Clorox (CLX)

We’re wary of Clorox. Its declining sales show demand has evaporated, a red flag for investors seeking high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why Clorox Is Not Exciting

Founded in 1913 with bleach as the sole product offering, Clorox (NYSE:CLX) today is a consumer products giant whose product portfolio spans everything from bleach to skincare to salad dressing to kitty litter.

- Annual sales declines of 1.3% for the past three years show its products struggled to connect with the market

- Forecasted revenue decline of 1.1% for the upcoming 12 months implies demand will fall even further

- On the bright side, its earnings growth was above the peer group average over the last three years as its EPS compounded at 20.6% annually

Clorox fails to meet our quality criteria. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than Clorox

At $113.95 per share, Clorox trades at 17.2x forward P/E. This valuation is fair for the quality you get, but we’re on the sidelines for now.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Clorox (CLX) Research Report: Q3 CY2025 Update

Consumer products giant Clorox (NYSE:CLX) reported Q3 CY2025 results exceeding the market’s revenue expectations, but sales fell by 18.9% year on year to $1.43 billion. Its non-GAAP profit of $0.85 per share was 9.2% above analysts’ consensus estimates.

Clorox (CLX) Q3 CY2025 Highlights:

- Revenue: $1.43 billion vs analyst estimates of $1.40 billion (18.9% year-on-year decline, 2% beat)

- Adjusted EPS: $0.85 vs analyst estimates of $0.78 (9.2% beat)

- Management reiterated its full-year Adjusted EPS guidance of $6.13 at the midpoint

- Operating Margin: 7.5%, down from 17.4% in the same quarter last year

- Organic Revenue fell 17% year on year vs analyst estimates of 18.2% declines (116.4 basis point beat)

- Market Capitalization: $13.75 billion

Company Overview

Founded in 1913 with bleach as the sole product offering, Clorox (NYSE:CLX) today is a consumer products giant whose product portfolio spans everything from bleach to skincare to salad dressing to kitty litter.

Clorox bleach is still a powerhouse home care brand used to clean, disinfect, and whiten. However, the company now also boasts Glad garbage bags, Burt’s Bees skincare products, Kingsford charcoal for grilling, and Fresh Step kitty litter to name a few. These brands are both household mainstays as well as innovators that help steer the direction of these categories. For example, Glad was one of the first garbage bags to feature drawstrings, making the bags easier to tie, lift, and carry.

Clorox’s core customer is typically someone who makes purchases for the household. These consumers seek trusted brands that are convenient to find and get the job done. While price matters, Clorox usually doesn’t have to be the cheapest option, as many are willing to pay a reasonable premium to buy established brands rather than lesser-known or private-label brands.

As a consumer goods giant, Clorox products can be found in many retail stores. Grocery stores, mass merchandisers like Walmart (NYSE:WMT), warehouse clubs like Costco (NASDAQ:COST), dollar stores like Dollar General (NYSE:DG), and drug stores like CVS (NYSE:CVS) all carry the company’s offerings.

4. Household Products

Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options. These trends can be double-edged swords that benefit companies who innovate quickly to take advantage of them and hurt companies that don't invest enough to meet consumers where they want to be with regards to trends.

Competitors that offer a wide range of household and personal care products include Proctor & Gamble (NYSE:PG), Unilever (LSE:ULVR), Reckitt Benckiser (LSE:RKT), and Colgate-Palmolive (NYSE:CL).

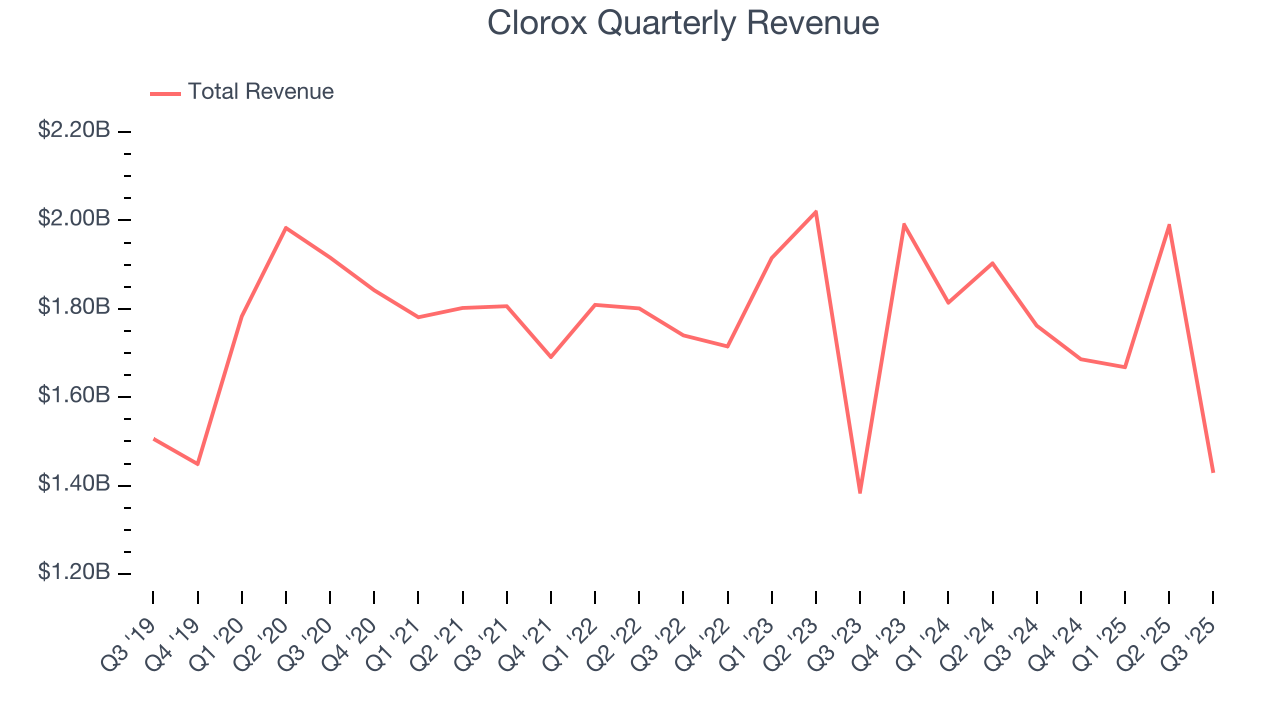

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $6.77 billion in revenue over the past 12 months, Clorox is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. To accelerate sales, Clorox likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Clorox’s revenue declined by 1.3% per year over the last three years, a tough starting point for our analysis.

This quarter, Clorox’s revenue fell by 18.9% year on year to $1.43 billion but beat Wall Street’s estimates by 2%.

Looking ahead, sell-side analysts expect revenue to decline by 1.6% over the next 12 months, similar to its three-year rate. This projection is underwhelming and implies its newer products will not catalyze better top-line performance yet.

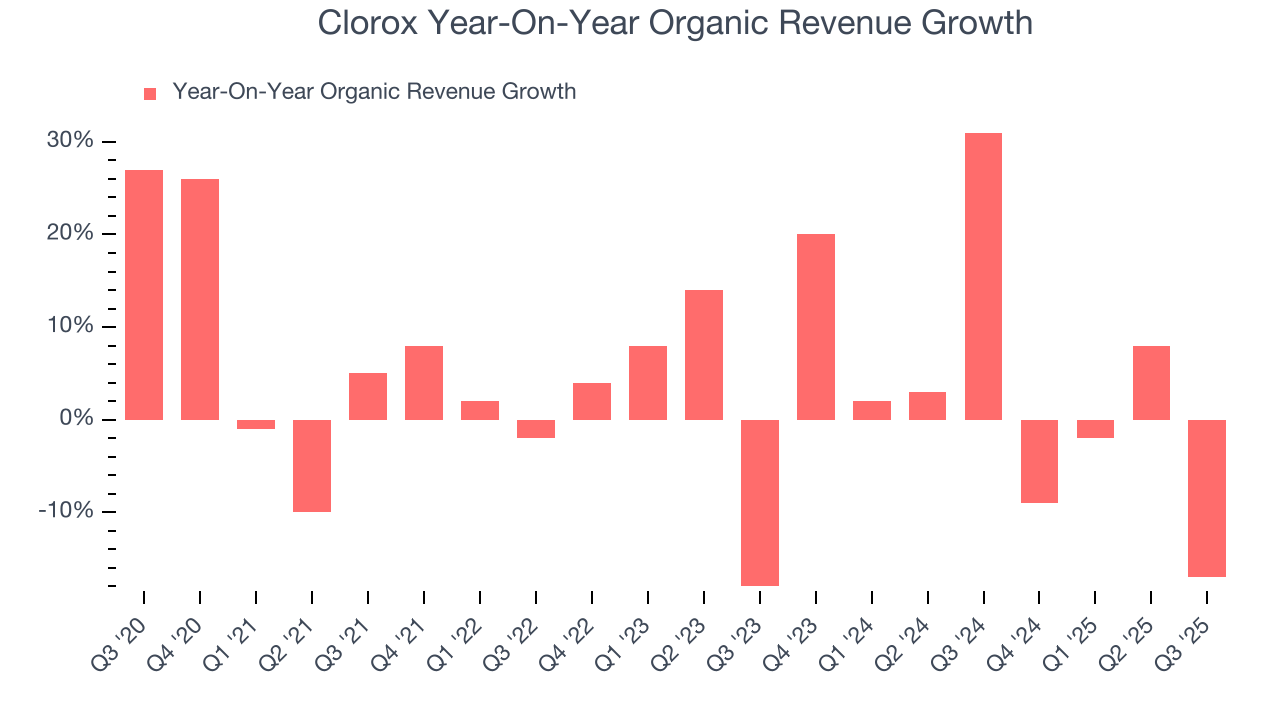

6. Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Clorox’s products has generally risen over the last two years but lagged behind the broader sector. On average, the company’s organic sales have grown by 4.5% year on year.

In the latest quarter, Clorox’s organic sales fell by 17% year on year. This decline was a reversal from its historical levels. We’ll keep a close eye on the company to see if this turns into a longer-term trend.

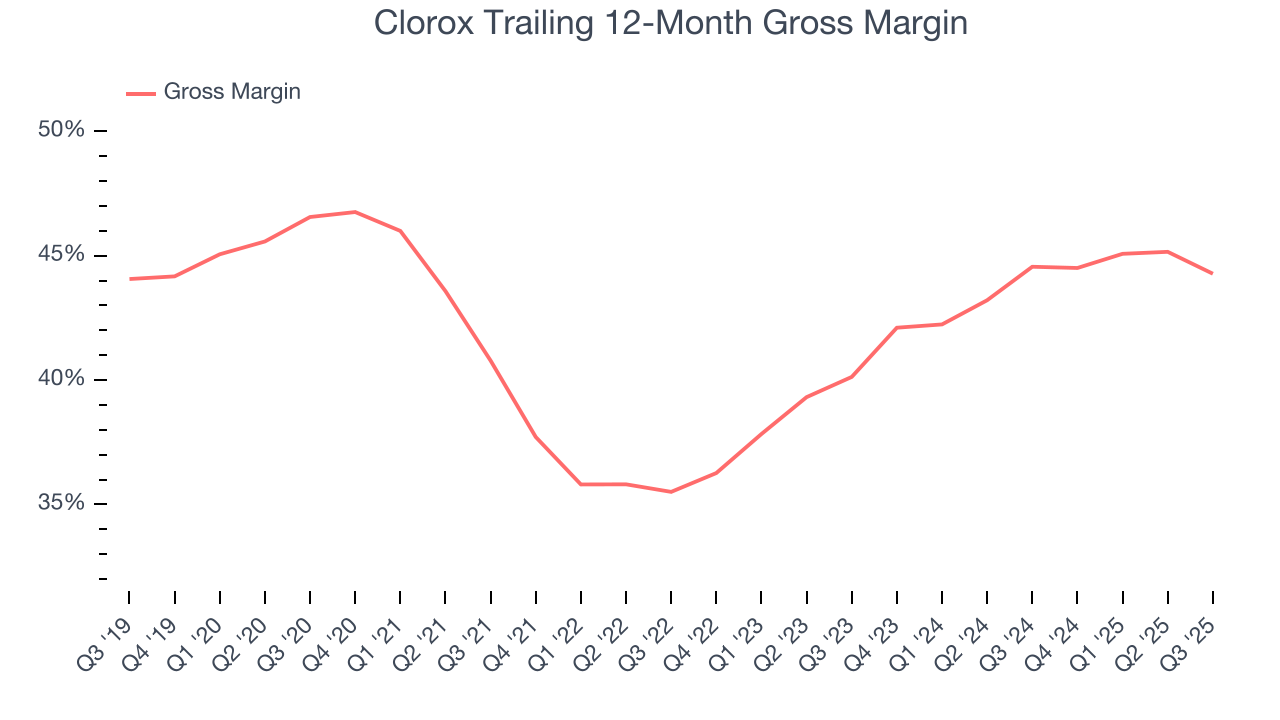

7. Gross Margin & Pricing Power

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products, has a stronger brand, and commands pricing power.

Clorox has great unit economics for a consumer staples company, giving it ample room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an excellent 44.4% gross margin over the last two years. That means Clorox only paid its suppliers $55.58 for every $100 in revenue.

This quarter, Clorox’s gross profit margin was 41.7%, marking a 4 percentage point decrease from 45.7% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

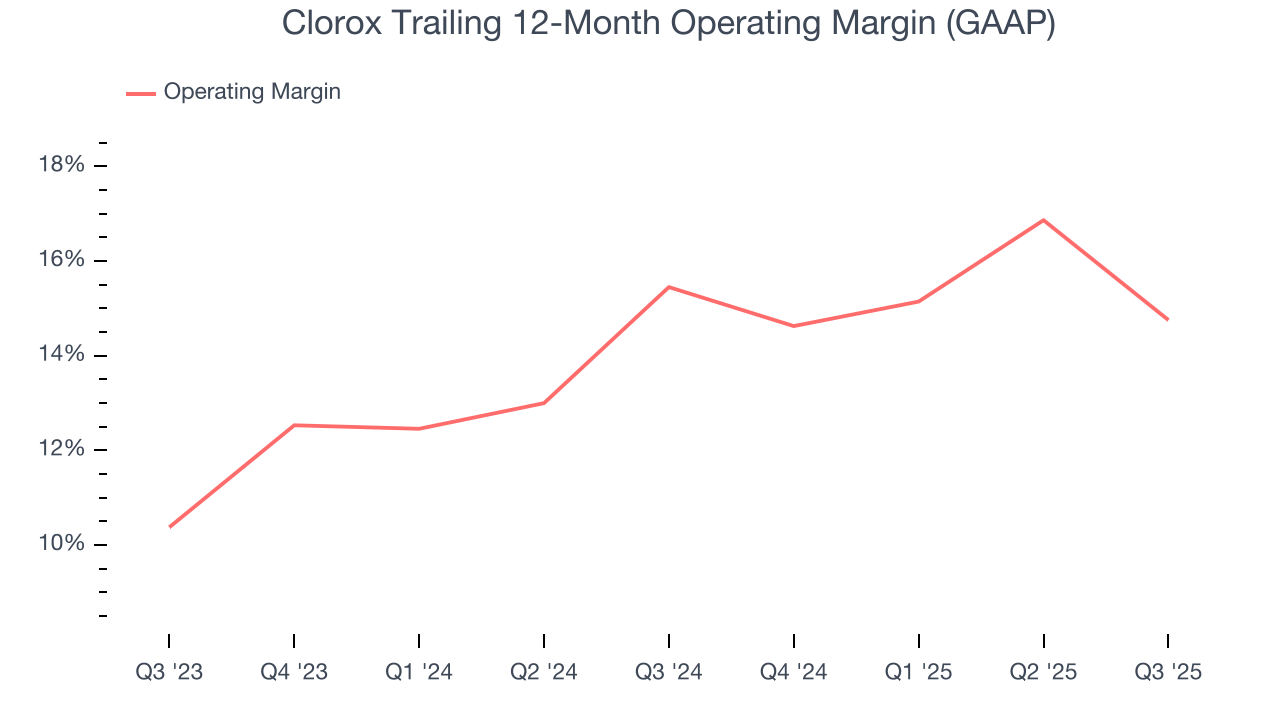

8. Operating Margin

Clorox’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 15.1% over the last two years. This profitability was top-notch for a consumer staples business, showing it’s an well-run company with an efficient cost structure. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Clorox’s operating margin might fluctuated slightly but has generally stayed the same over the last year, highlighting the consistency of its expense base.

This quarter, Clorox generated an operating margin profit margin of 7.5%, down 9.9 percentage points year on year. Since Clorox’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, and administrative overhead increased.

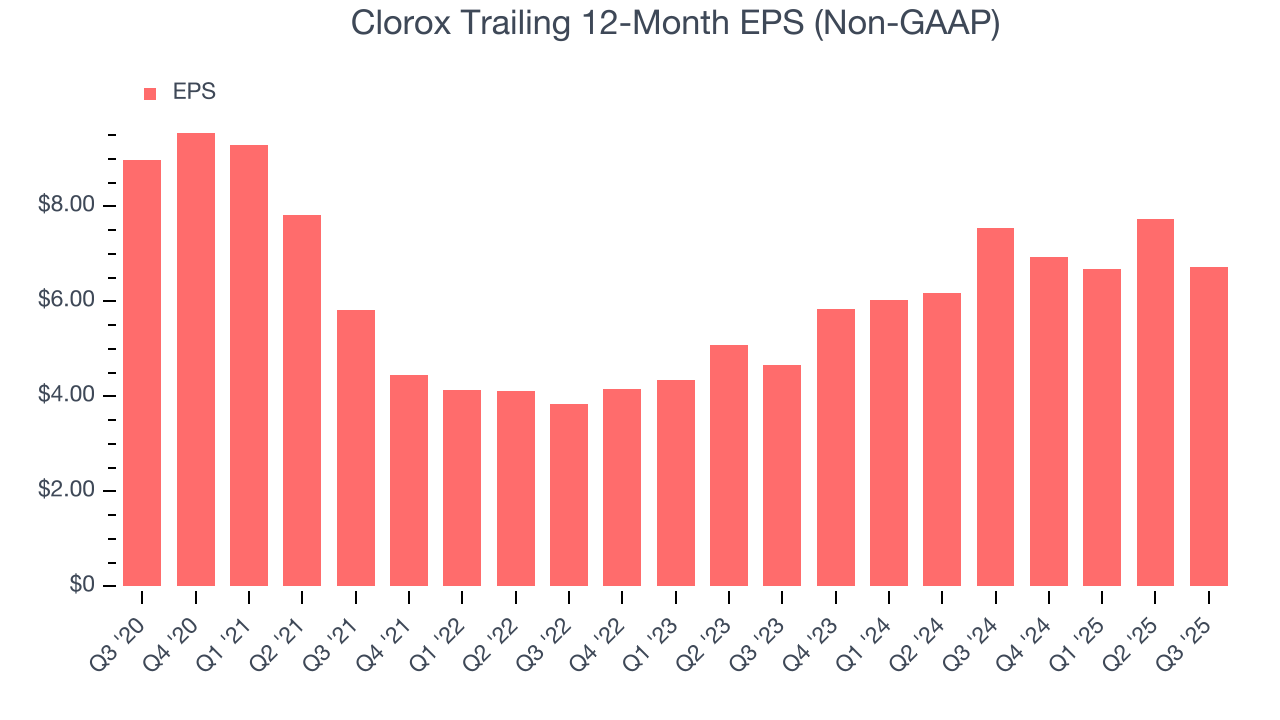

9. Earnings Per Share

We track the change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

In Q3, Clorox reported adjusted EPS of $0.85, down from $1.86 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 9.2%. Over the next 12 months, Wall Street expects Clorox’s full-year EPS of $6.72 to shrink by 3.1%.

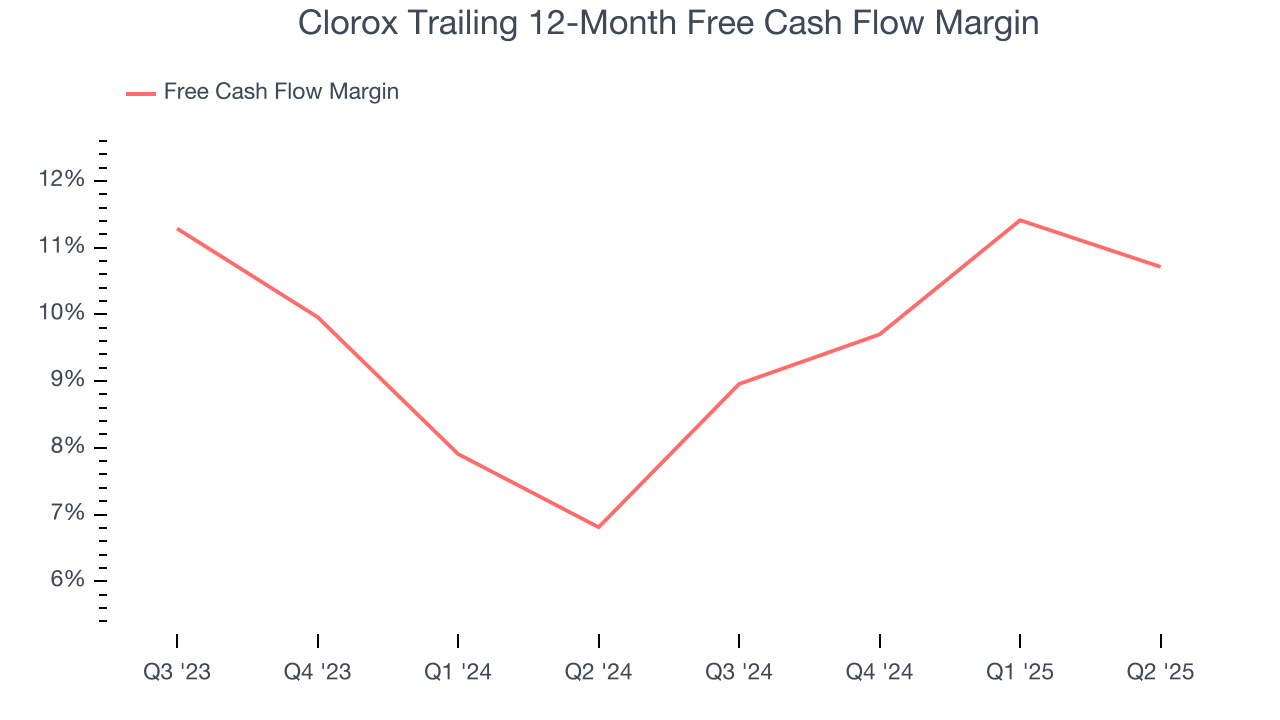

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Clorox has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors. The company’s free cash flow margin averaged 9.7% over the last two years, quite impressive for a consumer staples business.

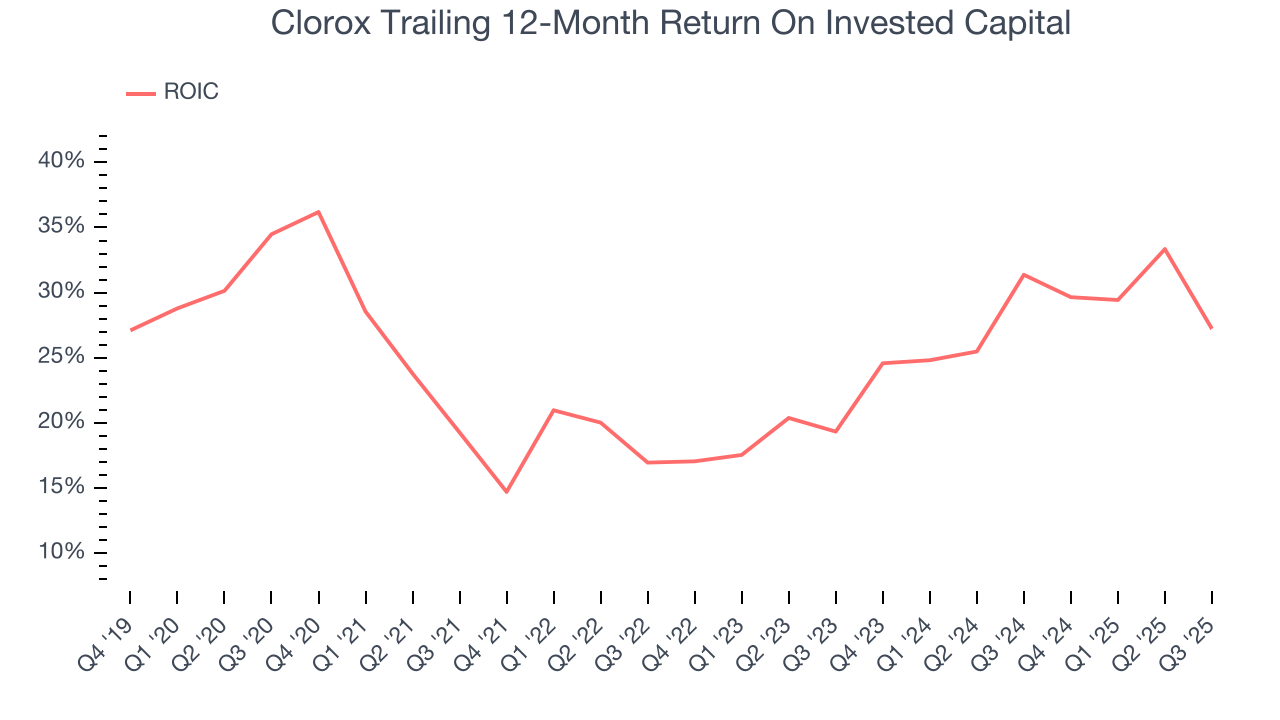

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Clorox hasn’t been the highest-quality company lately because of its poor top-line performance, it historically found a few growth initiatives that worked out well. Its five-year average ROIC was 22.8%, impressive for a consumer staples business.

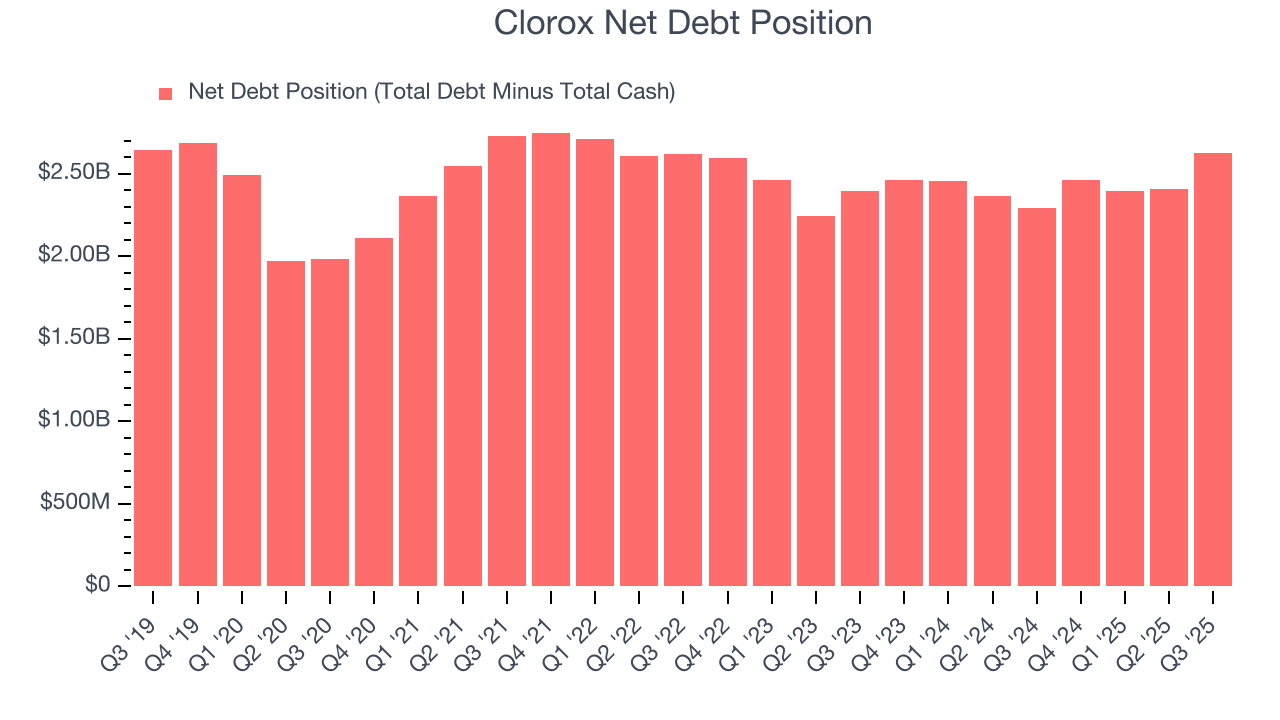

12. Balance Sheet Assessment

Clorox reported $166 million of cash and $2.79 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.36 billion of EBITDA over the last 12 months, we view Clorox’s 1.9× net-debt-to-EBITDA ratio as safe. We also see its $82 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Clorox’s Q3 Results

It was encouraging to see Clorox beat analysts’ revenue expectations this quarter on slightly higher-than-expected organic revenue growth. Moving down the income statement, EPS beat by a pretty convincing amount. Overall, this print had some key positives. The stock traded up 3.2% to $112.51 immediately after reporting.

14. Is Now The Time To Buy Clorox?

Updated: January 24, 2026 at 9:55 PM EST

Before investing in or passing on Clorox, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Clorox isn’t a terrible business, but it doesn’t pass our quality test. First off, its revenue has declined over the last three years, and analysts don’t see anything changing over the next 12 months. And while Clorox’s EPS growth over the last three years has been fantastic, its projected EPS for the next year is lacking.

Clorox’s P/E ratio based on the next 12 months is 17.2x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $120.41 on the company (compared to the current share price of $113.95).