Collegium Pharmaceutical (COLL)

We’re not sold on Collegium Pharmaceutical. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why Collegium Pharmaceutical Is Not Exciting

Pioneering abuse-deterrent technology in a field plagued by addiction concerns, Collegium Pharmaceutical (NASDAQ:COLL) develops and markets specialty medications for treating moderate to severe pain, including abuse-deterrent opioid formulations.

- Subscale operations are evident in its revenue base of $780.6 million, meaning it has fewer distribution channels than its larger rivals

- Estimated sales growth of 3.9% for the next 12 months implies demand will slow from its two-year trend

- A consolation is that its excellent adjusted operating margin highlights the strength of its business model

Collegium Pharmaceutical is in the doghouse. We’ve identified better opportunities elsewhere.

Why There Are Better Opportunities Than Collegium Pharmaceutical

At $34.53 per share, Collegium Pharmaceutical trades at 4.7x forward P/E. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Collegium Pharmaceutical (COLL) Research Report: Q4 CY2025 Update

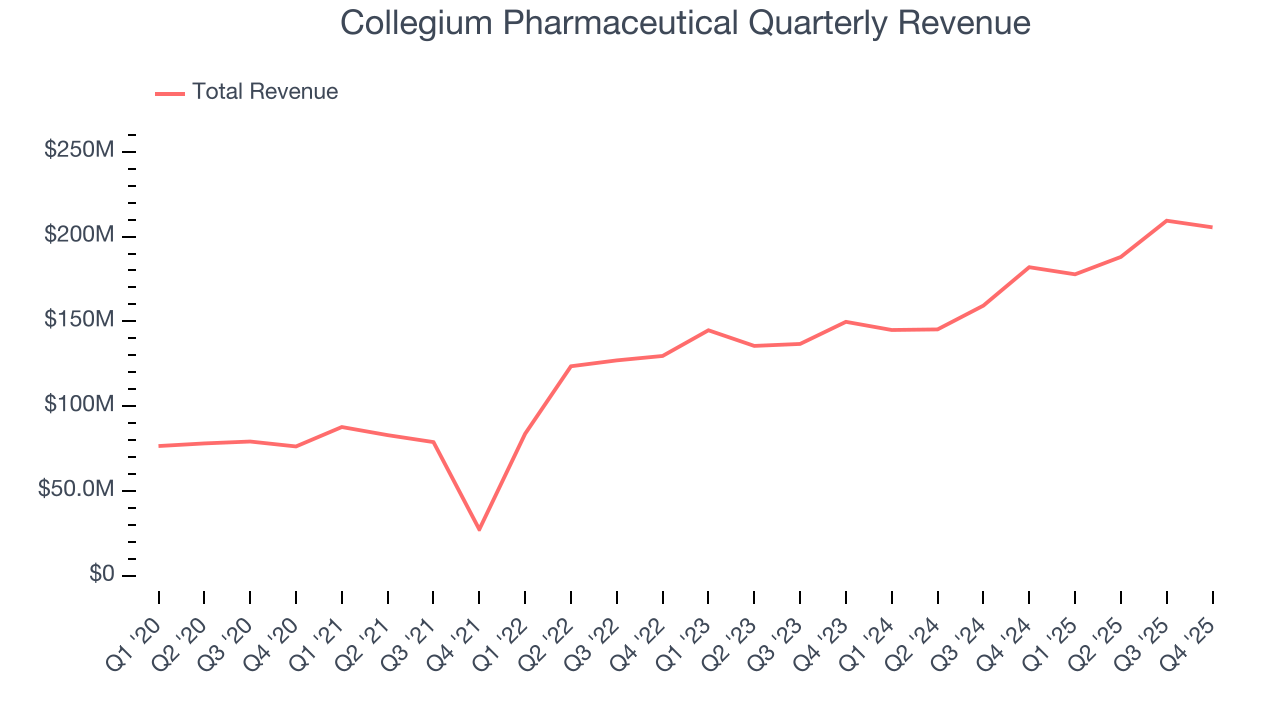

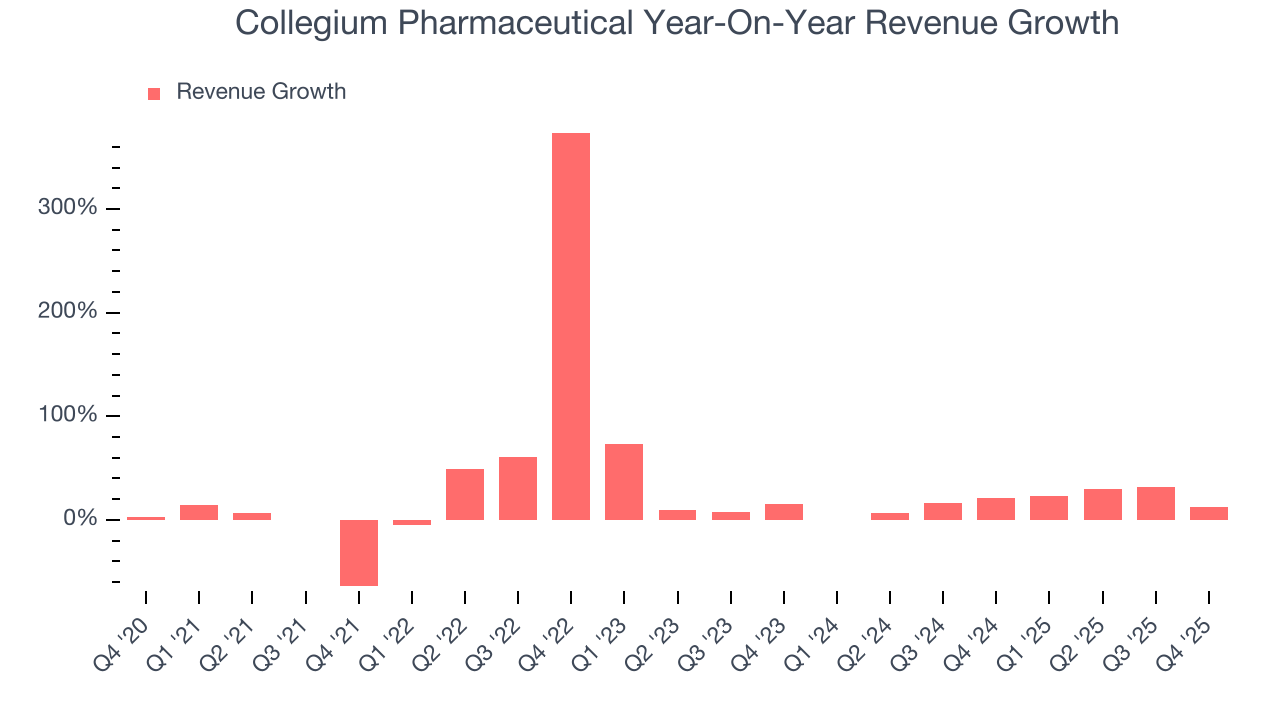

Pharmaceutical company Collegium Pharmaceutical (NASDAQ:COLL) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 12.9% year on year to $205.4 million. The company’s full-year revenue guidance of $815 million at the midpoint came in 1% above analysts’ estimates. Its non-GAAP profit of $2.04 per share was 4.7% below analysts’ consensus estimates.

Collegium Pharmaceutical (COLL) Q4 CY2025 Highlights:

- Revenue: $205.4 million vs analyst estimates of $206.4 million (12.9% year-on-year growth, in line)

- Adjusted EPS: $2.04 vs analyst expectations of $2.14 (4.7% miss)

- Adjusted EBITDA: $127.3 million vs analyst estimates of $126.2 million (62% margin, 0.9% beat)

- EBITDA guidance for the upcoming financial year 2026 is $465 million at the midpoint, above analyst estimates of $451.1 million

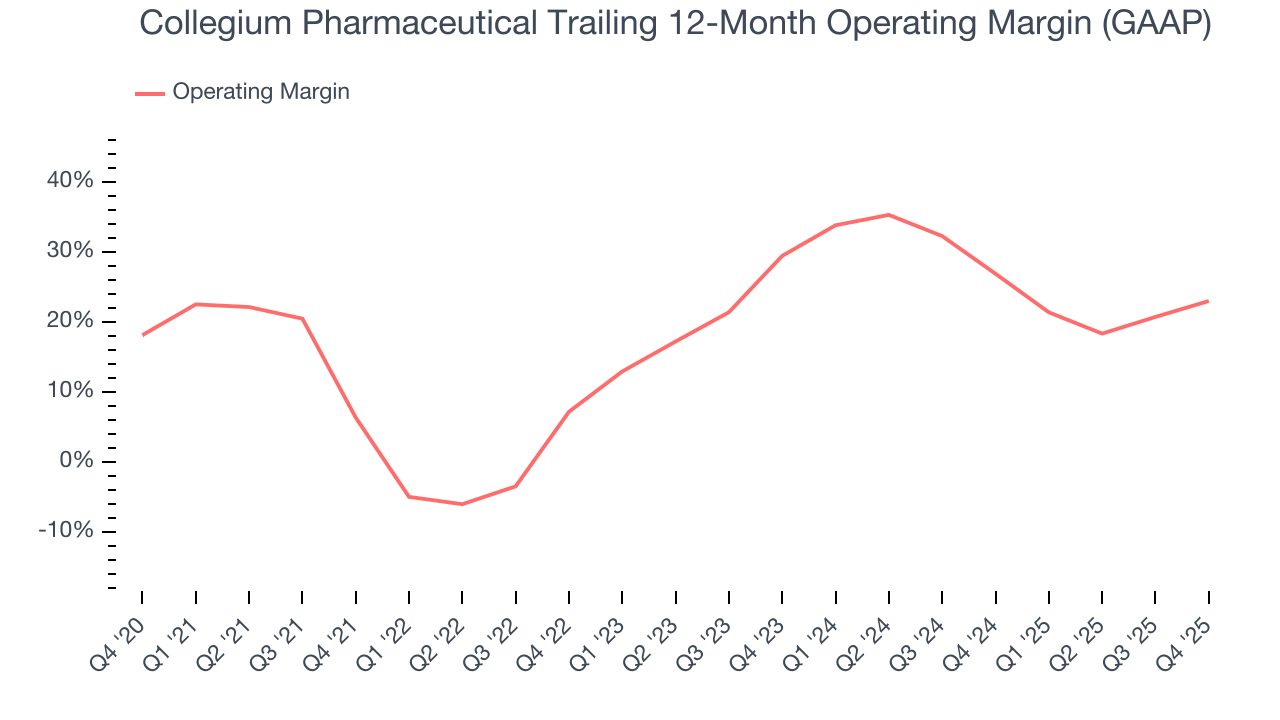

- Operating Margin: 29.6%, up from 20.9% in the same quarter last year

- Market Capitalization: $1.45 billion

Company Overview

Pioneering abuse-deterrent technology in a field plagued by addiction concerns, Collegium Pharmaceutical (NASDAQ:COLL) develops and markets specialty medications for treating moderate to severe pain, including abuse-deterrent opioid formulations.

Collegium's portfolio includes several pain management products with distinct properties. Its flagship product, Xtampza ER, uses the company's proprietary DETERx technology platform to create an extended-release oxycodone formulation designed to maintain its properties even when physically manipulated, addressing a key vulnerability of traditional opioid medications. The technology embeds oxycodone in wax-based microspheres that resist crushing, chewing, and other common methods of abuse.

The company also markets the Nucynta product line (tapentadol in extended and immediate-release formulations), Belbuca (a buccal film containing buprenorphine), and Symproic (for opioid-induced constipation). These medications serve patients with severe persistent pain requiring daily opioid treatment for whom alternative treatments have proven inadequate.

Physicians prescribe Collegium's products to patients suffering from conditions causing significant, ongoing pain that impacts daily functioning. For example, a patient with diabetic peripheral neuropathy might use Nucynta ER to manage the persistent burning pain in their feet that hasn't responded to non-opioid treatments.

Collegium generates revenue by selling its products to pharmaceutical wholesalers who distribute them to pharmacies, hospitals, and other healthcare facilities. The company employs a specialized sales force targeting healthcare professionals who frequently prescribe extended-release opioids.

The company operates in a highly regulated environment, with most of its products classified as controlled substances under the Controlled Substances Act. Xtampza ER and Nucynta are Schedule II substances (high potential for abuse), while Belbuca is Schedule III (moderate to low potential for abuse).

4. Branded Pharmaceuticals

Looking ahead, the branded pharmaceutical industry is positioned for tailwinds from advancements in precision medicine, increasing adoption of AI to enhance drug development efficiency, and growing global demand for treatments addressing chronic and rare diseases. However, headwinds include heightened regulatory scrutiny, pricing pressures from governments and insurers, and the looming patent cliffs for key blockbuster drugs. Patent cliffs bring about competition from generics, forcing branded pharmaceutical companies back to the drawing board to find the next big thing.

Collegium Pharmaceutical's competitors include Purdue Pharma (maker of OxyContin), Teva Pharmaceutical Industries (NYSE:TEVA), Endo International (OTC:ENDPQ), and other pharmaceutical companies that manufacture pain medications, particularly those with abuse-deterrent formulations.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $780.6 million in revenue over the past 12 months, Collegium Pharmaceutical is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Collegium Pharmaceutical’s 20.3% annualized revenue growth over the last five years was impressive. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Collegium Pharmaceutical’s annualized revenue growth of 17.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Collegium Pharmaceutical’s year-on-year revenue growth was 12.9%, and its $205.4 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 2.8% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges.

7. Operating Margin

Collegium Pharmaceutical has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 20.9%.

Analyzing the trend in its profitability, Collegium Pharmaceutical’s operating margin rose by 16.6 percentage points over the last five years, as its sales growth gave it immense operating leverage. Zooming into its more recent performance, however, we can see the company’s margin has decreased by 6.4 percentage points on a two-year basis. If Collegium Pharmaceutical wants to pass our bar, it must prove it can expand its profitability consistently.

This quarter, Collegium Pharmaceutical generated an operating margin profit margin of 29.6%, up 8.6 percentage points year on year. This increase was a welcome development and shows it was more efficient.

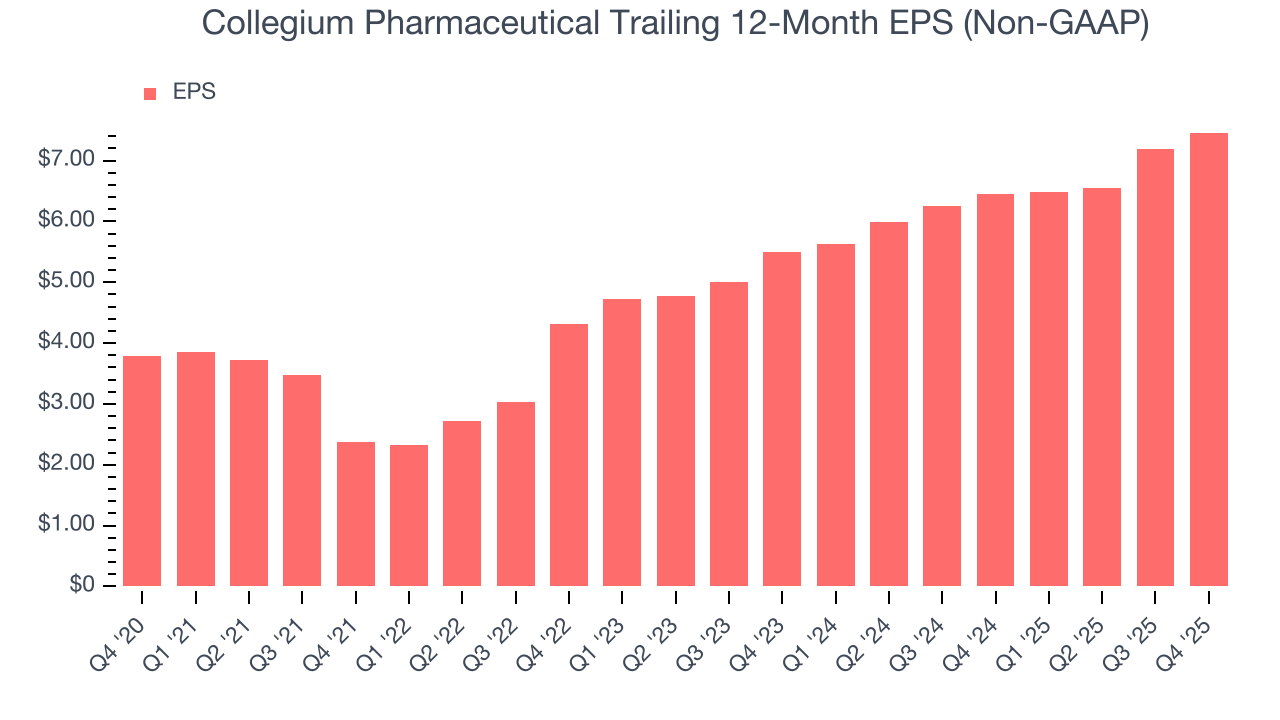

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Collegium Pharmaceutical’s EPS grew at a spectacular 14.5% compounded annual growth rate over the last five years. Despite its operating margin improvement during that time, this performance was lower than its 20.3% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

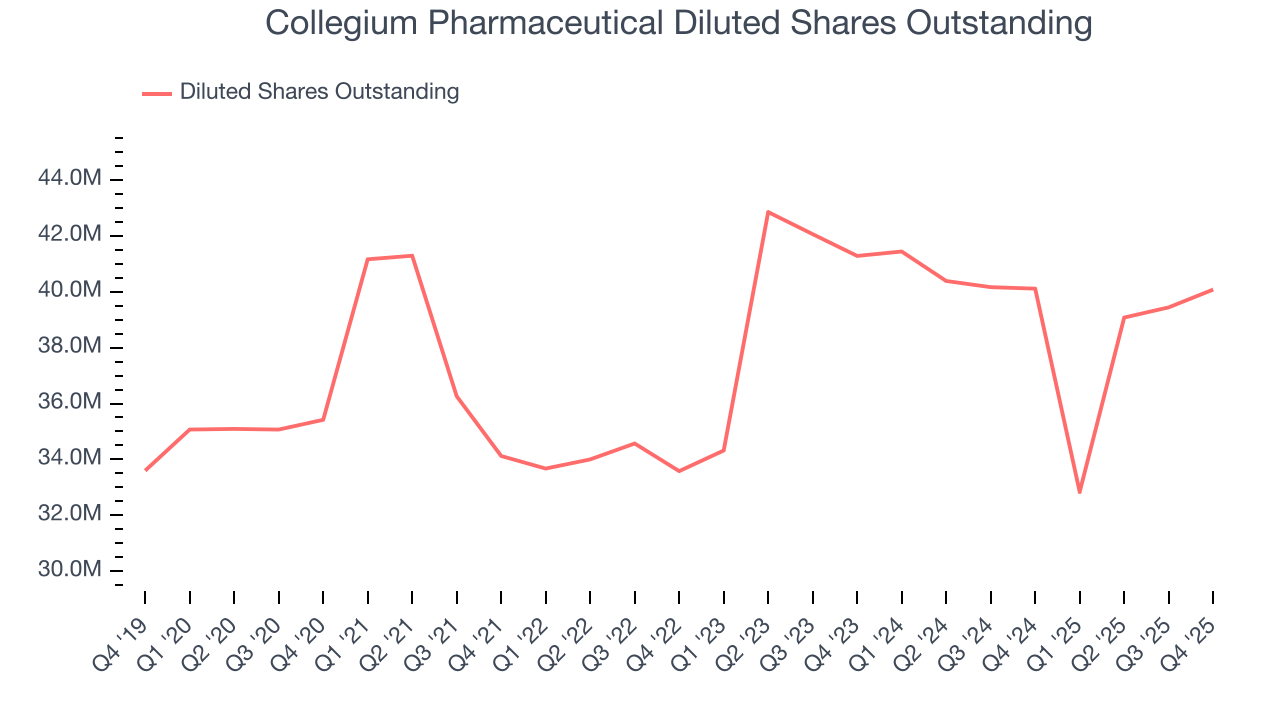

We can take a deeper look into Collegium Pharmaceutical’s earnings to better understand the drivers of its performance. A five-year view shows Collegium Pharmaceutical has diluted its shareholders, growing its share count by 13.2%. This dilution overshadowed its increased operational efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Collegium Pharmaceutical reported adjusted EPS of $2.04, up from $1.77 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Collegium Pharmaceutical’s full-year EPS of $7.46 to stay about the same.

9. Cash Is King

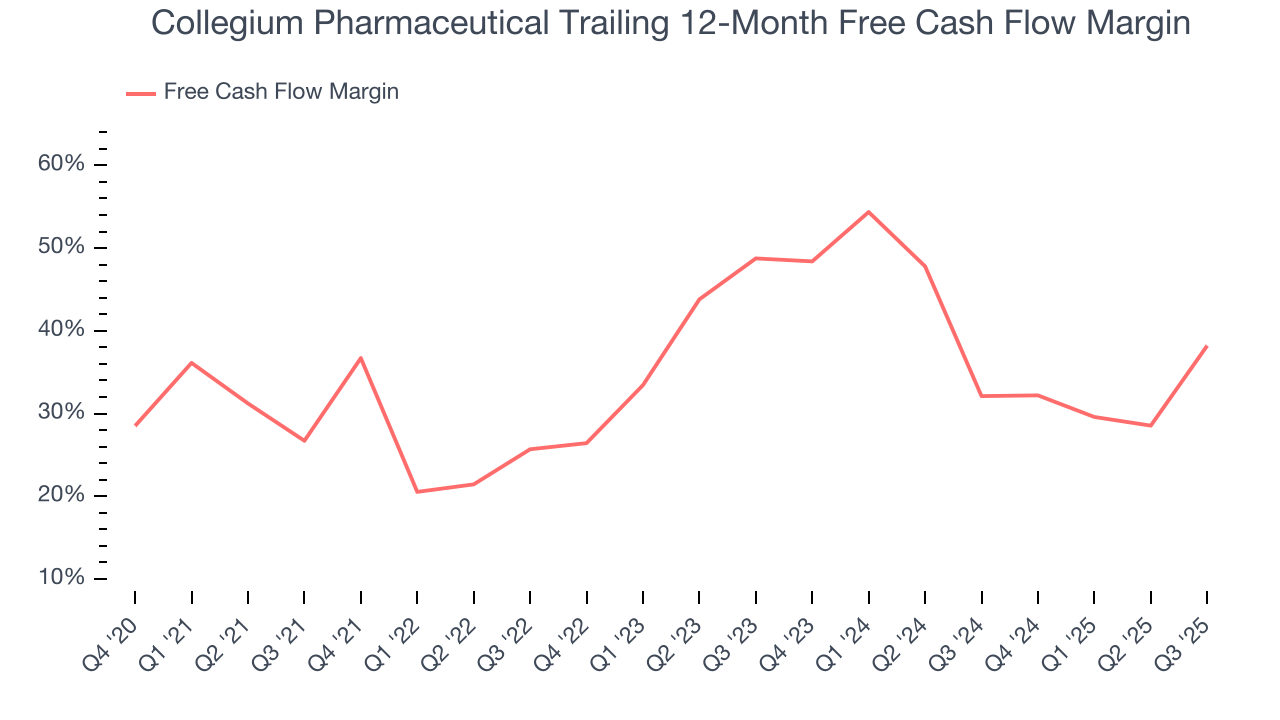

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Collegium Pharmaceutical has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the healthcare sector, averaging an eye-popping 36.1% over the last five years.

Taking a step back, we can see that Collegium Pharmaceutical’s margin expanded by 9.3 percentage points during that time. This is encouraging because it gives the company more optionality.

10. Return on Invested Capital (ROIC)

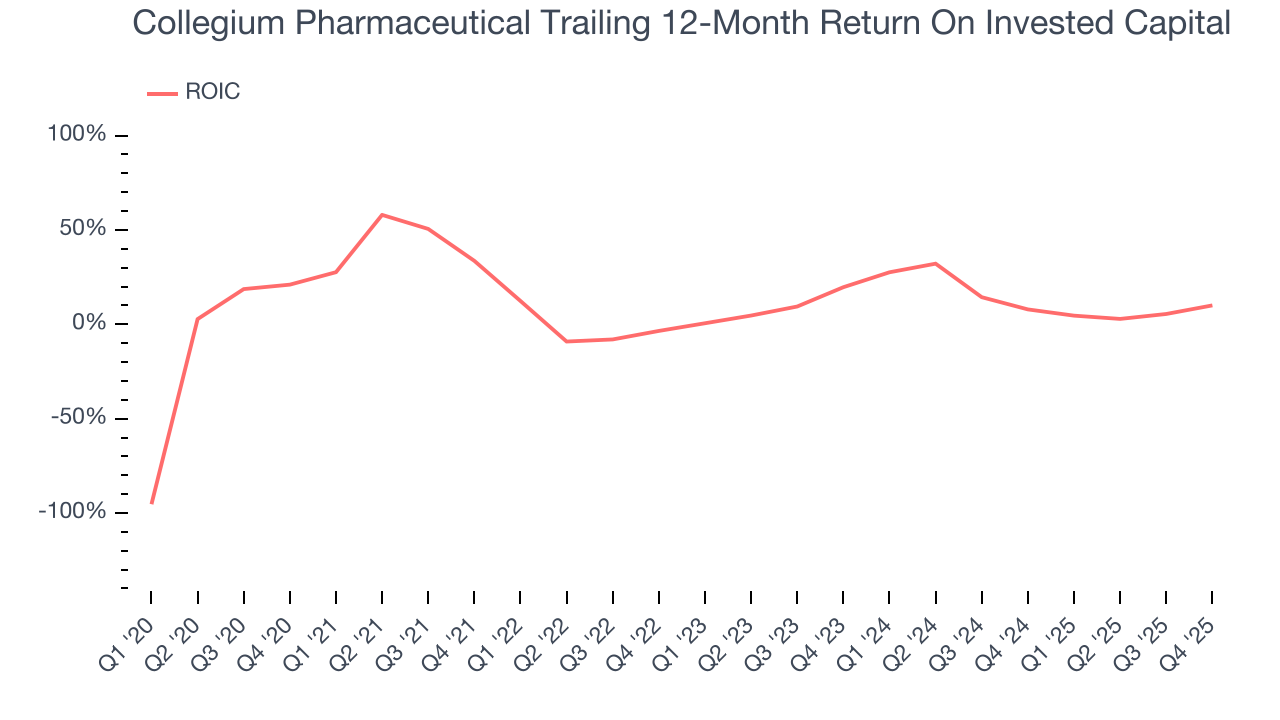

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Collegium Pharmaceutical hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked. Its five-year average ROIC was 13.5%, higher than most healthcare businesses.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Collegium Pharmaceutical’s ROIC has decreased over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

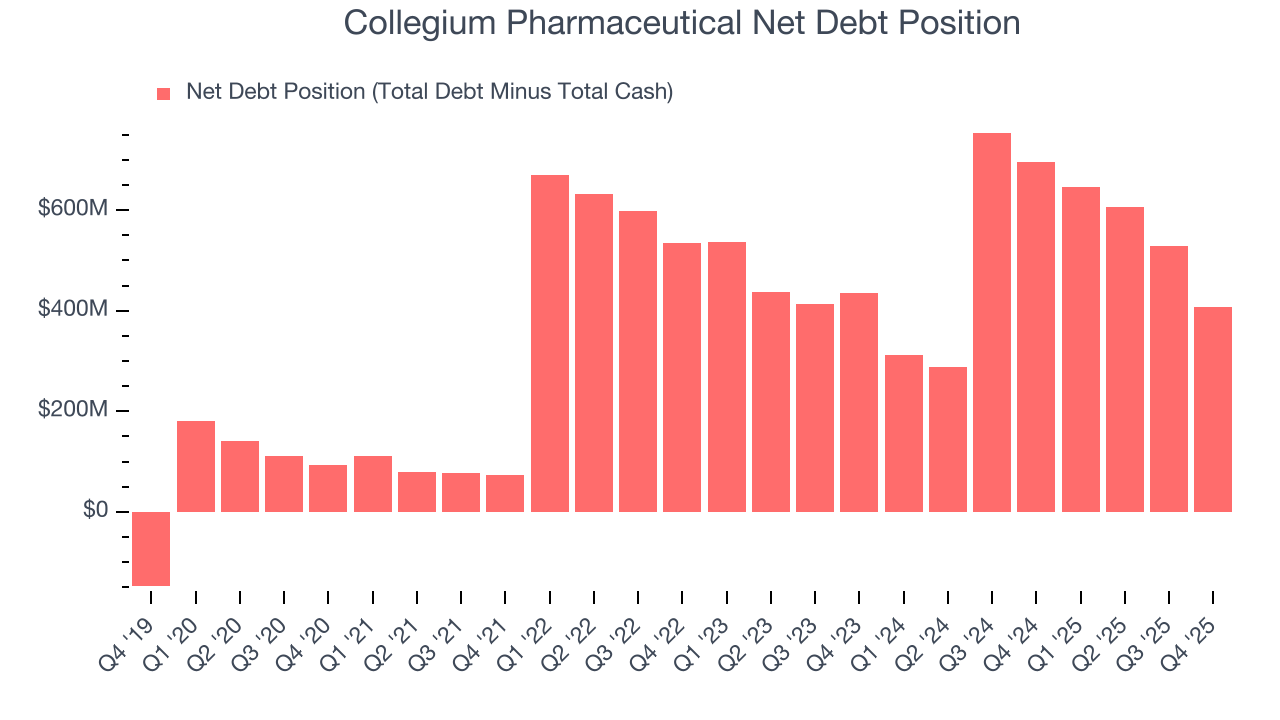

Collegium Pharmaceutical reported $407.6 million of cash and $814.9 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $460.5 million of EBITDA over the last 12 months, we view Collegium Pharmaceutical’s 0.9× net-debt-to-EBITDA ratio as safe. We also see its $39.57 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Collegium Pharmaceutical’s Q4 Results

It was good to see Collegium Pharmaceutical provide full-year revenue guidance that slightly beat analysts’ expectations. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its EPS missed and its revenue was in line with Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 3% to $44.37 immediately after reporting.

13. Is Now The Time To Buy Collegium Pharmaceutical?

Updated: March 16, 2026 at 12:22 AM EDT

Before investing in or passing on Collegium Pharmaceutical, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

There are some bright spots in Collegium Pharmaceutical’s fundamentals, but its business quality ultimately falls short. First off, its revenue growth was impressive over the last five years. And while Collegium Pharmaceutical’s subscale operations give it fewer distribution channels than its larger rivals, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits.

Collegium Pharmaceutical’s P/E ratio based on the next 12 months is 4.7x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $53.83 on the company (compared to the current share price of $34.53).