German American Bancorp (GABC)

There are things to like about German American Bancorp, but it doesn’t meet our bar for quality. We believe there are better stocks elsewhere.― StockStory Analyst Team

1. News

2. Summary

Why German American Bancorp Is Not Exciting

Founded in 1910 during a wave of community banking expansion in the Midwest, German American Bancorp (NASDAQ:GABC) is a financial holding company that provides banking, wealth management, and insurance services across southern Indiana and Kentucky.

- Capital trends were unexciting over the last five years as its 1.5% annual tangible book value per share growth was below the typical banking firm

- Annual earnings per share growth of 5.3% underperformed its revenue over the last five years, showing its incremental sales were less profitable

- On the bright side, its 13.6% annual net interest income growth over the last five years surpassed the sector average as its loans resonated with borrowers

German American Bancorp’s quality isn’t up to par. We’re redirecting our focus to better businesses.

Why There Are Better Opportunities Than German American Bancorp

German American Bancorp’s stock price of $40.03 implies a valuation ratio of 1.2x forward P/B. While valuation is appropriate for the quality you get, we’re still not buyers.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. German American Bancorp (GABC) Research Report: Q4 CY2025 Update

Regional banking company German American Bancorp (NASDAQ:GABC) announced better-than-expected revenue in Q4 CY2025, with sales up 47.1% year on year to $97.57 million. Its non-GAAP profit of $0.96 per share was 6.1% above analysts’ consensus estimates.

German American Bancorp (GABC) Q4 CY2025 Highlights:

- Net Interest Income: $78.68 million vs analyst estimates of $77.11 million (54.2% year-on-year growth, 2% beat)

- Net Interest Margin: 4.1% vs analyst estimates of 4% (9.2 basis point beat)

- Revenue: $97.57 million vs analyst estimates of $94.54 million (47.1% year-on-year growth, 3.2% beat)

- Efficiency Ratio: 48.6% vs analyst estimates of 50.8% (221.3 basis point beat)

- Adjusted EPS: $0.96 vs analyst estimates of $0.91 (6.1% beat)

- Tangible Book Value per Share: $20.08 vs analyst estimates of $19.62 (12% year-on-year growth, 2.3% beat)

- Market Capitalization: $1.62 billion

Company Overview

Founded in 1910 during a wave of community banking expansion in the Midwest, German American Bancorp (NASDAQ:GABC) is a financial holding company that provides banking, wealth management, and insurance services across southern Indiana and Kentucky.

German American Bancorp operates through three distinct business segments that work together to serve its regional customer base. The Core Banking segment forms the foundation of the business, where the company attracts deposits from the public and uses these funds to originate various types of loans. These include consumer loans, commercial and agricultural loans, real estate financing, and residential mortgages. The bank also sells residential mortgage loans in the secondary market as part of its regular operations.

Beyond traditional banking, the company's Wealth Management segment offers comprehensive financial planning services. Through its banking subsidiary and German American Investment Services, the company provides trust administration, investment advisory services, brokerage options, and retirement planning to help clients build and preserve wealth over generations.

The Insurance segment, operated primarily through German American Insurance, rounds out the company's financial services ecosystem by offering personal and corporate property and casualty insurance products. A business owner might open a commercial checking account with German American Bank, secure financing for business expansion, establish retirement plans for employees through the Wealth Management division, and protect business assets with insurance policies—all through one financial relationship.

The company maintains a securities portfolio consisting primarily of government agency securities, municipal obligations, and mortgage-backed securities. As a financial institution, German American operates under extensive regulatory oversight from agencies including the Federal Reserve, the FDIC, and state banking authorities.

4. Regional Banks

Regional banks, financial institutions operating within specific geographic areas, serve as intermediaries between local depositors and borrowers. They benefit from rising interest rates that improve net interest margins (the difference between loan yields and deposit costs), digital transformation reducing operational expenses, and local economic growth driving loan demand. However, these banks face headwinds from fintech competition, deposit outflows to higher-yielding alternatives, credit deterioration (increasing loan defaults) during economic slowdowns, and regulatory compliance costs. Recent concerns about regional bank stability following high-profile failures and significant commercial real estate exposure present additional challenges.

German American Bancorp competes with other regional banks operating in Indiana and Kentucky, including Old National Bancorp (NASDAQ:ONB), Stock Yards Bancorp (NASDAQ:SYBT), and First Financial Bancorp (NASDAQ:FFBC), as well as larger national banks with a presence in its markets.

5. Sales Growth

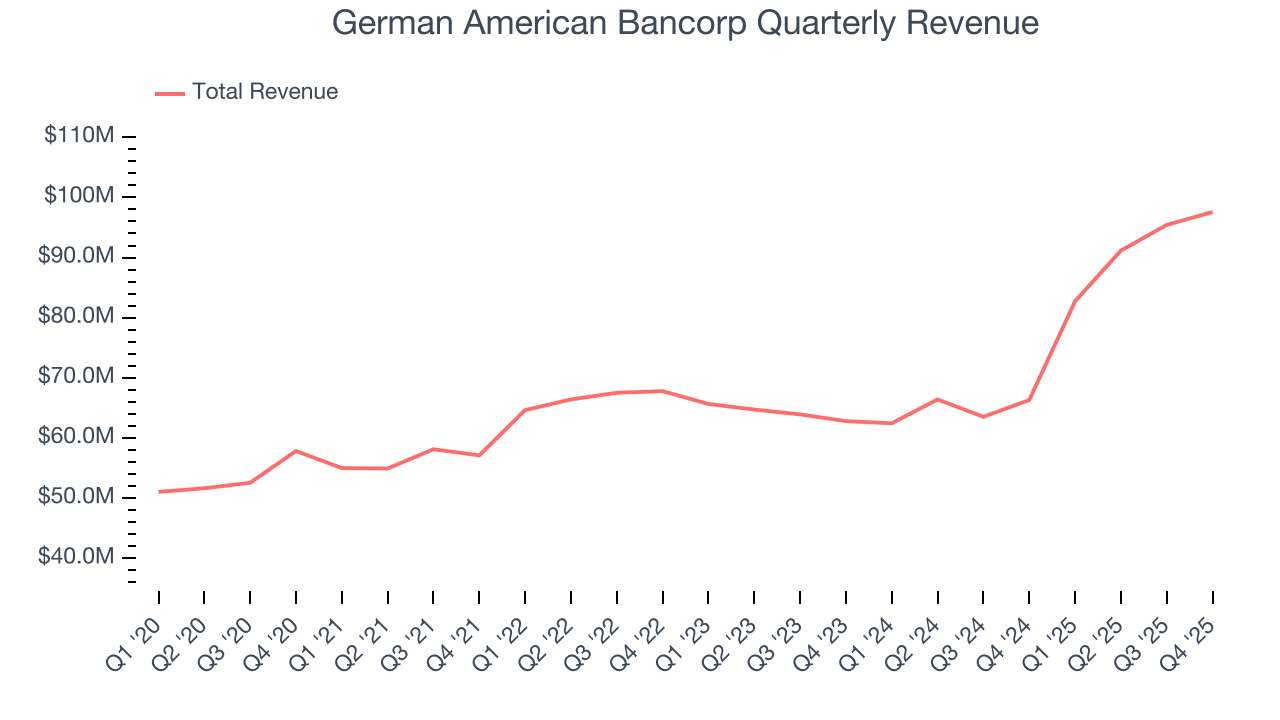

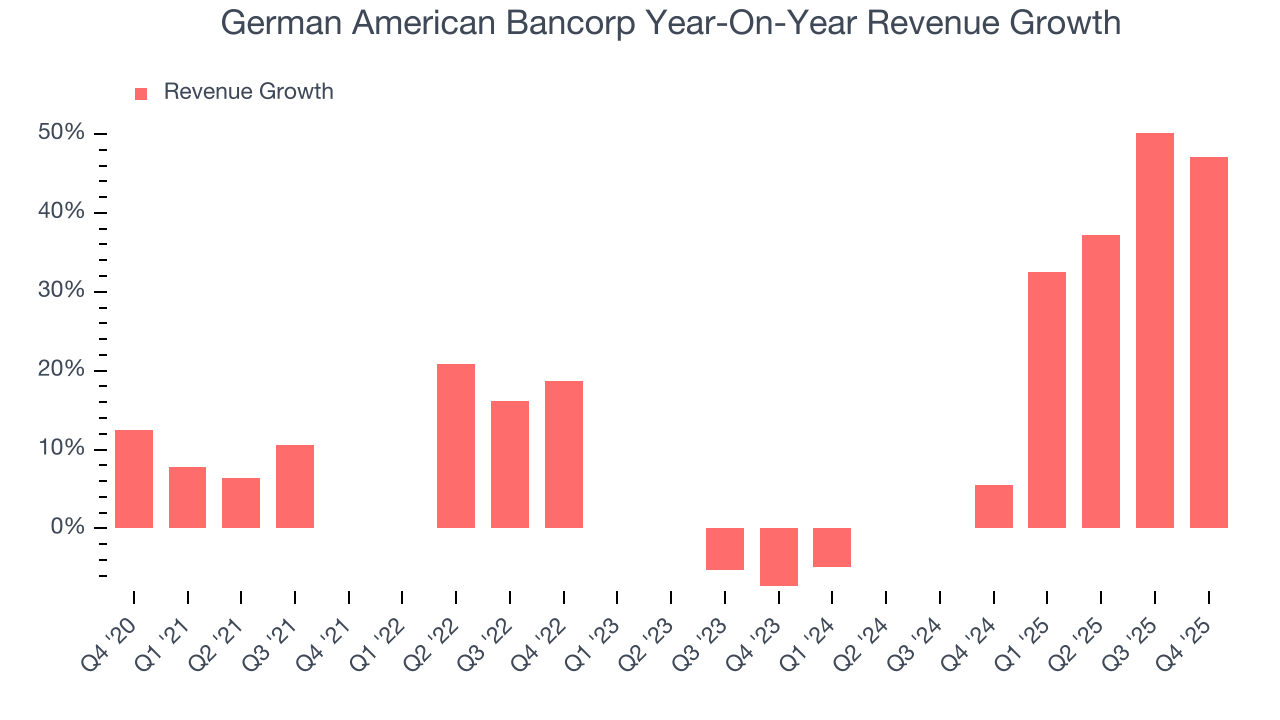

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees. Over the last five years, German American Bancorp grew its revenue at a decent 11.5% compounded annual growth rate. Its growth was slightly above the average banking company and shows its offerings resonate with customers.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. German American Bancorp’s annualized revenue growth of 19.4% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, German American Bancorp reported magnificent year-on-year revenue growth of 47.1%, and its $97.57 million of revenue beat Wall Street’s estimates by 3.2%.

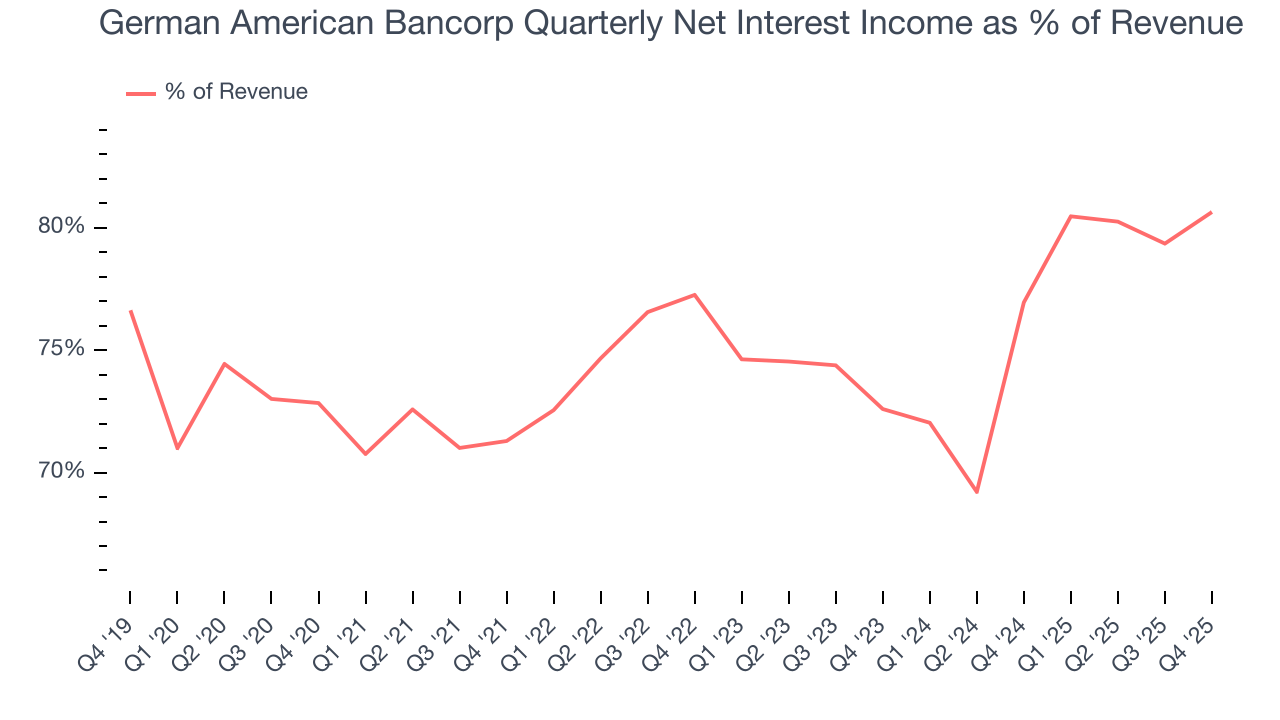

Net interest income made up 74.8% of the company’s total revenue during the last five years, meaning lending operations are German American Bancorp’s largest source of revenue.

Our experience and research show the market cares primarily about a bank’s net interest income growth as non-interest income is considered a lower-quality and non-recurring revenue source.

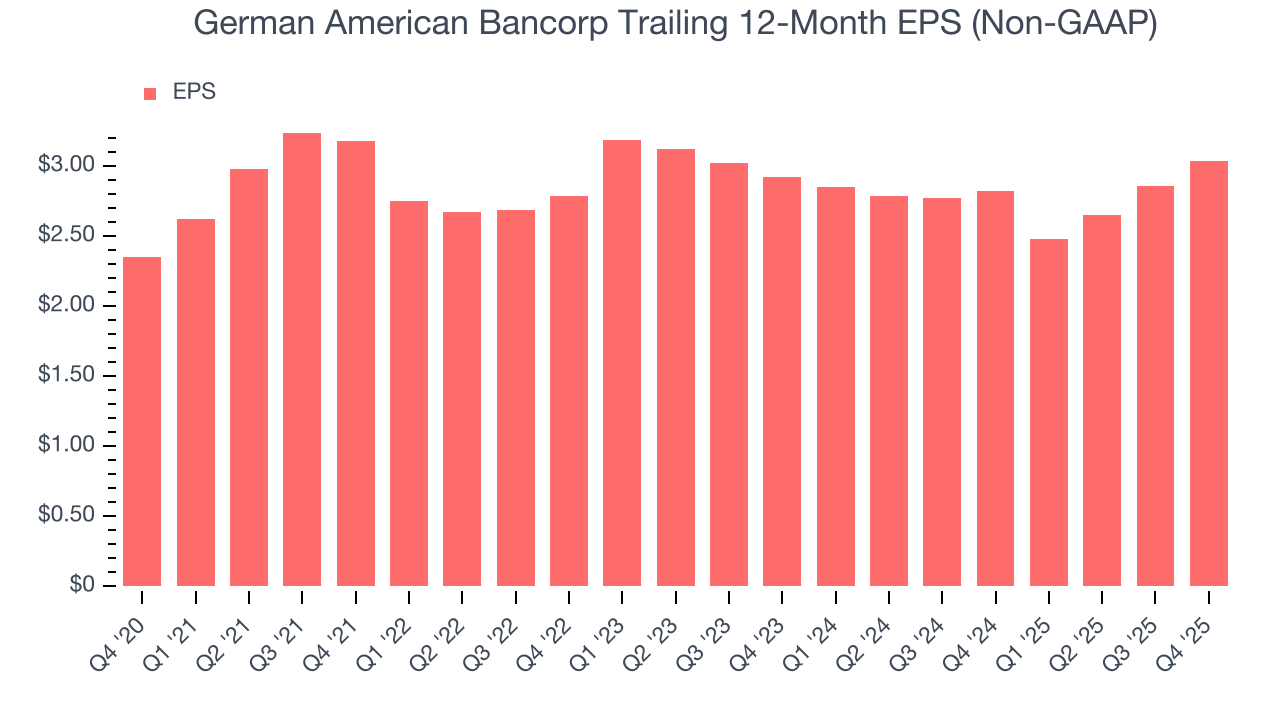

6. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

German American Bancorp’s EPS grew at a weak 5.3% compounded annual growth rate over the last five years, lower than its 11.5% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For German American Bancorp, its two-year annual EPS growth of 2% was lower than its five-year trend. This wasn’t great, but at least the company was successful in other measures of financial health.

In Q4, German American Bancorp reported adjusted EPS of $0.96, up from $0.78 in the same quarter last year. This print beat analysts’ estimates by 6.1%. Over the next 12 months, Wall Street expects German American Bancorp’s full-year EPS of $3.04 to grow 24.1%.

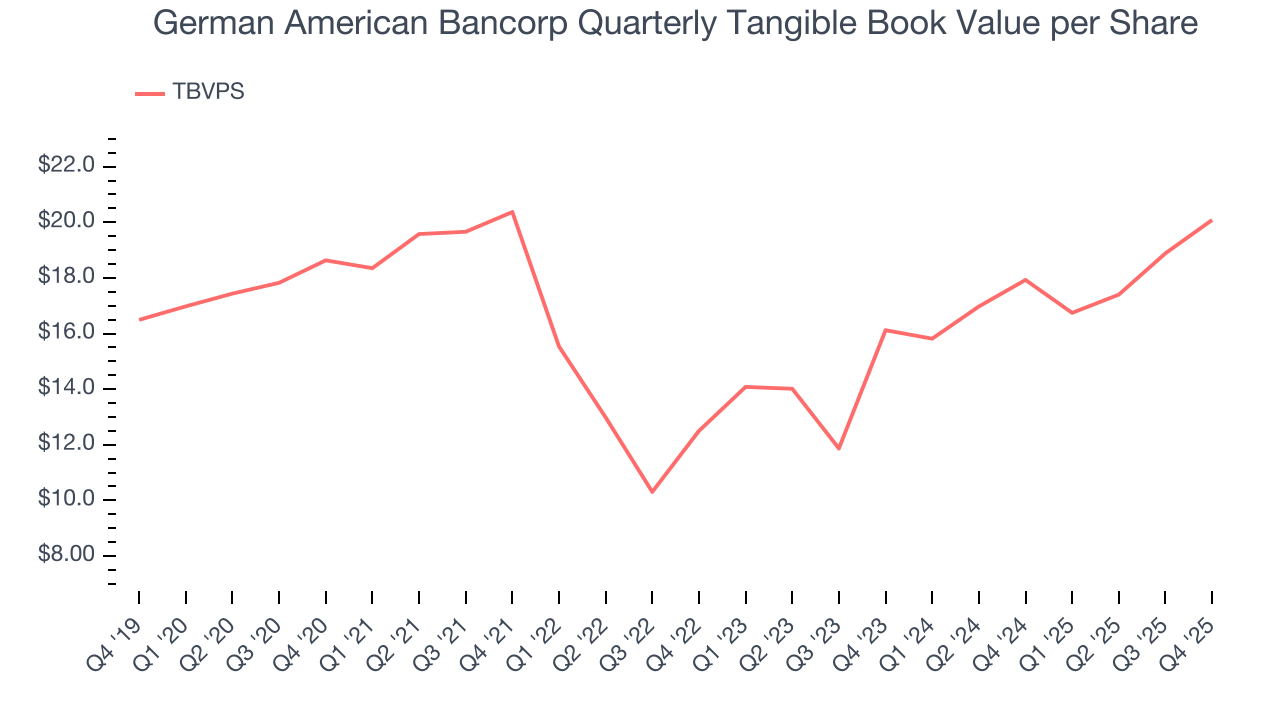

7. Tangible Book Value Per Share (TBVPS)

Banks profit by intermediating between depositors and borrowers, making them fundamentally balance sheet-driven enterprises. Market participants emphasize balance sheet quality and sustained book value growth when evaluating these institutions.

This is why we consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation. On the other hand, EPS is often distorted by mergers and flexible loan loss accounting. TBVPS provides clearer performance insights.

German American Bancorp’s TBVPS grew at a sluggish 1.5% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 11.6% annually over the last two years from $16.12 to $20.08 per share.

Over the next 12 months, Consensus estimates call for German American Bancorp’s TBVPS to grow by 14.8% to $23.06, decent growth rate.

8. Balance Sheet Assessment

Leverage is core to a financial firm’s business model (loans funded by deposits). To ensure economic stability and avoid a repeat of the 2008 GFC, regulators require certain levels of capital and liquidity, focusing on the Tier 1 capital ratio.

Tier 1 capital is the highest-quality capital that a firm holds, consisting primarily of common stock and retained earnings, but also physical gold. It serves as the primary cushion against losses and is the first line of defense in times of financial distress.

This capital is divided by risk-weighted assets to derive the Tier 1 capital ratio. Risk-weighted means that cash and US treasury securities are assigned little risk while unsecured consumer loans and equity investments get much higher risk weights, for example.

New regulation after the 2008 financial crisis requires that all firms must maintain a Tier 1 capital ratio greater than 4.5%. On top of this, there are additional buffers based on scale, risk profile, and other regulatory classifications, so that at the end of the day, firms generally must maintain a 7-10% ratio at minimum.

Over the last two years, German American Bancorp has averaged a Tier 1 capital ratio of 13.9%, which is considered safe and well capitalized in the event that macro or market conditions suddenly deteriorate.

9. Return on Equity

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, German American Bancorp has averaged an ROE of 13%, healthy for a company operating in a sector where the average shakes out around 7.5% and those putting up 15%+ are greatly admired. This shows German American Bancorp has a decent competitive moat.

10. Key Takeaways from German American Bancorp’s Q4 Results

We enjoyed seeing German American Bancorp beat analysts’ revenue expectations this quarter. We were also happy its tangible book value per share outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $43.19 immediately after reporting.

11. Is Now The Time To Buy German American Bancorp?

Updated: March 15, 2026 at 12:46 AM EDT

Before deciding whether to buy German American Bancorp or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

German American Bancorp isn’t a bad business, but we have other favorites. First off, its revenue growth was good over the last five years. And while German American Bancorp’s TBVPS growth was weak over the last five years, its expanding net interest margin shows its loan book is becoming more profitable.

German American Bancorp’s P/B ratio based on the next 12 months is 1.2x. This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $47.33 on the company (compared to the current share price of $40.03).