GoDaddy (GDDY)

GoDaddy faces an uphill battle. Its weak revenue growth and gross margin show it not only lacks demand but also decent unit economics.― StockStory Analyst Team

1. News

2. Summary

Why We Think GoDaddy Will Underperform

Known for its memorable Super Bowl commercials that put it on the map, GoDaddy (NYSE:GDDY) is a domain registrar and web services provider that helps entrepreneurs establish an online presence through domain registration, website building, hosting, and e-commerce tools.

- Offerings struggled to generate meaningful interest as its average billings growth of 5.5% over the last year did not impress

- Estimated sales growth of 5.7% for the next 12 months implies demand will slow from its two-year trend

- High servicing costs result in a relatively inferior gross margin of 63.6% that must be offset through increased usage

GoDaddy’s quality doesn’t meet our bar. Better stocks can be found in the market.

Why There Are Better Opportunities Than GoDaddy

GoDaddy’s stock price of $79.83 implies a valuation ratio of 2.1x forward price-to-sales. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. GoDaddy (GDDY) Research Report: Q4 CY2025 Update

Domain registrar and web services company GoDaddy (NYSE:GDDY) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 6.8% year on year to $1.27 billion. On the other hand, next quarter’s revenue guidance of $1.26 billion was less impressive, coming in 1.4% below analysts’ estimates. Its GAAP profit of $1.80 per share was 14% above analysts’ consensus estimates.

GoDaddy (GDDY) Q4 CY2025 Highlights:

- Revenue: $1.27 billion vs analyst estimates of $1.27 billion (6.8% year-on-year growth, in line)

- EPS (GAAP): $1.80 vs analyst estimates of $1.58 (14% beat)

- Adjusted EBITDA: $431.2 million vs analyst estimates of $418.8 million (33.8% margin, 3% beat)

- Revenue Guidance for Q1 CY2026 is $1.26 billion at the midpoint, below analyst estimates of $1.28 billion

- Operating Margin: 24.9%, up from 21.4% in the same quarter last year

- Free Cash Flow Margin: 29.1%, down from 34.8% in the previous quarter

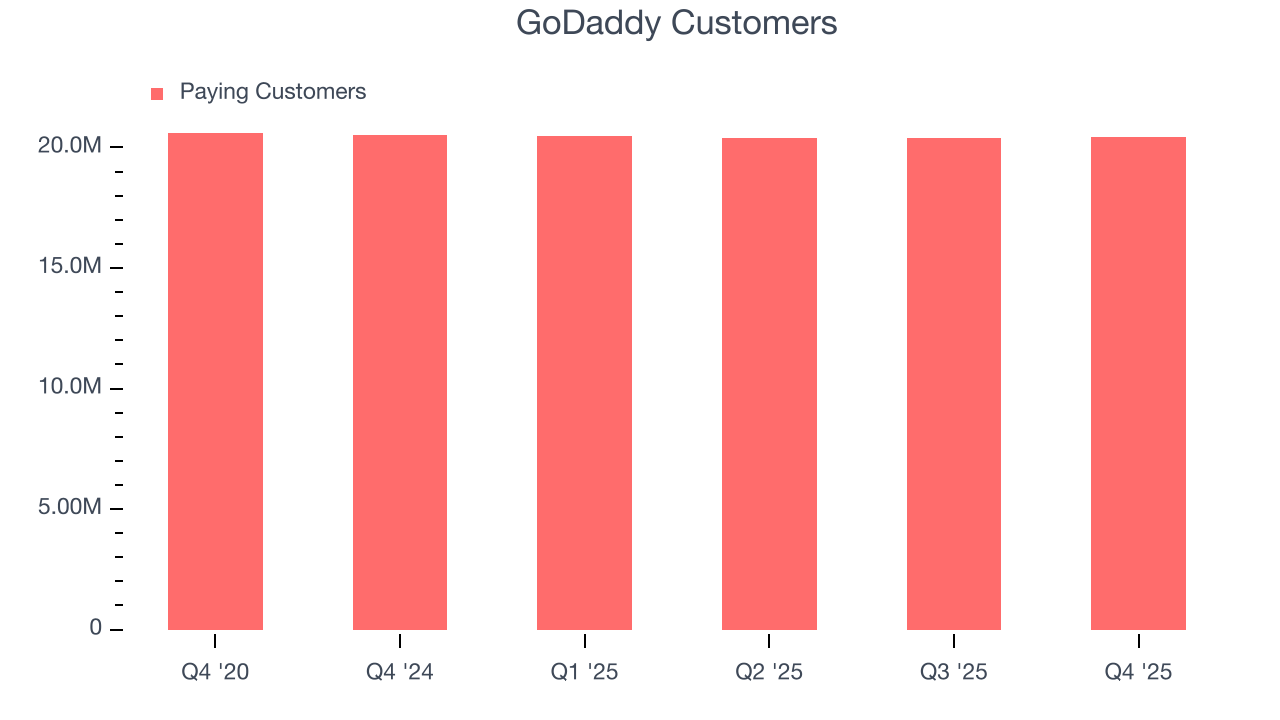

- Customers: 20.42 million, up from 20.41 million in the previous quarter

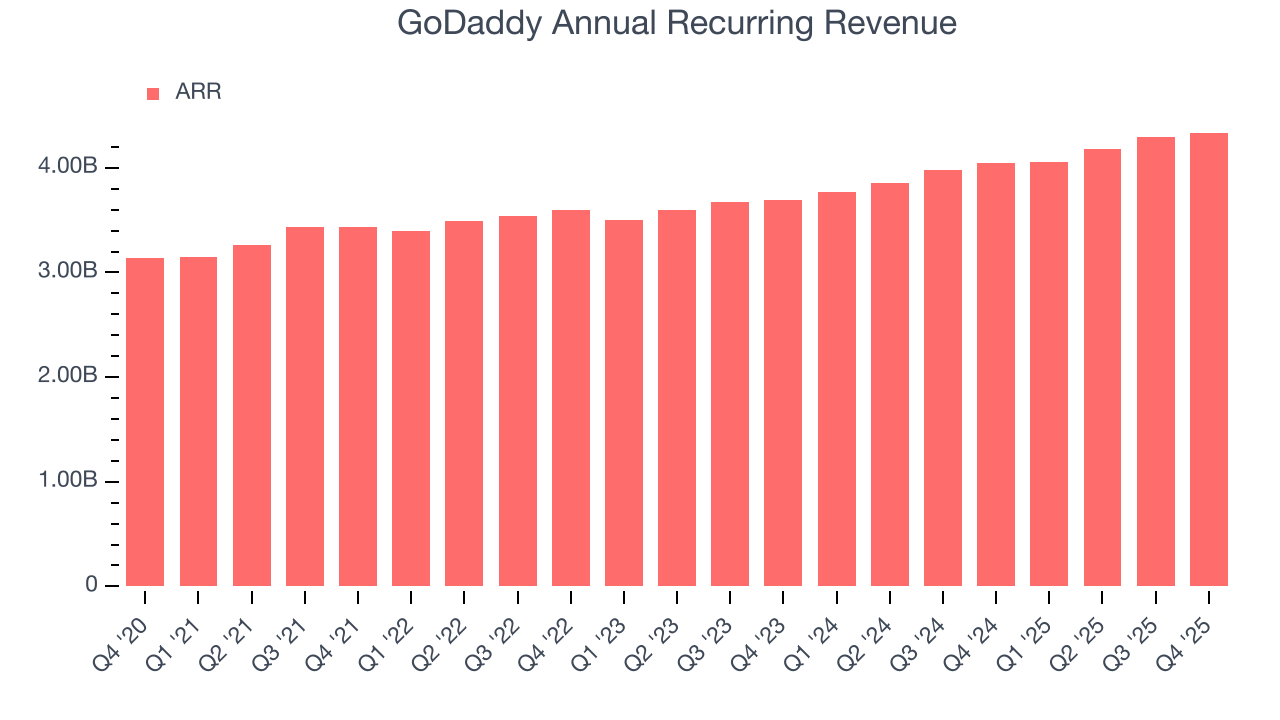

- Annual Recurring Revenue: $4.34 billion (7.3% year-on-year growth, beat)

- Billings: $1.23 billion at quarter end, up 5.5% year on year

- Market Capitalization: $11.86 billion

Company Overview

Known for its memorable Super Bowl commercials that put it on the map, GoDaddy (NYSE:GDDY) is a domain registrar and web services provider that helps entrepreneurs establish an online presence through domain registration, website building, hosting, and e-commerce tools.

The company operates in a "one-stop shop" model, providing solutions across the entire digital journey of small businesses and individuals. Beyond its core domain registration service with approximately 85 million domains under management (representing about 24% of all registered domains worldwide), GoDaddy offers a comprehensive ecosystem of products tailored to different customer segments.

For those building websites, GoDaddy provides both simplified solutions like Websites + Marketing for non-technical users and more flexible options like Managed WordPress for developers. Its commerce offerings enable customers to sell products online through integrated storefronts, in physical locations via point-of-sale systems, and across marketplaces like Amazon and social platforms like Instagram.

The company has expanded its toolkit with GoDaddy Airo, an AI-powered solution that creates personalized website content, logos, and marketing materials. It also offers productivity tools like professional email services through Microsoft 365 integration, security products including SSL certificates, and web hosting services ranging from basic shared hosting to virtual private servers.

GoDaddy generates revenue through subscription-based services and transaction fees from its payment processing system, GoDaddy Payments. The company serves various customer segments including "Independents" (primarily microbusinesses), "WebPros" (website designers and developers building sites for clients), domain investors, and corporate domain portfolio owners. With approximately 48% of its customers located outside the U.S., GoDaddy has invested significantly in localizing its offerings for international markets.

4. E-commerce Software

While e-commerce has been around for over two decades and enjoyed meaningful growth, its overall penetration of retail still remains low. Only around $1 in every $5 spent on retail purchases comes from digital orders, leaving over 80% of the retail market still ripe for online disruption. It is these large swathes of the retail where e-commerce has not yet taken hold that drives the demand for various e-commerce software solutions.

GoDaddy's competitors include domain registrars like Namecheap and Network Solutions, website building platforms such as Wix (NASDAQ: WIX), Squarespace (NYSE: SQSP), and Shopify (NYSE: SHOP), as well as hosting providers like Cloudflare (NYSE: NET), DigitalOcean (NYSE: DOCN), and Bluehost.

5. Revenue Growth

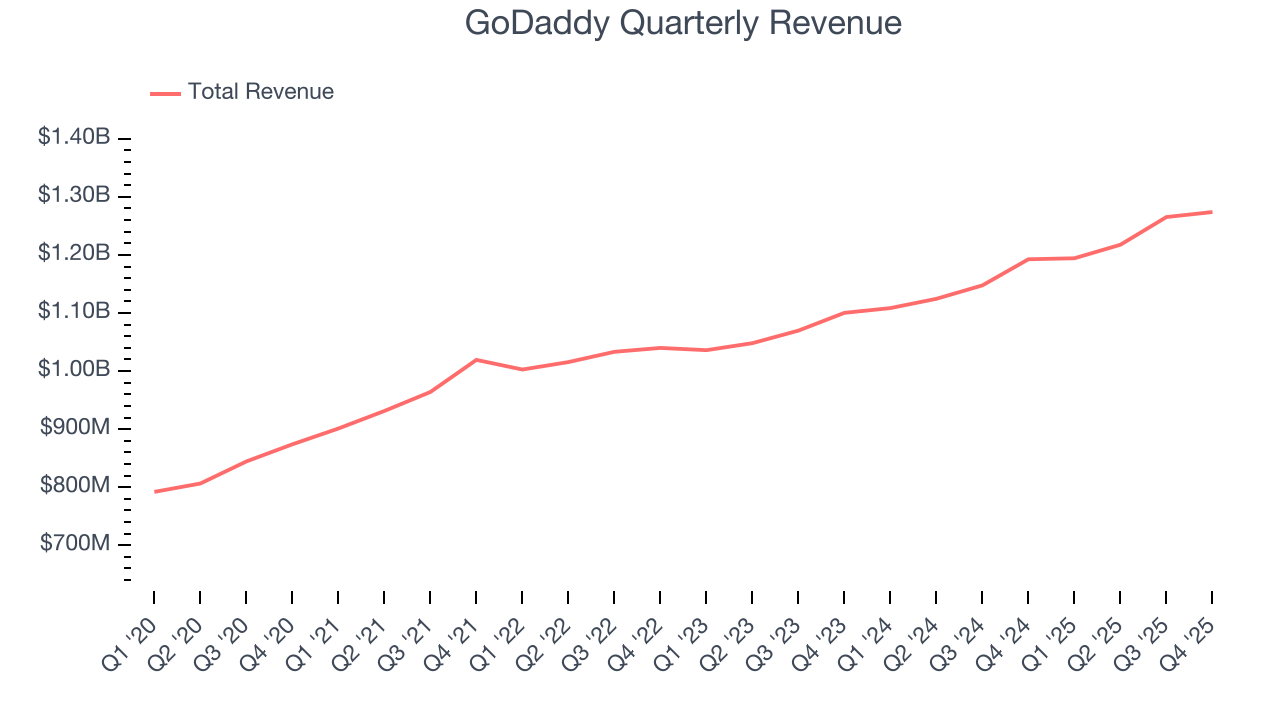

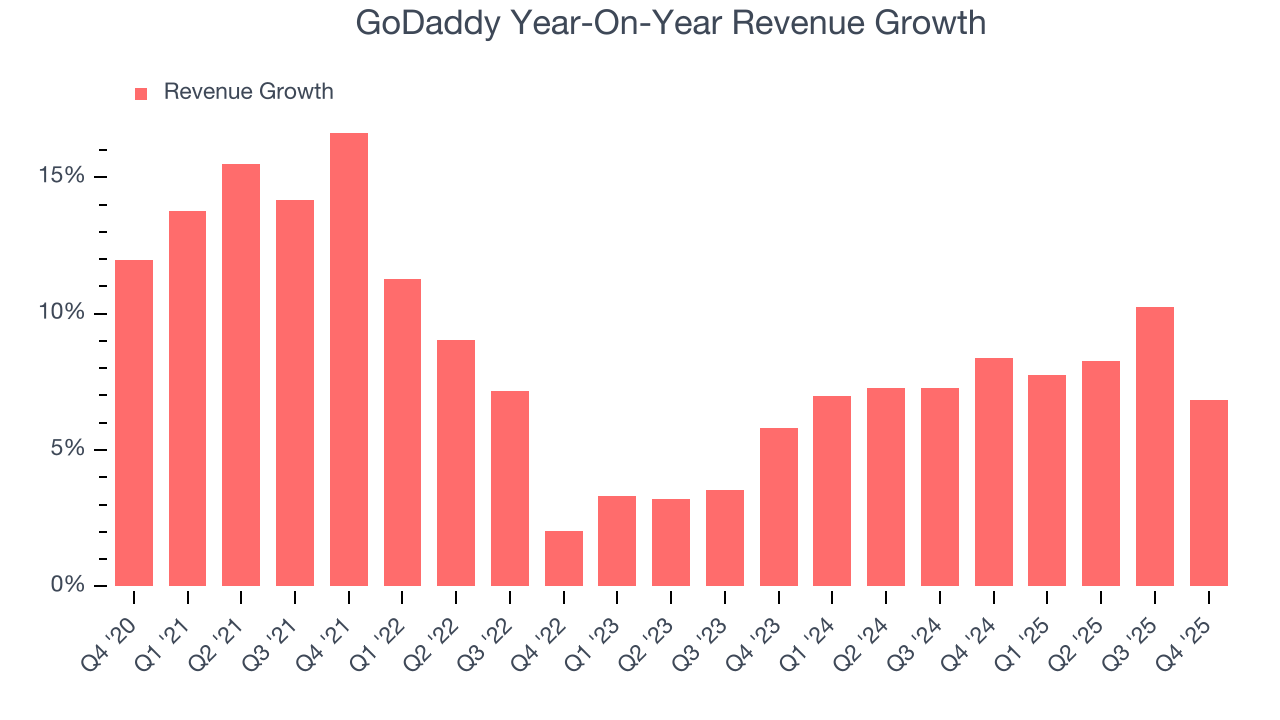

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, GoDaddy’s 8.3% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the software sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. GoDaddy’s annualized revenue growth of 7.9% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, GoDaddy grew its revenue by 6.8% year on year, and its $1.27 billion of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 5.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.6% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

6. Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

GoDaddy’s ARR came in at $4.34 billion in Q4, and over the last four quarters, its growth was underwhelming as it averaged 7.8% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in securing longer-term commitments.

7. Customer Base

GoDaddy reported 20.42 million customers at the end of the quarter, a sequential increase of 9,000. That’s a little better than last quarter and quite a bit above the typical growth we’ve seen over the previous year. However, the increase in customers wasn’t backed by an equivalent increase in annualized recurring revenue (ARR), suggesting that GoDaddy is disproportionately winning smaller customers.

8. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for GoDaddy to acquire new customers as its CAC payback period checked in at 147.4 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

9. Gross Margin & Pricing Power

For software companies like GoDaddy, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

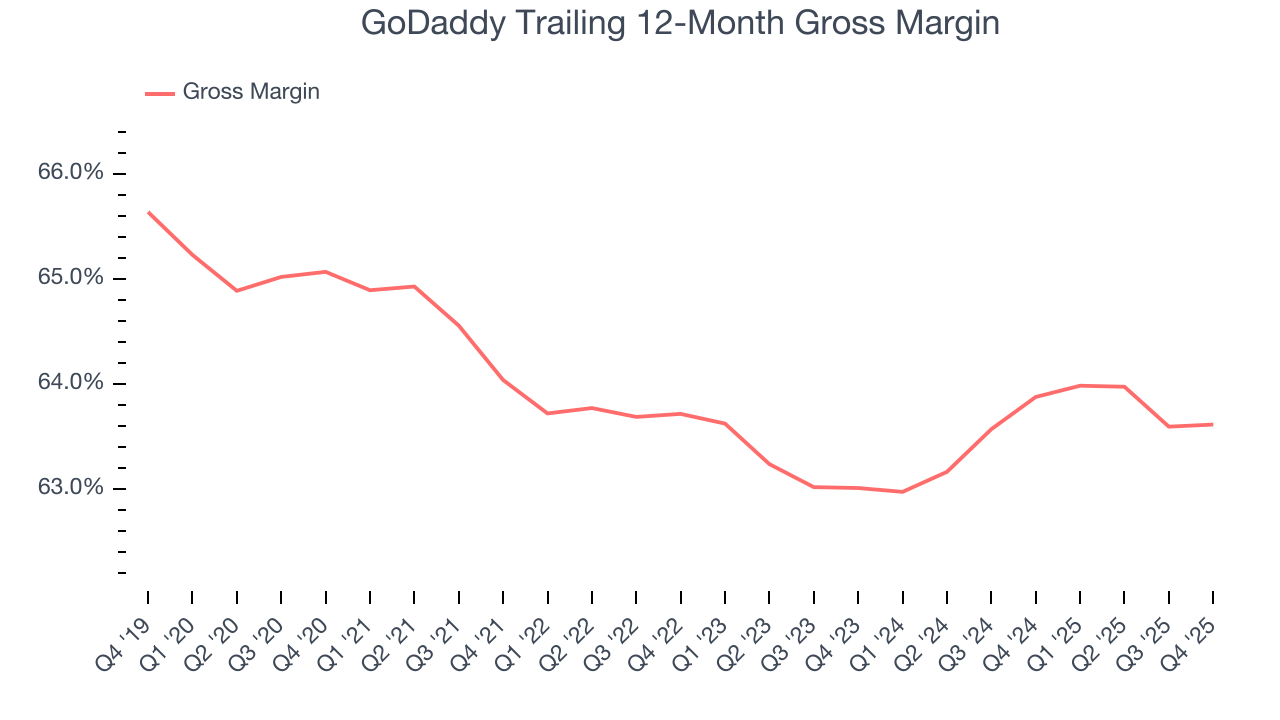

GoDaddy’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 63.6% gross margin over the last year. Said differently, GoDaddy had to pay a chunky $36.39 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. GoDaddy has seen gross margins improve by 0.6 percentage points over the last 2 year, which is slightly better than average for software.

GoDaddy’s gross profit margin came in at 64.6% this quarter, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

10. Operating Margin

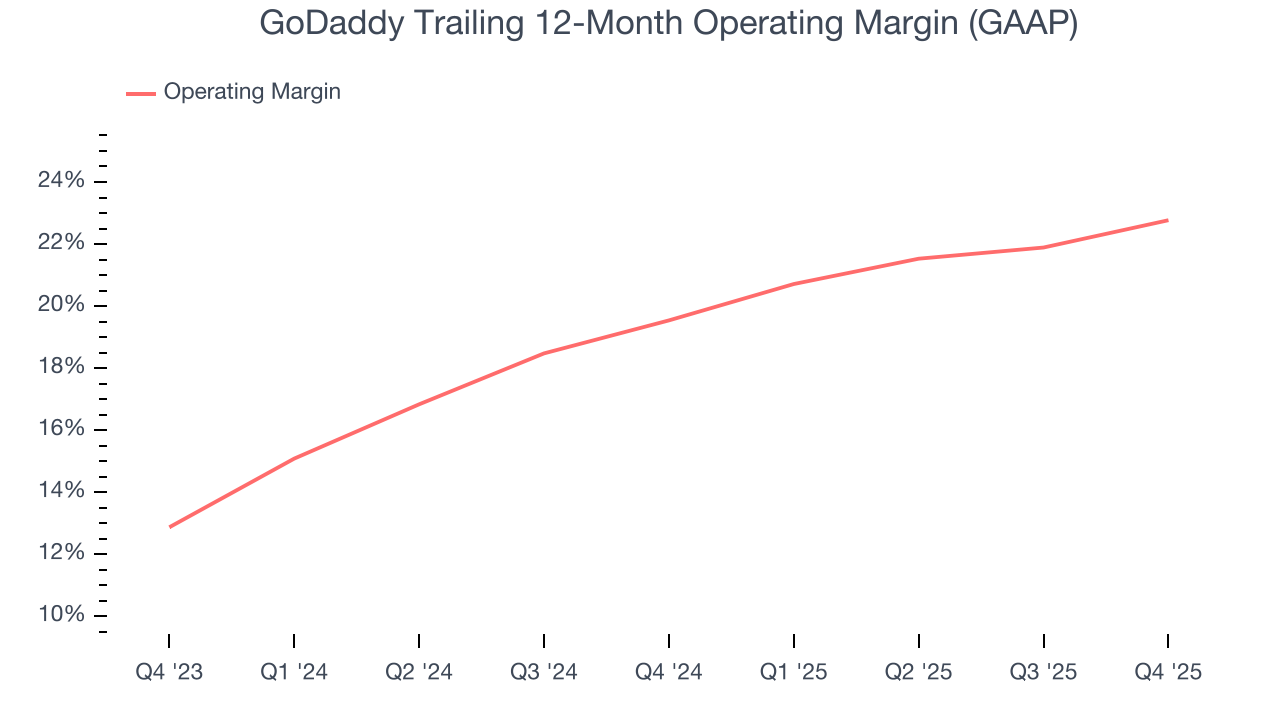

GoDaddy has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 22.8%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, GoDaddy’s operating margin rose by 3.2 percentage points over the last two years, as its sales growth gave it operating leverage.

This quarter, GoDaddy generated an operating margin profit margin of 24.9%, up 3.5 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

11. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

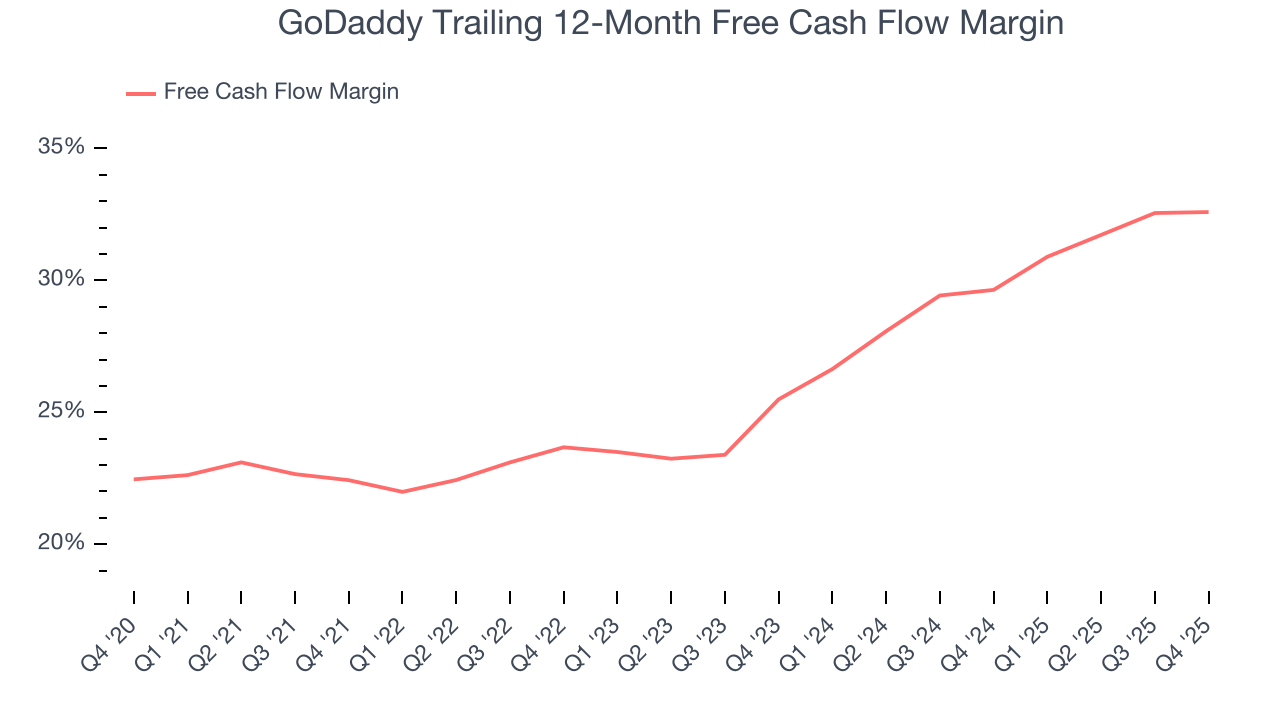

GoDaddy has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 32.6% over the last year.

GoDaddy’s free cash flow clocked in at $370.3 million in Q4, equivalent to a 29.1% margin. This cash profitability was in line with the comparable period last year but below its one-year average. In a silo, this isn’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts predict GoDaddy’s cash conversion will improve. Their consensus estimates imply its free cash flow margin of 32.6% for the last 12 months will increase to 35.8%, it options for capital deployment (investments, share buybacks, etc.).

12. Balance Sheet Assessment

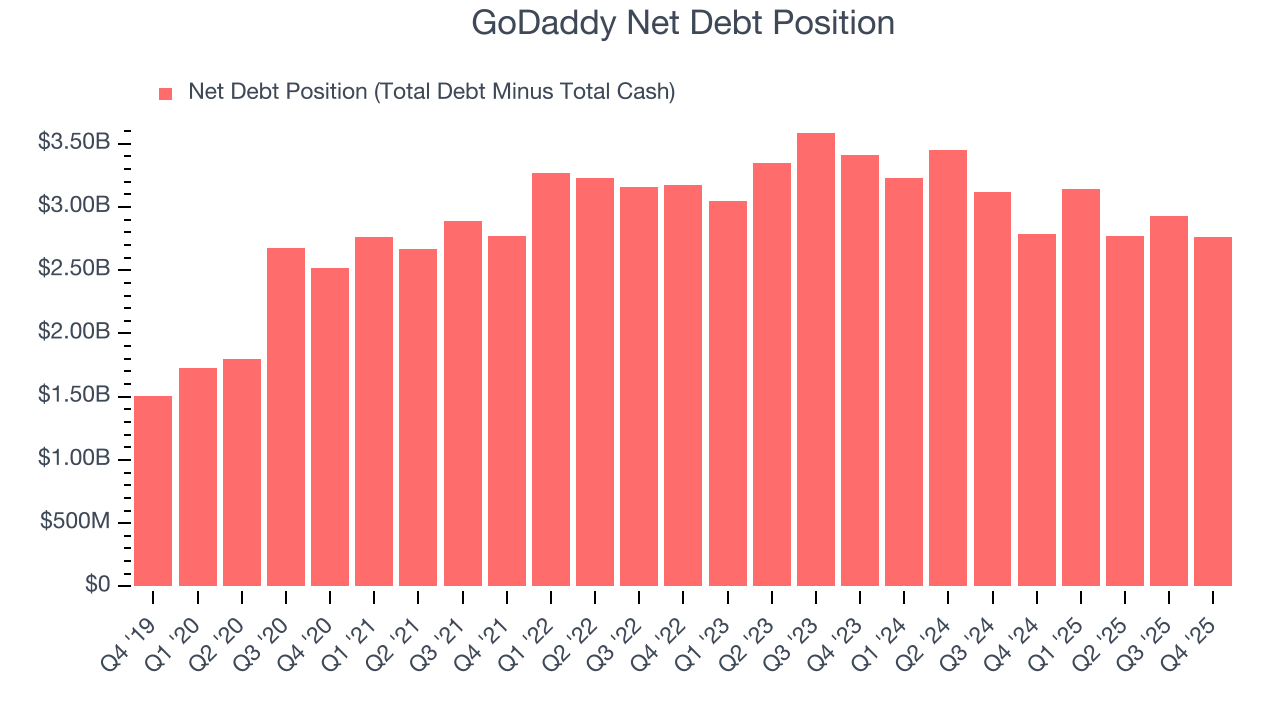

GoDaddy reported $1.08 billion of cash and $3.84 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.59 billion of EBITDA over the last 12 months, we view GoDaddy’s 1.7× net-debt-to-EBITDA ratio as safe. We also see its $151 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from GoDaddy’s Q4 Results

It was encouraging to see GoDaddy beat analysts’ EBITDA expectations this quarter. We were also happy its annual recurring revenue narrowly outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter slightly missed and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 6.4% to $86.41 immediately following the results.

14. Is Now The Time To Buy GoDaddy?

Updated: March 29, 2026 at 10:21 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own GoDaddy, you should also grasp the company’s longer-term business quality and valuation.

GoDaddy doesn’t pass our quality test. To begin with, its revenue growth was weak over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its impressive operating margins show it has a highly efficient business model, the downside is its bookings have disappointed as fewer customers are signing sales agreements. On top of that, its ARR has disappointed and shows the company is having difficulty retaining customers and their spending.

GoDaddy’s price-to-sales ratio based on the next 12 months is 2.1x. While this valuation is fair, the upside isn’t great compared to the potential downside. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $117.67 on the company (compared to the current share price of $79.83).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.