JELD-WEN (JELD)

We wouldn’t recommend JELD-WEN. Its falling revenue and negative returns on capital suggest it’s destroying value as demand fizzles out.― StockStory Analyst Team

1. News

2. Summary

Why We Think JELD-WEN Will Underperform

Founded in the 1960s as a general wood-making company, JELD-WEN (NYSE:JELD) manufactures doors, windows, and other related building products.

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 4.5% annually over the last five years

- Sales were less profitable over the last five years as its earnings per share fell by 18.9% annually, worse than its revenue declines

- Short cash runway increases the probability of a capital raise that dilutes existing shareholders

JELD-WEN’s quality isn’t great. There are more appealing investments to be made.

Why There Are Better Opportunities Than JELD-WEN

JELD-WEN’s stock price of $3.03 implies a valuation ratio of 11.3x forward EV-to-EBITDA. This multiple is lower than most industrials companies, but for good reason.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. JELD-WEN (JELD) Research Report: Q3 CY2025 Update

Building products manufacturer JELD-WEN (NYSE:JELD) fell short of the markets revenue expectations in Q3 CY2025, with sales falling 13.4% year on year to $809.5 million. The company’s full-year revenue guidance of $3.15 billion at the midpoint came in 2.9% below analysts’ estimates. Its non-GAAP loss of $0.20 per share was significantly below analysts’ consensus estimates.

JELD-WEN (JELD) Q3 CY2025 Highlights:

- Revenue: $809.5 million vs analyst estimates of $825.7 million (13.4% year-on-year decline, 2% miss)

- Adjusted EPS: -$0.20 vs analyst estimates of $0.14 (significant miss)

- Adjusted EBITDA: $44.4 million vs analyst estimates of $57.56 million (5.5% margin, 22.9% miss)

- The company dropped its revenue guidance for the full year to $3.15 billion at the midpoint from $3.3 billion, a 4.5% decrease

- EBITDA guidance for the full year is $112.5 million at the midpoint, below analyst estimates of $173.2 million

- Operating Margin: -25%, down from -5.6% in the same quarter last year

- Free Cash Flow was -$13.1 million compared to -$6.2 million in the same quarter last year

- Organic Revenue fell 10% year on year

- Market Capitalization: $370.6 million

Company Overview

Founded in the 1960s as a general wood-making company, JELD-WEN (NYSE:JELD) manufactures doors, windows, and other related building products.

The company serves the North American and European construction market with building materials. Simply put, its products give homebuilders the materials and products needed to build new homes and remodel existing ones.

JELD-WEN’s products include interior and exterior doors like patio doors and sliding door systems. It also offers non-residential doors made of steel, glass, and fiberglass to meet the often custom needs of enterprise customers. Its window products range from wood and vinyl residential windows to multi-pane windows with high-performance glazing that boast superior energy efficiency. The company’s offerings try to strike a balance between utility and aesthetics.

Door and window sales constitute the vast majority of JELD-WEN’s revenue. While the company does provide some installation services, they do not generate a meaningful portion of sales.

4. Home Construction Materials

Traditionally, home construction materials companies have built economic moats with expertise in specialized areas, brand recognition, and strong relationships with contractors. More recently, advances to address labor availability and job site productivity have spurred innovation that is driving incremental demand. However, these companies are at the whim of residential construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of home construction materials companies.

Competitors offering door and window building materials include Masonite (NYSE:DOOR), and private companies Pella and Ply Gem.

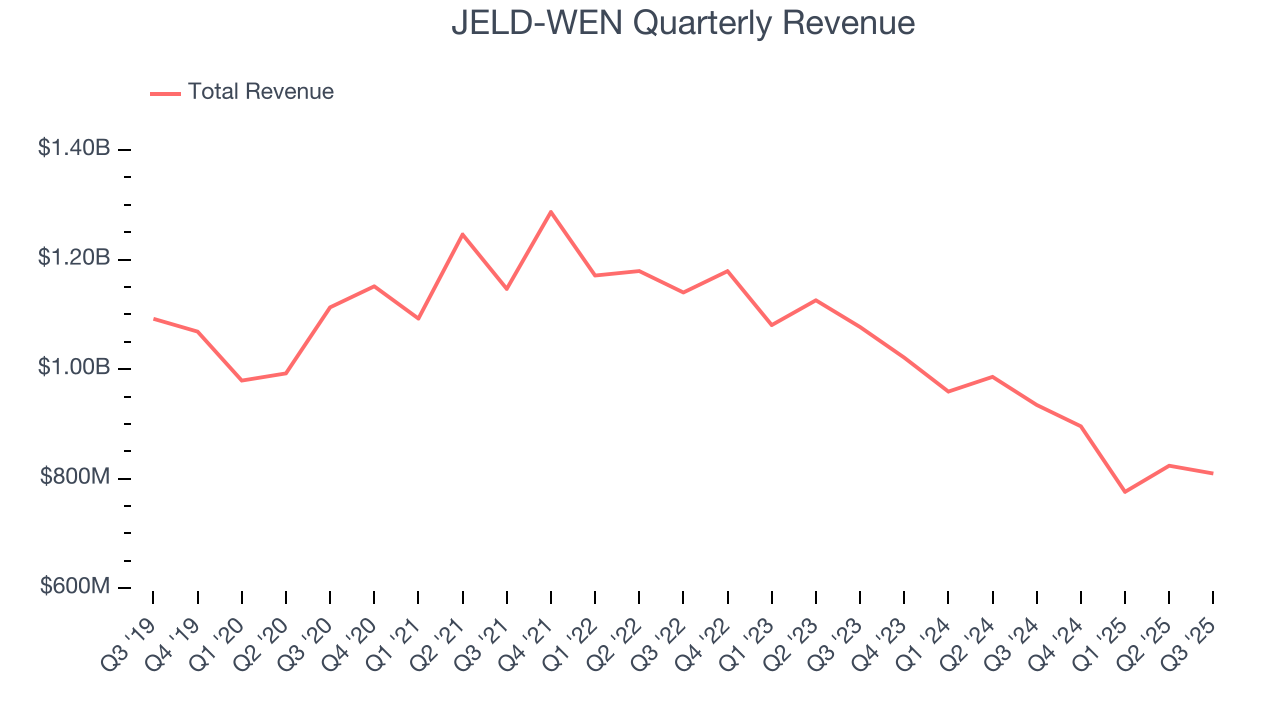

5. Revenue Growth

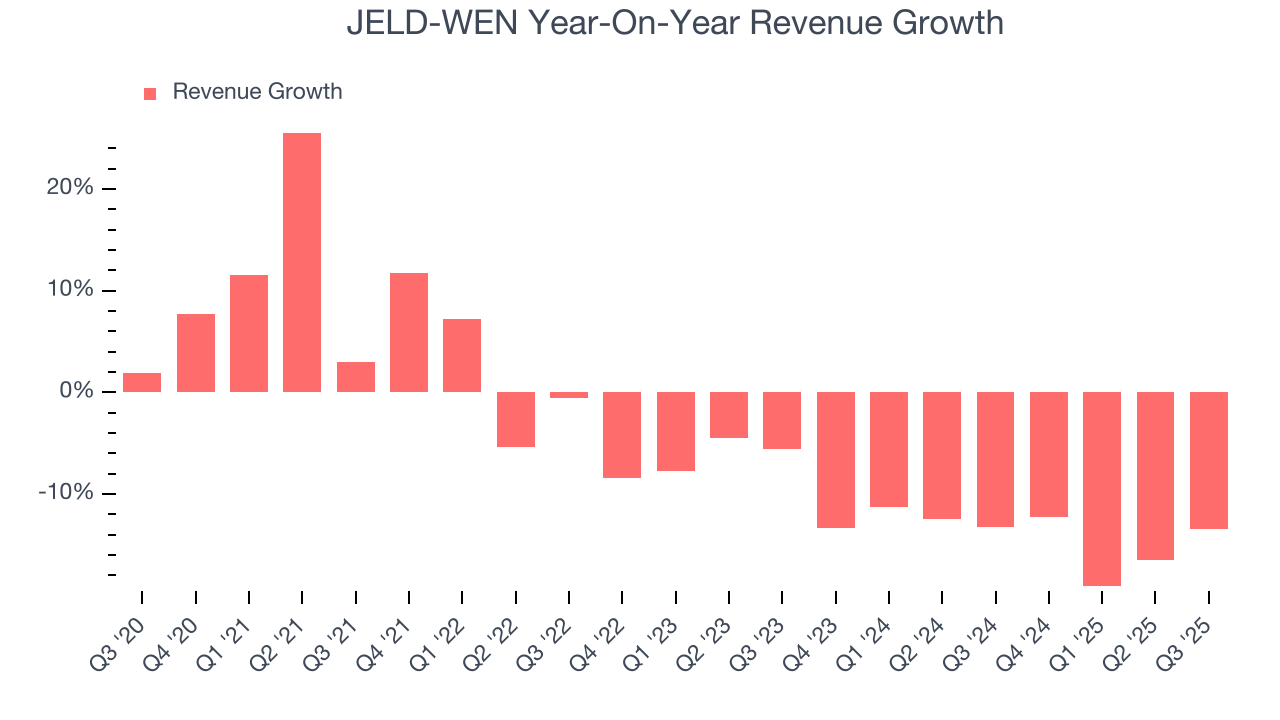

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. JELD-WEN’s demand was weak over the last five years as its sales fell at a 4.5% annual rate. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. JELD-WEN’s recent performance shows its demand remained suppressed as its revenue has declined by 13.9% annually over the last two years.

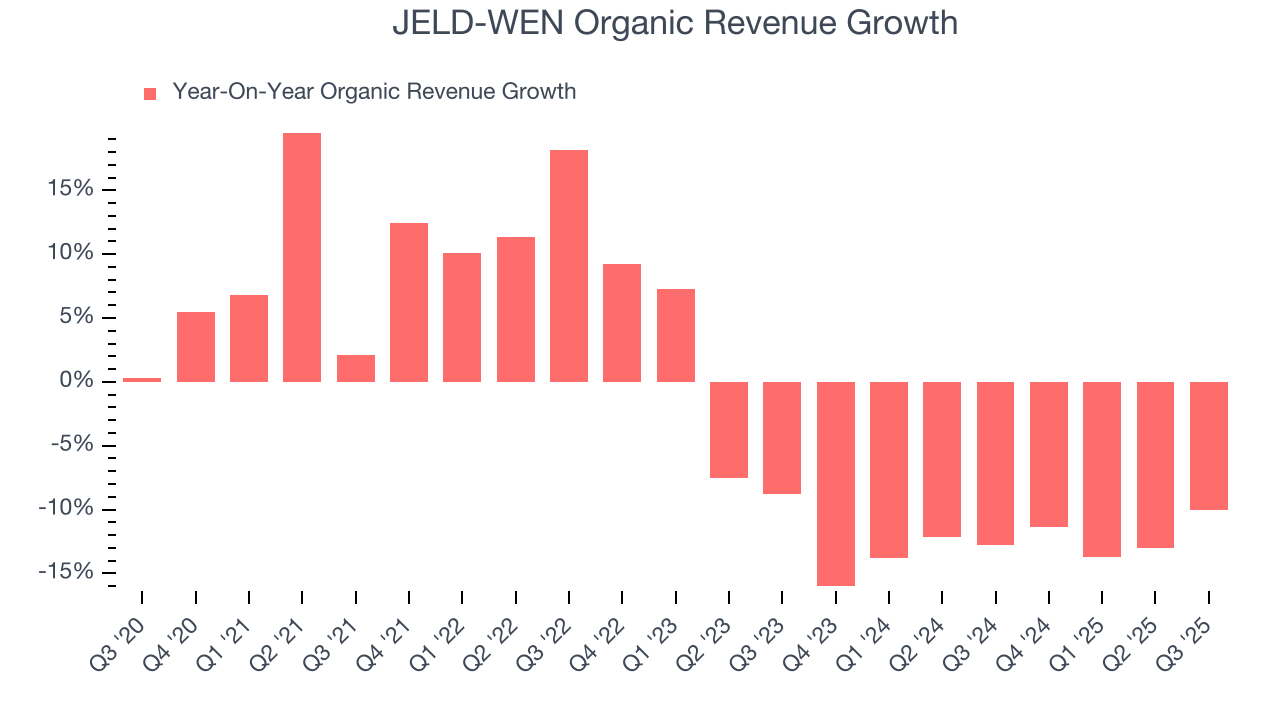

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, JELD-WEN’s organic revenue averaged 12.9% year-on-year declines. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, JELD-WEN missed Wall Street’s estimates and reported a rather uninspiring 13.4% year-on-year revenue decline, generating $809.5 million of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

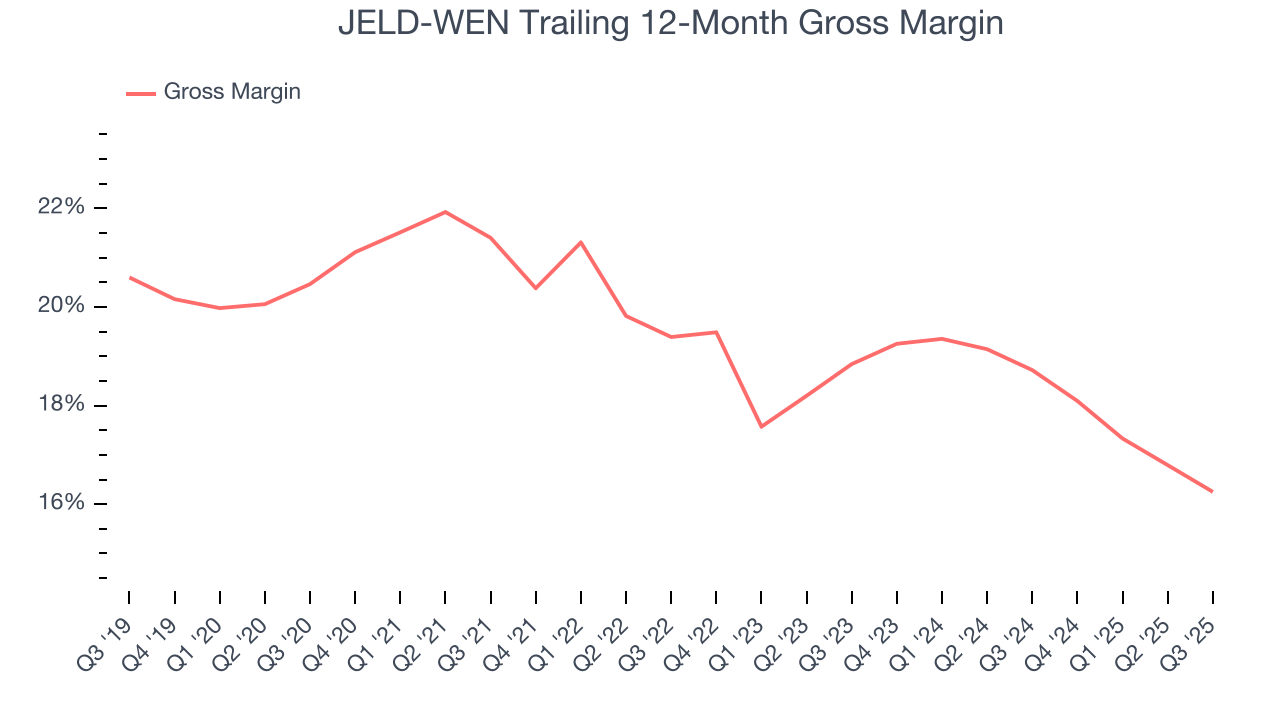

6. Gross Margin & Pricing Power

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

JELD-WEN has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 19.1% gross margin over the last five years. That means JELD-WEN paid its suppliers a lot of money ($80.90 for every $100 in revenue) to run its business.

This quarter, JELD-WEN’s gross profit margin was 17.4%, marking a 1.8 percentage point decrease from 19.2% in the same quarter last year. JELD-WEN’s full-year margin has also been trending down over the past 12 months, decreasing by 2.5 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

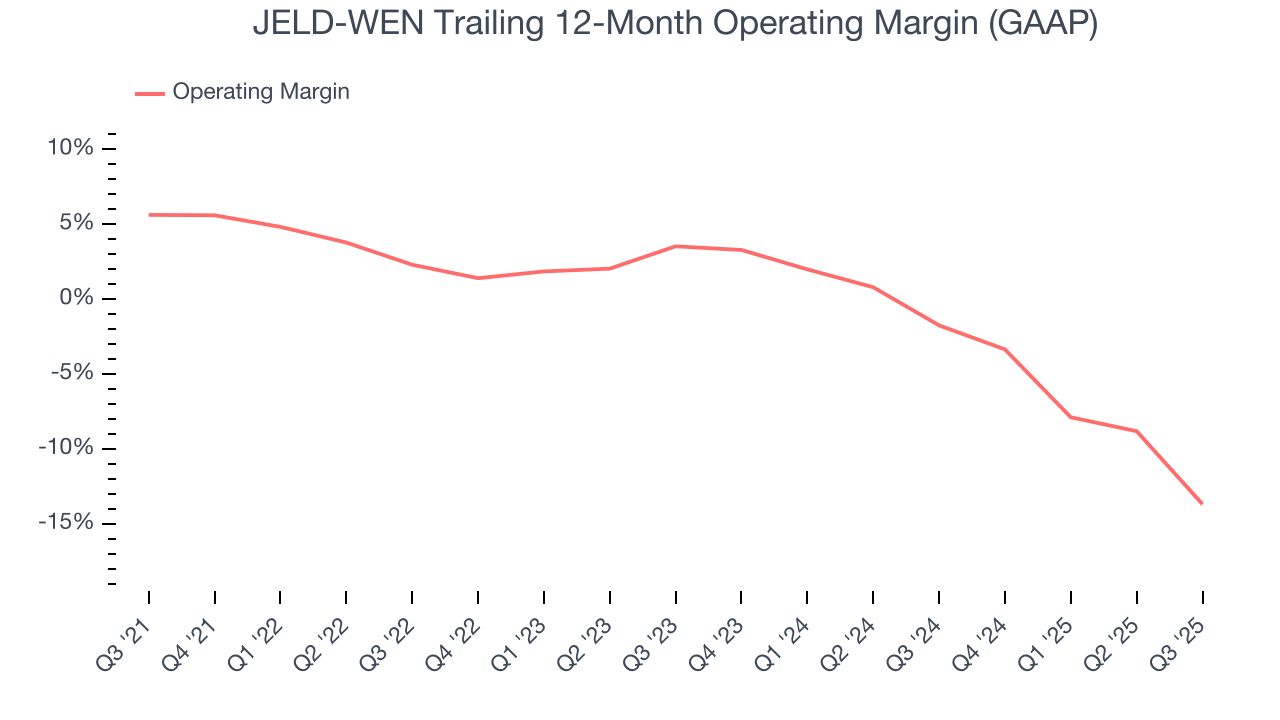

7. Operating Margin

JELD-WEN was roughly breakeven when averaging the last five years of quarterly operating profits, inadequate for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, JELD-WEN’s operating margin decreased by 19.3 percentage points over the last five years. JELD-WEN’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, JELD-WEN generated an operating margin profit margin of negative 25%, down 19.4 percentage points year on year. Since JELD-WEN’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

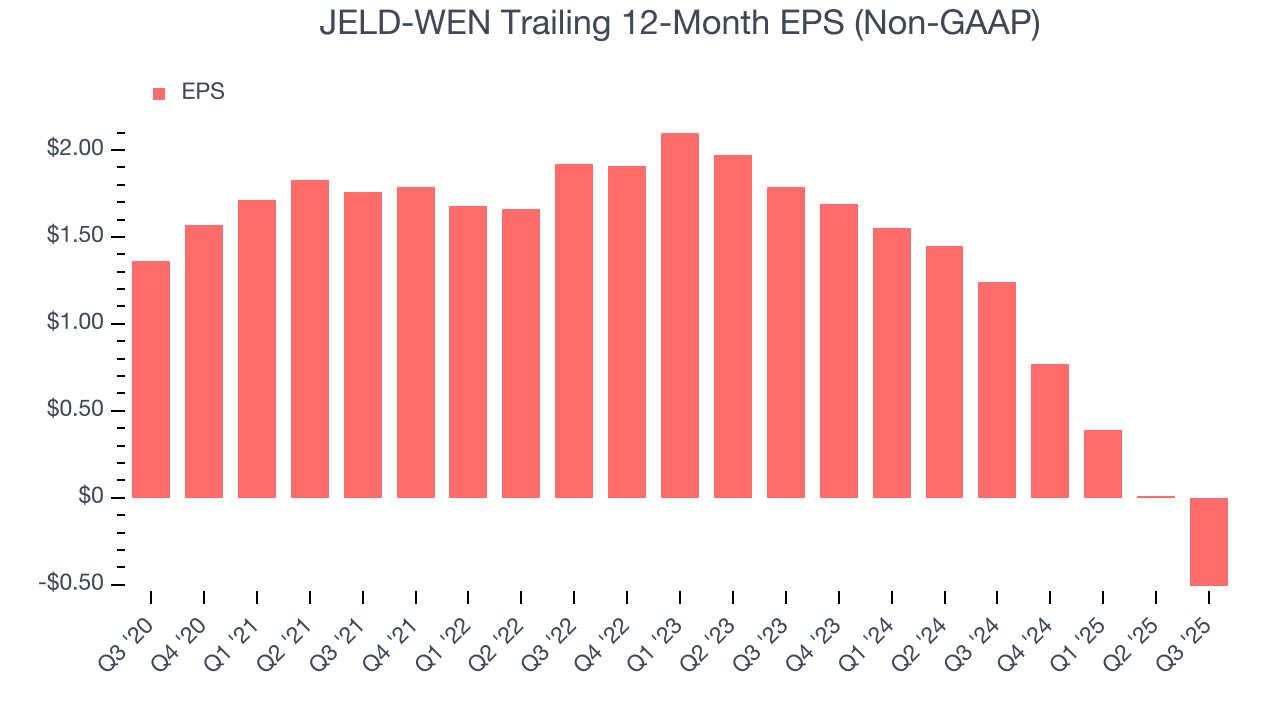

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for JELD-WEN, its EPS declined by 18.9% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Diving into the nuances of JELD-WEN’s earnings can give us a better understanding of its performance. As we mentioned earlier, JELD-WEN’s operating margin declined by 19.3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For JELD-WEN, its two-year annual EPS declines of 51.2% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q3, JELD-WEN reported adjusted EPS of negative $0.20, down from $0.32 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast JELD-WEN’s full-year EPS of negative $0.51 will flip to positive $0.34.

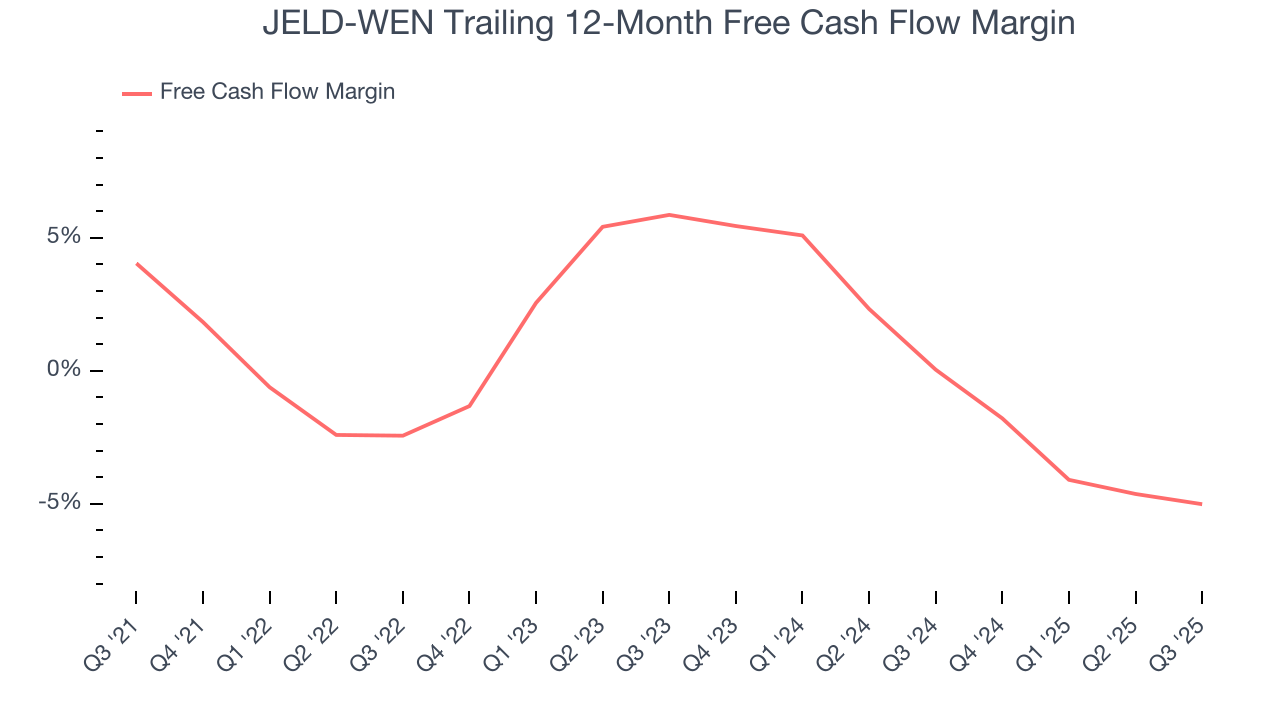

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

JELD-WEN broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, we can see that JELD-WEN’s margin dropped by 9.1 percentage points during that time. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s in the middle of a big investment cycle.

JELD-WEN burned through $13.1 million of cash in Q3, equivalent to a negative 1.6% margin. The company’s cash burn was similar to its $6.2 million of lost cash in the same quarter last year.

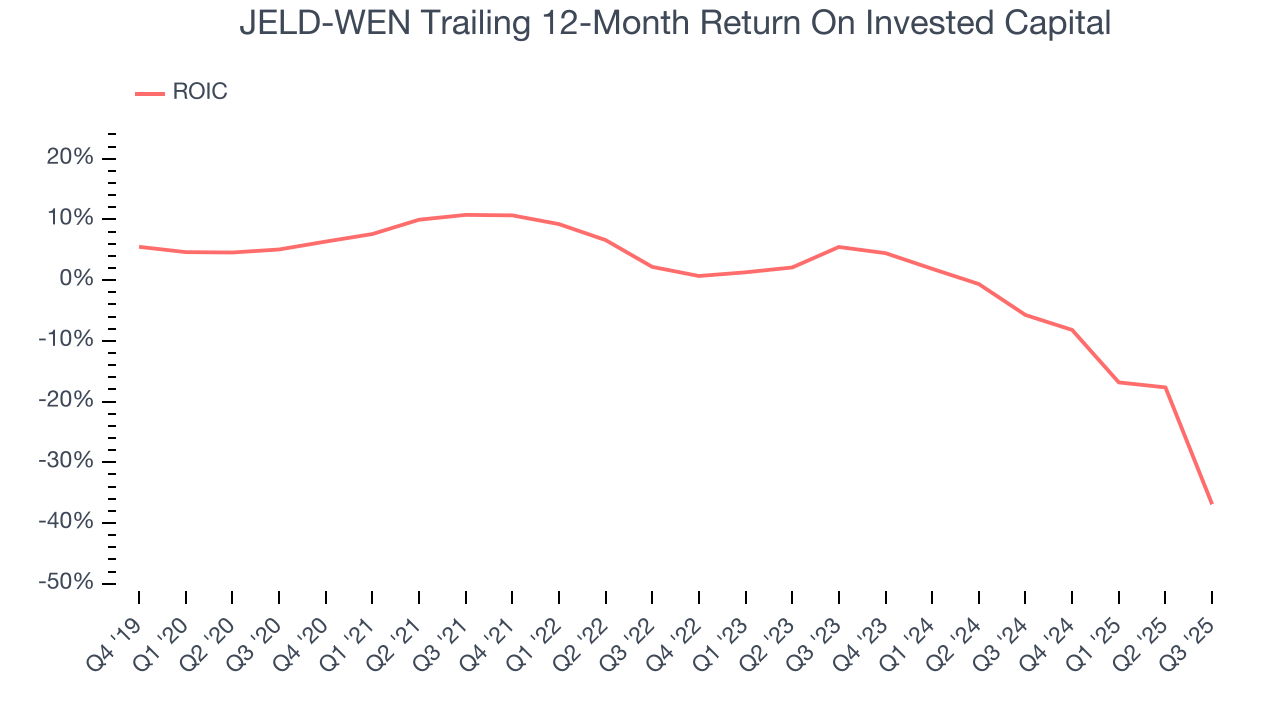

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

JELD-WEN’s five-year average ROIC was negative 4.8%, meaning management lost money while trying to expand the business. Its returns were among the worst in the industrials sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, JELD-WEN’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

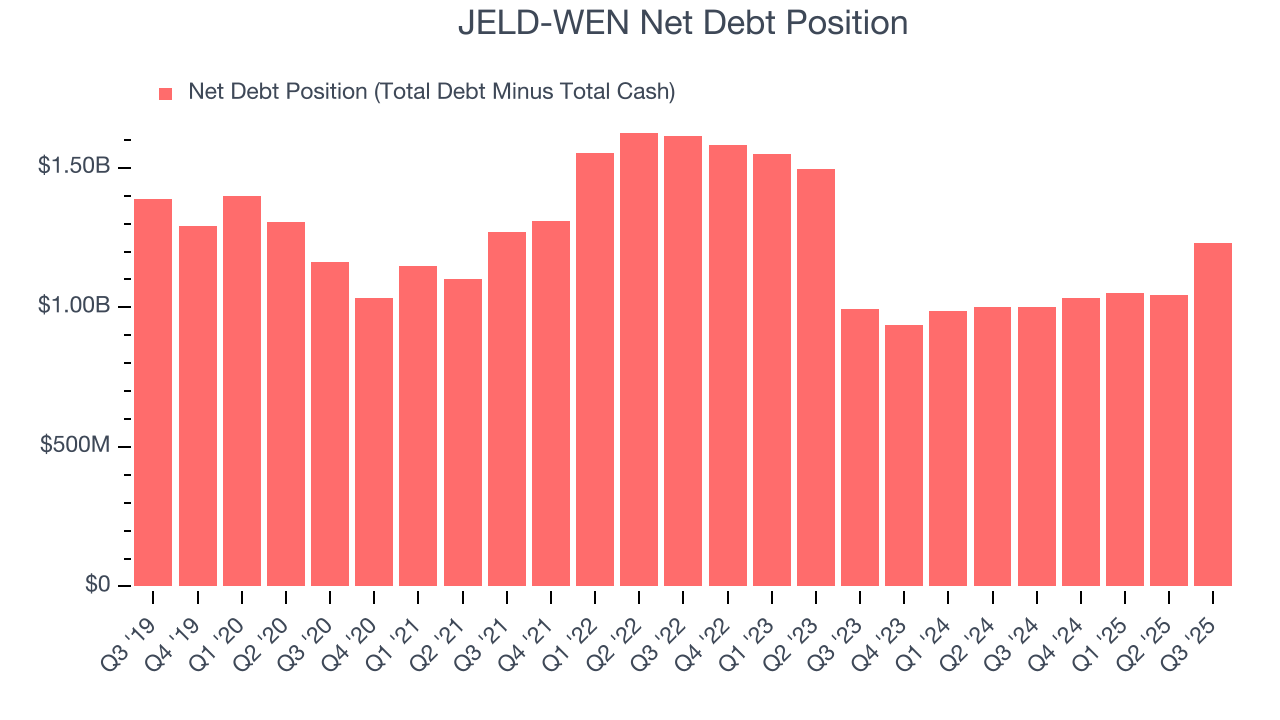

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

JELD-WEN burned through $165.7 million of cash over the last year, and its $1.34 billion of debt exceeds the $108.4 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the JELD-WEN’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of JELD-WEN until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

12. Key Takeaways from JELD-WEN’s Q3 Results

This was a bad quarter, with revenue and EBITDA missing expectations. Full-year revenue guidance was lowered and EBITDA guidance came in below Wall Street's estimates. Overall, this was a very weak quarter. The stock traded down 12.7% to $3.65 immediately following the results.

13. Is Now The Time To Buy JELD-WEN?

Updated: January 24, 2026 at 10:35 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in JELD-WEN.

We cheer for all companies making their customers lives easier, but in the case of JELD-WEN, we’ll be cheering from the sidelines. First off, its revenue has declined over the last five years, and analysts expect its demand to deteriorate over the next 12 months. On top of that, JELD-WEN’s diminishing returns show management's prior bets haven't worked out, and its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

JELD-WEN’s EV-to-EBITDA ratio based on the next 12 months is 11.3x. This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $2.70 on the company (compared to the current share price of $3.03), implying they don’t see much short-term potential in JELD-WEN.