BrightSpring Health Services (BTSG)

BrightSpring Health Services is intriguing. Its strong sales growth shows it won market share, and there’s a decent chance its momentum will continue.― StockStory Analyst Team

1. News

2. Summary

Why BrightSpring Health Services Is Interesting

Founded in 1974, BrightSpring Health Services (NASDAQ:BTSG) offers home health care, hospice, neuro-rehabilitation, and pharmacy services.

- Estimated revenue growth of 14.9% for the next 12 months implies its momentum over the last two years will continue

- Impressive 18.3% annual revenue growth over the last five years indicates it’s winning market share this cycle

- One risk is its responsiveness to unforeseen market trends is restricted due to its substandard adjusted operating margin profitability

BrightSpring Health Services shows some potential. If you’re a believer, the valuation looks fair.

Why Is Now The Time To Buy BrightSpring Health Services?

At $38.04 per share, BrightSpring Health Services trades at 25x forward P/E. This multiple is higher than that of most healthcare companies, sure, but we still think the valuation is fair given the revenue growth.

If you think the market is not giving the company enough credit for its fundamentals, now could be a good time to invest.

3. BrightSpring Health Services (BTSG) Research Report: Q4 CY2025 Update

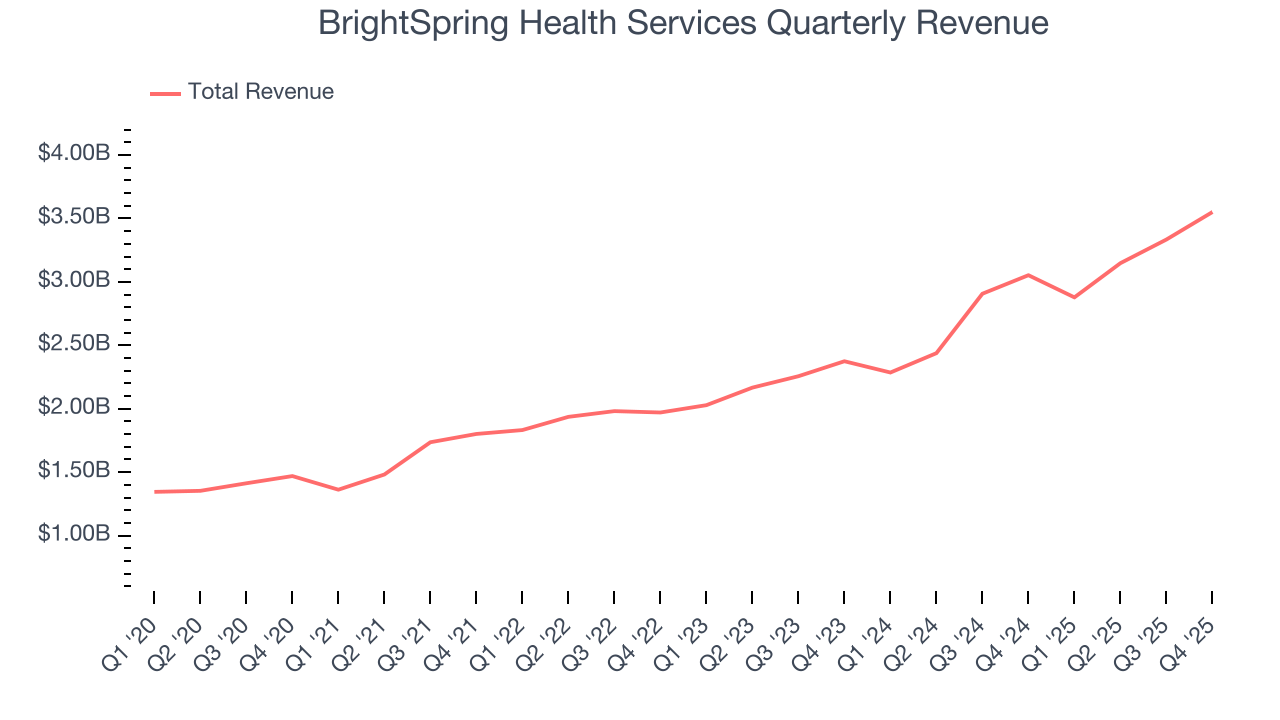

Healthcare services provider BrightSpring Health Services (NASDAQ:BTSG) announced better-than-expected revenue in Q4 CY2025, with sales up 16.3% year on year to $3.55 billion. The company’s full-year revenue guidance of $14.73 billion at the midpoint came in 0.7% above analysts’ estimates. Its non-GAAP profit of $0.33 per share was 4.7% below analysts’ consensus estimates.

BrightSpring Health Services (BTSG) Q4 CY2025 Highlights:

- Revenue: $3.55 billion vs analyst estimates of $3.38 billion (16.3% year-on-year growth, 5% beat)

- Adjusted EPS: $0.33 vs analyst expectations of $0.35 (4.7% miss)

- Adjusted EBITDA: $184 million vs analyst estimates of $177.1 million (5.2% margin, 3.9% beat)

- EBITDA guidance for the upcoming financial year 2026 is $775 million at the midpoint, above analyst estimates of $702 million

- Operating Margin: 3%, in line with the same quarter last year

- Free Cash Flow Margin: 5.5%, up from 2.5% in the same quarter last year

- Market Capitalization: $8.31 billion

Company Overview

Founded in 1974, BrightSpring Health Services (NASDAQ:BTSG) offers home health care, hospice, neuro-rehabilitation, and pharmacy services.

The company focuses on serving individuals in need of high-quality, personalized care in home and community settings as opposed to formal facilities such as hospitals.

4. Senior Health, Home Health & Hospice

The senior health, home care, and hospice care industries provide essential services to aging populations and patients with chronic or terminal conditions. These companies benefit from stable, recurring revenue driven by relationships with patients and families that can extend many months or even years. However, the labor-intensive nature of the business makes it vulnerable to rising labor costs and staffing shortages, while profitability is constrained by reimbursement rates from Medicare, Medicaid, and private insurers. Looking ahead, the industry is positioned for tailwinds from an aging population, increasing chronic disease prevalence, and a growing preference for personalized in-home care. Advancements in remote monitoring and telehealth are expected to enhance efficiency and care delivery. However, headwinds such as labor shortages, wage inflation, and regulatory uncertainty around reimbursement could pose challenges. Investments in digitization and technology-driven care will be critical for long-term success.

Competitors include Amedisys (NASDAQ:AMED), Encompass Health (NYSE:EHC), UnitedHealth Group (NYSE:UNH), and Addus HomeCare (NASDAQ:ADUS).

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $12.91 billion in revenue over the past 12 months, BrightSpring Health Services has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

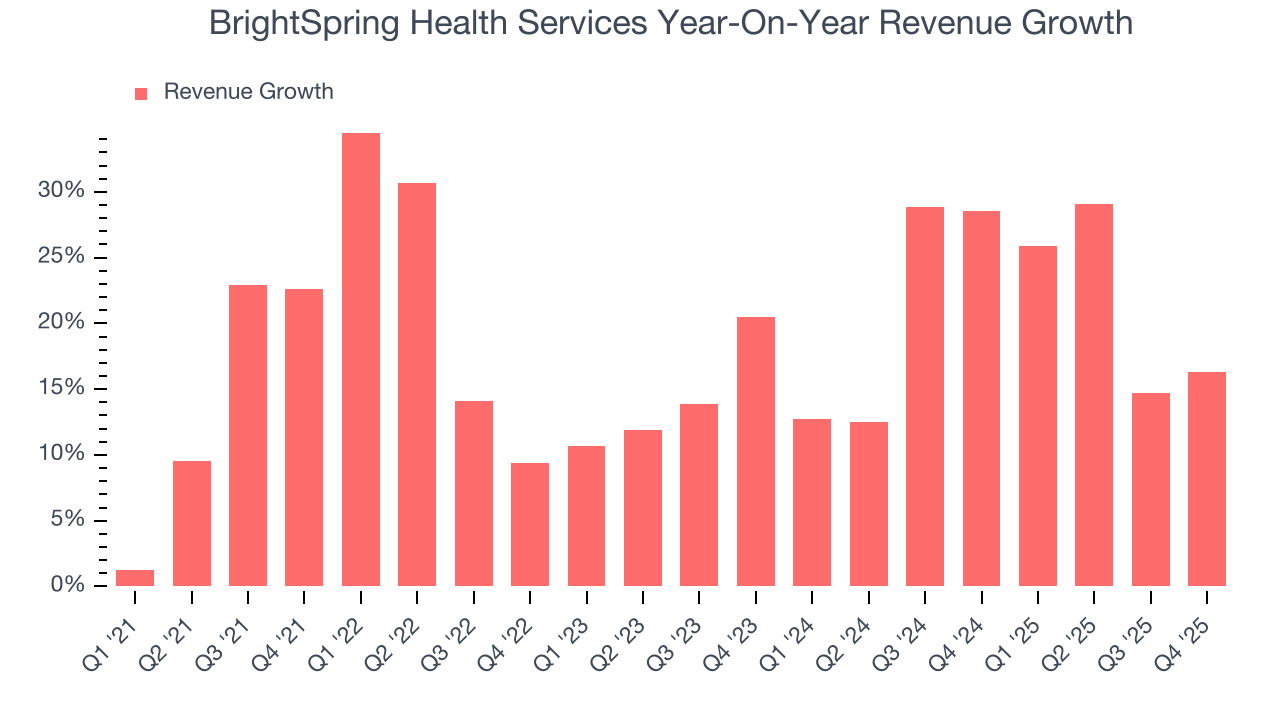

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, BrightSpring Health Services grew its sales at an impressive 18.3% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. BrightSpring Health Services’s annualized revenue growth of 20.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

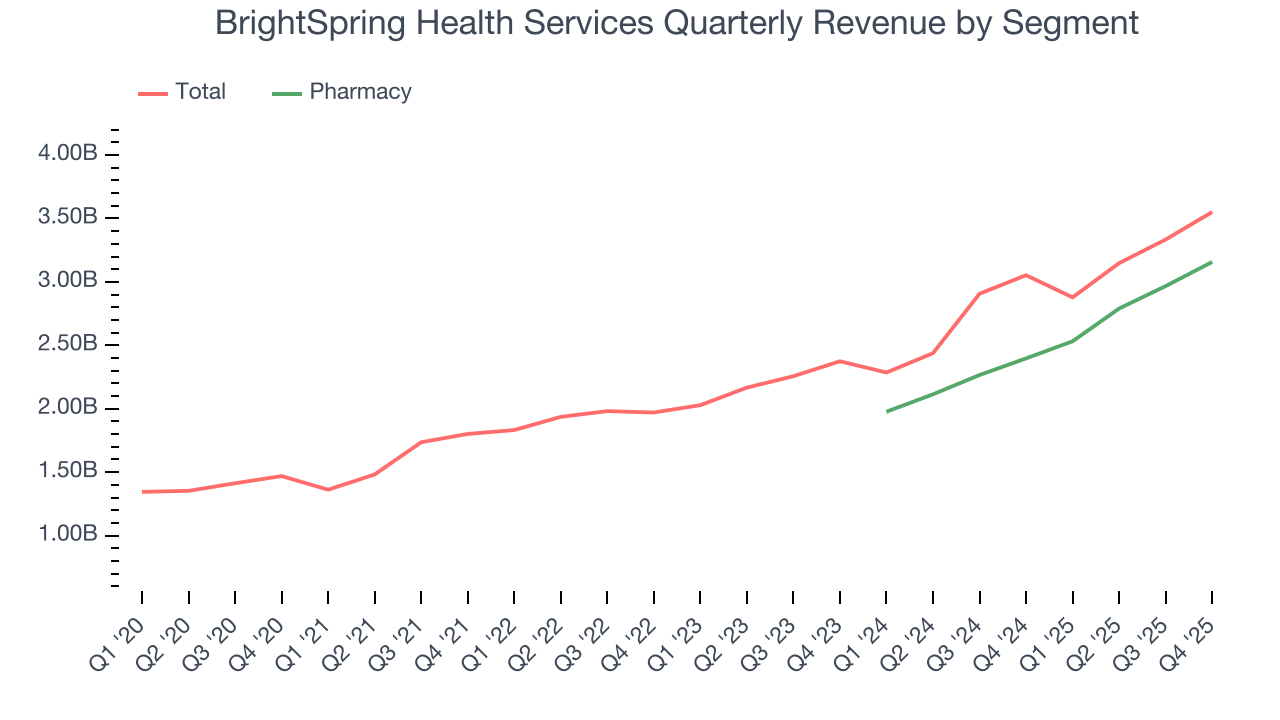

We can better understand the company’s revenue dynamics by analyzing its most important segment, Pharmacy. Over the last two years, BrightSpring Health Services’s Pharmacy revenue averaged 30.7% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, BrightSpring Health Services reported year-on-year revenue growth of 16.3%, and its $3.55 billion of revenue exceeded Wall Street’s estimates by 5%.

Looking ahead, sell-side analysts expect revenue to grow 13.4% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is attractive given its scale and suggests the market is baking in success for its products and services.

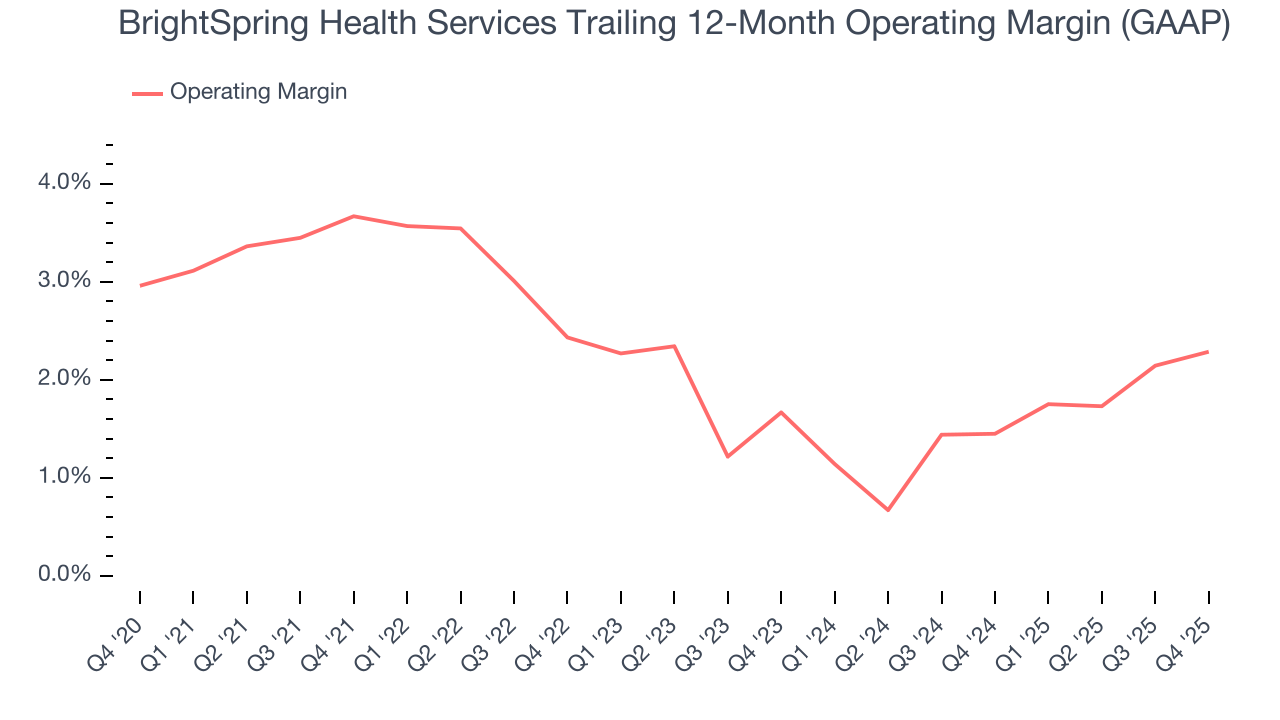

7. Operating Margin

BrightSpring Health Services was profitable over the last five years but held back by its large cost base. Its average operating margin of 2.2% was weak for a healthcare business.

Analyzing the trend in its profitability, BrightSpring Health Services’s operating margin decreased by 1.4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. BrightSpring Health Services’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, BrightSpring Health Services generated an operating margin profit margin of 3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

8. Cash Is King

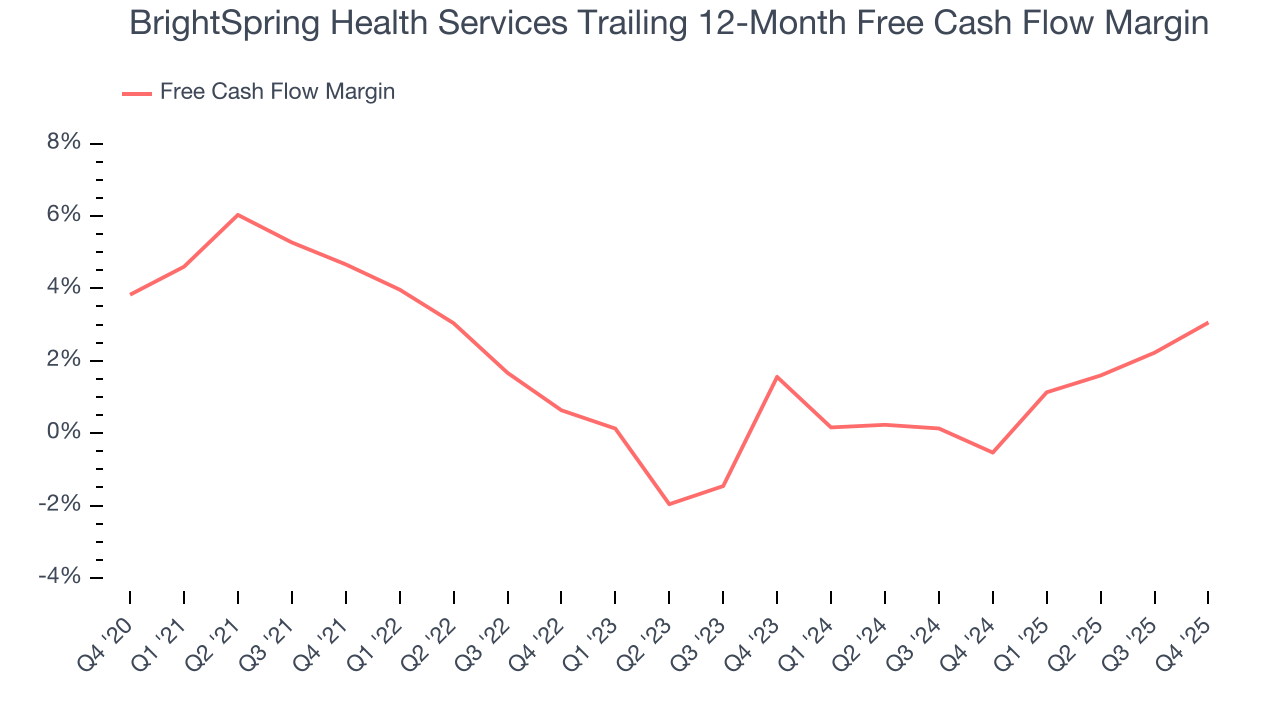

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

BrightSpring Health Services has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1.8%, subpar for a healthcare business.

Taking a step back, we can see that BrightSpring Health Services’s margin dropped by 1.6 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the longer-term trend returns, it could signal it’s in the middle of an investment cycle.

BrightSpring Health Services’s free cash flow clocked in at $193.9 million in Q4, equivalent to a 5.5% margin. This result was good as its margin was 3 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

9. Balance Sheet Assessment

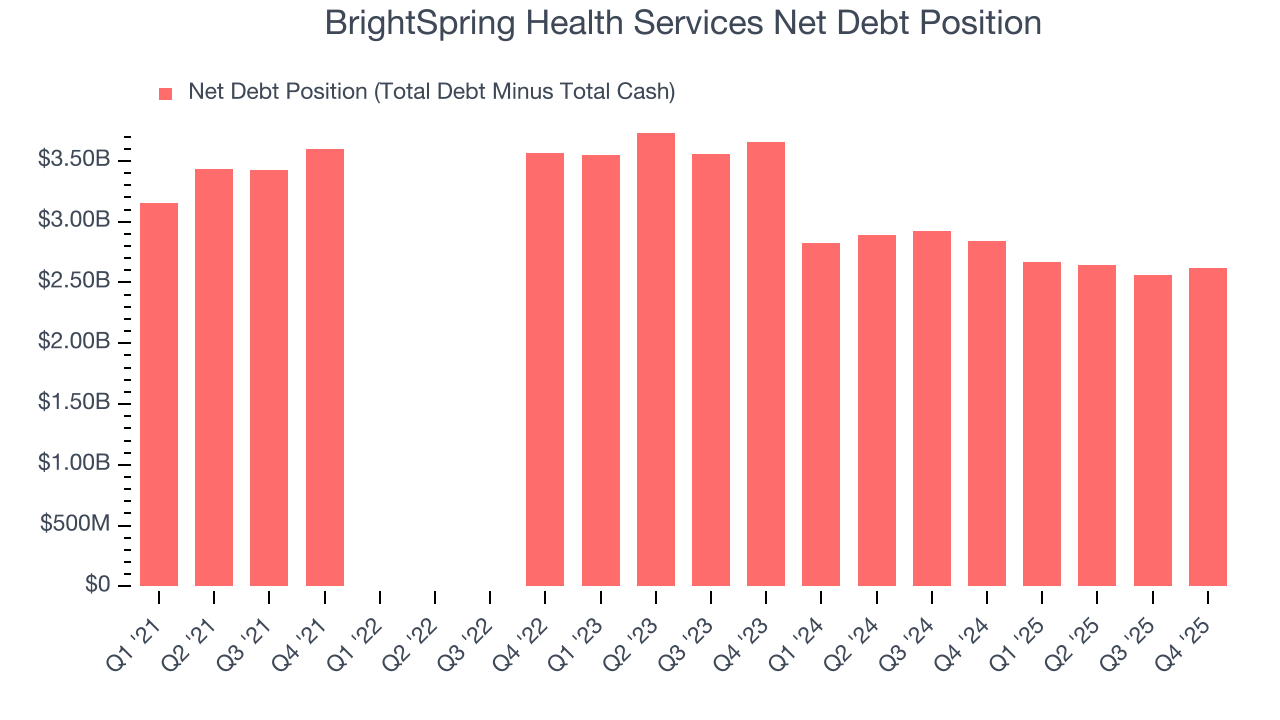

BrightSpring Health Services reported $88.37 million of cash and $2.71 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $618 million of EBITDA over the last 12 months, we view BrightSpring Health Services’s 4.2× net-debt-to-EBITDA ratio as safe. We also see its $80.24 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

10. Key Takeaways from BrightSpring Health Services’s Q4 Results

We were impressed by how significantly BrightSpring Health Services blew past analysts’ revenue expectations this quarter. We were also glad its full-year EBITDA guidance trumped Wall Street’s estimates. On the other hand, its EPS missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 1.9% to $40.88 immediately after reporting.

11. Is Now The Time To Buy BrightSpring Health Services?

Updated: March 17, 2026 at 12:08 AM EDT

When considering an investment in BrightSpring Health Services, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

There are a lot of things to like about BrightSpring Health Services. To kick things off, its revenue growth was impressive over the last five years. And while its operating margins are low compared to other healthcare companies, its scale and strong customer awareness give it negotiating power.

BrightSpring Health Services’s P/E ratio based on the next 12 months is 24.8x. When scanning the healthcare space, BrightSpring Health Services trades at a fair valuation. For those confident in the business and its management team, this is a good time to invest.

Wall Street analysts have a consensus one-year price target of $51.27 on the company (compared to the current share price of $39.09), implying they see 31.1% upside in buying BrightSpring Health Services in the short term.