Dave (DAVE)

Dave is a sound business. Its impressive revenue growth indicates the value of its offerings.― StockStory Analyst Team

1. News

2. Summary

Why Dave Is Interesting

Named after the biblical David fighting financial Goliaths, Dave (NASDAQ:DAVE) is a digital financial services platform that helps Americans living paycheck to paycheck with cash advances, banking services, and tools to improve their financial health.

- Impressive 35.2% annual revenue growth over the last five years indicates it’s winning market share this cycle

- One risk is its negative return on equity shows management lost money while trying to expand the business

Dave almost passes our quality test. If you believe in the company, the valuation looks reasonable.

Why Is Now The Time To Buy Dave?

Dave’s stock price of $191.77 implies a valuation ratio of 13.4x forward P/E. Looking at the financials space, we think the multiple is fair for the revenue growth characteristics.

If you think the market is undervaluing the company, now could be a good time to build a position.

3. Dave (DAVE) Research Report: Q3 CY2025 Update

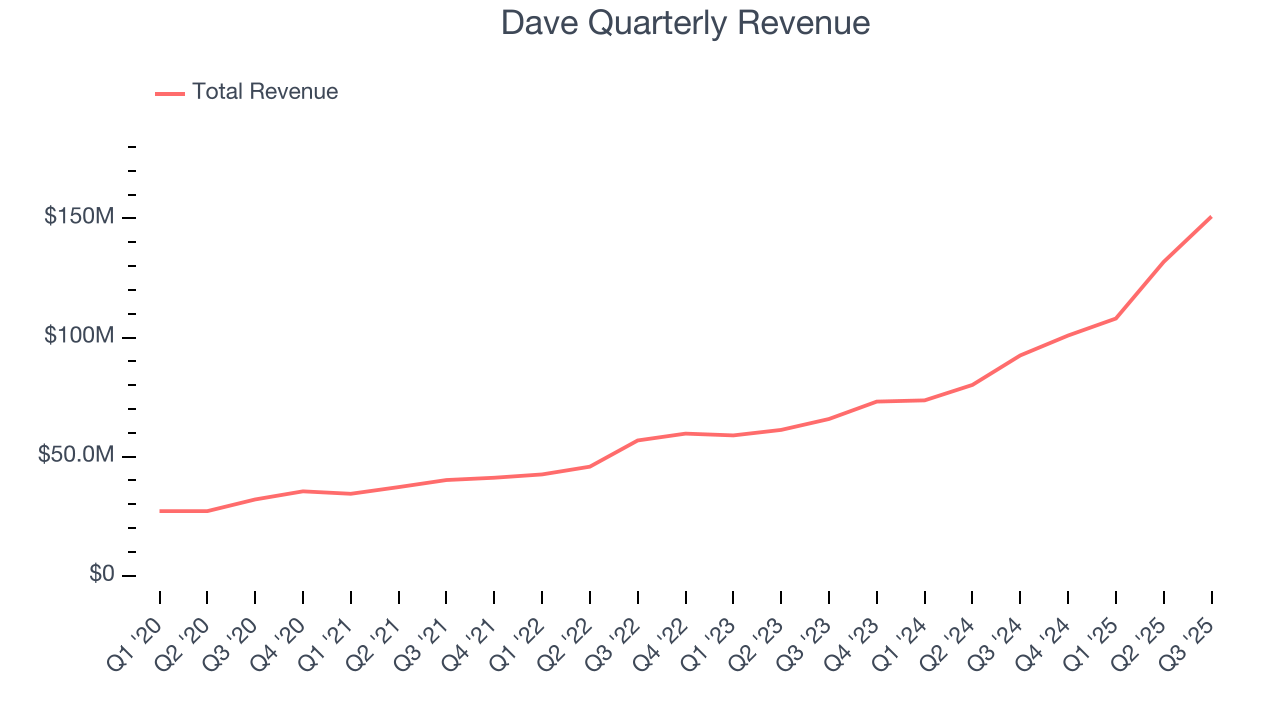

Digital banking platform Dave (NASDAQ:DAVE) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 63% year on year to $150.8 million. The company’s full-year revenue guidance of $545.5 million at the midpoint came in 6.5% above analysts’ estimates. Its non-GAAP profit of $4.24 per share was 81% above analysts’ consensus estimates.

Dave (DAVE) Q3 CY2025 Highlights:

Company Overview

Named after the biblical David fighting financial Goliaths, Dave (NASDAQ:DAVE) is a digital financial services platform that helps Americans living paycheck to paycheck with cash advances, banking services, and tools to improve their financial health.

Dave's flagship product is ExtraCash, which provides 0% interest cash advances to help users avoid overdraft fees or bridge the gap until their next paycheck. The company uses machine learning algorithms to analyze users' spending patterns and income history to determine advance amounts, which typically range from $5 to $500. Repayment is timed to coincide with the user's next expected paycheck, usually within 7-10 days.

The company also offers Dave Banking, a digital checking account with no minimum balance requirements or monthly fees. These FDIC-insured accounts come with features like early direct deposit access, cash-back rewards, and a 4% annual percentage yield on deposits. Users can access their funds through a Dave debit card, which offers fee-free withdrawals at thousands of ATMs nationwide.

Beyond banking services, Dave provides tools to help users improve their financial situation. The Budget feature helps members track spending and receive alerts about potential overdrafts. Side Hustle connects users with gig economy and part-time job opportunities, while Surveys offers a way to earn small amounts of supplemental income by completing online questionnaires.

Dave generates revenue through optional tips on cash advances, express fees for instant transfers, subscription fees for certain features, and interchange fees when users make purchases with their Dave debit cards. The company partners with Evolve Bank & Trust to provide its banking services and with Galileo Financial Technologies for payment processing infrastructure.

4. Personal Loan

Personal loan providers offer unsecured credit for various consumer needs. The sector benefits from digital application processes, increasing consumer comfort with online financial services, and opportunities in underserved credit segments. Headwinds include credit risk management in unsecured lending, regulatory oversight of lending practices, and intense competition affecting margins from both traditional and fintech lenders.

Dave competes with traditional banks and neobanks like Chime and Varo, cash advance providers such as Earnin and MoneyLion, and payment platforms with banking features like Cash App (Block, NYSE:SQ) and Venmo (PayPal, NASDAQ:PYPL). In the broader fintech space, Dave also faces competition from buy-now-pay-later services like Affirm (NASDAQ:AFRM) and Afterpay (Block, NYSE:SQ).

5. Revenue Growth

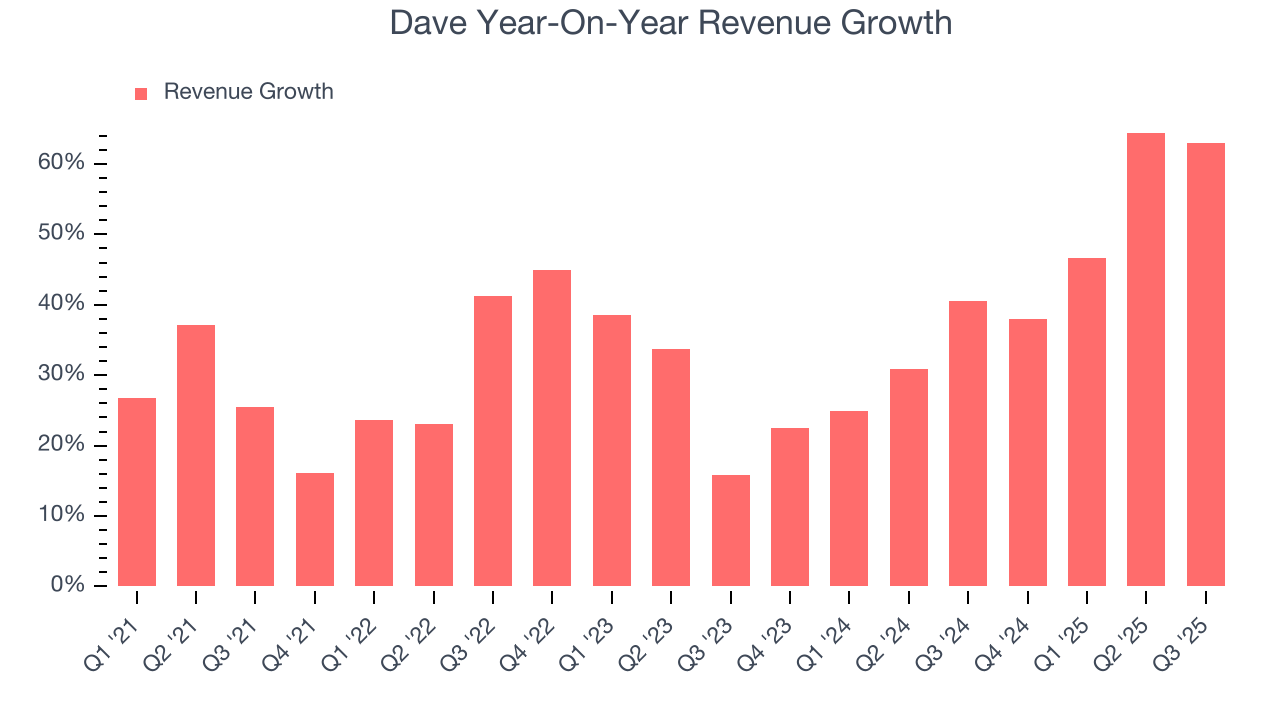

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Dave’s revenue grew at an incredible 35.2% compounded annual growth rate over the last five years. Its growth beat the average financials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Dave’s annualized revenue growth of 41.4% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Dave reported magnificent year-on-year revenue growth of 63%, and its $150.8 million of revenue beat Wall Street’s estimates by 13%.

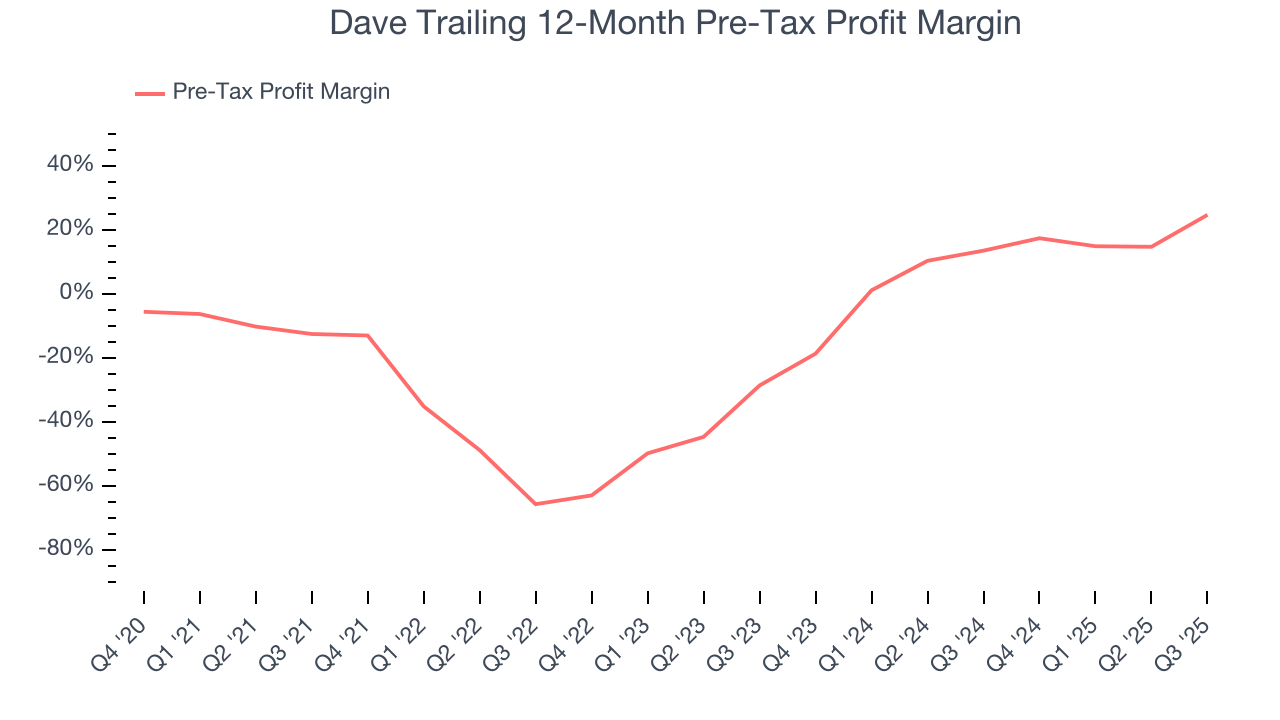

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Personal Loan companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

The pre-tax profit margin includes interest because it's central to how financial institutions generate revenue and manage costs. Tax considerations are excluded since they represent government policy rather than operational performance, giving investors a clearer view of business fundamentals.

Over the last four years, Dave’s pre-tax profit margin has fallen by 37.2 percentage points, going from negative 12.5% to 24.7%. It has also expanded by 53.3 percentage points on a two-year basis, showing its expenses have consistently grown at a slower rate than revenue. This typically signals prudent management.

In Q3, Dave’s pre-tax profit margin was 38.7%. This result was 37.8 percentage points better than the same quarter last year.

7. Return on Equity

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Dave has averaged an ROE of negative 28.4%, a disappointing result relative to the majority of firms putting up 25%+. But we wouldn’t write off Dave given its success in other measures of financial health.

8. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Dave has no debt, so leverage is not an issue here.

9. Key Takeaways from Dave’s Q3 Results

It was good to see Dave beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 12.5% to $269.89 immediately following the results.

10. Is Now The Time To Buy Dave?

Updated: March 2, 2026 at 12:04 AM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

There are things to like about Dave. To kick things off, its revenue growth was exceptional over the last five years. And while its relatively low ROE suggests management has struggled to find compelling investment opportunities, its astounding EPS growth over the last two years shows its profits are trickling down to shareholders. On top of that, its expanding pre-tax profit margin shows the business has become more efficient.

Dave’s P/E ratio based on the next 12 months is 13.4x. Looking at the financials space right now, Dave trades at a compelling valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $300.11 on the company (compared to the current share price of $191.77), implying they see 56.5% upside in buying Dave in the short term.