Karat Packaging (KRT)

We aren’t fans of Karat Packaging. Its growth has decelerated and its failure to generate meaningful free cash flow makes us question its prospects.― StockStory Analyst Team

1. News

2. Summary

Why Karat Packaging Is Not Exciting

Founded as Lollicup, Karat Packaging (NASDAQ: KRT) distributes and manufactures environmentally-friendly disposable foodservice packaging solutions.

- Poor free cash flow generation means it has few chances to reinvest for growth, repurchase shares, or distribute capital

- Sales trends were unexciting over the last two years as its 7.4% annual growth was below the typical industrials company

- A positive is that its stellar returns on capital showcase management’s ability to surface highly profitable business ventures, and its rising returns show it’s making even more lucrative bets

Karat Packaging doesn’t pass our quality test. There are more promising prospects in the market.

Why There Are Better Opportunities Than Karat Packaging

Karat Packaging’s stock price of $26.66 implies a valuation ratio of 11x forward P/E. Yes, this valuation multiple is lower than that of other industrials peers, but we’ll remind you that you often get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Karat Packaging (KRT) Research Report: Q4 CY2025 Update

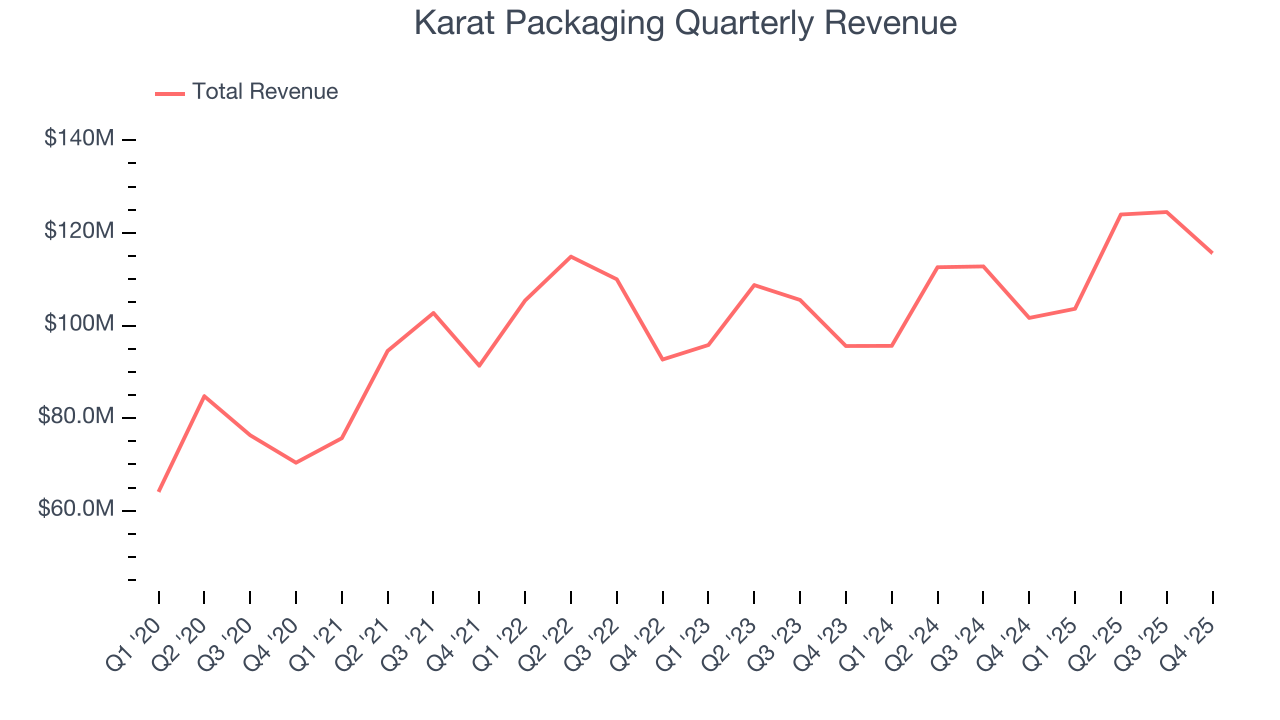

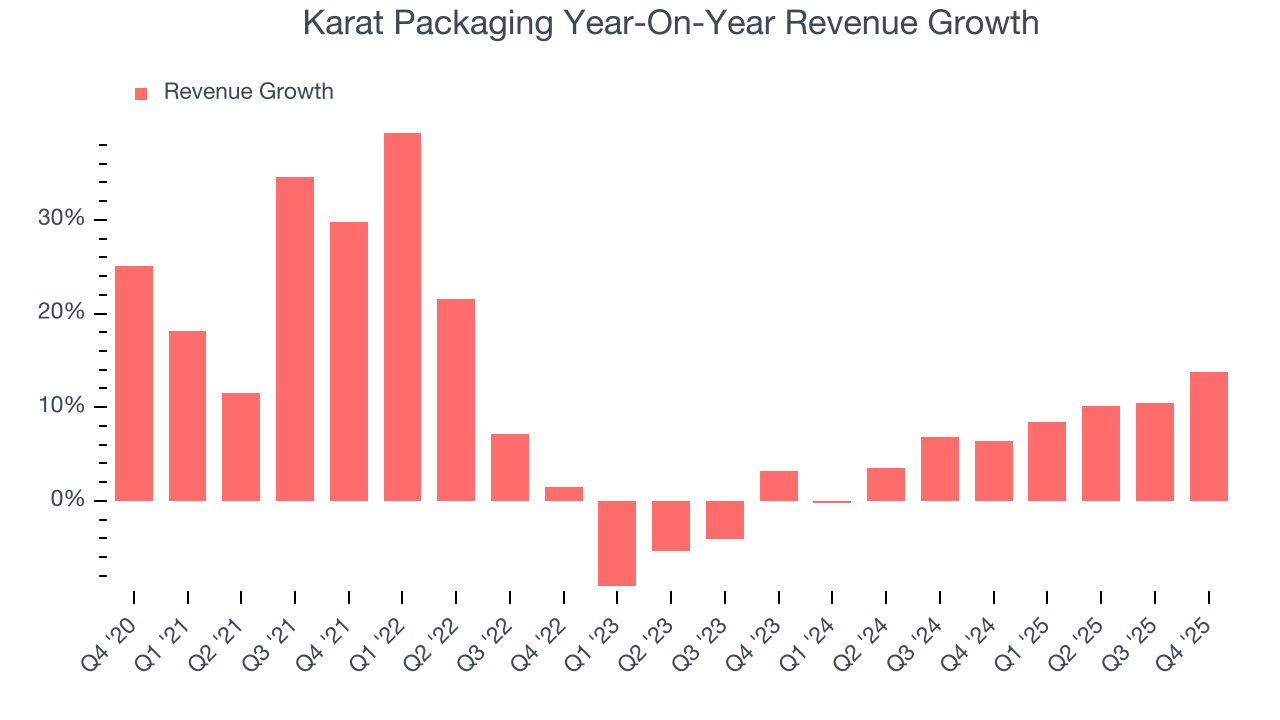

Foodservice packaging supplier Karat Packaging (NASDAQ:KRT) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 13.7% year on year to $115.6 million. On the other hand, next quarter’s revenue guidance of $113 million was less impressive, coming in 2.6% below analysts’ estimates. Its non-GAAP profit of $0.34 per share was 21.4% above analysts’ consensus estimates.

Karat Packaging (KRT) Q4 CY2025 Highlights:

- Revenue: $115.6 million vs analyst estimates of $113.9 million (13.7% year-on-year growth, 1.5% beat)

- Adjusted EPS: $0.34 vs analyst estimates of $0.28 (21.4% beat)

- Adjusted EBITDA: $12.5 million vs analyst estimates of $10.4 million (10.8% margin, 20.2% beat)

- Revenue Guidance for Q1 CY2026 is $113 million at the midpoint, below analyst estimates of $116 million

- Operating Margin: 7.3%, in line with the same quarter last year

- Market Capitalization: $458.7 million

Company Overview

Founded as Lollicup, Karat Packaging (NASDAQ: KRT) distributes and manufactures environmentally-friendly disposable foodservice packaging solutions.

The company's product offerings span several brands tailored to specific market needs. Karat, the primary brand, offers a wide array of disposable products ranging from cups to containers. Karat Earth extends this range with eco-friendly options, promoting sustainability with biodegradable and compostable products. Additionally, Tea Zone caters to the bubble tea market with a selection of high-quality teas and syrups, while Total Clean provides a variety of janitorial products.

Karat Packaging generates revenue by selling these products to food service operators, distributors, and large restaurant chains throughout the United States. The business model capitalizes on recurring revenue streams from ongoing supply agreements, supported by a cost structure that balances fixed manufacturing investments with variable costs linked to materials and distribution. This strategy not only meets market demand for disposable solutions but also aligns with increasing environmental awareness among consumers.

4. Specialty Equipment Distributors

Historically, specialty equipment distributors have boasted deep selection and expertise in sometimes narrow areas like single-use packaging or unique lighting equipment. Additionally, the industry has evolved to include more automated industrial equipment and machinery over the last decade, driving efficiencies and enabling valuable data collection. Specialty equipment distributors whose offerings keep up with these trends can take share in a still-fragmented market, but like the broader industrials sector, this space is at the whim of economic cycles that impact the capital spending and manufacturing propelling industry volumes.

A public competitor in the disposable foodservice products sector is Pactiv Evergreen (NASDAQ:PTVE) while two prominent private competitors are Dart Container and WinCup.

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Karat Packaging grew its sales at a solid 9.6% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Karat Packaging’s recent performance shows its demand has slowed as its annualized revenue growth of 7.4% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Karat Packaging reported year-on-year revenue growth of 13.7%, and its $115.6 million of revenue exceeded Wall Street’s estimates by 1.5%. Company management is currently guiding for a 9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 11.5% over the next 12 months, an improvement versus the last two years. This projection is admirable and indicates its newer products and services will spur better top-line performance.

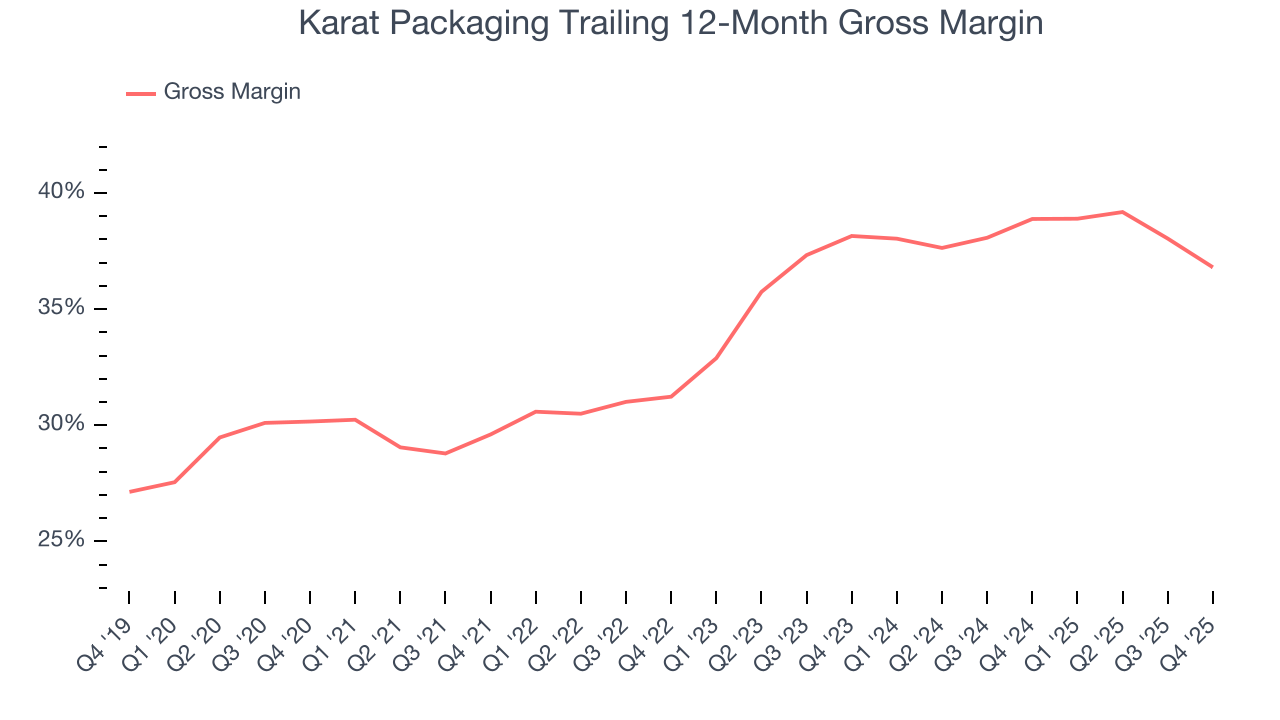

6. Gross Margin & Pricing Power

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

Karat Packaging’s gross margin is good compared to other industrials businesses and signals it sells differentiated products, not commodities. As you can see below, it averaged an impressive 35.1% gross margin over the last five years. Said differently, Karat Packaging paid its suppliers $64.90 for every $100 in revenue.

In Q4, Karat Packaging produced a 34% gross profit margin , marking a 5.1 percentage point decrease from 39.2% in the same quarter last year. Karat Packaging’s full-year margin has also been trending down over the past 12 months, decreasing by 2.1 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

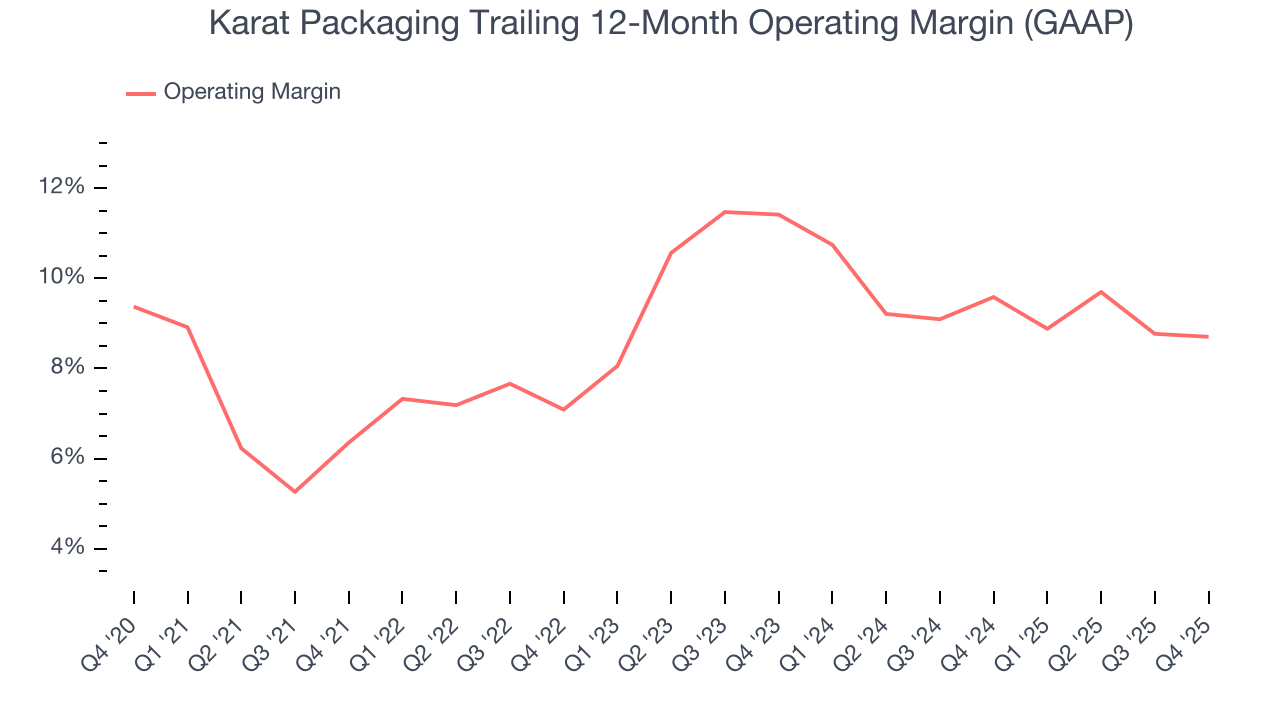

7. Operating Margin

Karat Packaging has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.7%, higher than the broader industrials sector.

Looking at the trend in its profitability, Karat Packaging’s operating margin rose by 2.3 percentage points over the last five years, as its sales growth gave it operating leverage. Its expansion was impressive, especially when considering most Specialty Equipment Distributors peers saw their margins plummet.

This quarter, Karat Packaging generated an operating margin profit margin of 7.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

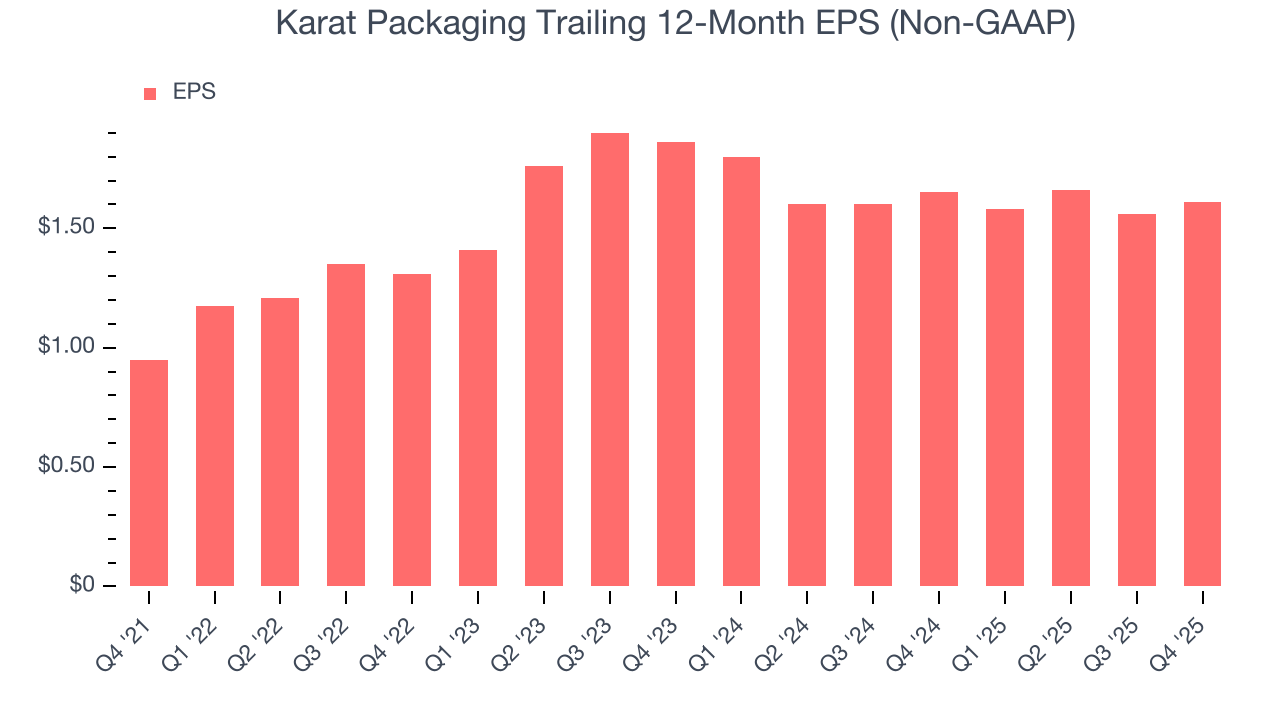

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Karat Packaging’s full-year EPS grew at a remarkable 14.1% compounded annual growth rate over the last four years, better than the broader industrials sector.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Karat Packaging, its EPS declined by 7% annually over the last two years while its revenue grew by 7.4%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Karat Packaging reported adjusted EPS of $0.34, up from $0.29 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Karat Packaging’s full-year EPS of $1.61 to grow 3.1%.

9. Cash Is King

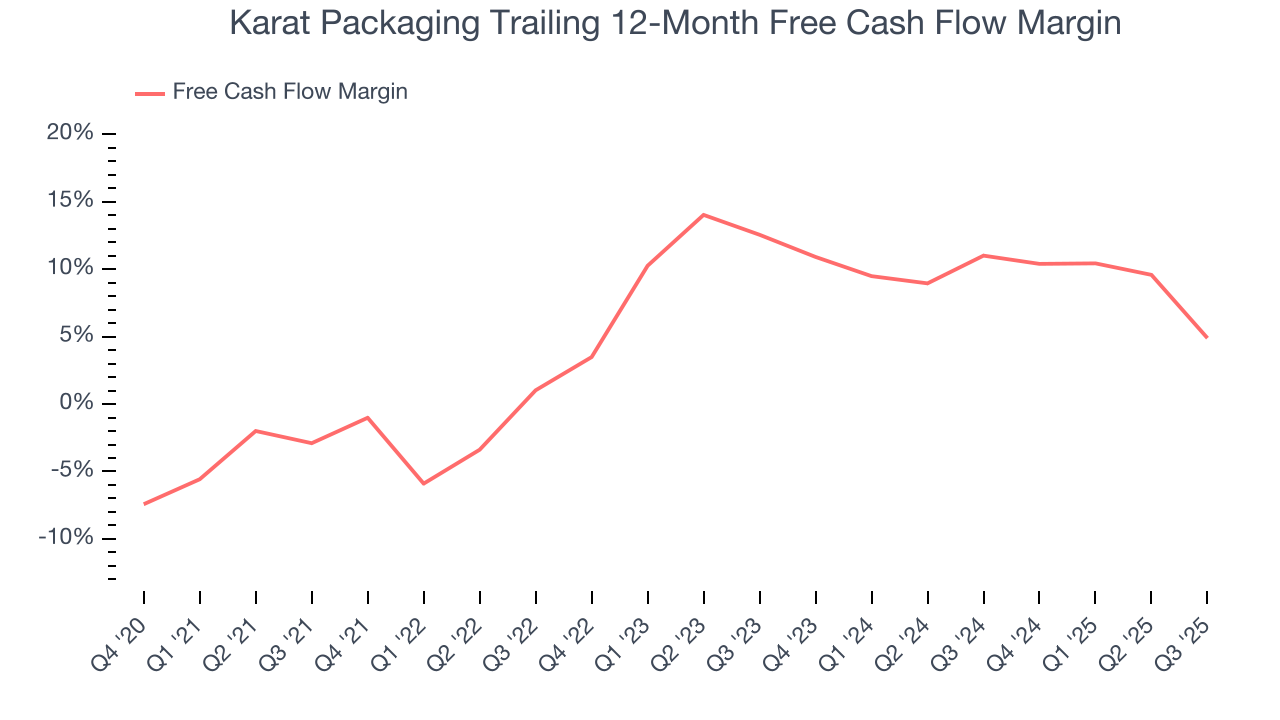

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Karat Packaging has shown mediocre cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 5.8%, below what we’d expect for an industrials business.

Taking a step back, an encouraging sign is that Karat Packaging’s margin expanded by 7.5 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

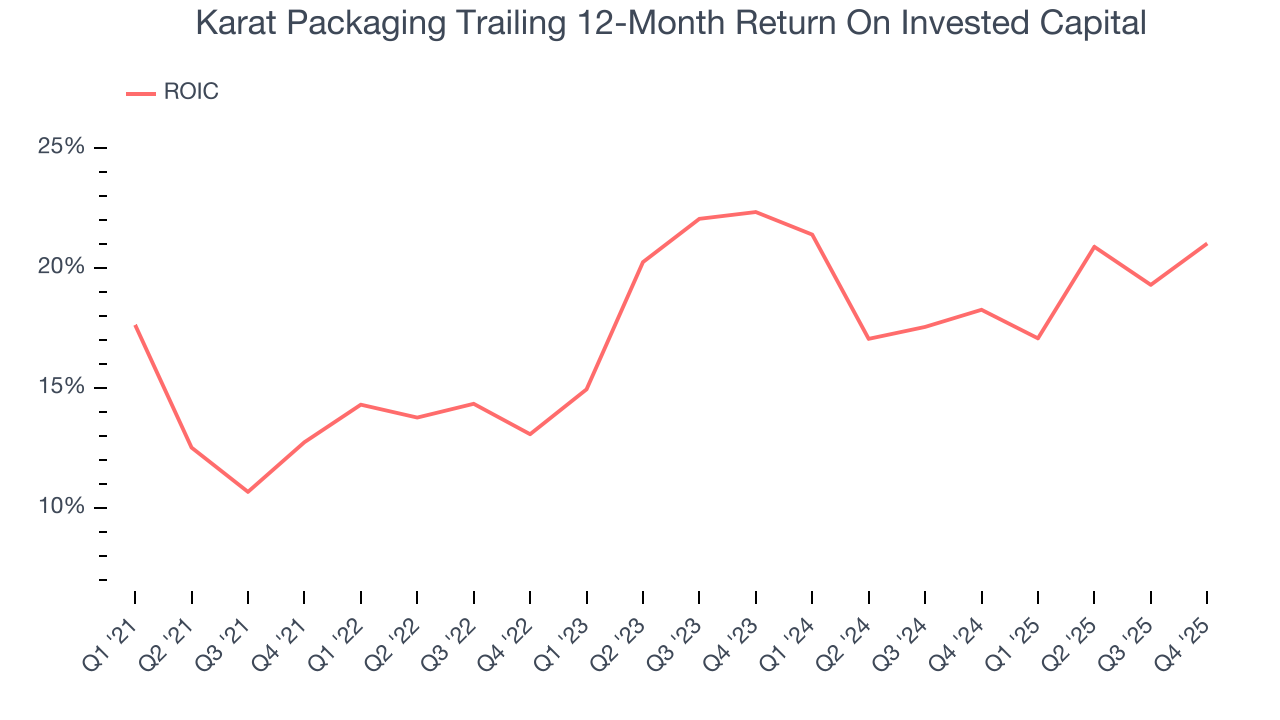

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Karat Packaging hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked out well. Its five-year average ROIC was 17.5%, impressive for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Karat Packaging’s ROIC has increased over the last few years. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

11. Key Takeaways from Karat Packaging’s Q4 Results

We were impressed by how significantly Karat Packaging blew past analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 3.6% to $23.10 immediately following the results.

12. Is Now The Time To Buy Karat Packaging?

Updated: March 14, 2026 at 11:14 PM EDT

Before investing in or passing on Karat Packaging, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Karat Packaging has a few positive attributes, but it doesn’t top our wishlist. First off, its revenue growth was solid over the last five years and is expected to accelerate over the next 12 months. On top of that, Karat Packaging’s rising cash profitability gives it more optionality, and its projected EPS for the next year implies the company’s fundamentals will improve.

Karat Packaging’s P/E ratio based on the next 12 months is 11x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $29.50 on the company (compared to the current share price of $26.66).