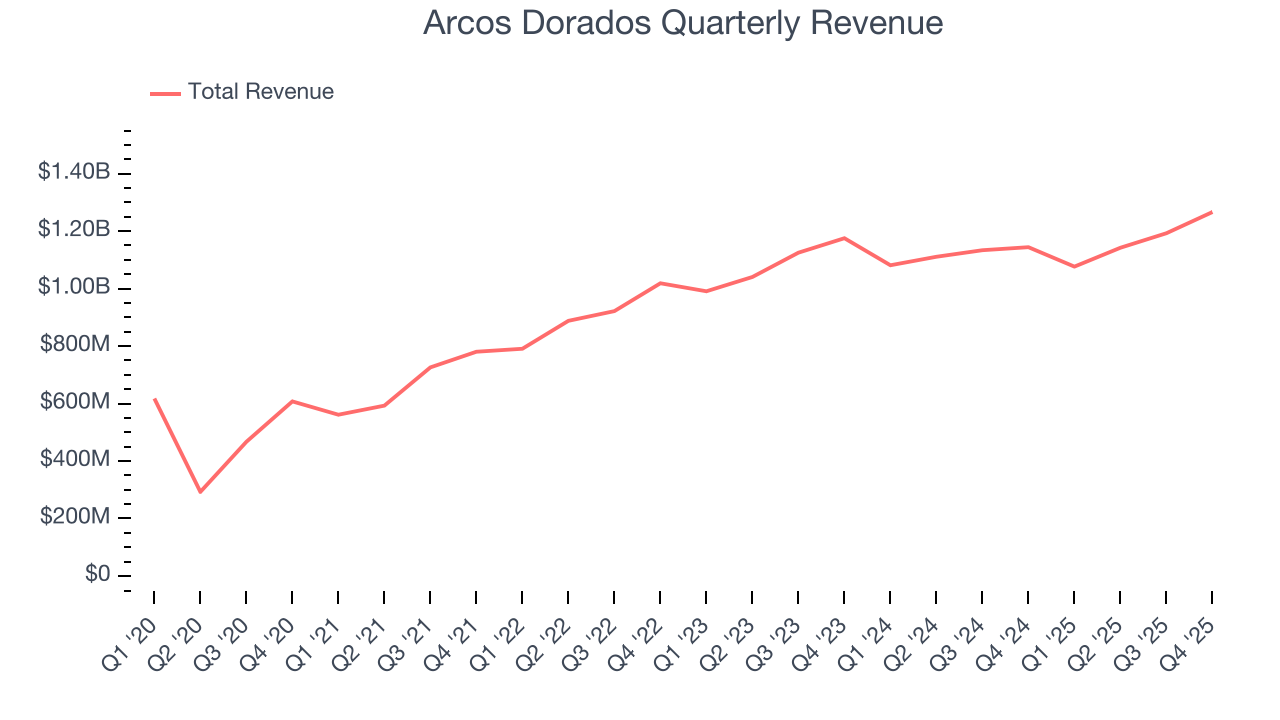

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $4.68 billion in revenue over the past 12 months, Arcos Dorados is one of the larger restaurant chains in the industry and benefits from a well-known brand that influences consumer purchasing decisions.

As you can see below, Arcos Dorados’s sales grew at a decent 7.9% compounded annual growth rate over the last six years as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, Arcos Dorados’s year-on-year revenue growth was 10.7%, and its $1.27 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 12% over the next 12 months, an acceleration versus the last six years. This projection is commendable and indicates its newer menu offerings will spur better top-line performance.

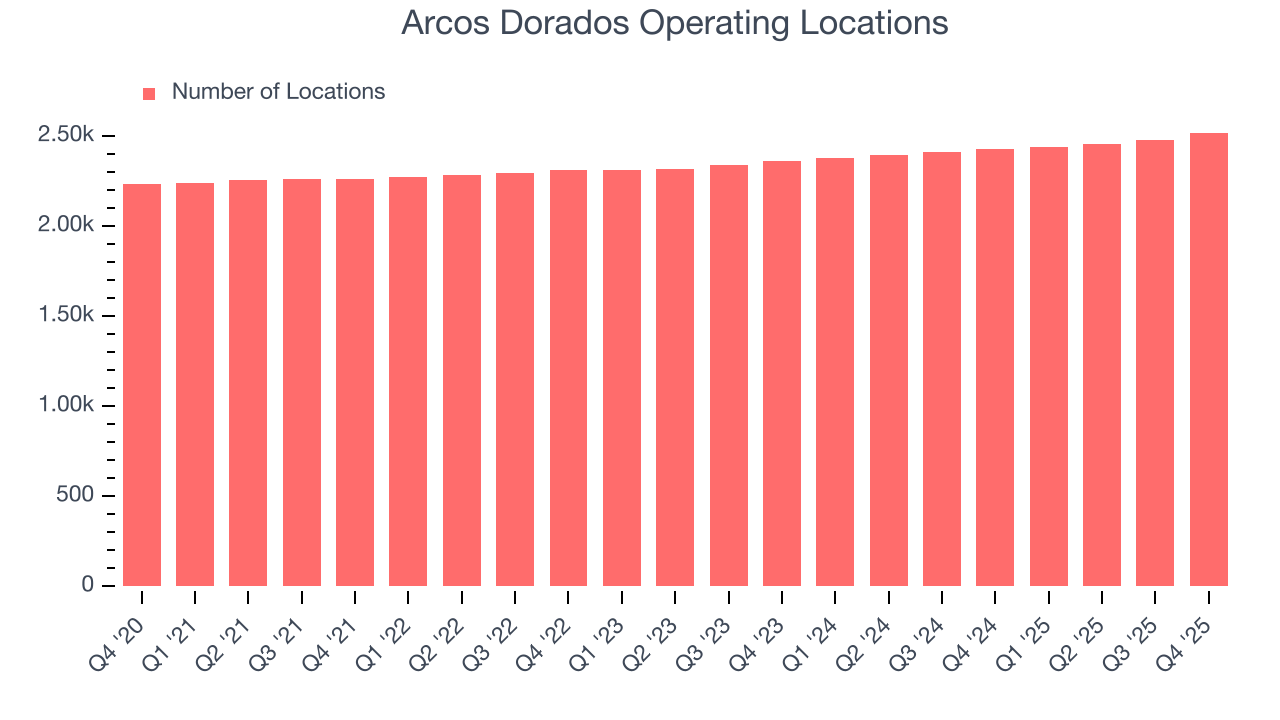

6. Restaurant Performance

Number of Restaurants

The number of dining locations a restaurant chain operates is a critical driver of how quickly company-level sales can grow.

Arcos Dorados sported 2,520 locations in the latest quarter. Over the last two years, it has opened new restaurants quickly, averaging 3% annual growth. This was faster than the broader restaurant sector.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

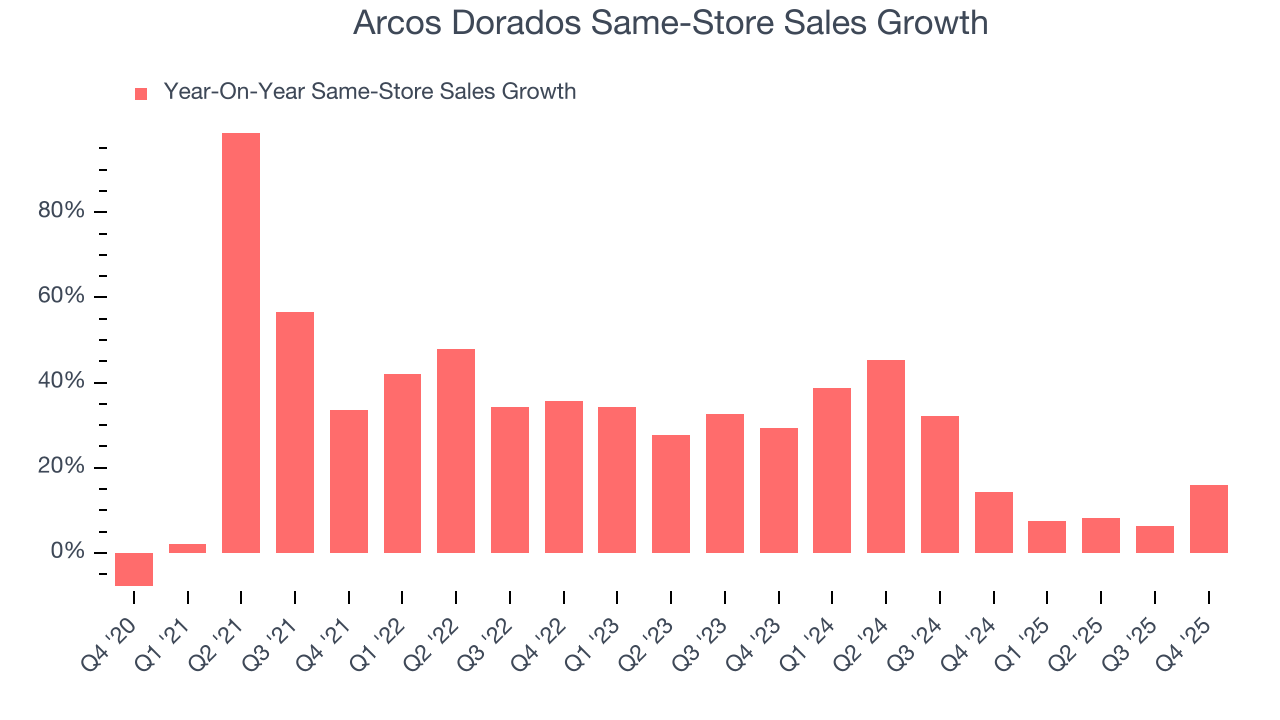

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

Arcos Dorados has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 21%. This performance suggests its rollout of new restaurants is beneficial for shareholders. We like this backdrop because it gives Arcos Dorados multiple ways to win: revenue growth can come from new restaurants or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, Arcos Dorados’s same-store sales rose 16% year on year. This growth was a deceleration from its historical levels, showing the business is still performing well but losing a bit of steam.

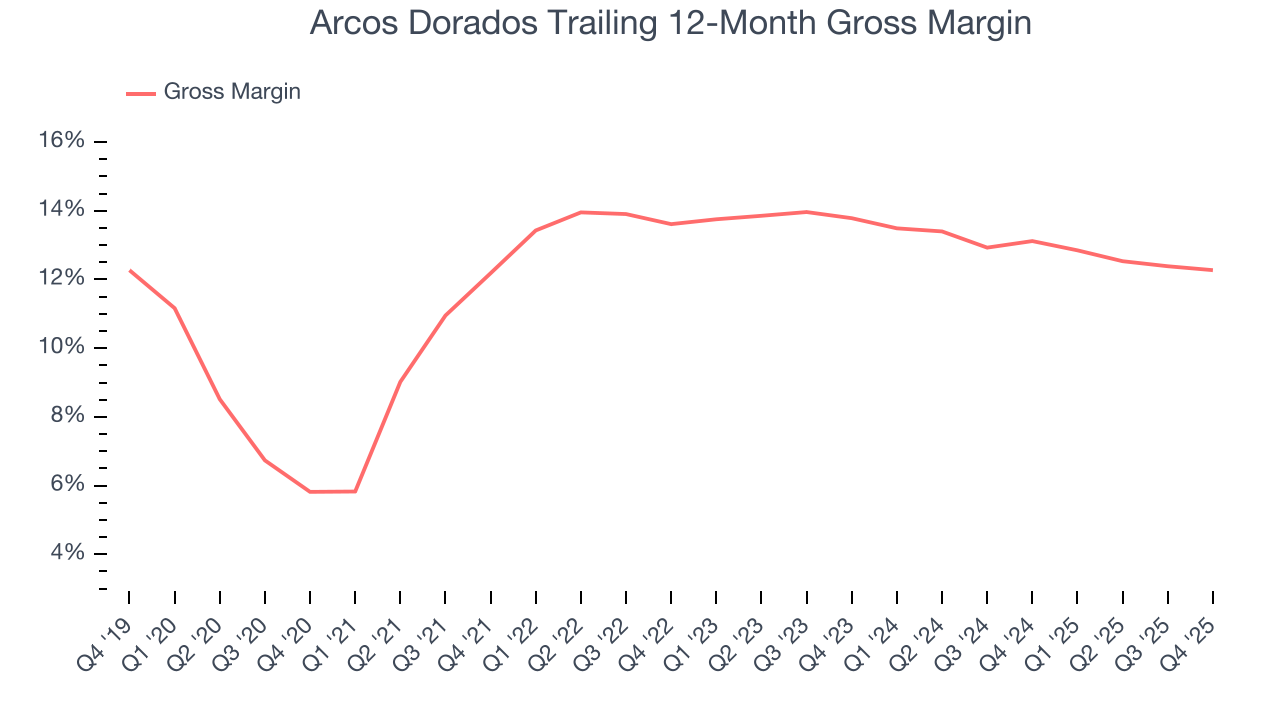

7. Gross Margin & Pricing Power

Gross profit margins tell us how much money a restaurant gets to keep after paying for the direct costs of the meals it sells, like ingredients, and indicate its level of pricing power.

Arcos Dorados has bad unit economics for a restaurant company, signaling it operates in a competitive market and has little room for error if demand unexpectedly falls. As you can see below, it averaged a 12.7% gross margin over the last two years. Said differently, Arcos Dorados had to pay a chunky $87.31 to its suppliers for every $100 in revenue.

In Q4, Arcos Dorados produced a 14.2% gross profit margin, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as ingredients and transportation expenses) have been stable and it isn’t under pressure to lower prices.

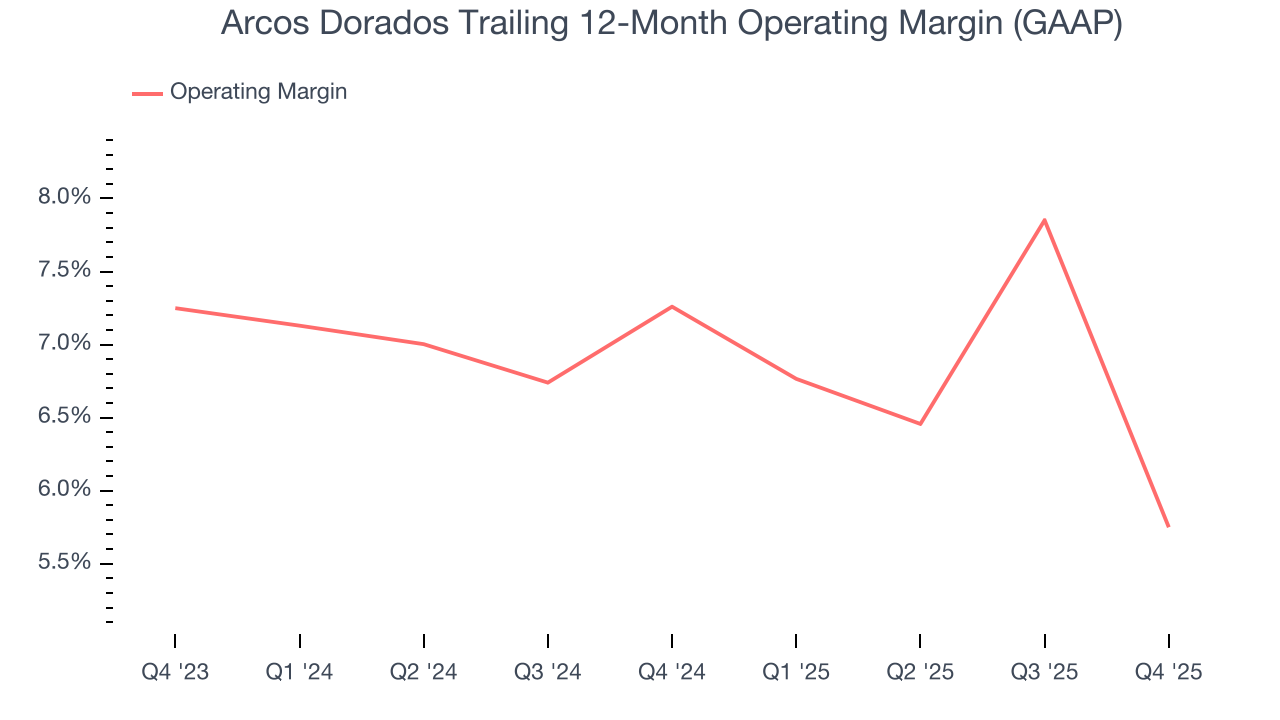

8. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Arcos Dorados was profitable over the last two years but held back by its large cost base. Its average operating margin of 6.5% was weak for a restaurant business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Arcos Dorados’s operating margin decreased by 1.5 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Arcos Dorados’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Arcos Dorados generated an operating margin profit margin of 1.1%, down 7.9 percentage points year on year. Since Arcos Dorados’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, and administrative overhead increased.

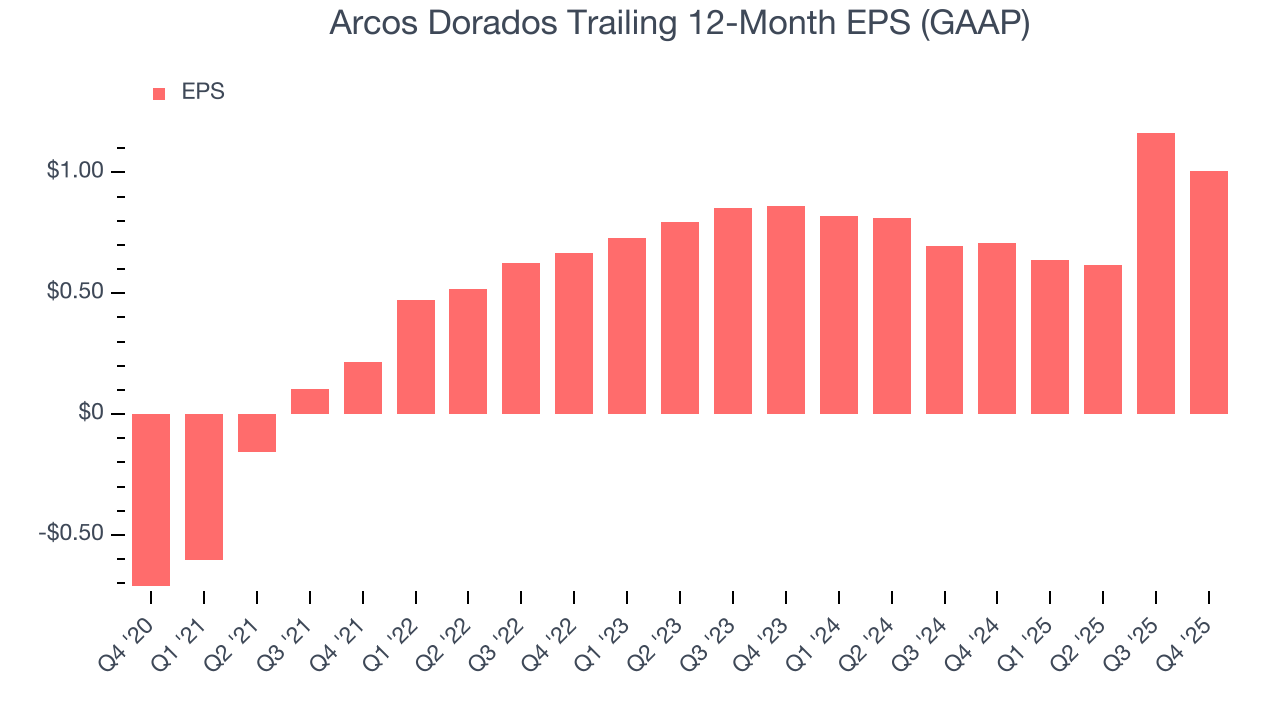

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Arcos Dorados’s EPS grew at 17% compounded annual growth rate over the last six years, higher than its 7.9% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

In Q4, Arcos Dorados reported EPS of $0.12, down from $0.28 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

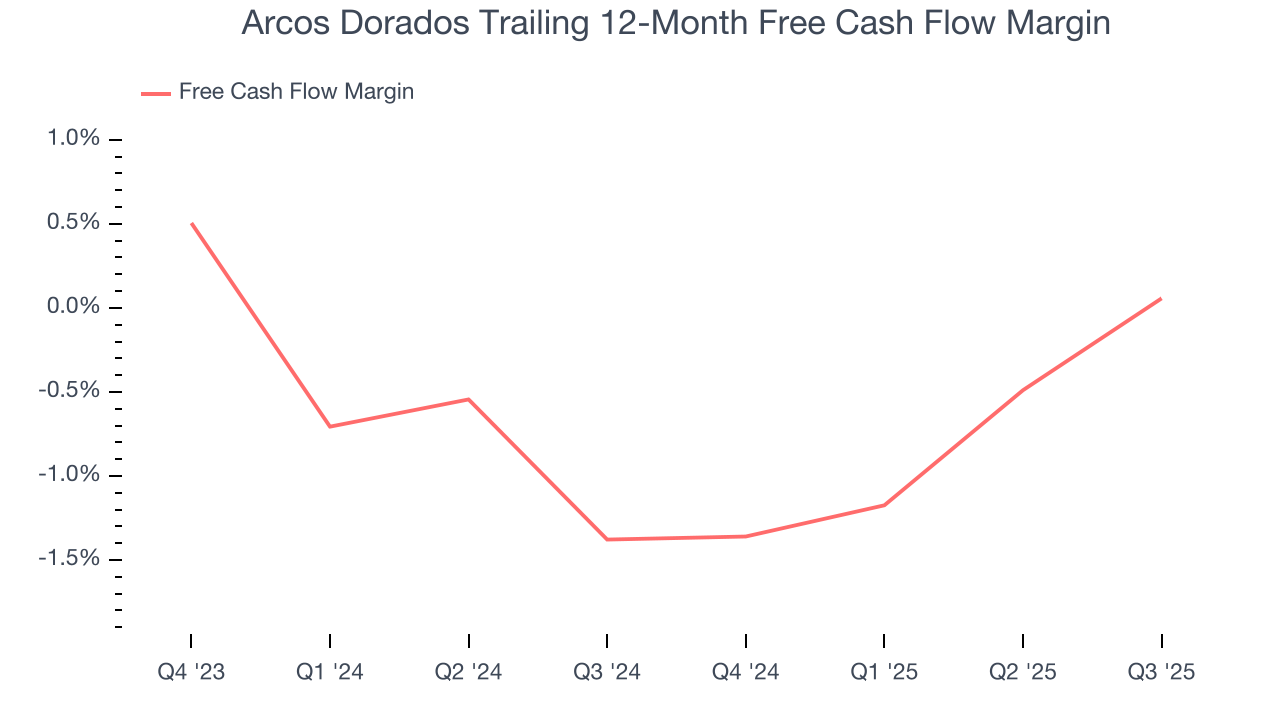

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Arcos Dorados broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Arcos Dorados’s five-year average ROIC was 10.9%, higher than most restaurant businesses. This illustrates its management team’s ability to invest in profitable growth opportunities and generate value for shareholders.

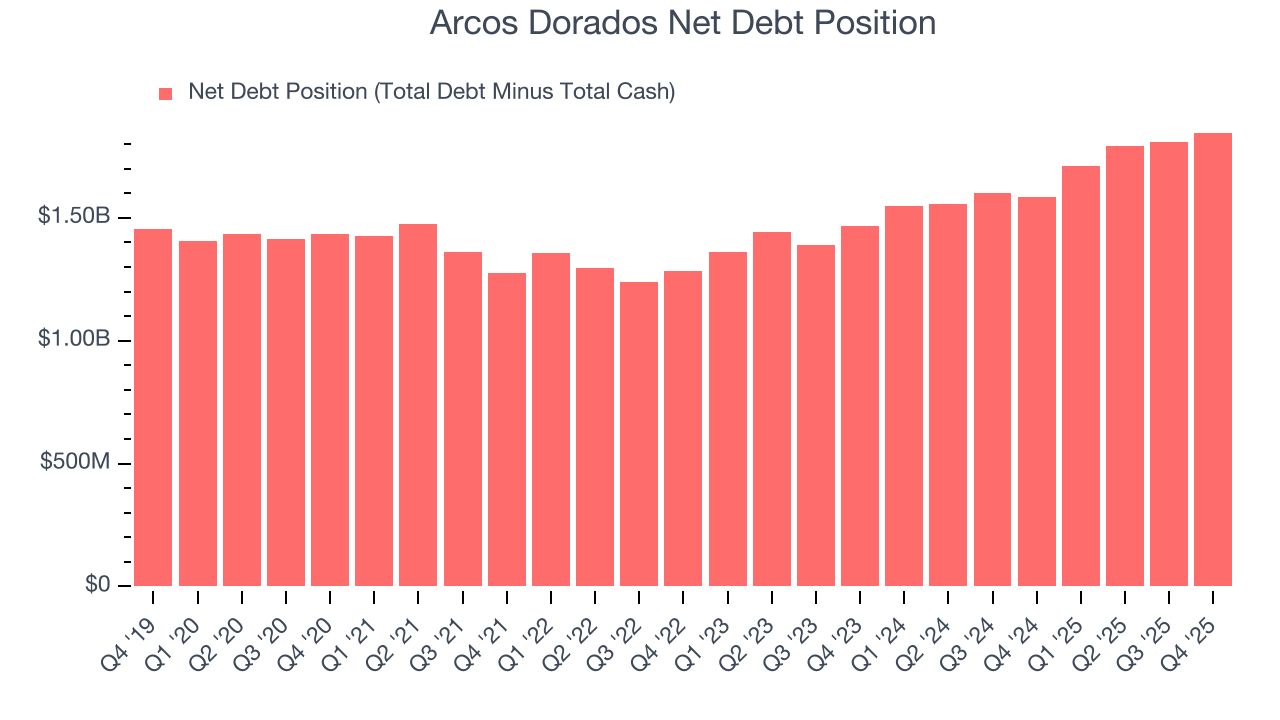

12. Balance Sheet Assessment

Arcos Dorados reported $422.3 million of cash and $2.27 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $575.2 million of EBITDA over the last 12 months, we view Arcos Dorados’s 3.2× net-debt-to-EBITDA ratio as safe. We also see its $2.35 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Arcos Dorados’s Q4 Results

We were impressed by how significantly Arcos Dorados blew past analysts’ EBITDA expectations this quarter. We were also excited its same-store sales outperformed Wall Street’s estimates by a wide margin. On the other hand, its EPS missed and its revenue was in line with Wall Street’s estimates. Overall, this print was mixed. The market seemed to be hoping for more, and the stock traded down 2.9% to $7.48 immediately following the results.

14. Is Now The Time To Buy Arcos Dorados?

Updated: March 19, 2026 at 10:55 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

There are a lot of things to like about Arcos Dorados. First off, its revenue growth was decent over the last six years and is expected to accelerate over the next 12 months. And while Arcos Dorados’s projected EPS for the next year is lacking, its marvelous same-store sales growth is on another level.

Arcos Dorados’s forward price-to-sales ratio is 0.3x. The market typically values companies like Arcos Dorados based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. There’s no rush to buy the stock - add this one to your watchlist and come back to it later.

Wall Street analysts have a consensus one-year price target of $9.91 on the company (compared to the current share price of $7.68).