Hudson Technologies (HDSN)

We’re wary of Hudson Technologies. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Hudson Technologies Will Underperform

Founded in 1991, Hudson Technologies (NASDAQ:HDSN) specializes in refrigerant services and solutions, providing refrigerant sales, reclamation, and recycling.

- Sales are projected to be flat over the next 12 months and imply weak demand

- A silver lining is that its healthy operating margin shows it’s a well-run company with efficient processes

Hudson Technologies doesn’t fulfill our quality requirements. We believe there are better opportunities elsewhere.

Why There Are Better Opportunities Than Hudson Technologies

At $5.92 per share, Hudson Technologies trades at 14.6x forward P/E. Yes, this valuation multiple is lower than that of other industrials peers, but we’ll remind you that you often get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Hudson Technologies (HDSN) Research Report: Q4 CY2025 Update

Refrigerant services company Hudson Technologies (NASDAQ:HDSN) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 28.2% year on year to $44.41 million. Its GAAP loss of $0.20 per share was significantly below analysts’ consensus estimates.

Hudson Technologies (HDSN) Q4 CY2025 Highlights:

- Revenue: $44.41 million vs analyst estimates of $38.12 million (28.2% year-on-year growth, 16.5% beat)

- EPS (GAAP): -$0.20 vs analyst estimates of -$0.08 (significant miss)

- Operating Margin: -25.2%, down from -8.5% in the same quarter last year

- Free Cash Flow was -$33.65 million, down from $19.16 million in the same quarter last year

- Market Capitalization: $307 million

Company Overview

Founded in 1991, Hudson Technologies (NASDAQ:HDSN) specializes in refrigerant services and solutions, providing refrigerant sales, reclamation, and recycling.

The company addresses the need for responsible refrigerant management, including reclamation and recycling, to comply with regulatory standards and environmental safety. The company’s offerings have certainly been more top-of-mind for companies in the last decade as ESG efforts have ramped up.

Hudson Technologies' services include refrigerant sales, recovery, recycling, and reclamation. Its reclamation services purify refrigerants to industry specifications for air conditioning, refrigeration, and heating systems. A company might hire Hudson Technology to service HVAC systems in commercial buildings to ensure optimal and eco-friendly operation or provide refrigerant recovery services during system repairs or decommissioning.

Hudson Technologies generates revenue from selling reclaimed and virgin refrigerants and providing associated services to clients. Sales are conducted through direct distribution channels and partner networks. The business model encompasses fixed costs related to facilities and equipment maintenance, and variable costs driven by the volume of refrigerants processed. While some aspects of revenue are project-based, recurring revenue streams are established through ongoing service contracts and the sale of refrigerants to regular customers.

4. Specialty Equipment Distributors

Historically, specialty equipment distributors have boasted deep selection and expertise in sometimes narrow areas like single-use packaging or unique lighting equipment. Additionally, the industry has evolved to include more automated industrial equipment and machinery over the last decade, driving efficiencies and enabling valuable data collection. Specialty equipment distributors whose offerings keep up with these trends can take share in a still-fragmented market, but like the broader industrials sector, this space is at the whim of economic cycles that impact the capital spending and manufacturing propelling industry volumes.

Competitors in the refrigerant services and solutions industry include Arkema (OTC:ARKAY), The Chemours Company (NYSE:CC), and Honeywell International (NASDAQ:HON).

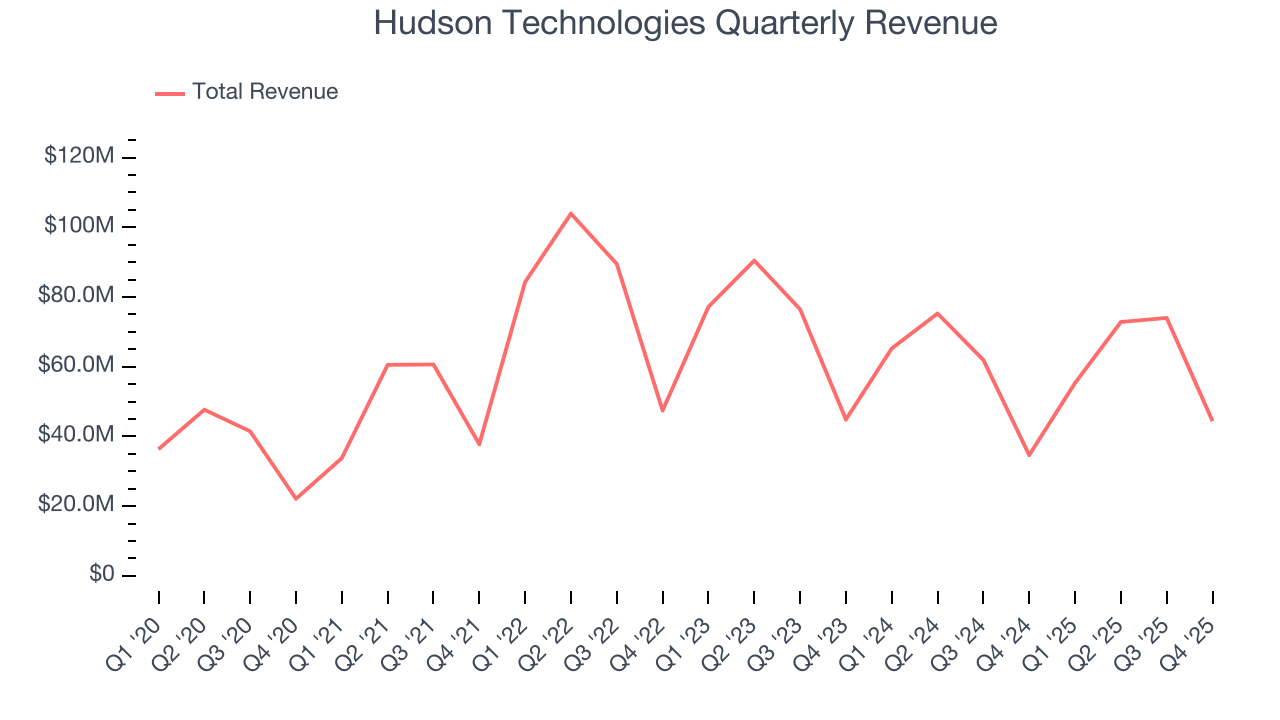

5. Revenue Growth

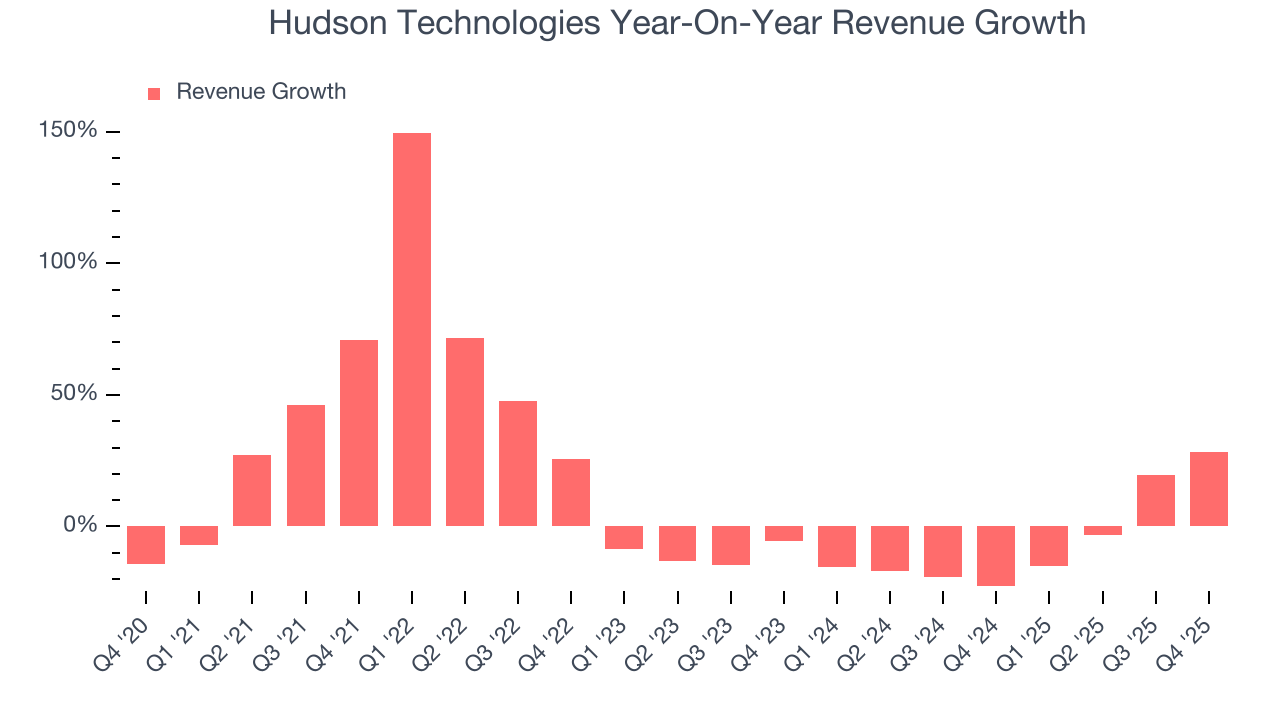

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Hudson Technologies’s sales grew at an impressive 10.8% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Hudson Technologies’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 7.6% over the last two years.

This quarter, Hudson Technologies reported robust year-on-year revenue growth of 28.2%, and its $44.41 million of revenue topped Wall Street estimates by 16.5%.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

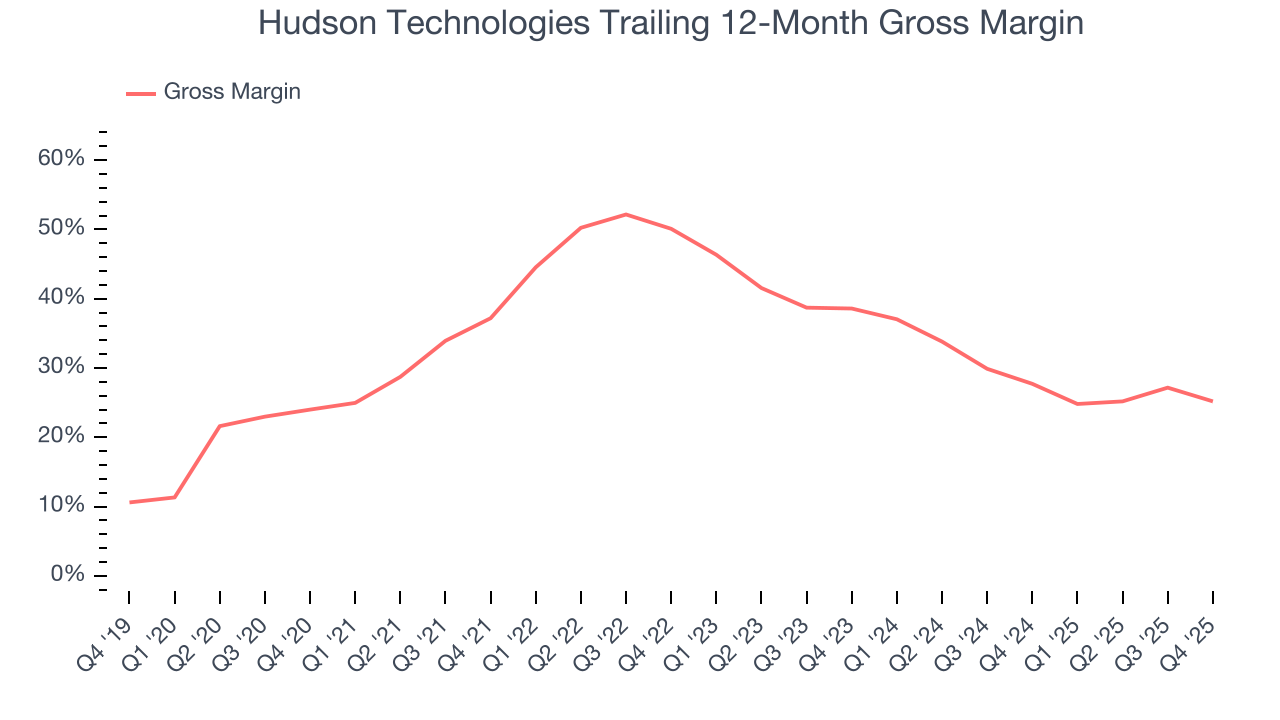

6. Gross Margin & Pricing Power

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Hudson Technologies’s unit economics are great compared to the broader industrials sector and signal that it enjoys product differentiation through quality or brand. As you can see below, it averaged an excellent 36.7% gross margin over the last five years. That means Hudson Technologies only paid its suppliers $63.29 for every $100 in revenue.

Hudson Technologies produced a 8% gross profit margin in Q4, down 8.7 percentage points year on year. Hudson Technologies’s full-year margin has also been trending down over the past 12 months, decreasing by 2.5 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

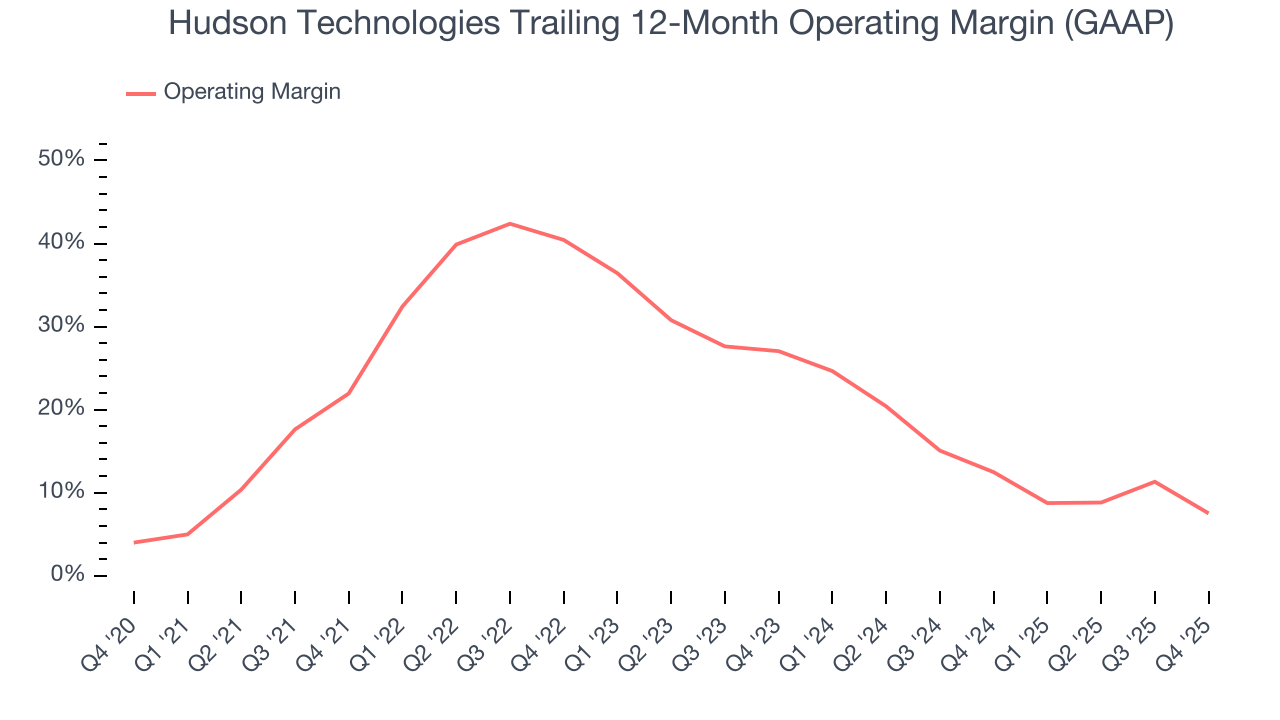

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Hudson Technologies has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 23.3%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Hudson Technologies’s operating margin decreased by 14.4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Hudson Technologies generated an operating margin profit margin of negative 25.2%, down 16.7 percentage points year on year. Since Hudson Technologies’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

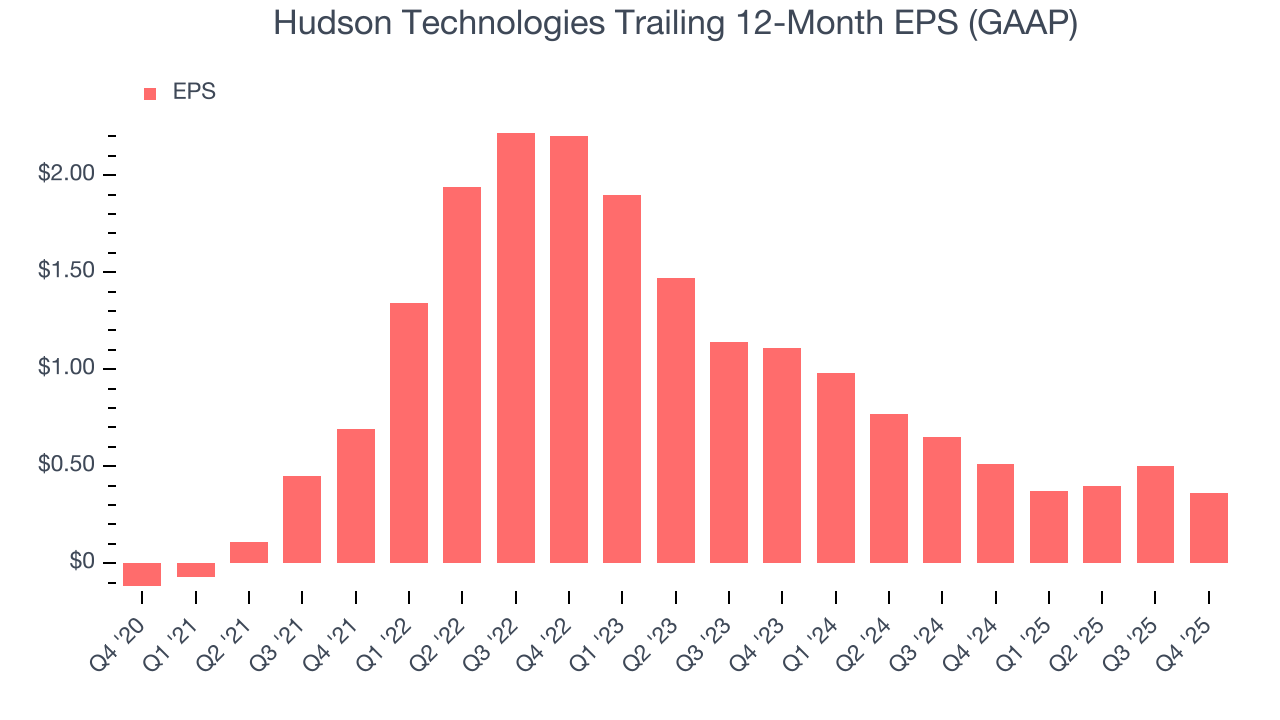

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Hudson Technologies’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Hudson Technologies, its EPS declined by more than its revenue over the last two years, dropping 43.1%. This tells us the company struggled to adjust to shrinking demand.

We can take a deeper look into Hudson Technologies’s earnings to better understand the drivers of its performance. Hudson Technologies’s operating margin has declined over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Hudson Technologies reported EPS of negative $0.20, down from negative $0.06 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Hudson Technologies’s full-year EPS of $0.36 to grow 30.6%.

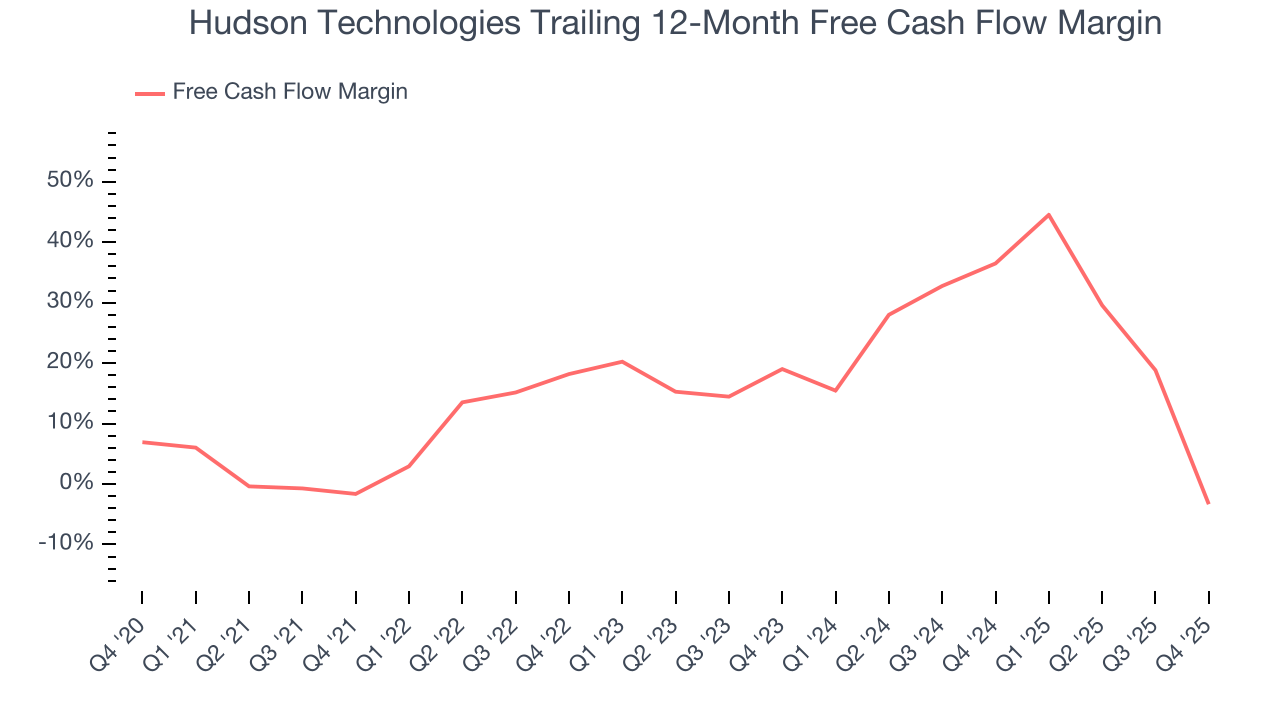

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Hudson Technologies has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 14.7% over the last five years. Hudson Technologies has shown terrific cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders.

Taking a step back, we can see that Hudson Technologies’s margin dropped by 1.7 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

Hudson Technologies burned through $33.65 million of cash in Q4, equivalent to a negative 75.8% margin. The company’s cash flow turned negative after being positive in the same quarter last year, suggesting its historical struggles have dragged on.

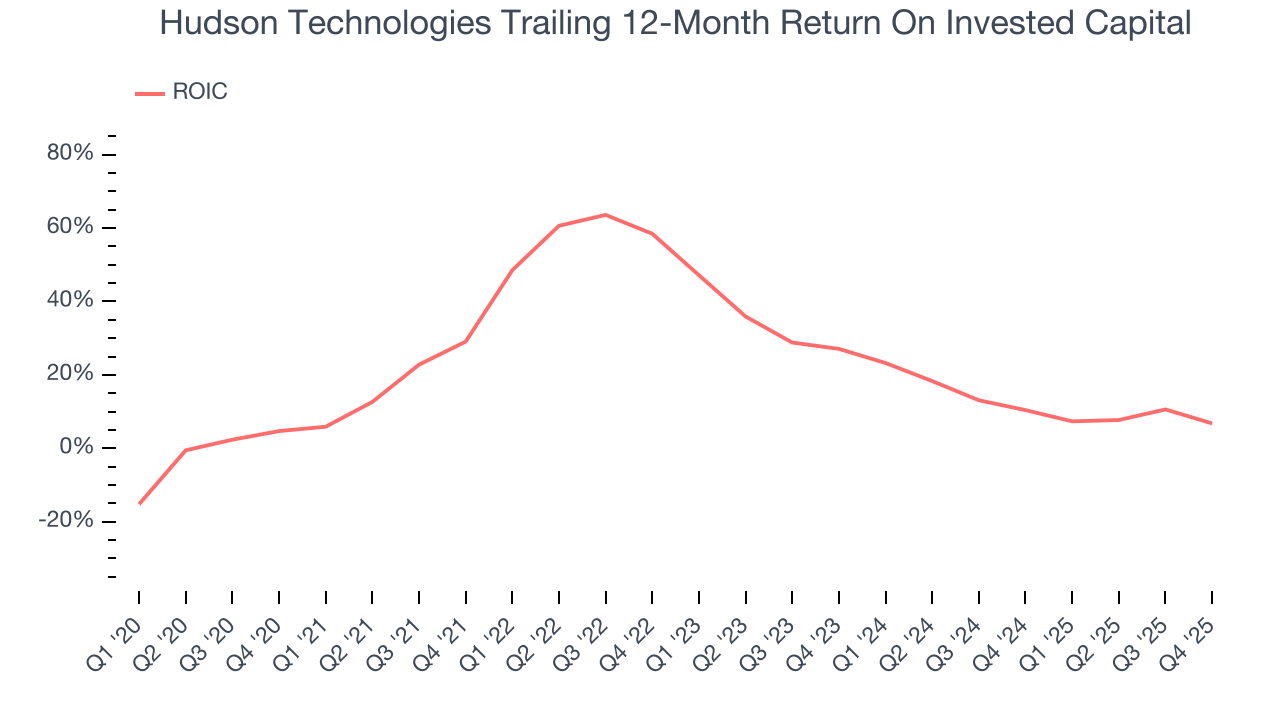

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Hudson Technologies hasn’t been the highest-quality company lately, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 26.4%, splendid for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Hudson Technologies’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

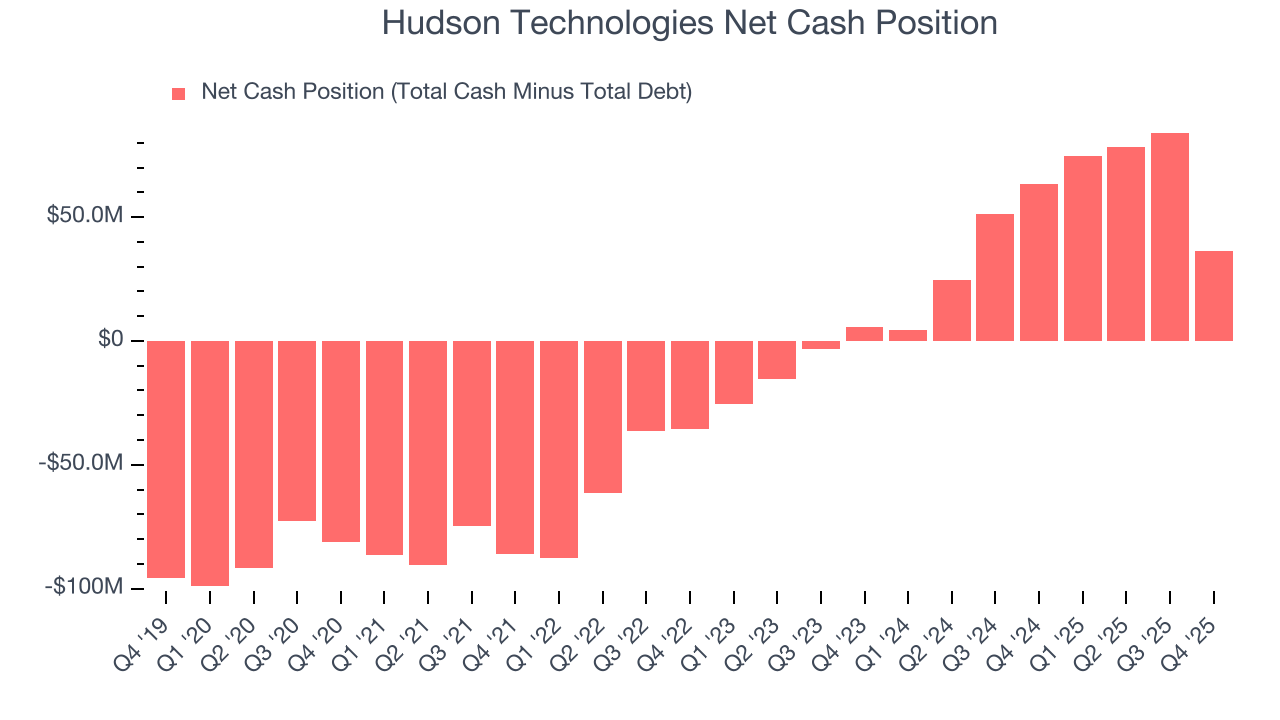

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Hudson Technologies is a well-capitalized company with $39.46 million of cash and $3.23 million of debt on its balance sheet. This $36.22 million net cash position is 13.7% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Hudson Technologies’s Q4 Results

We were impressed by how significantly Hudson Technologies blew past analysts’ revenue expectations this quarter. On the other hand, its EPS missed. Overall, this was a weaker quarter. The stock traded down 2.6% to $6.90 immediately following the results.

13. Is Now The Time To Buy Hudson Technologies?

Updated: March 18, 2026 at 11:12 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Hudson Technologies.

Hudson Technologies isn’t a terrible business, but it doesn’t pass our bar. Although its revenue growth was impressive over the last five years, it’s expected to deteriorate over the next 12 months and its diminishing returns show management's prior bets haven't worked out. And while the company’s impressive operating margins show it has a highly efficient business model, the downside is its projected EPS for the next year is lacking.

Hudson Technologies’s P/E ratio based on the next 12 months is 14.9x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $9 on the company (compared to the current share price of $5.98).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.