Figs (FIGS)

Figs is up against the odds. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Figs Will Underperform

Rising to fame via TikTok and founded in 2013 by Heather Hasson and Trina Spear, Figs (NYSE:FIGS) is a healthcare apparel company known for its stylish approach to medical attire and uniforms.

- Muted 19.1% annual revenue growth over the last five years shows its demand lagged behind its consumer discretionary peers

- Falling earnings per share over the last four years has some investors worried as stock prices ultimately follow EPS over the long term

- Operating margin falls short of the industry average, and the smaller profit dollars make it harder to react to unexpected market developments

Figs is in the doghouse. There are better opportunities in the market.

Why There Are Better Opportunities Than Figs

Figs’s stock price of $14.22 implies a valuation ratio of 56.5x forward P/E. We consider this valuation aggressive considering the weaker revenue growth profile.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Figs (FIGS) Research Report: Q4 CY2025 Update

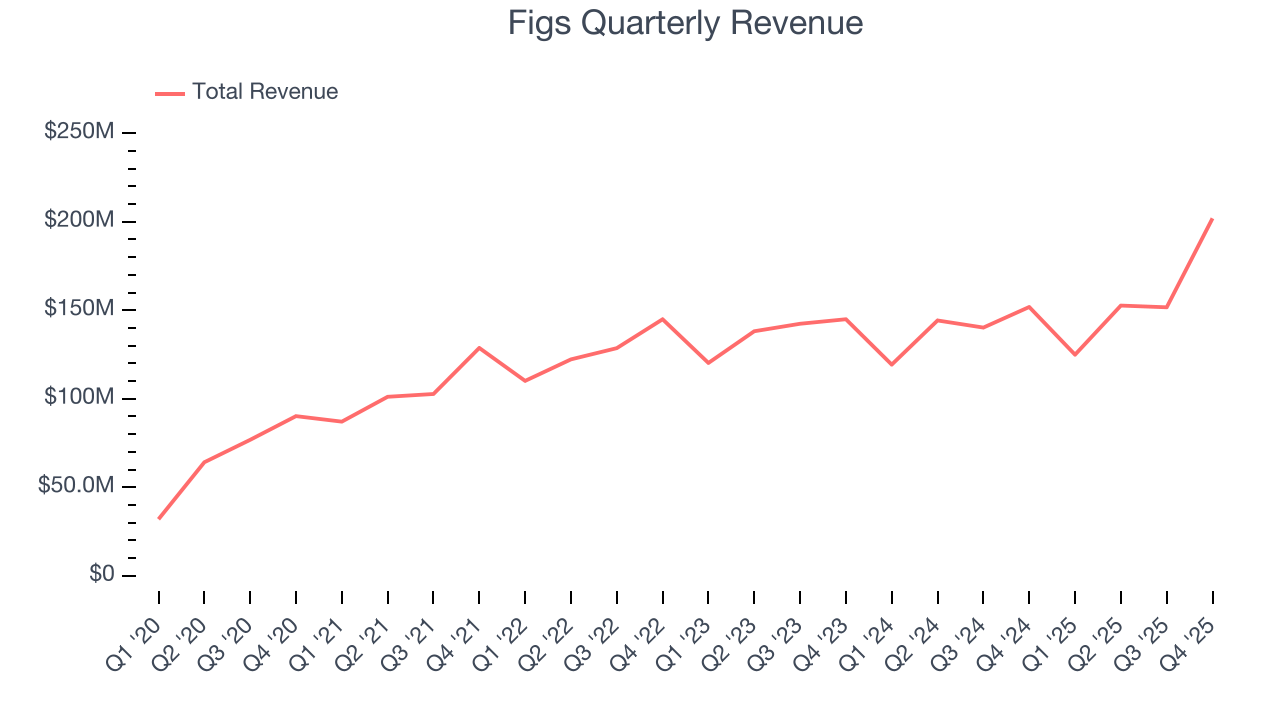

Healthcare apparel company Figs (NYSE:FIGS) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 33% year on year to $201.9 million. Its GAAP profit of $0.10 per share was significantly above analysts’ consensus estimates.

Figs (FIGS) Q4 CY2025 Highlights:

- Revenue: $201.9 million vs analyst estimates of $165.8 million (33% year-on-year growth, 21.8% beat)

- EPS (GAAP): $0.10 vs analyst estimates of $0.02 (significant beat)

- Adjusted EBITDA: $26.73 million vs analyst estimates of $13.65 million (13.2% margin, 95.8% beat)

- Operating Margin: 9.3%, up from 5.9% in the same quarter last year

- Free Cash Flow Margin: 28.8%, up from 17.8% in the same quarter last year

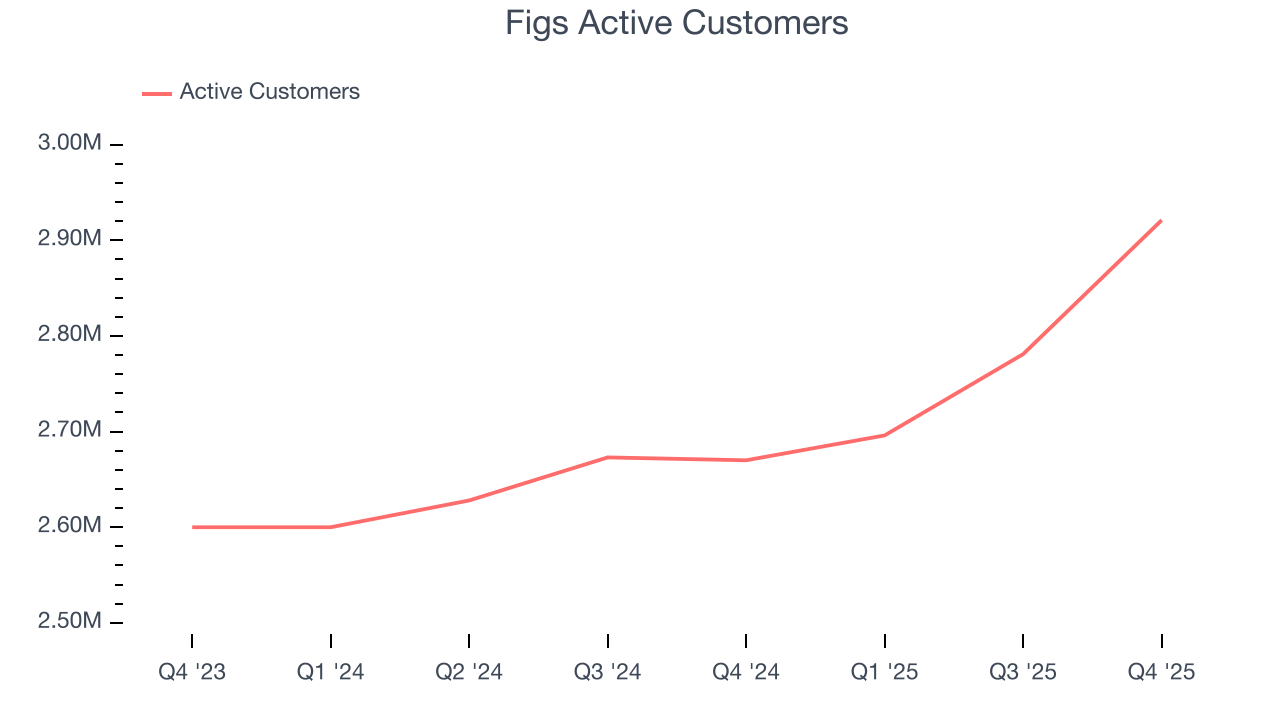

- Active Customers: 2.92 million, up 251,000 year on year

- Market Capitalization: $1.80 billion

Company Overview

Rising to fame via TikTok and founded in 2013 by Heather Hasson and Trina Spear, Figs (NYSE:FIGS) is a healthcare apparel company known for its stylish approach to medical attire and uniforms.

Before Figs, most medical scrubs were unisex, uncomfortable, and lacked style. Figs changed this by introducing scrubs that not only met the practical demands of healthcare professionals but also provided a modern, tailored fit and aesthetic appeal. This focus on design, comfort, and functionality quickly resonated with medical professionals.

The company's product line includes scrubs, lab coats, and other medical apparel accessories designed for men and women, and could expand its offerings into adjacent areas over time. Figs’s products stand out due to their proprietary fabric technology, which is antimicrobial, wrinkle-resistant, moisture-wicking, and highly durable.

Figs operates on a direct-to-consumer model, primarily selling its products online, allowing the company to maintain control over its brand experience, customer service, and pricing strategy. The direct-to-consumer model also enables Figs to build a community with its customer base bolstered by engagement through social media and other digital platforms.

4. Consumer Discretionary - Apparel and Accessories

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Apparel and accessories companies design, brand, and distribute clothing, handbags, jewelry, and related lifestyle products, often spanning multiple price tiers. Tailwinds include premiumization trends (consumers trading up for perceived quality), international expansion into emerging markets, and growing digital commerce penetration. However, these businesses face headwinds from highly cyclical demand, intense promotional environments, and counterfeit competition undermining brand equity. Tariff volatility and sourcing concentration in a handful of countries add risk. Additionally, rapidly changing fashion cycles and the rise of ultra-fast-fashion digital competitors compress product life cycles and make demand forecasting exceptionally difficult.

Figs's primary competitors include Dickies Medical (owned by VF Corp NYSE:VFC) and private companies Cherokee Uniforms, Barco Uniforms, Scrubs & Beyond, and Medline Industries.

5. Revenue Growth

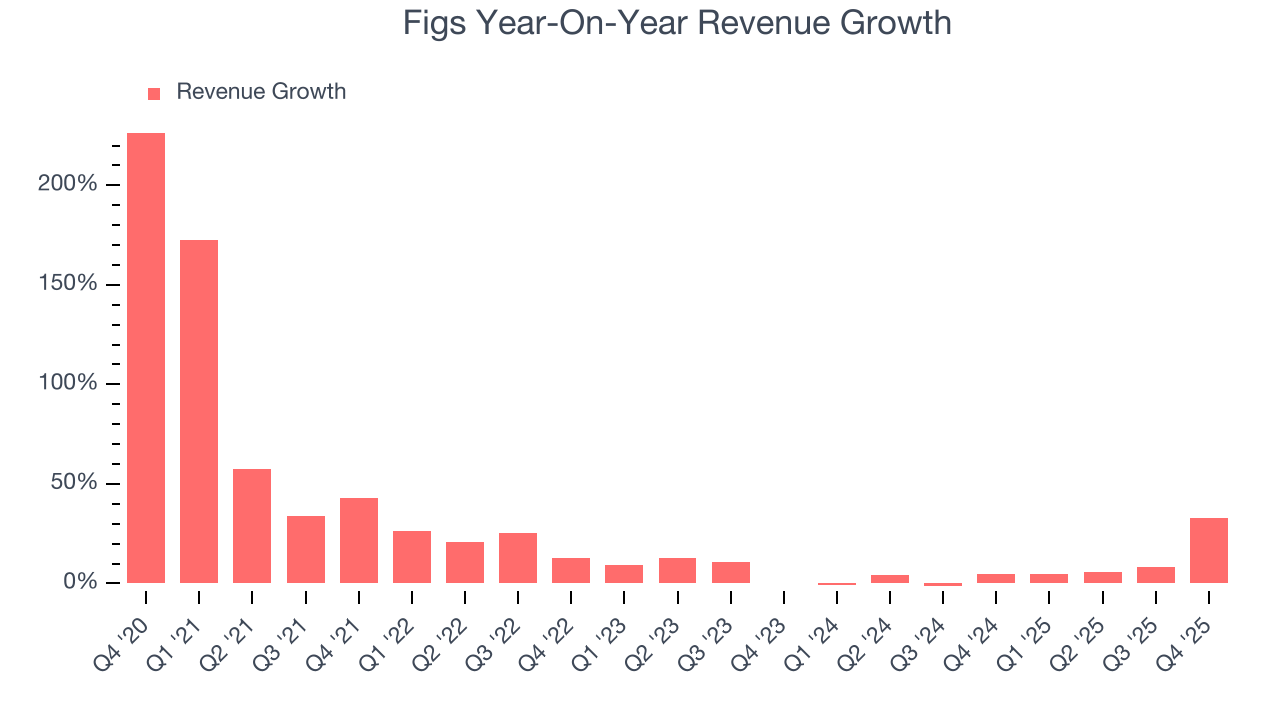

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Figs grew its sales at a 19.1% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Figs’s recent performance shows its demand has slowed as its annualized revenue growth of 7.5% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

We can better understand the company’s revenue dynamics by analyzing its number of active customers, which reached 2.92 million in the latest quarter. Over the last two years, Figs’s active customers averaged 5% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Figs reported wonderful year-on-year revenue growth of 33%, and its $201.9 million of revenue exceeded Wall Street’s estimates by 21.8%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

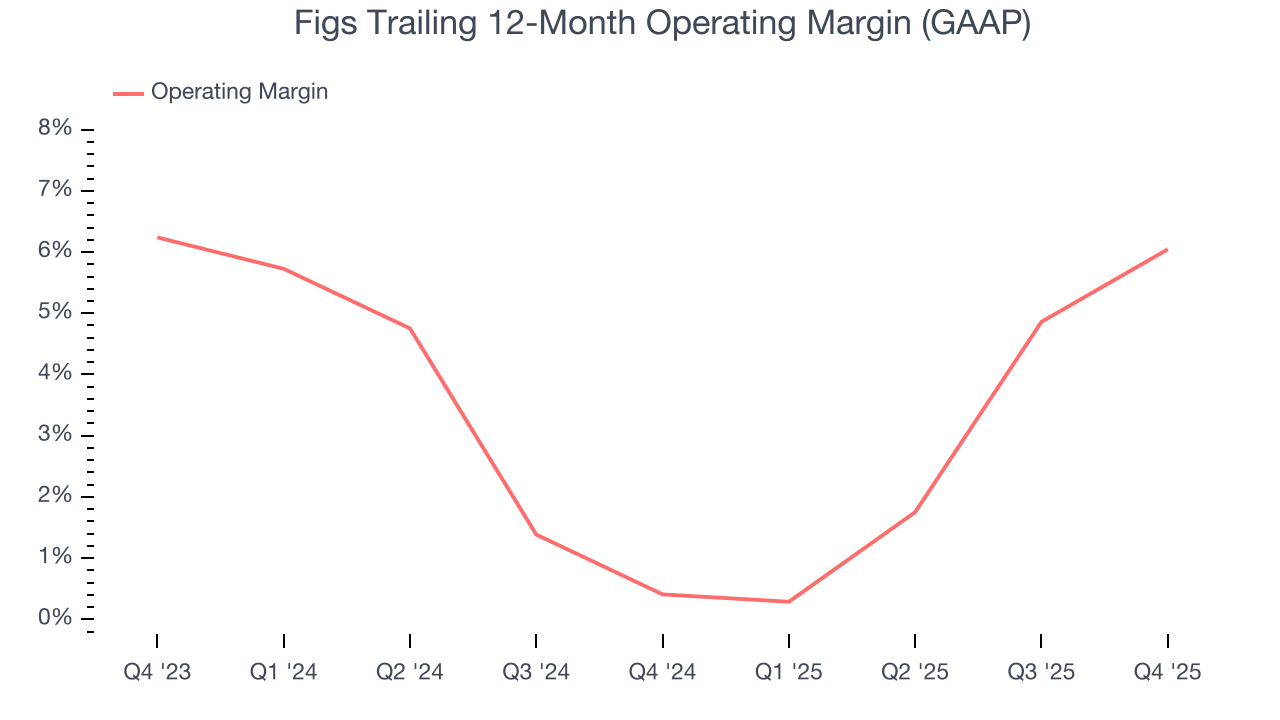

6. Operating Margin

Figs’s operating margin has been trending up over the last 12 months and averaged 3.4% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

This quarter, Figs generated an operating margin profit margin of 9.3%, up 3.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

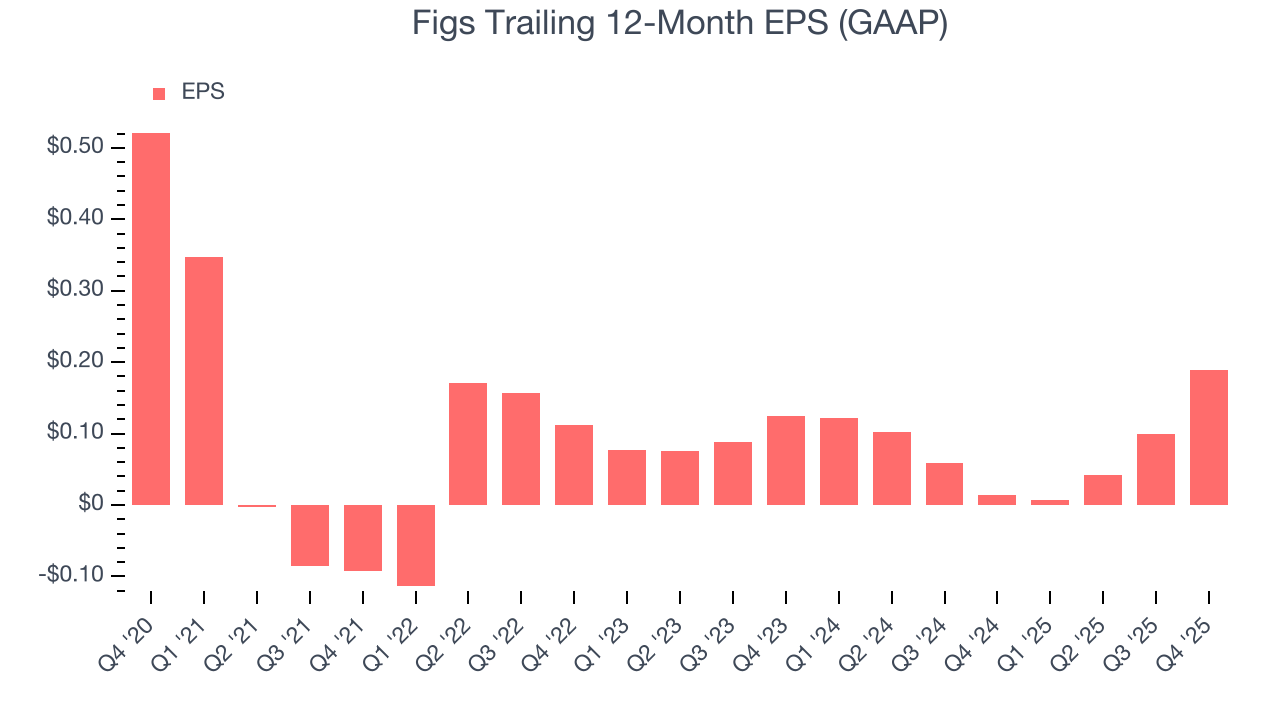

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Figs, its EPS declined by 18.3% annually over the last five years while its revenue grew by 19.1%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Figs reported EPS of $0.10, up from $0.01 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Figs’s full-year EPS of $0.19 to shrink by 39.3%.

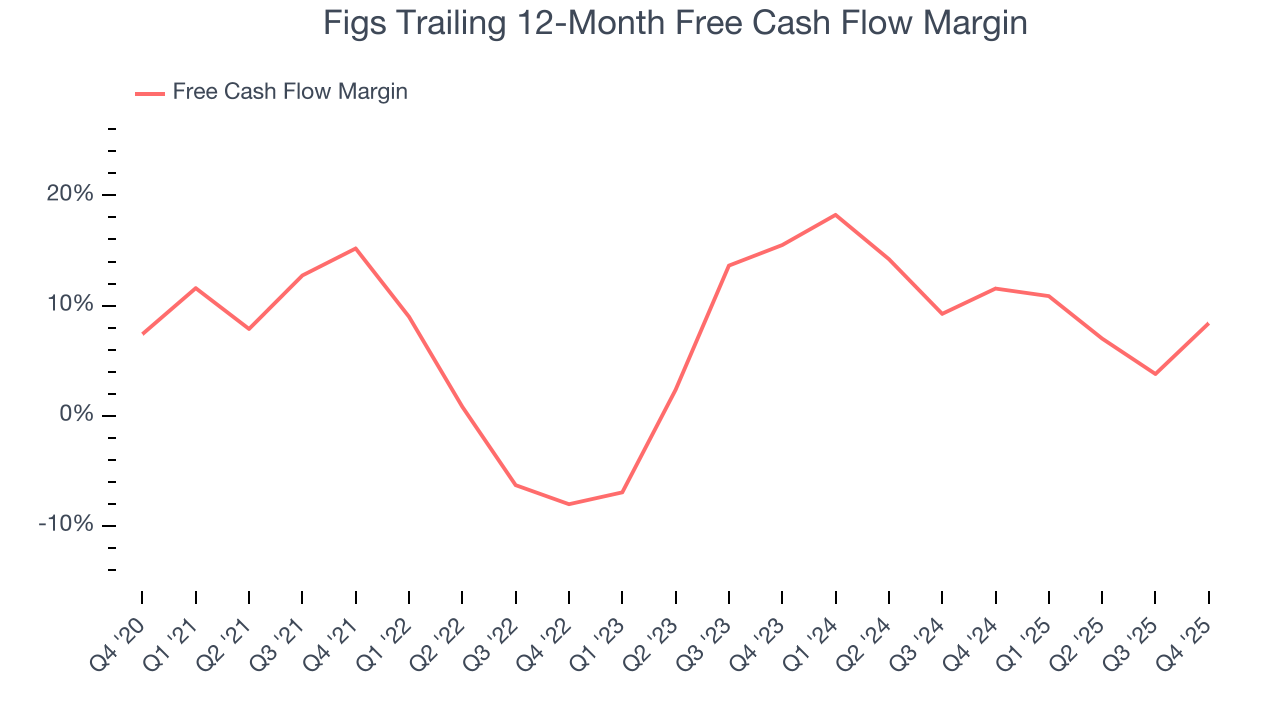

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Figs has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 9.9%, lousy for a consumer discretionary business.

Figs’s free cash flow clocked in at $58.07 million in Q4, equivalent to a 28.8% margin. This result was good as its margin was 10.9 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

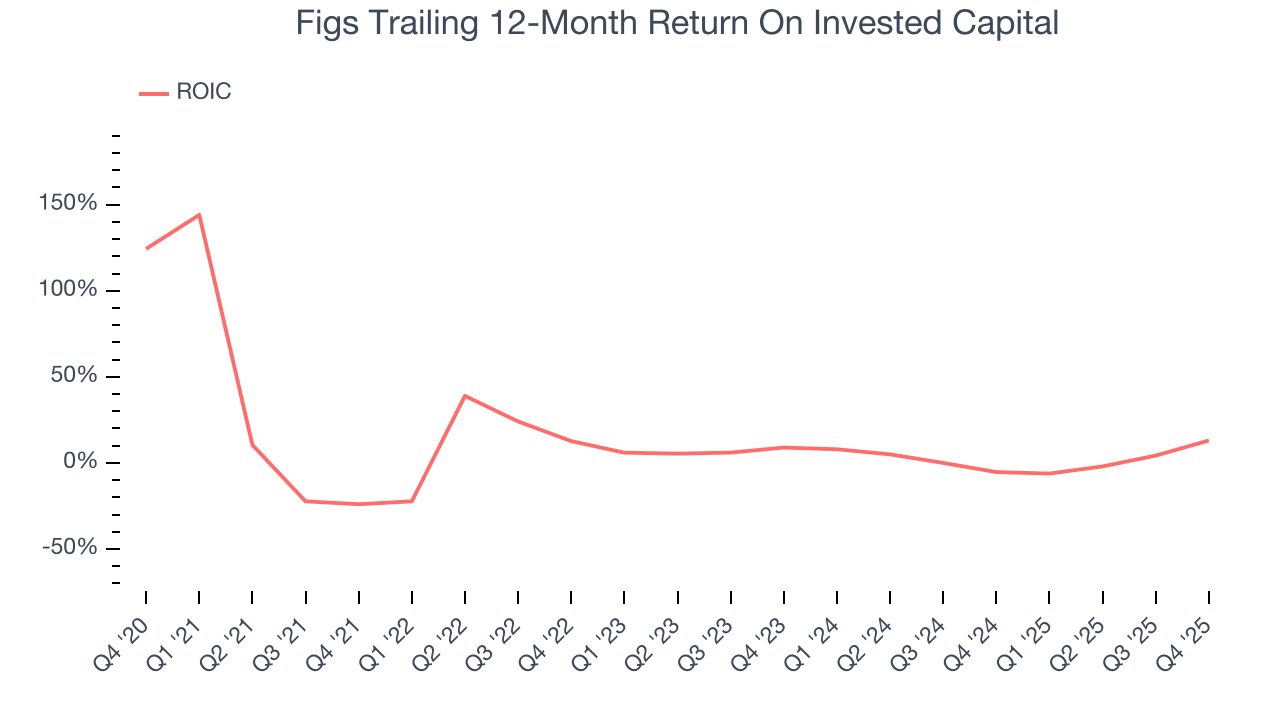

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Figs historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 1.1%, lower than the typical cost of capital (how much it costs to raise money) for consumer discretionary companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Figs’s has increased over the last few years. This is a good sign, and we hope the company can continue improving.

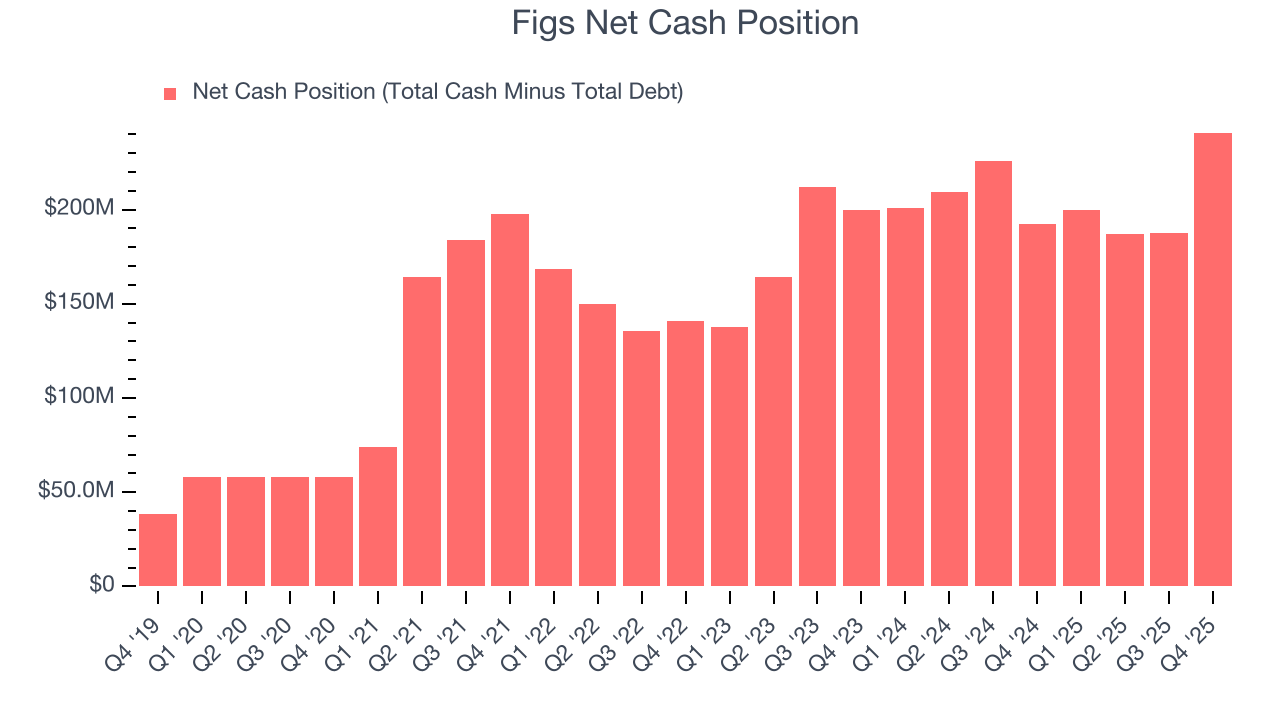

10. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Figs is a profitable, well-capitalized company with $300.8 million of cash and $60 million of debt on its balance sheet. This $240.8 million net cash position is 13.4% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Figs’s Q4 Results

It was good to see Figs beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 6.2% to $13.25 immediately following the results.

12. Is Now The Time To Buy Figs?

Updated: March 20, 2026 at 11:09 PM EDT

When considering an investment in Figs, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Figs doesn’t pass our quality test. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its Forecasted free cash flow margin for next year suggests the company will fail to improve its cash conversion. On top of that, its declining EPS over the last four years makes it a less attractive asset to the public markets.

Figs’s P/E ratio based on the next 12 months is 56.5x. This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $16.31 on the company (compared to the current share price of $14.22).