Atlanticus Holdings (ATLC)

Atlanticus Holdings is intriguing, but the state of its balance sheet makes us slightly uncomfortable.― StockStory Analyst Team

1. News

2. Summary

Why Atlanticus Holdings Is Not Exciting

Using data analytics to serve the millions of Americans with less-than-perfect credit scores, Atlanticus Holdings (NASDAQ:ATLC) provides technology and services that help lenders offer credit products to consumers often overlooked by traditional financing providers.

- Earnings per share have dipped by 5.7% annually over the past four years, which is concerning because stock prices follow EPS over the long term

- High net-debt-to-EBITDA ratio of 70× could force the company to raise capital at unfavorable terms if market conditions deteriorate

Atlanticus Holdings has some respectable qualities, but we wouldn’t invest until its EBITDA can comfortably support its debt.

Why There Are Better Opportunities Than Atlanticus Holdings

Atlanticus Holdings’s stock price of $55.03 implies a valuation ratio of 6.4x forward P/E. Atlanticus Holdings’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Atlanticus Holdings (ATLC) Research Report: Q4 CY2025 Update

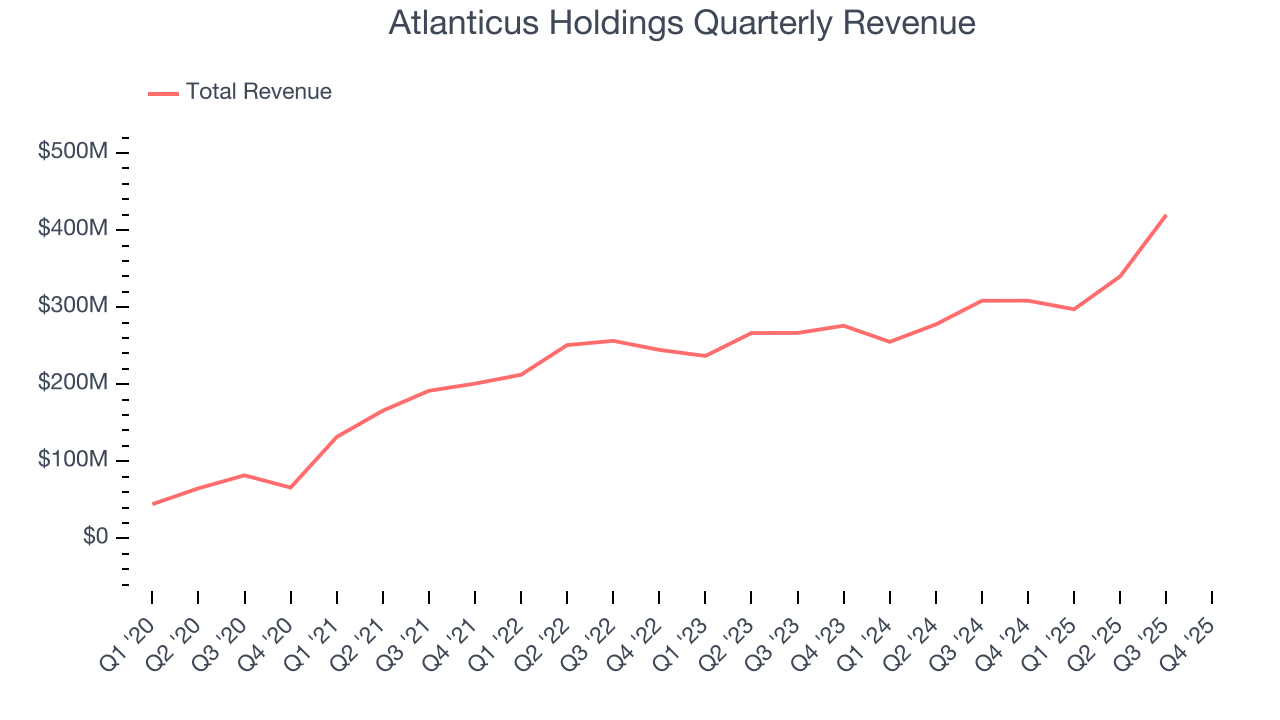

Financial technology company Atlanticus Holdings (NASDAQ:ATLC) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 138% year on year to $734.4 million. Its GAAP profit of $1.75 per share was 10.1% above analysts’ consensus estimates.

Atlanticus Holdings (ATLC) Q4 CY2025 Highlights:

- Revenue: $734.4 million vs analyst estimates of $568.6 million (138% year-on-year growth, 29.1% beat)

- Pre-tax Profit: $46.22 million (6.3% margin)

- EPS (GAAP): $1.75 vs analyst estimates of $1.59 (10.1% beat)

- Market Capitalization: $834.8 million

Company Overview

Using data analytics to serve the millions of Americans with less-than-perfect credit scores, Atlanticus Holdings (NASDAQ:ATLC) provides technology and services that help lenders offer credit products to consumers often overlooked by traditional financing providers.

Atlanticus operates through two main segments: Credit as a Service (CaaS) and Auto Finance. The CaaS segment serves as a program manager for bank partners like Bank of Missouri and WebBank, offering a technology platform that enables instant credit decisions at retail points of sale, through digital marketing channels, and via partnerships. Private label credit cards are issued under the Fortiva and Curae brands (the latter focused on healthcare financing), while general purpose credit cards use the Aspire, Imagine, and Fortiva brands.

The company's proprietary decisioning platform leverages machine learning and hundreds of data points to evaluate applications, allowing its bank partners to approve consumers with lower FICO scores who might be rejected by traditional lenders. When receivables are generated, Atlanticus typically acquires them from its bank partners, earning returns through interest, fees, and merchant payments.

In the Auto Finance segment, through its CAR subsidiary, Atlanticus purchases and services auto loans from independent dealerships in the buy-here, pay-here used car market. It generates revenue by purchasing loans at a discount and through servicing fees. The company also provides floor-plan financing and other services to its network of dealers across numerous states.

Atlanticus processes these transactions through paperless platforms that integrate with retailers, healthcare providers, and auto dealers, creating a seamless experience for both merchants and consumers seeking financing options.

4. Personal Loan

Personal loan providers offer unsecured credit for various consumer needs. The sector benefits from digital application processes, increasing consumer comfort with online financial services, and opportunities in underserved credit segments. Headwinds include credit risk management in unsecured lending, regulatory oversight of lending practices, and intense competition affecting margins from both traditional and fintech lenders.

Atlanticus Holdings competes with traditional credit card issuers, payment technology providers like Block (NYSE:SQ) and PayPal (NASDAQ:PYPL), buy-now-pay-later companies such as Affirm (NASDAQ:AFRM) and Klarna, and other financial technology firms focused on non-prime consumers like Upstart (NASDAQ:UPST) and Enova International (NYSE:ENVA).

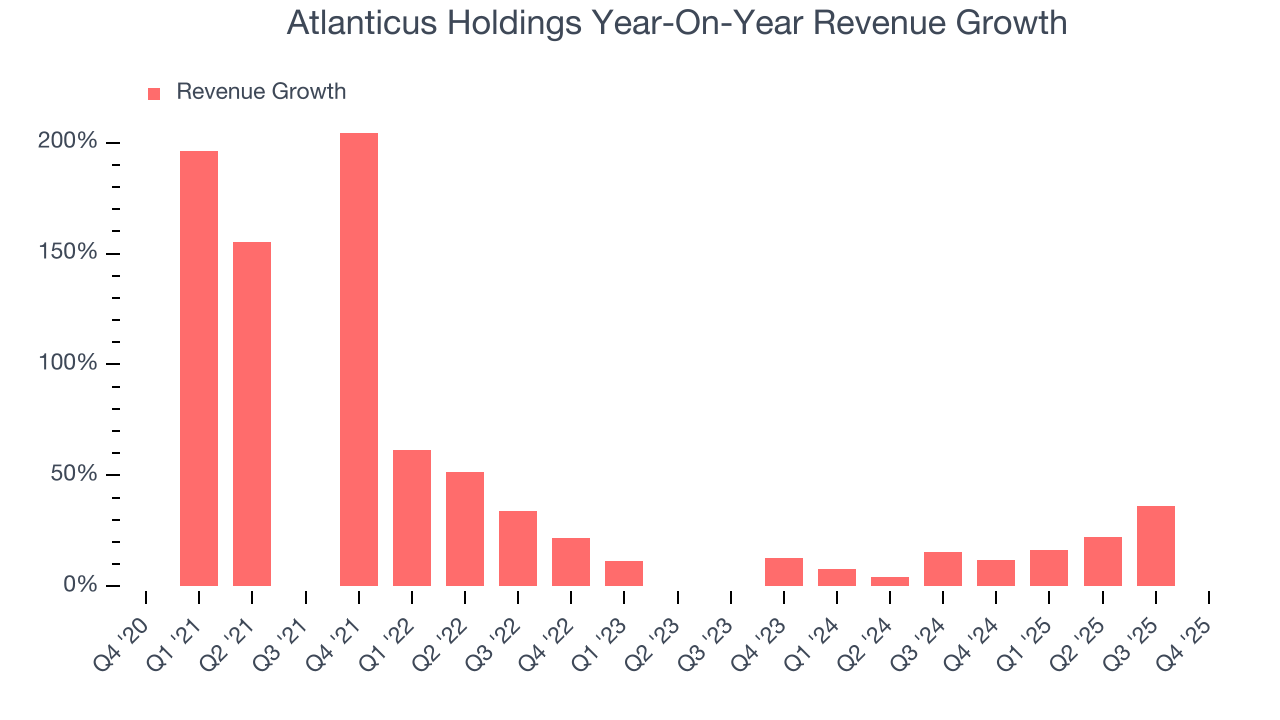

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Atlanticus Holdings’s revenue grew at an incredible 47.4% compounded annual growth rate over the last five years. Its growth beat the average financials company and shows its offerings resonate with customers.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Atlanticus Holdings’s annualized revenue growth of 30.9% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Atlanticus Holdings reported magnificent year-on-year revenue growth of 138%, and its $734.4 million of revenue beat Wall Street’s estimates by 29.1%.

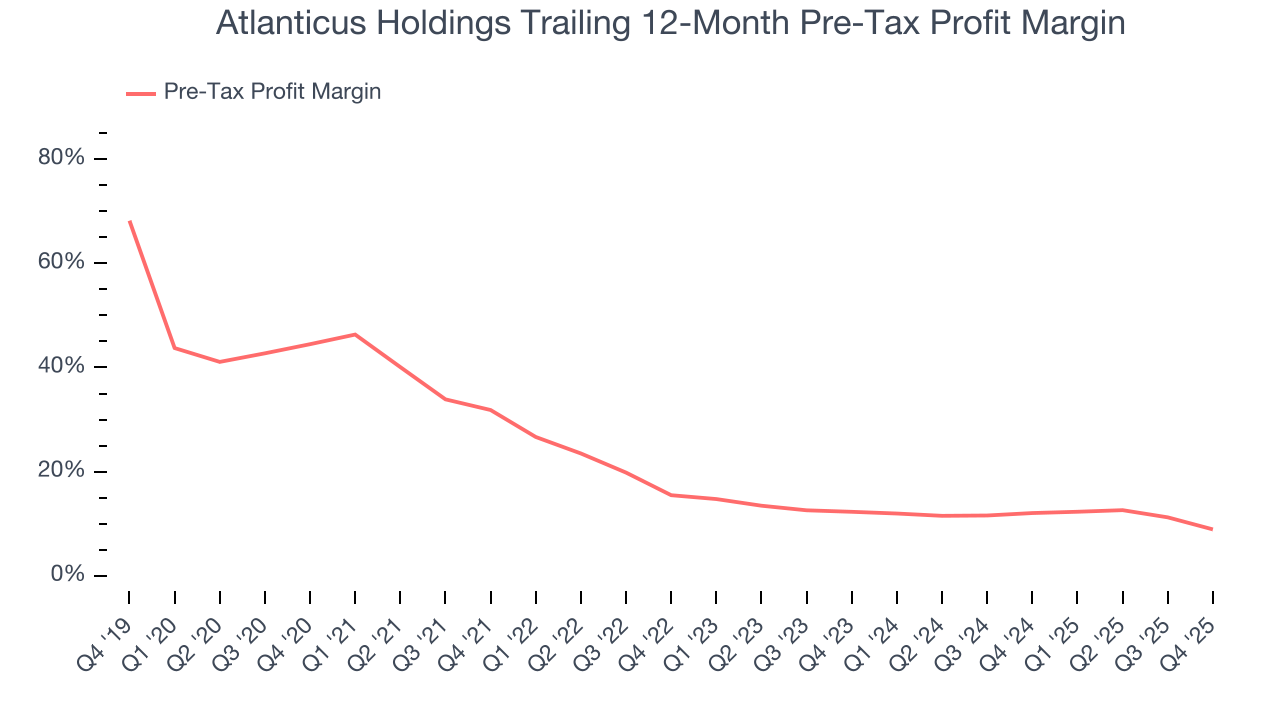

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Personal Loan companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

This is because for financials businesses, interest income and expense should be factored into the definition of profit but taxes - which are largely out of a company's control - should not.

Over the last five years, Atlanticus Holdings’s pre-tax profit margin has risen by 35.6 percentage points, going from 31.8% to 8.9%. It has also declined by 3.4 percentage points on a two-year basis, showing its expenses have consistently increased at a faster rate than revenue. This usually raises questions unless the company is in high-growth mode and reinvesting its profits into attractive ventures.

Atlanticus Holdings’s pre-tax profit margin came in at 6.3% this quarter. This result was 6.6 percentage points worse than the same quarter last year.

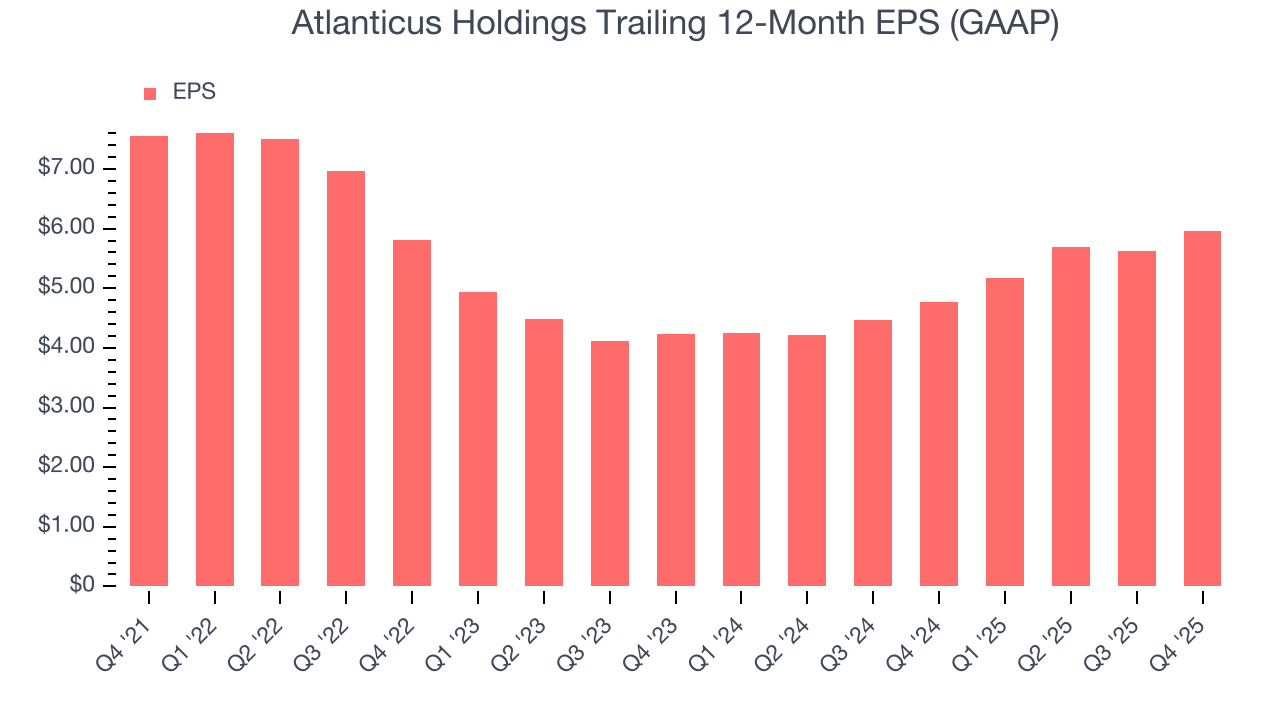

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Atlanticus Holdings’s full-year EPS dropped 25.2%, or 5.8% annually, over the last four years. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Atlanticus Holdings’s EPS grew at a remarkable 18.6% compounded annual growth rate over the last two years. This performance was better than most financials businesses.

We can take a deeper look into Atlanticus Holdings’s earnings to better understand the drivers of its performance. Atlanticus Holdings’s pre-tax profit margin has declined over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Atlanticus Holdings reported EPS of $1.75, up from $1.42 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Atlanticus Holdings’s full-year EPS of $5.96 to grow 46.3%.

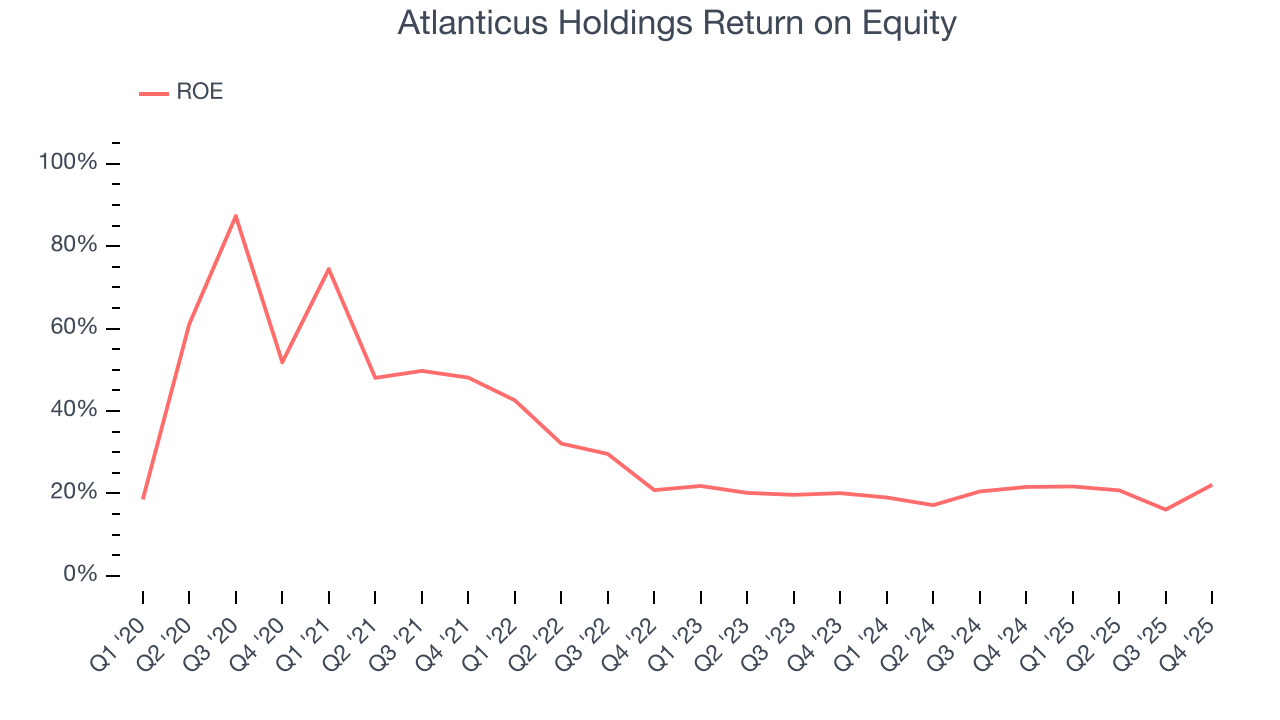

8. Return on Equity

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, Atlanticus Holdings has averaged an ROE of 29.3%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This is a bright spot for Atlanticus Holdings.

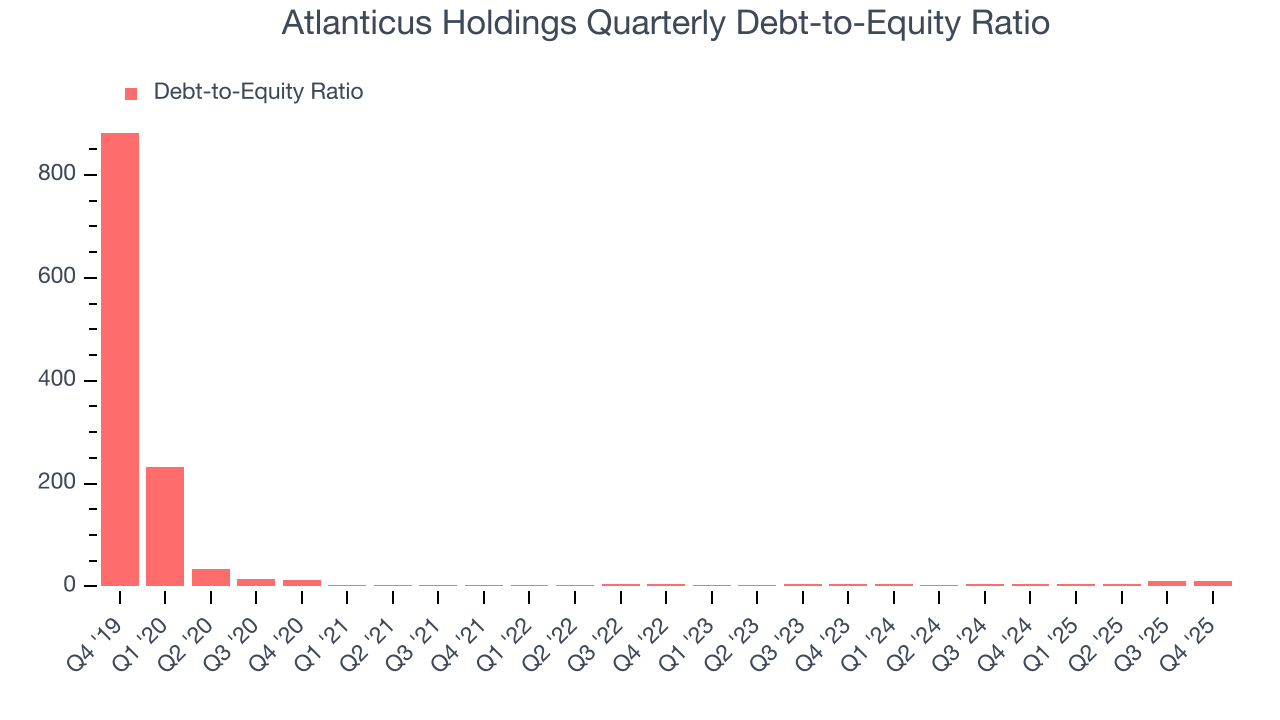

9. Balance Sheet Risk

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Atlanticus Holdings currently has $6.54 billion of debt and $608.7 million of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 7.3×. We think this is dangerous - for a financials business, anything above 3.5× raises red flags.

10. Key Takeaways from Atlanticus Holdings’s Q4 Results

We were impressed by how significantly Atlanticus Holdings blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $52.74 immediately after reporting.

11. Is Now The Time To Buy Atlanticus Holdings?

Updated: March 13, 2026 at 1:14 AM EDT

When considering an investment in Atlanticus Holdings, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Atlanticus Holdings is a pretty decent company if you ignore its balance sheet. First off, its revenue growth was exceptional over the last five years and is expected to accelerate over the next 12 months. And while its declining pre-tax profit margin shows the business has become less efficient, its stellar ROE suggests it has been a well-run company historically.

Atlanticus Holdings’s P/E ratio based on the next 12 months is 6.4x. Certain aspects of its fundamentals are attractive, but we aren’t investing at the moment because its balance sheet makes us uneasy. Interested in this company and its prospects? We recommend you wait until its debt load falls or its profits increase.

Wall Street analysts have a consensus one-year price target of $91.60 on the company (compared to the current share price of $55.03).