Amphastar Pharmaceuticals (AMPH)

We’re cautious of Amphastar Pharmaceuticals. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Amphastar Pharmaceuticals Will Underperform

Founded in 1996 and known for its expertise in complex drug formulations, Amphastar Pharmaceuticals (NASDAQ:AMPH) develops and manufactures technically challenging injectable and inhalation medications, including both generic and proprietary pharmaceutical products.

- Smaller revenue base of $719.9 million means it hasn’t achieved the economies of scale that some industry juggernauts enjoy

- The good news is that its earnings growth has outpaced its peers over the last five years as its EPS has compounded at 38.4% annually

Amphastar Pharmaceuticals’s quality doesn’t meet our expectations. We’re hunting for superior stocks elsewhere.

Why There Are Better Opportunities Than Amphastar Pharmaceuticals

Amphastar Pharmaceuticals’s stock price of $19.52 implies a valuation ratio of 5.9x forward P/E. Amphastar Pharmaceuticals’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Amphastar Pharmaceuticals (AMPH) Research Report: Q4 CY2025 Update

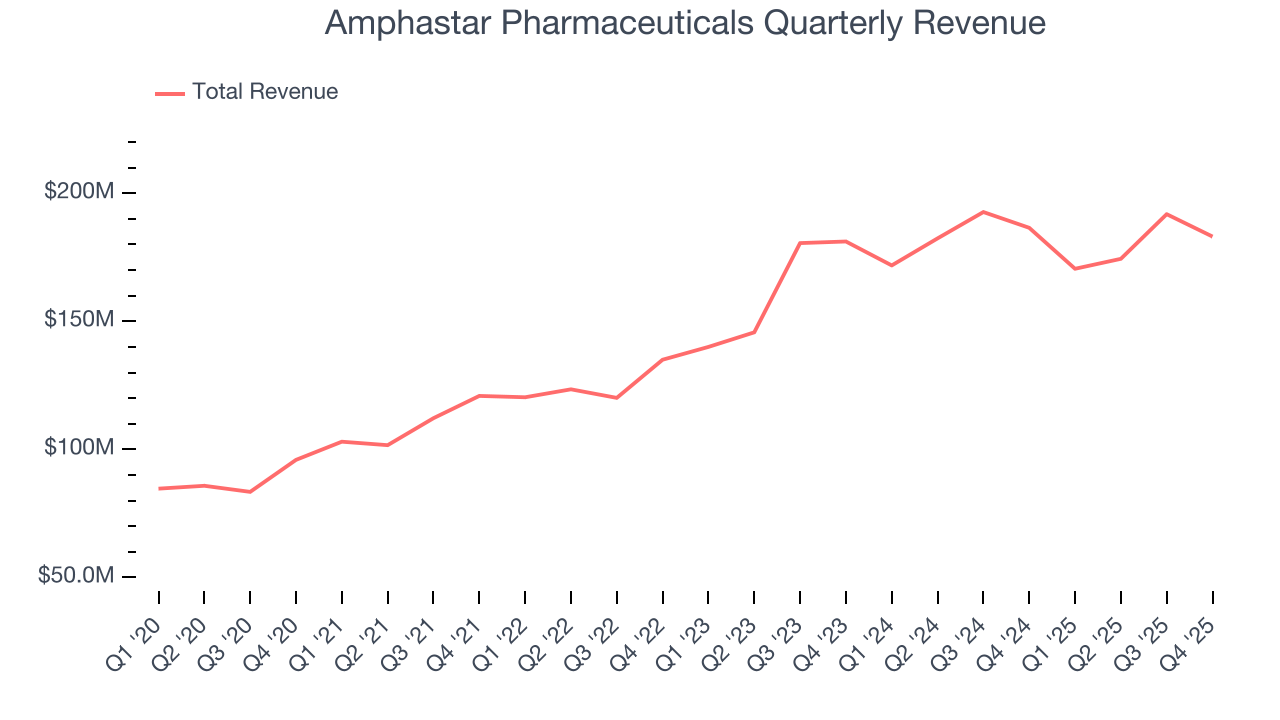

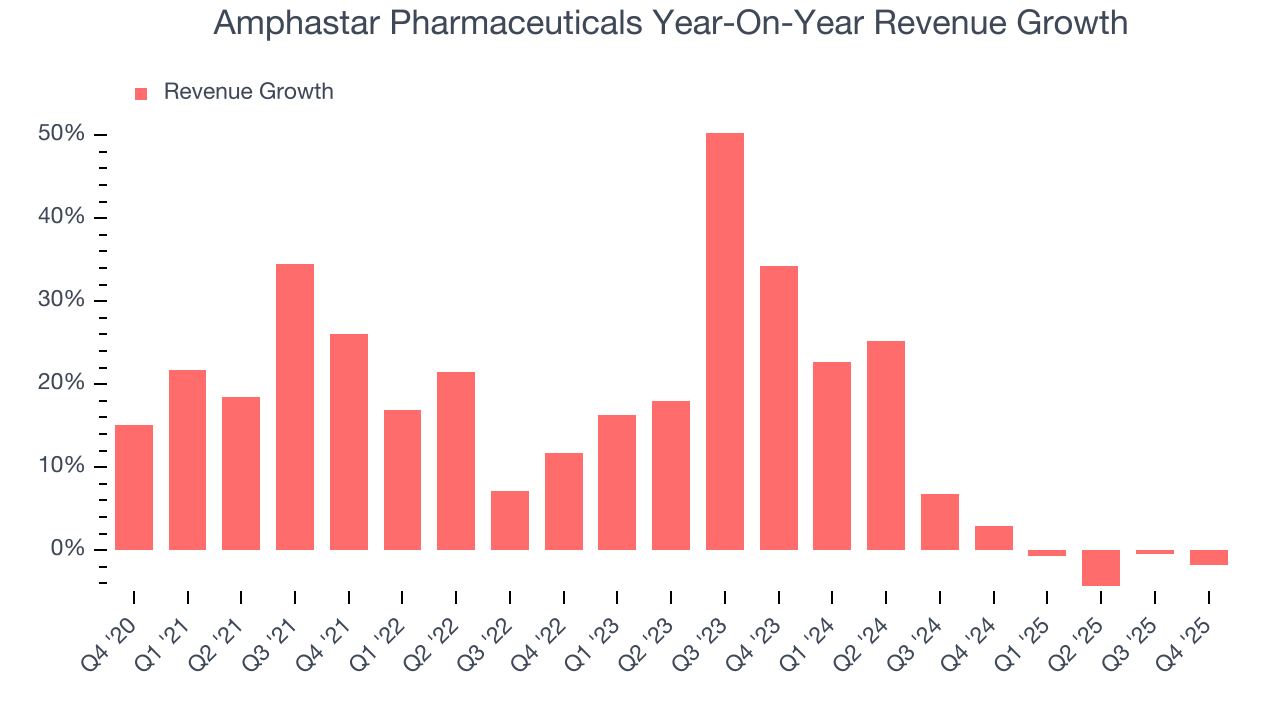

Pharmaceutical company Amphastar Pharmaceuticals (NASDAQAMPH) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 1.8% year on year to $183.1 million. Its non-GAAP profit of $0.73 per share was 20.5% below analysts’ consensus estimates.

Amphastar Pharmaceuticals (AMPH) Q4 CY2025 Highlights:

- Revenue: $183.1 million vs analyst estimates of $187.1 million (1.8% year-on-year decline, 2.2% miss)

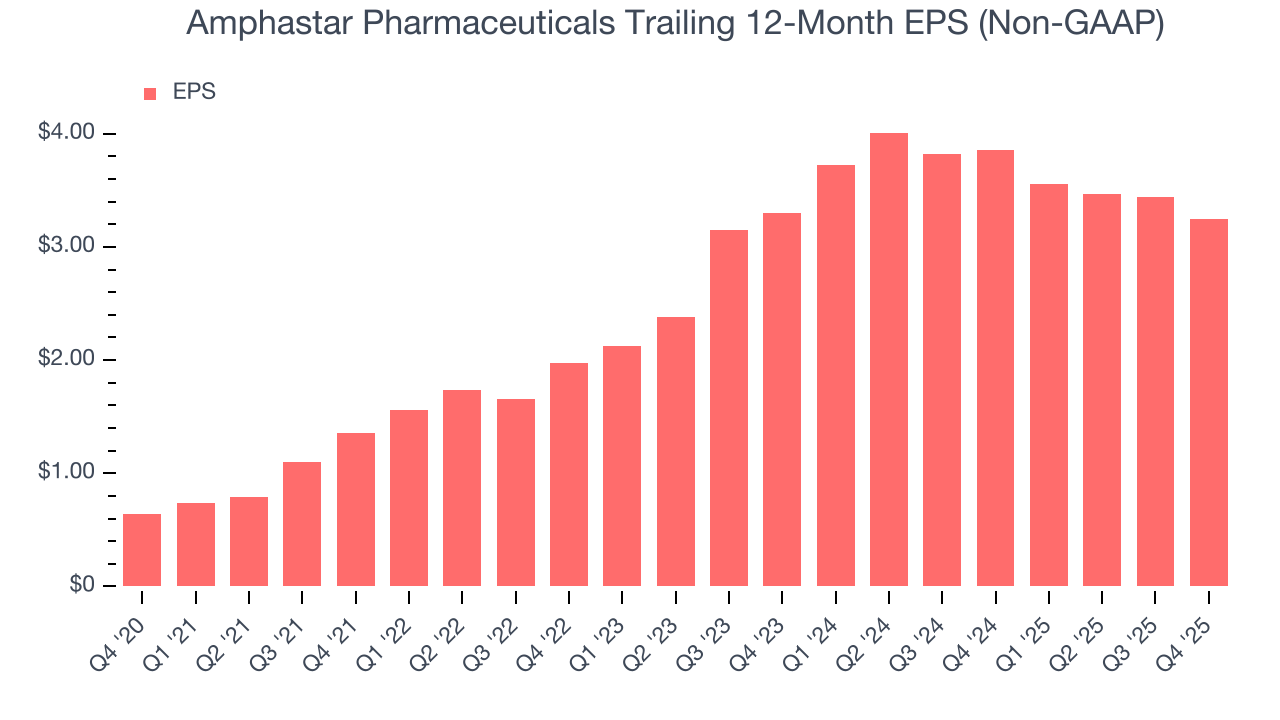

- Adjusted EPS: $0.73 vs analyst expectations of $0.92 (20.5% miss)

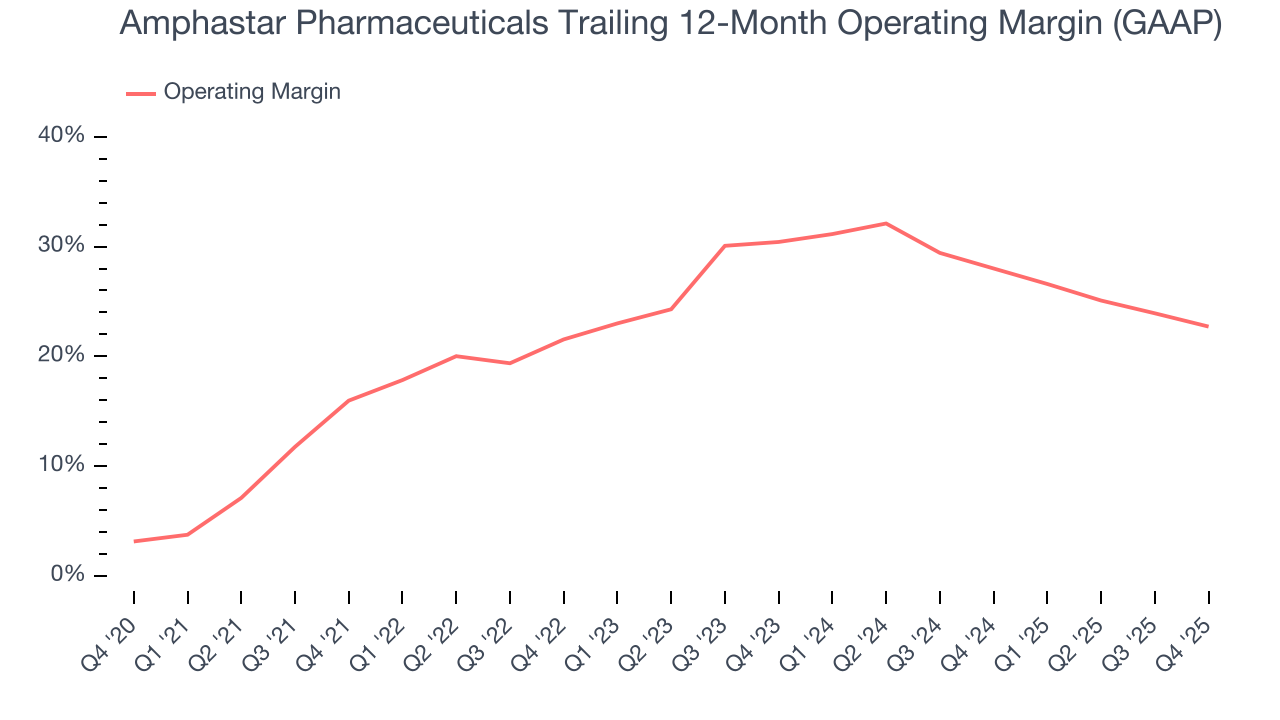

- Operating Margin: 19.4%, down from 24.2% in the same quarter last year

- Market Capitalization: $1.29 billion

Company Overview

Founded in 1996 and known for its expertise in complex drug formulations, Amphastar Pharmaceuticals (NASDAQ:AMPH) develops and manufactures technically challenging injectable and inhalation medications, including both generic and proprietary pharmaceutical products.

Amphastar specializes in products with high technical barriers to market entry, focusing on medications that require sophisticated manufacturing processes and rigorous quality controls. The company's portfolio includes over 25 products, with notable offerings such as BAQSIMI (a nasal glucagon powder for treating severe hypoglycemia), Primatene MIST (an over-the-counter asthma inhaler), and various injectable medications including epinephrine, glucagon, and naloxone.

What sets Amphastar apart is its vertically integrated structure and diverse technical capabilities. The company not only formulates and packages final drug products but also manufactures many of its own active pharmaceutical ingredients (APIs), including insulin. This vertical integration gives Amphastar greater control over its supply chain and quality standards while potentially improving margins.

Amphastar's technical expertise spans several challenging areas of pharmaceutical development. The company has developed capabilities in characterizing complex molecules, analyzing immunogenicity (how drugs trigger immune responses), engineering drug particles for optimal delivery, and creating sustained-release formulations. These specialized skills enable Amphastar to tackle difficult-to-manufacture products that many competitors cannot easily replicate.

For healthcare providers, Amphastar's products offer essential treatment options across multiple therapeutic areas. A hospital might stock Amphastar's prefilled epinephrine syringes for emergency anaphylaxis treatment, while an endocrinologist might prescribe BAQSIMI for diabetic patients at risk of severe hypoglycemia. Meanwhile, consumers with mild asthma can purchase Primatene MIST without a prescription at retail pharmacies.

The company markets its products primarily to hospitals, long-term care facilities, clinics, and retail pharmacies, working through major group purchasing organizations and specialty distributors. Amphastar is also developing a pipeline of over 20 product candidates, including generic, biosimilar, and proprietary medications, with a particular focus on interchangeable insulin products for diabetes care.

4. Generic Pharmaceuticals

The generic pharmaceutical industry operates on a volume-driven, low-cost business model, producing bioequivalent versions of branded drugs once their patents expire. These companies benefit from consistent demand for affordable medications, as they are critical to reducing healthcare costs. Generics typically face lower R&D expenses and shorter regulatory approval timelines compared to branded drug makers, enabling cost efficiencies. However, the industry is highly competitive, with intense pricing pressures, thin margins, and frequent legal challenges from branded pharmaceutical companies over patent disputes. Looking ahead, the industry is supported by tailwinds such as the role of AI in streamlining drug development (reverse engineering complex formulations) and manufacturing efficiency (optimize processes and remove inefficiencies). Governments and insurers' focus on reducing drug costs can also boost generics' adoption. However, headwinds include escalating pricing pressure from large buyers like pharmacy chains and healthcare distributors as well as evolving regulatory hurdles.

Amphastar faces competition from pharmaceutical companies specializing in injectable and inhalation markets, including Pfizer (NYSE:PFE), Teva Pharmaceutical Industries (NYSE:TEVA), Viatris (NASDAQ:VTRS), Sandoz (NYSE:SDZ), Fresenius Kabi, and Hikma Pharmaceuticals (OTC:HKMPY). In the diabetes care space, particularly for insulin products, Amphastar competes with Novo Nordisk (NYSE:NVO) and Eli Lilly (NYSE:LLY).

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $719.9 million in revenue over the past 12 months, Amphastar Pharmaceuticals is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Amphastar Pharmaceuticals’s 15.5% annualized revenue growth over the last five years was solid. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Amphastar Pharmaceuticals’s recent performance shows its demand has slowed as its annualized revenue growth of 5.4% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Amphastar Pharmaceuticals missed Wall Street’s estimates and reported a rather uninspiring 1.8% year-on-year revenue decline, generating $183.1 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 11.2% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and implies its newer products and services will catalyze better top-line performance.

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Amphastar Pharmaceuticals has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 24.5%.

Analyzing the trend in its profitability, Amphastar Pharmaceuticals’s operating margin rose by 6.7 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming into its more recent performance, however, we can see the company’s margin has decreased by 7.7 percentage points on a two-year basis. If Amphastar Pharmaceuticals wants to pass our bar, it must prove it can expand its profitability consistently.

In Q4, Amphastar Pharmaceuticals generated an operating margin profit margin of 19.4%, down 4.8 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Amphastar Pharmaceuticals’s EPS grew at an astounding 38.4% compounded annual growth rate over the last five years, higher than its 15.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Amphastar Pharmaceuticals’s earnings to better understand the drivers of its performance. As we mentioned earlier, Amphastar Pharmaceuticals’s operating margin declined this quarter but expanded by 6.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Amphastar Pharmaceuticals reported adjusted EPS of $0.73, down from $0.92 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Amphastar Pharmaceuticals’s full-year EPS of $3.25 to grow 8.8%.

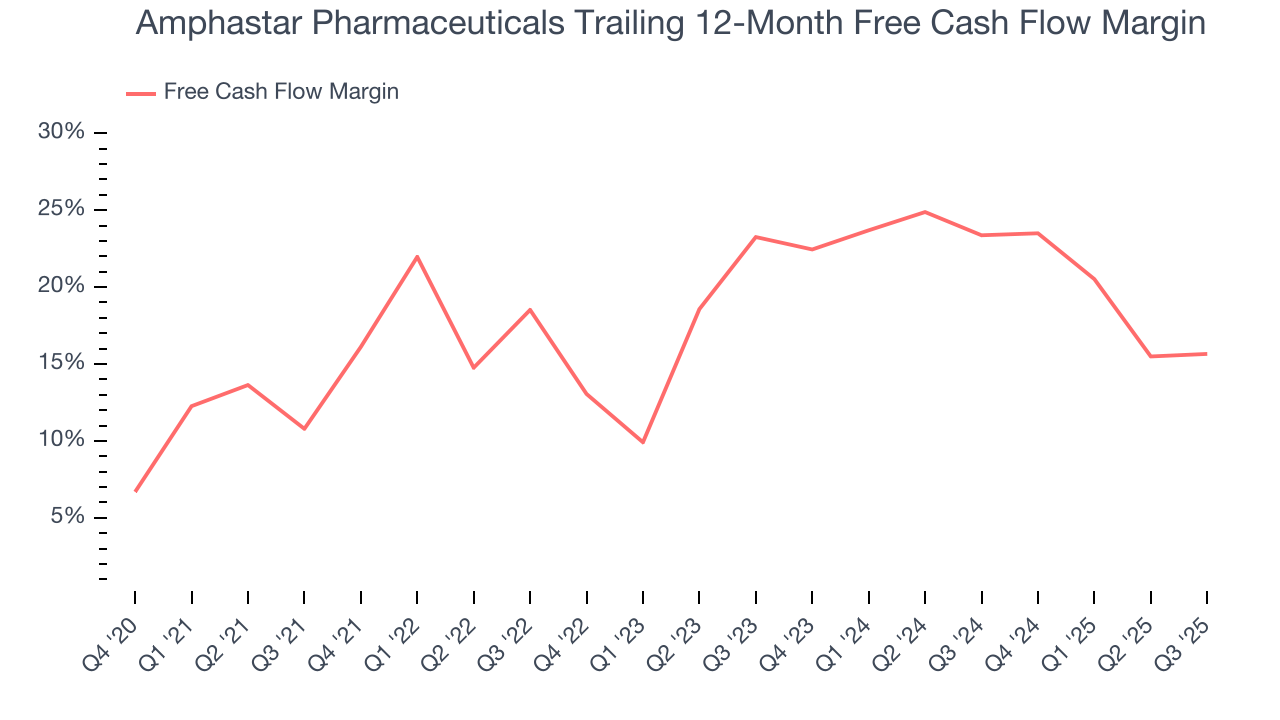

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Amphastar Pharmaceuticals has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 19.3% over the last five years, quite impressive for a healthcare business.

Taking a step back, we can see that Amphastar Pharmaceuticals’s margin expanded by 6.3 percentage points during that time. This is encouraging because it gives the company more optionality.

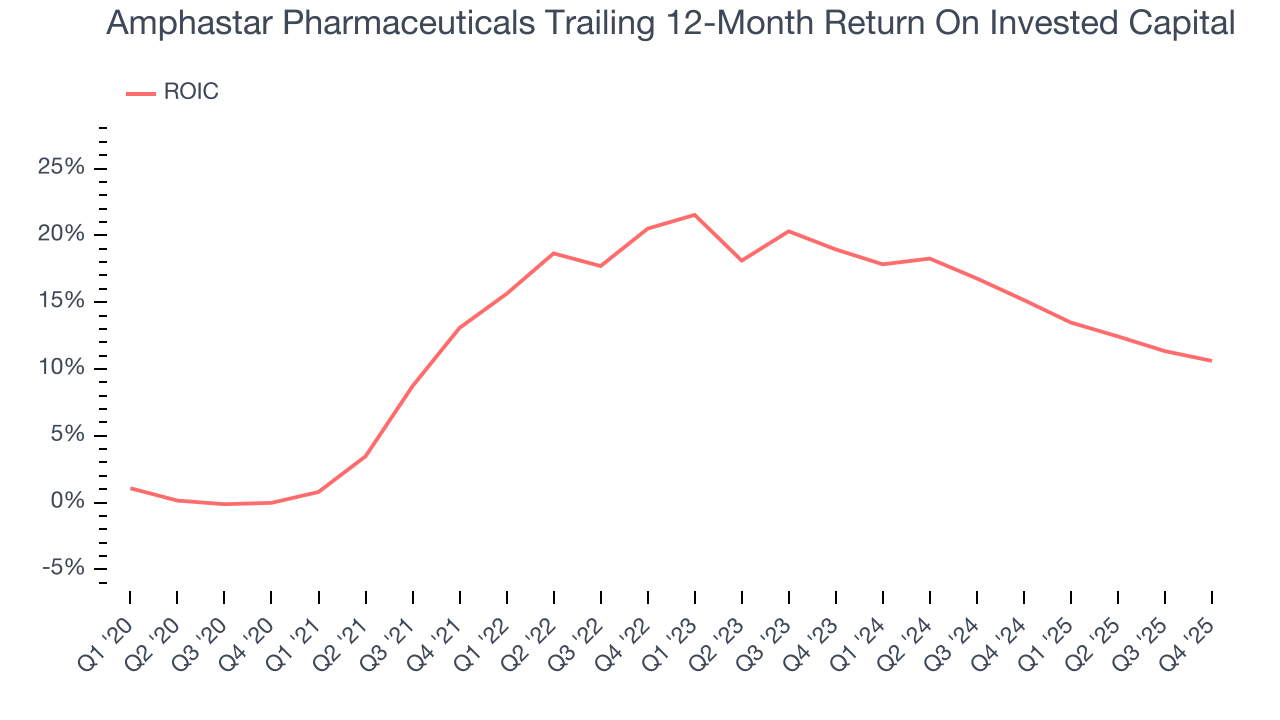

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Amphastar Pharmaceuticals hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked out well. Its five-year average ROIC was 15.7%, impressive for a healthcare business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Amphastar Pharmaceuticals’s ROIC decreased by 3.9 percentage points annually each year over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

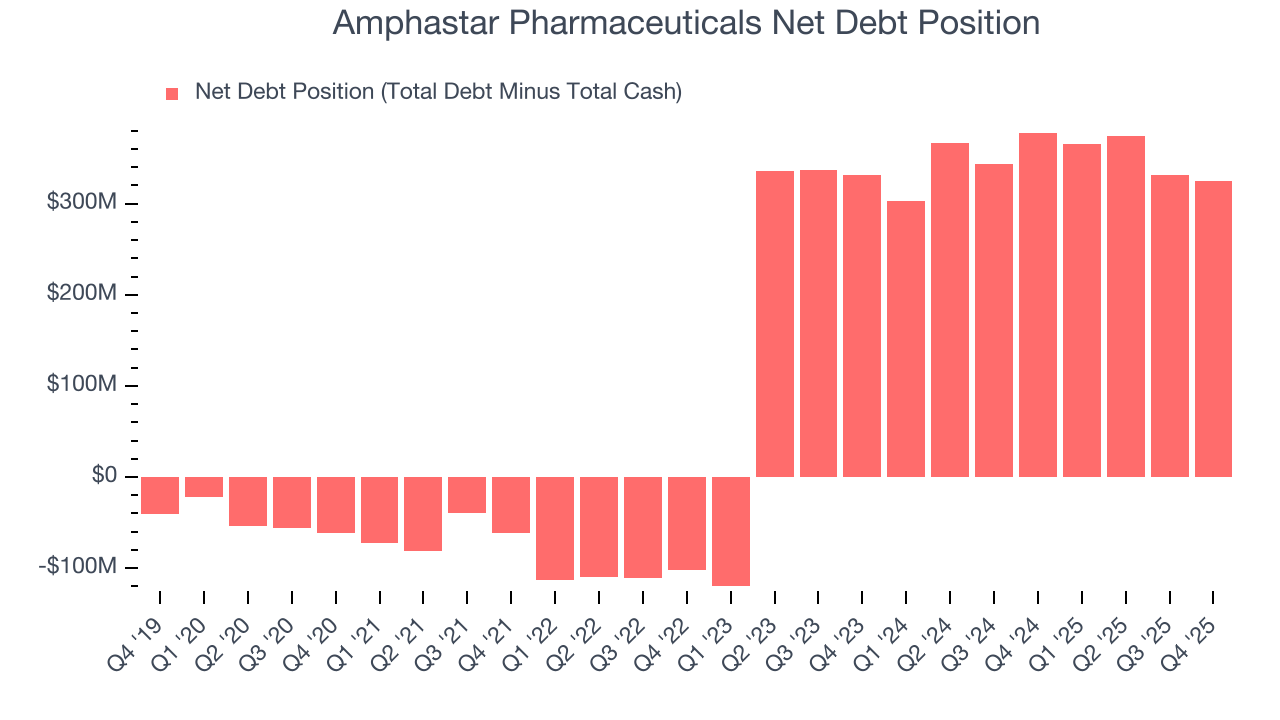

11. Balance Sheet Assessment

Amphastar Pharmaceuticals reported $285 million of cash and $610.4 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $247.5 million of EBITDA over the last 12 months, we view Amphastar Pharmaceuticals’s 1.3× net-debt-to-EBITDA ratio as safe. We also see its $13.4 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Amphastar Pharmaceuticals’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 11.7% to $23.38 immediately after reporting.

13. Is Now The Time To Buy Amphastar Pharmaceuticals?

Updated: March 22, 2026 at 12:17 AM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Amphastar Pharmaceuticals isn’t a terrible business, but it doesn’t pass our quality test. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its subscale operations give it fewer distribution channels than its larger rivals. And while the company’s astounding EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its diminishing returns show management's prior bets haven't worked out.

Amphastar Pharmaceuticals’s P/E ratio based on the next 12 months is 5.9x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $29 on the company (compared to the current share price of $19.52).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.