AppLovin (APP)

Not many stocks excite us like AppLovin. Its rare blend of high growth, robust profitability, and a strong outlook makes it a wonderful asset.― StockStory Analyst Team

1. News

2. Summary

Why We Like AppLovin

Sitting at the crossroads of the mobile advertising ecosystem with over 200 free-to-play games in its portfolio, AppLovin (NASDAQ:APP) provides software solutions that help mobile app developers market, monetize, and grow their apps through AI-powered advertising and analytics tools.

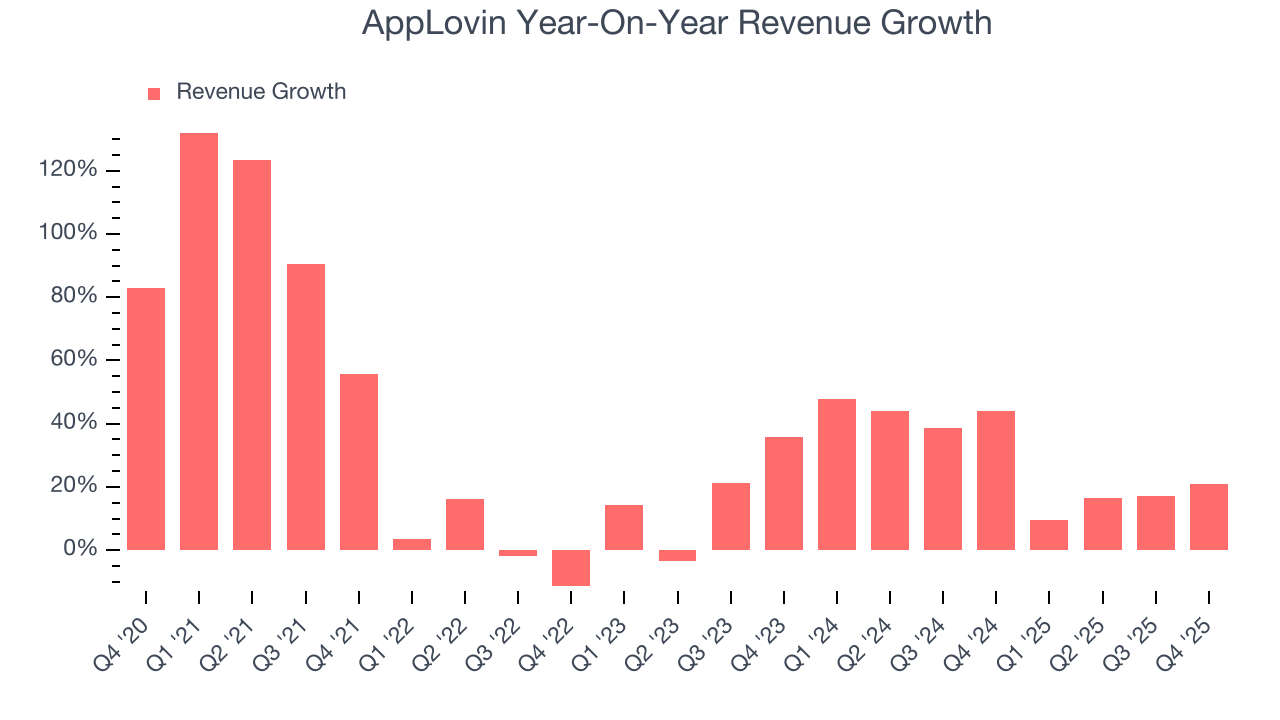

- Annual revenue growth of 29.2% over the last two years was superb and indicates its market share is rising

- Projected revenue growth of 46.7% for the next 12 months is above its two-year trend, pointing to accelerating demand

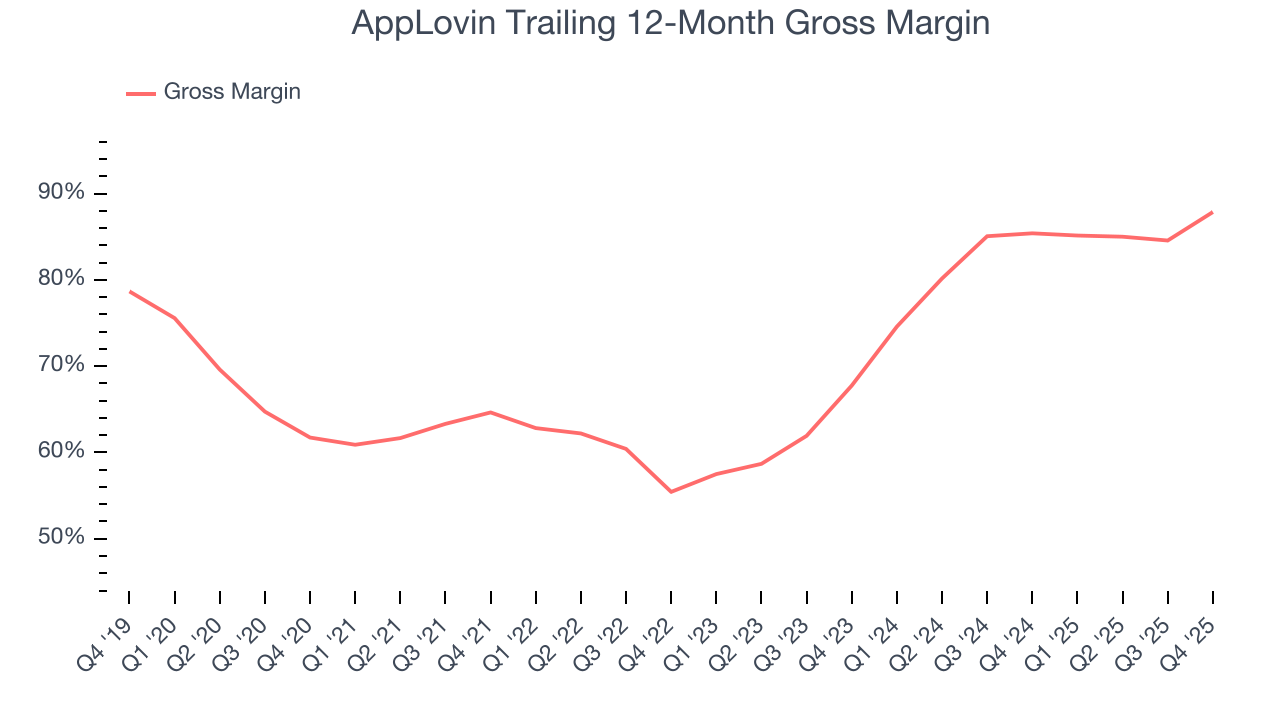

- Software is difficult to replicate at scale and results in a best-in-class gross margin of 87.9%

AppLovin is a standout company. The valuation seems reasonable based on its quality, and we believe now is the time to invest in the stock.

Why Is Now The Time To Buy AppLovin?

AppLovin’s stock price of $417.50 implies a valuation ratio of 16.6x forward price-to-sales. Yes, the stock’s seemingly high valuation multiple could mean short-term volatility. But given its business quality, we think the multiple is justified.

Our work shows, time and again, that buying high-quality companies and holding them routinely leads to market outperformance. Over a multi-year investment horizon, entry price doesn’t matter nearly as much as business quality.

3. AppLovin (APP) Research Report: Q4 CY2025 Update

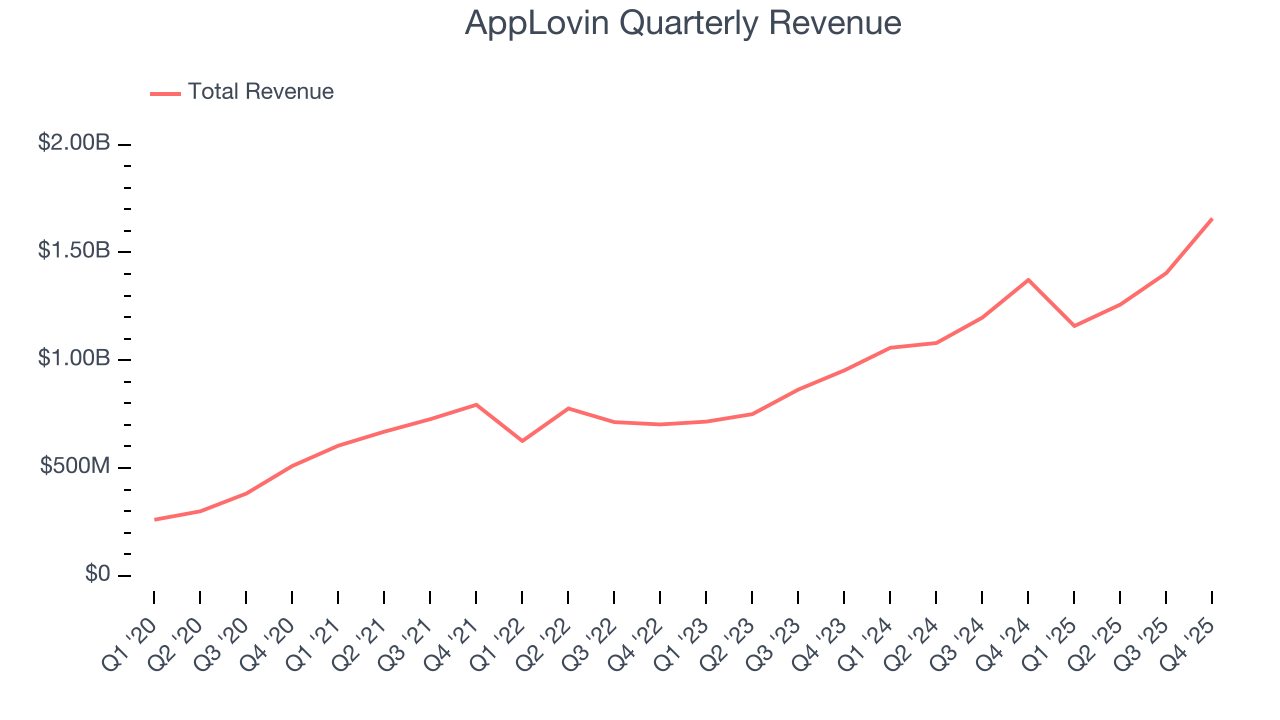

Mobile app technology company AppLovin (NASDAQ:APP) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 20.8% year on year to $1.66 billion. Guidance for next quarter’s revenue was optimistic at $1.76 billion at the midpoint, 3% above analysts’ estimates. Its GAAP profit of $3.24 per share was 10.1% above analysts’ consensus estimates.

AppLovin (APP) Q4 CY2025 Highlights:

- Revenue: $1.66 billion vs analyst estimates of $1.62 billion (20.8% year-on-year growth, 2.2% beat)

- EPS (GAAP): $3.24 vs analyst estimates of $2.94 (10.1% beat)

- Adjusted EBITDA: $1.40 billion vs analyst estimates of $1.33 billion (84.4% margin, 5.3% beat)

- Revenue Guidance for Q1 CY2026 is $1.76 billion at the midpoint, above analyst estimates of $1.71 billion

- EBITDA guidance for Q1 CY2026 is $1.48 billion at the midpoint, above analyst estimates of $1.39 billion

- Operating Margin: 76.9%, up from 44.3% in the same quarter last year

- Free Cash Flow Margin: 79%, up from 75% in the previous quarter

- Market Capitalization: $159.8 billion

Company Overview

Sitting at the crossroads of the mobile advertising ecosystem with over 200 free-to-play games in its portfolio, AppLovin (NASDAQ:APP) provides software solutions that help mobile app developers market, monetize, and grow their apps through AI-powered advertising and analytics tools.

AppLovin's business is built around two main segments: its Software Platform and Apps. The Software Platform includes four key products that work together to form a comprehensive ecosystem. AppDiscovery helps advertisers find the right users for their apps using AI-powered targeting. MAX is a monetization solution that runs real-time competitive auctions to maximize advertising revenue for publishers. Adjust provides measurement and analytics tools that help marketers track performance and optimize campaigns. Wurl extends AppLovin's reach into connected TV, distributing streaming content and providing advertising solutions in this growing market.

The company's Apps segment operates a diversified portfolio of free-to-play mobile games across various genres including casual, match-three, card/casino, and hyper-casual games. These games serve a dual purpose: generating direct revenue through in-app purchases and advertising, while also providing valuable user data that enhances the company's AI-powered advertising platform.

AppLovin's business model creates a virtuous cycle where data from its extensive app portfolio improves its advertising technology, which in turn attracts more advertisers seeking effective user acquisition. This scale enables AppLovin to offer highly targeted advertising that benefits both advertisers looking to reach relevant users and publishers seeking to maximize revenue from their advertising inventory.

4. Advertising Software

The digital advertising market is large, growing, and becoming more diverse, both in terms of audiences and media. As a result, there is a growing need for software that enables advertisers to use data to automate and optimize ad placements.

AppLovin competes with large technology companies that offer mobile advertising solutions including Meta (NASDAQ:META), Alphabet (NASDAQ:GOOG), and Unity Software (NYSE:U). In the mobile gaming space, its competitors include Activision Blizzard (NASDAQ:ATVI), Take-Two Interactive (NASDAQ:TTWO), and Tencent (OTC:TCEHY).

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, AppLovin’s 30.4% annualized revenue growth over the last five years was impressive. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. AppLovin’s annualized revenue growth of 29.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, AppLovin reported robust year-on-year revenue growth of 20.8%, and its $1.66 billion of revenue topped Wall Street estimates by 2.2%. Company management is currently guiding for a 51.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 43.1% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and suggests its newer products and services will catalyze better top-line performance.

6. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

AppLovin is extremely efficient at acquiring new customers, and its CAC payback period checked in at 0.1 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give AppLovin more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

7. Gross Margin & Pricing Power

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

AppLovin’s gross margin is one of the best in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 87.9% gross margin over the last year. Said differently, roughly $87.86 was left to spend on selling, marketing, and R&D for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. AppLovin has seen gross margins improve by 20.1 percentage points over the last 2 year, which is elite in the software space.

In Q4, AppLovin produced a 88.9% gross profit margin, up 12.3 percentage points year on year. AppLovin’s full-year margin has also been trending up over the past 12 months, increasing by 2.5 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

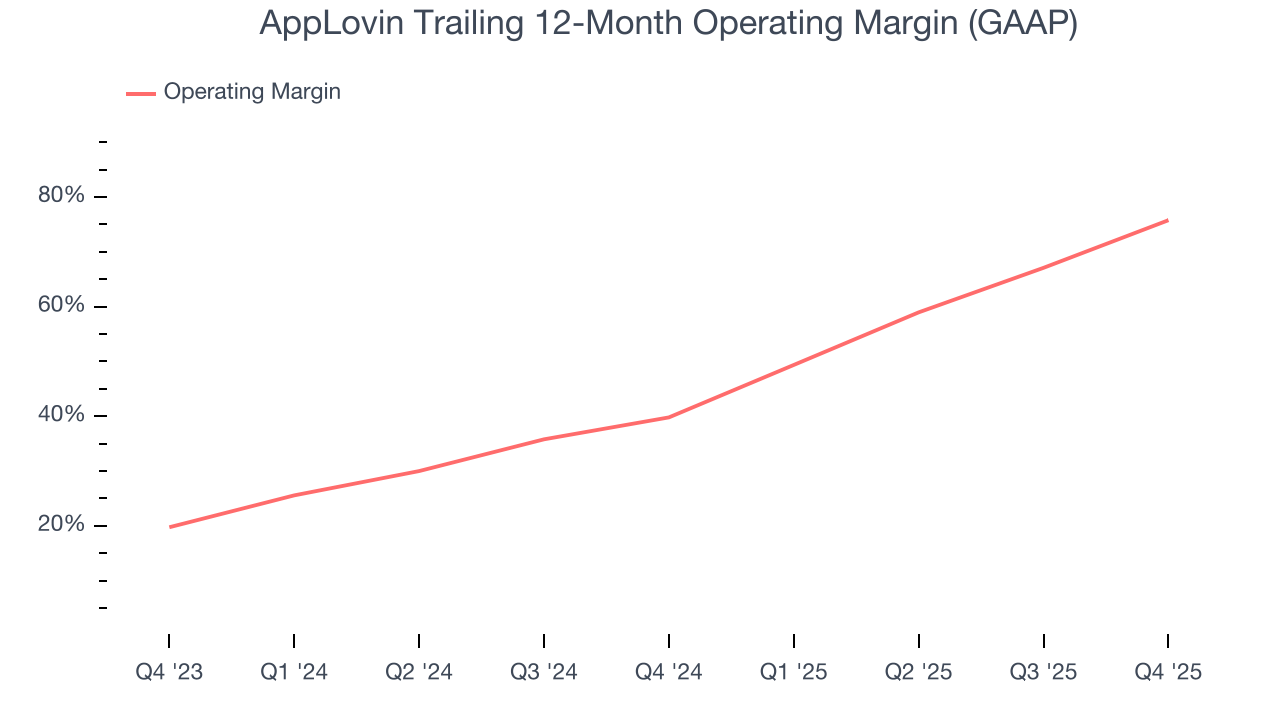

8. Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

AppLovin has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 75.8%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, AppLovin’s operating margin rose by 36 percentage points over the last two years, as its sales growth gave it immense operating leverage.

In Q4, AppLovin generated an operating margin profit margin of 76.9%, up 32.6 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

9. Cash Is King

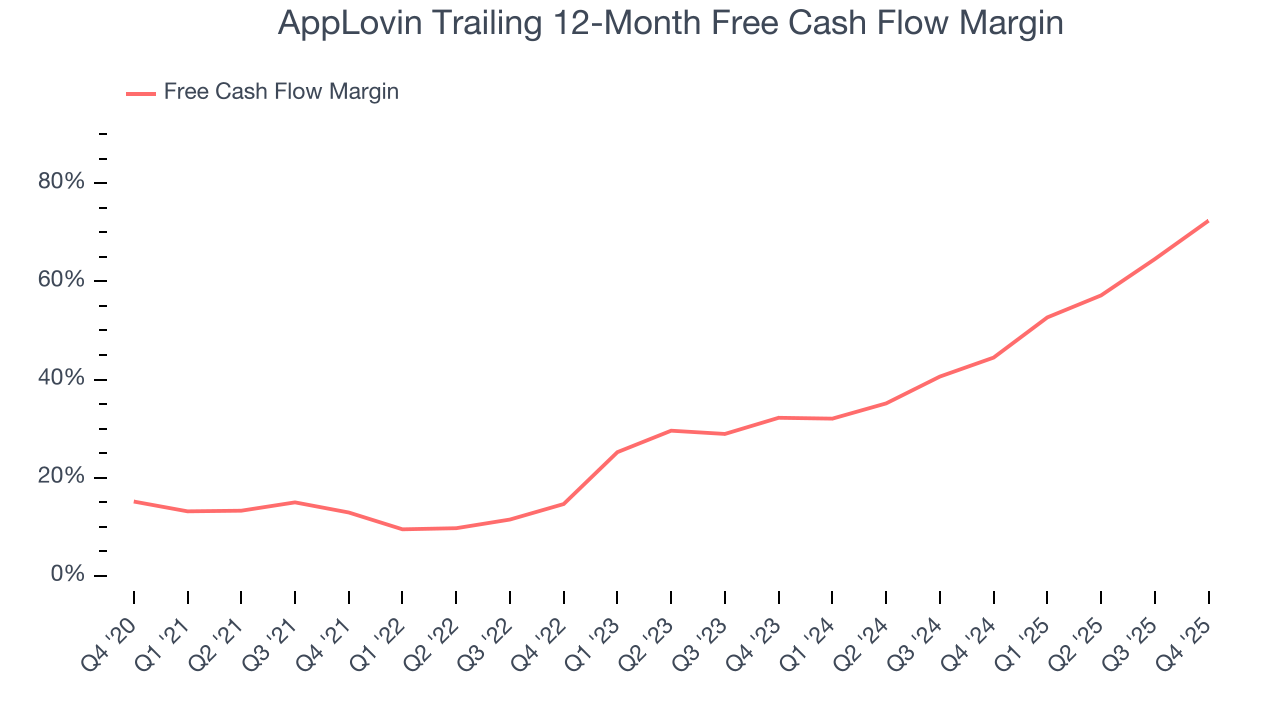

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

AppLovin has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 72.4% over the last year.

AppLovin’s free cash flow clocked in at $1.31 billion in Q4, equivalent to a 79% margin. This result was good as its margin was 28.2 percentage points higher than in the same quarter last year. Its cash profitability was also above its one-year level, and we hope the company can build on this trend.

Over the next year, analysts predict AppLovin’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 72.4% for the last 12 months will decrease to 61%.

10. Balance Sheet Assessment

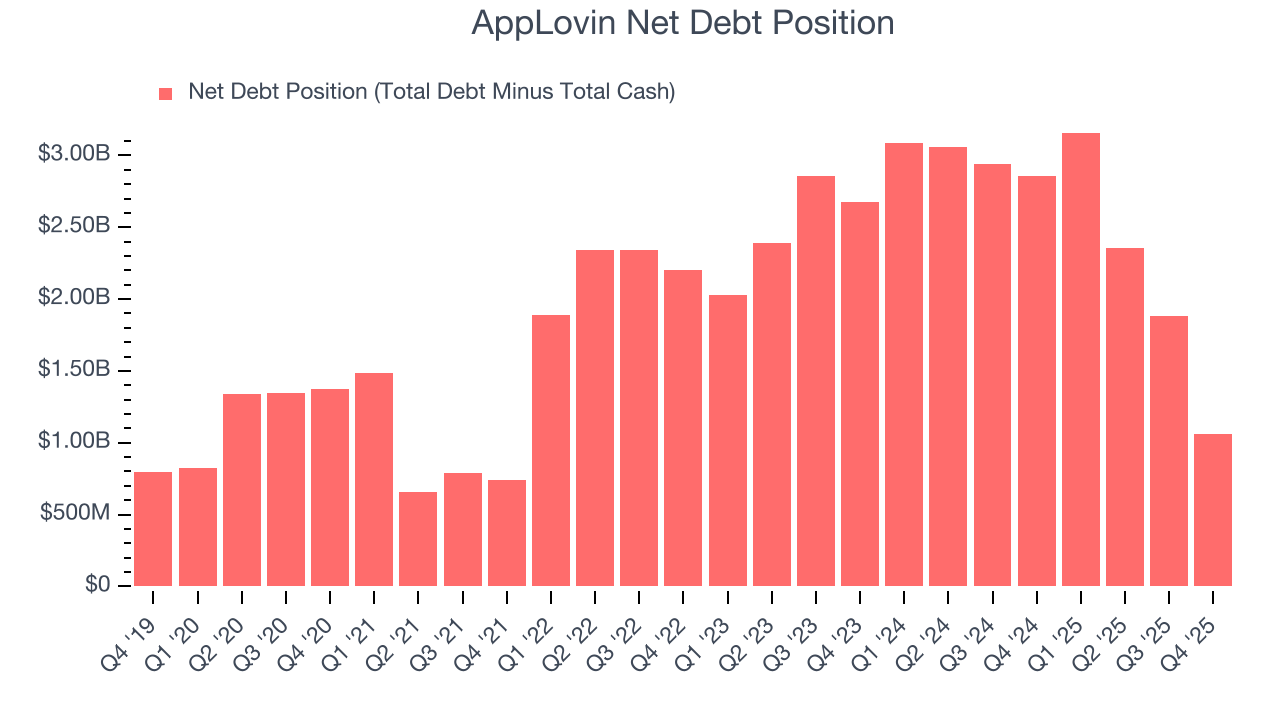

AppLovin reported $2.49 billion of cash and $3.54 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $4.51 billion of EBITDA over the last 12 months, we view AppLovin’s 0.2× net-debt-to-EBITDA ratio as safe. We also see its $104.4 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from AppLovin’s Q4 Results

We were impressed by AppLovin’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also glad its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The market seemed to be hoping for more, and the stock traded down 1.2% to $453.71 immediately after reporting.

12. Is Now The Time To Buy AppLovin?

Updated: February 25, 2026 at 9:41 PM EST

Are you wondering whether to buy AppLovin or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

AppLovin is a cream-of-the-crop software company. For starters, its revenue growth was strong over the last five years and is expected to accelerate over the next 12 months. On top of that, its bountiful generation of free cash flow empowers it to invest in growth initiatives, and its admirable gross margin indicates excellent unit economics.

AppLovin’s price-to-sales ratio based on the next 12 months is 16.6x. You get what you pay for, and in this case, the higher valuation is warranted because AppLovin’s fundamentals clearly illustrate it’s a special business. We think the stock is attractive here.

Wall Street analysts have a consensus one-year price target of $661.59 on the company (compared to the current share price of $417.50), implying they see 58.5% upside in buying AppLovin in the short term.