ICF International (ICFI)

ICF International faces an uphill battle. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think ICF International Will Underperform

Operating at the intersection of policy, technology, and implementation for over five decades, ICF International (NASDAQ:ICFI) provides professional consulting services and technology solutions to government agencies and commercial clients across energy, health, environment, and security sectors.

- Annual sales declines of 2.3% for the past two years show its products and services struggled to connect with the market during this cycle

- Demand cratered as it couldn’t win new orders over the past two years, leading to an average 7.4% decline in its backlog

- Earnings per share lagged its peers over the last two years as they only grew by 2% annually

ICF International falls short of our expectations. We see more lucrative opportunities elsewhere.

Why There Are Better Opportunities Than ICF International

ICF International’s stock price of $67.60 implies a valuation ratio of 9.8x forward P/E. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. ICF International (ICFI) Research Report: Q4 CY2025 Update

Professional consulting firm ICF International (NASDAQ:ICFI) reported Q4 CY2025 results exceeding the market’s revenue expectations, but sales fell by 10.6% year on year to $443.7 million. The company expects the full year’s revenue to be around $1.93 billion, close to analysts’ estimates. Its non-GAAP profit of $1.47 per share was 1.5% below analysts’ consensus estimates.

ICF International (ICFI) Q4 CY2025 Highlights:

- Revenue: $443.7 million vs analyst estimates of $439.5 million (10.6% year-on-year decline, 1% beat)

- Adjusted EPS: $1.47 vs analyst expectations of $1.49 (1.5% miss)

- Adjusted EBITDA: $45.96 million vs analyst estimates of $48.12 million (10.4% margin, 4.5% miss)

- Adjusted EPS guidance for the upcoming financial year 2026 is $7.10 at the midpoint

- Operating Margin: 6.5%, in line with the same quarter last year

- Free Cash Flow Margin: 15.5%, down from 18% in the same quarter last year

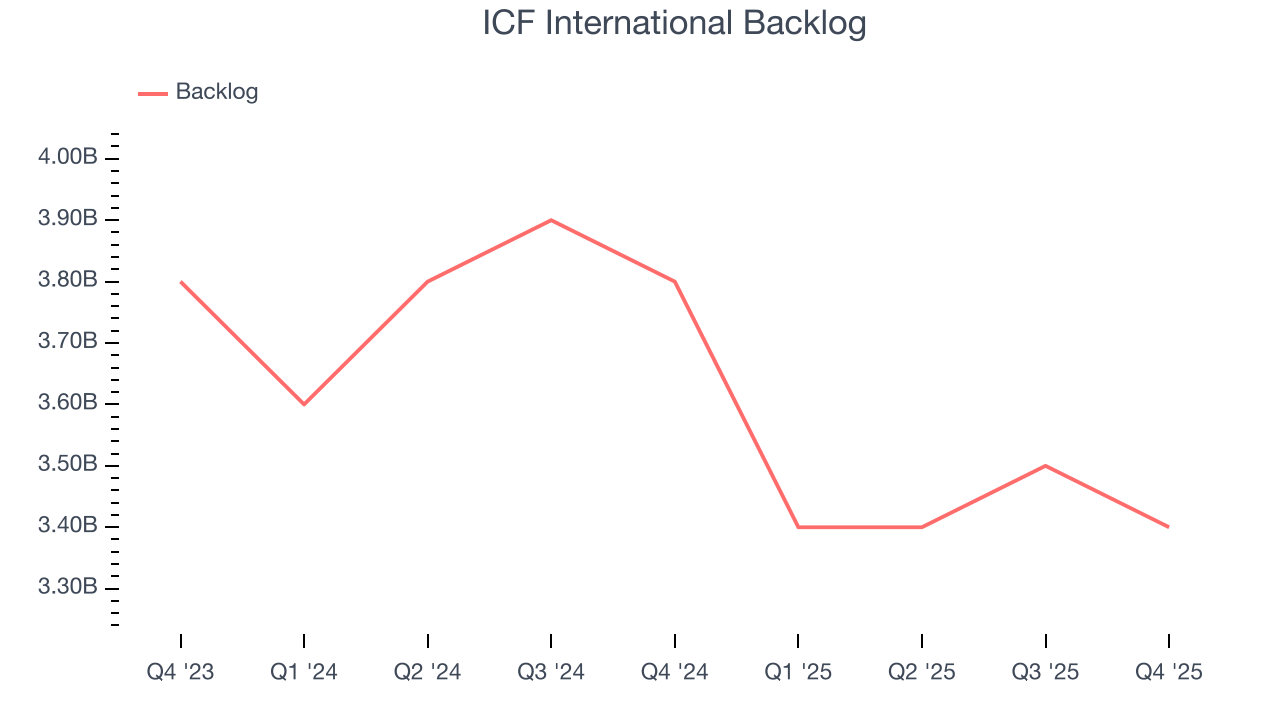

- Backlog: $3.4 billion at quarter end, down 10.5% year on year

- Market Capitalization: $1.39 billion

Company Overview

Operating at the intersection of policy, technology, and implementation for over five decades, ICF International (NASDAQ:ICFI) provides professional consulting services and technology solutions to government agencies and commercial clients across energy, health, environment, and security sectors.

ICF's services span five core areas: advisory services, program implementation, analytics, digital solutions, and engagement services. The company helps clients navigate complex challenges by combining subject matter expertise with technical capabilities to deliver practical solutions.

In the energy sector, ICF assists utilities and government agencies with power market analysis, grid modernization, renewable energy implementation, and energy efficiency programs. For example, a utility might engage ICF to design and implement residential demand-side management programs that reduce peak electricity usage while helping consumers lower their bills.

Environmental work includes impact assessments, compliance programs, and disaster recovery services. Following major hurricanes like Maria or Ian, ICF helps affected communities rebuild by managing recovery funds, designing resilient infrastructure, and implementing housing assistance programs.

In health and social programs, ICF supports agencies like the Centers for Disease Control and Prevention (CDC) and the National Institutes of Health (NIH) with program evaluation, data collection, and technical assistance. The company might help design public health campaigns, manage healthcare quality initiatives, or evaluate the effectiveness of social welfare programs.

ICF generates revenue through consulting contracts, typically ranging from one month to five years. Government clients represent approximately three-quarters of ICF's business, including U.S. federal agencies, state and local governments, and international bodies like the European Commission. Commercial clients, including corporations and non-profit organizations, make up the remaining quarter.

The company maintains a global footprint with headquarters in the Washington, D.C. area, 55 regional offices throughout the United States, and 15 international locations in countries including the United Kingdom, Belgium, India, and Canada. This geographic diversity allows ICF to serve clients worldwide while maintaining local expertise in key markets.

4. Government & Technical Consulting

The sector has historically benefitted from steady government spending on defense, infrastructure, and regulatory compliance, providing firms long-term contract stability. However, the Trump administration is showing more willingness than previous administrations to upend government spending and bloat. Whether or not defense budgets get cut, the rising demand for cybersecurity, AI-driven defense solutions, and sustainability consulting should benefit the sector for years, as agencies and enterprises seek expertise in navigating complex technology and regulations. Additionally, industrial automation and digital engineering are driving efficiency gains in infrastructure and technical consulting projects, which could help profit margins.

ICF International competes with large consulting firms like Accenture, Deloitte, and Booz Allen Hamilton, as well as specialized government contractors such as CACI International, Leidos Holdings, and Science Applications International Corporation (SAIC). In the energy and environmental space, competitors include Tetra Tech and AECOM.

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

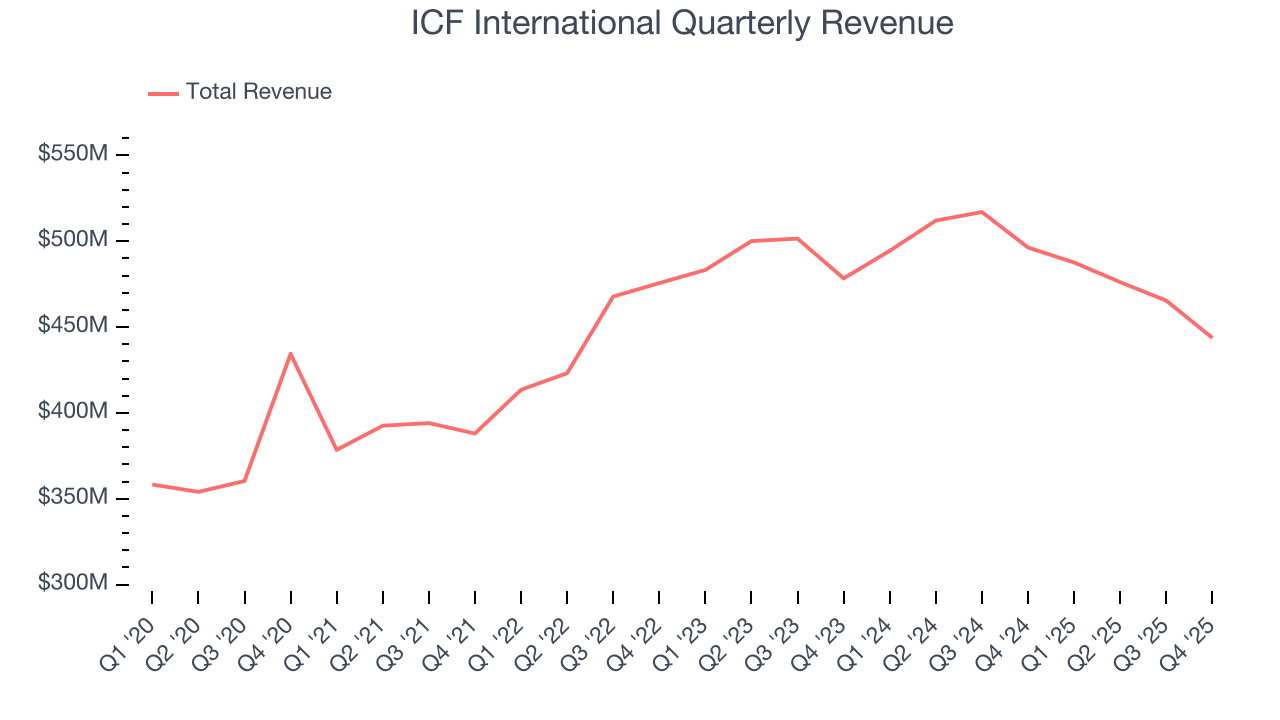

With $1.87 billion in revenue over the past 12 months, ICF International is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

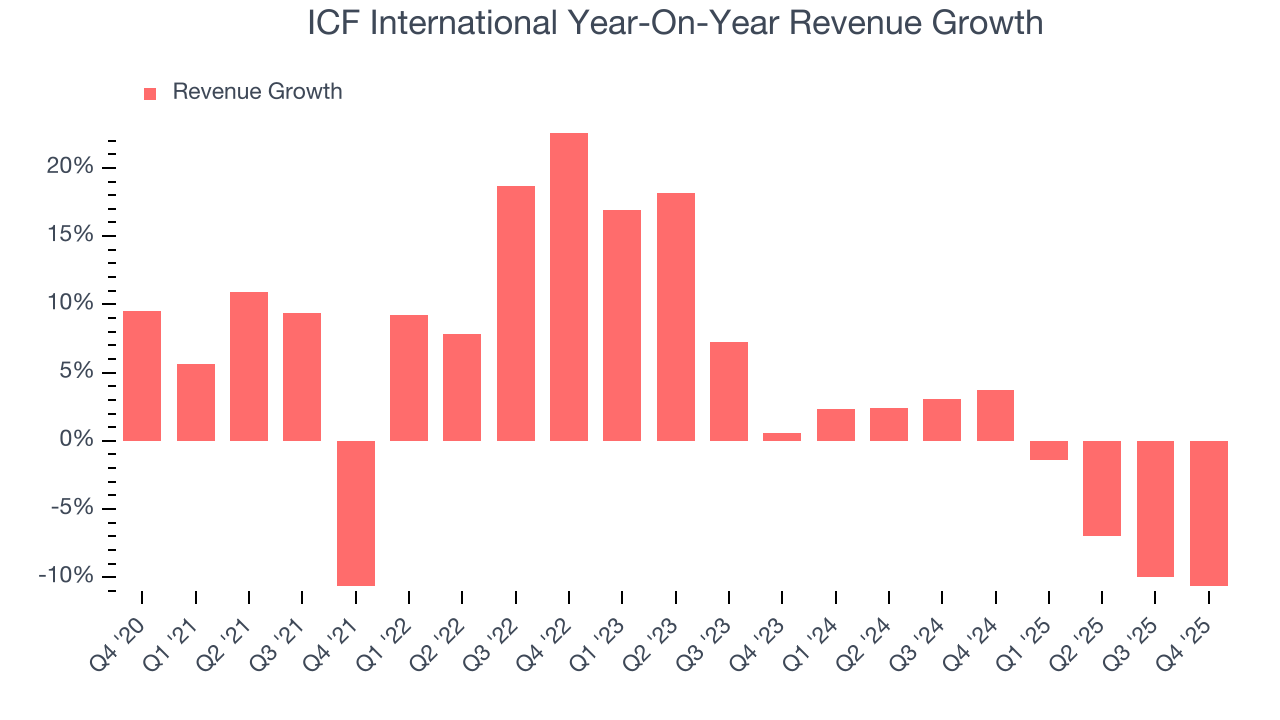

As you can see below, ICF International grew its sales at a mediocre 4.4% compounded annual growth rate over the last five years. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. ICF International’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 2.3% annually.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. ICF International’s backlog reached $3.4 billion in the latest quarter and averaged 7.4% year-on-year declines over the last two years. Because this number is lower than its revenue growth, we can see the company hasn’t secured enough new orders to maintain its growth rate in the future.

This quarter, ICF International’s revenue fell by 10.6% year on year to $443.7 million but beat Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 2.2% over the next 12 months. Although this projection implies its newer products and services will fuel better top-line performance, it is still below the sector average.

6. Operating Margin

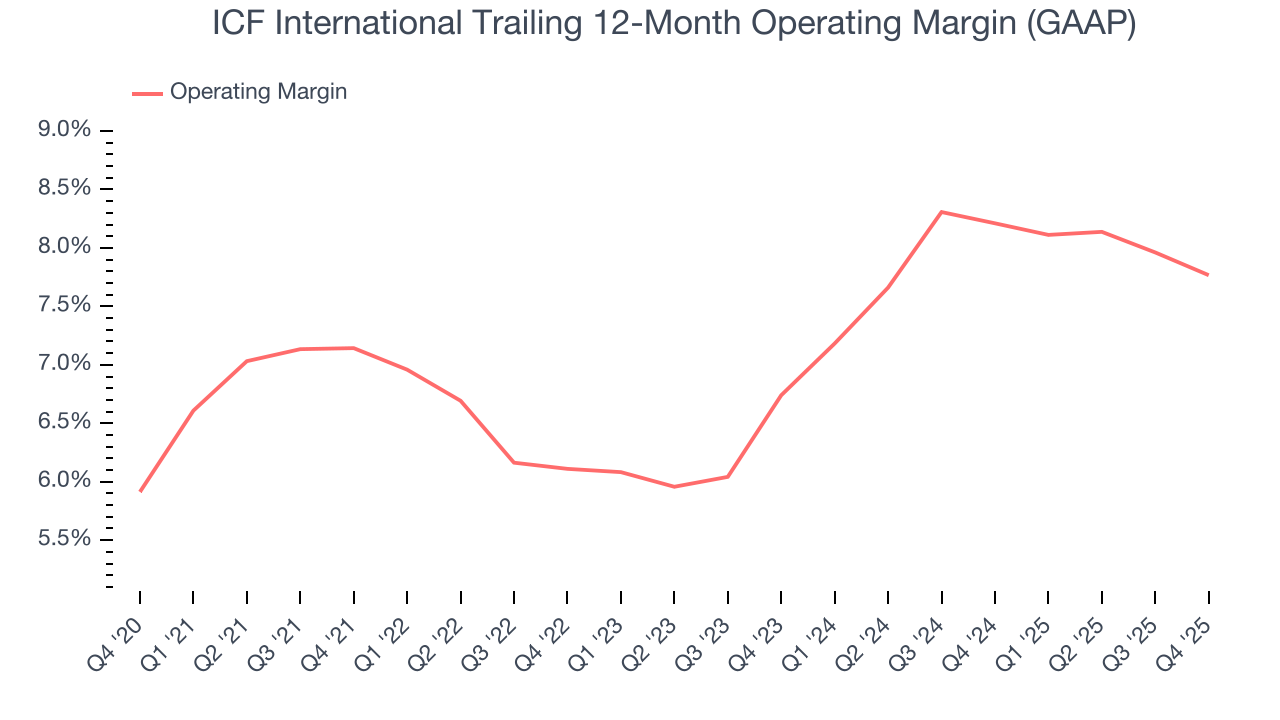

ICF International’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 7.2% over the last five years. This profitability was paltry for a business services business and caused by its suboptimal cost structure.

Looking at the trend in its profitability, ICF International’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, ICF International generated an operating margin profit margin of 6.5%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

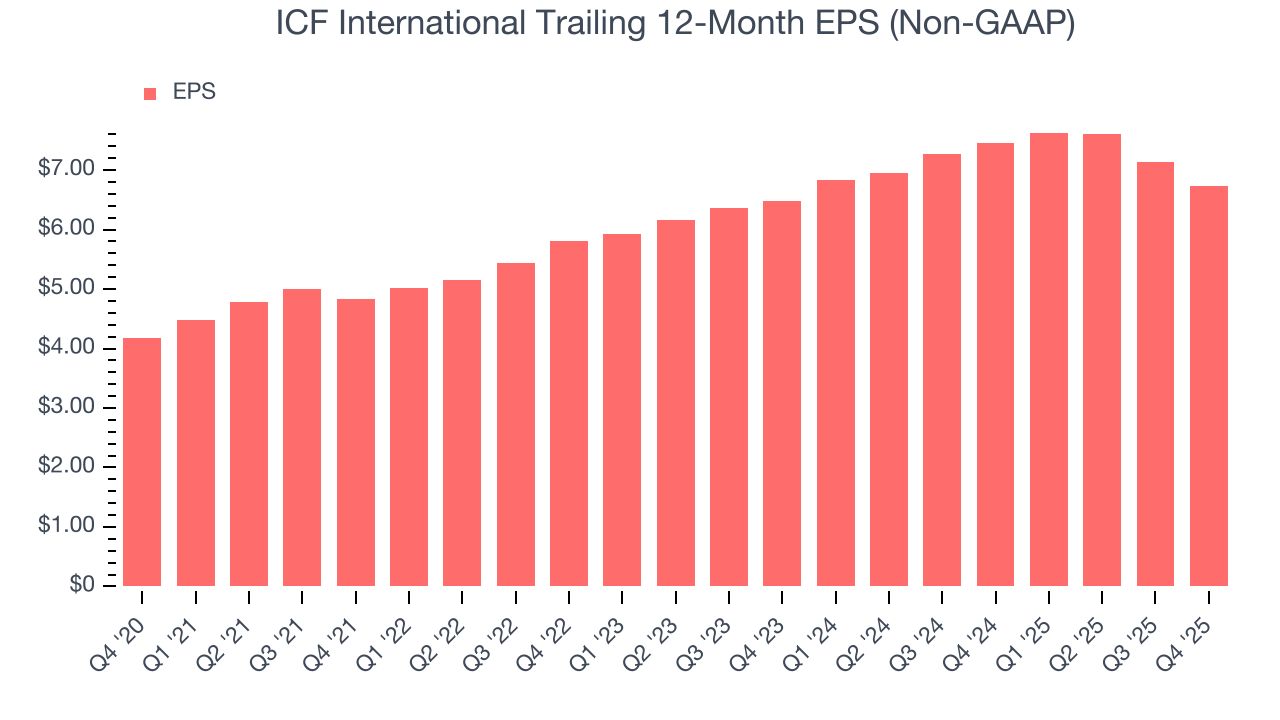

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

ICF International’s EPS grew at a solid 10% compounded annual growth rate over the last five years, higher than its 4.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For ICF International, its two-year annual EPS growth of 2% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q4, ICF International reported adjusted EPS of $1.47, down from $1.87 in the same quarter last year. This print slightly missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects ICF International’s full-year EPS of $6.74 to grow 5.6%.

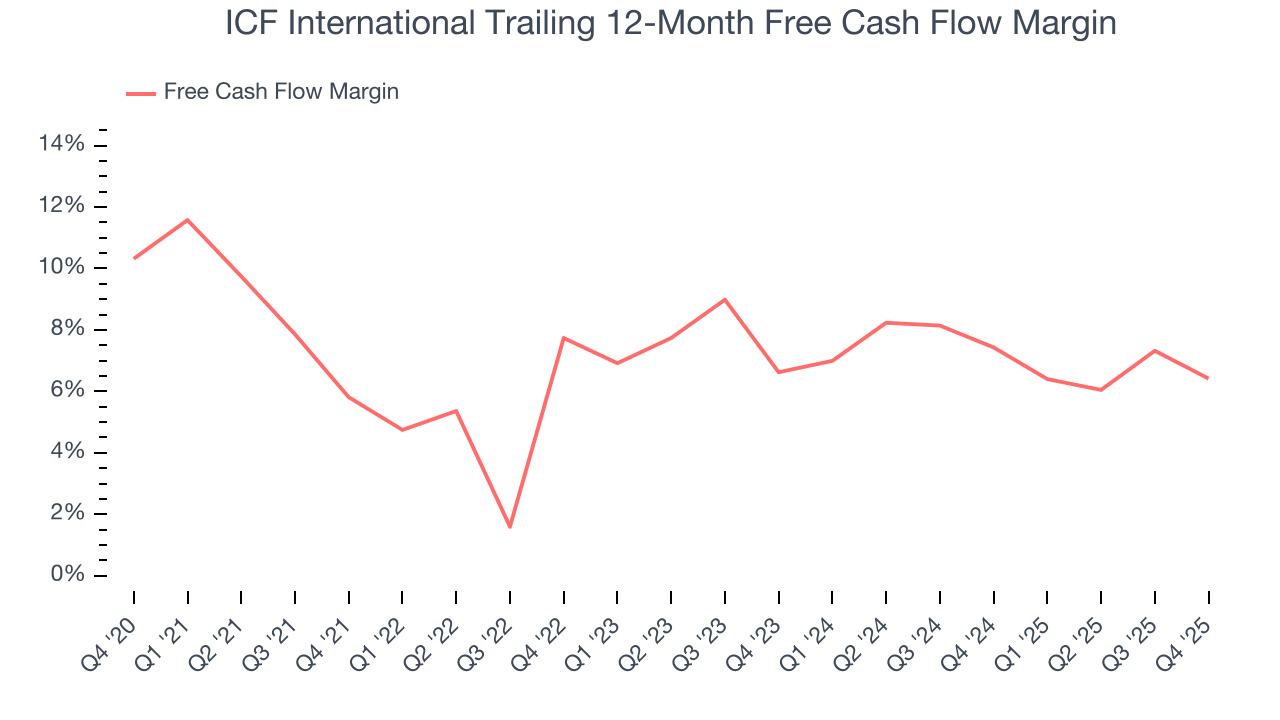

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

ICF International has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.8% over the last five years, slightly better than the broader business services sector.

ICF International’s free cash flow clocked in at $68.71 million in Q4, equivalent to a 15.5% margin. The company’s cash profitability regressed as it was 2.5 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

ICF International historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.1%, somewhat low compared to the best business services companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, ICF International’s ROIC increased by 2.3 percentage points annually each year over the last few years. This is a good sign, and we hope the company can continue improving.

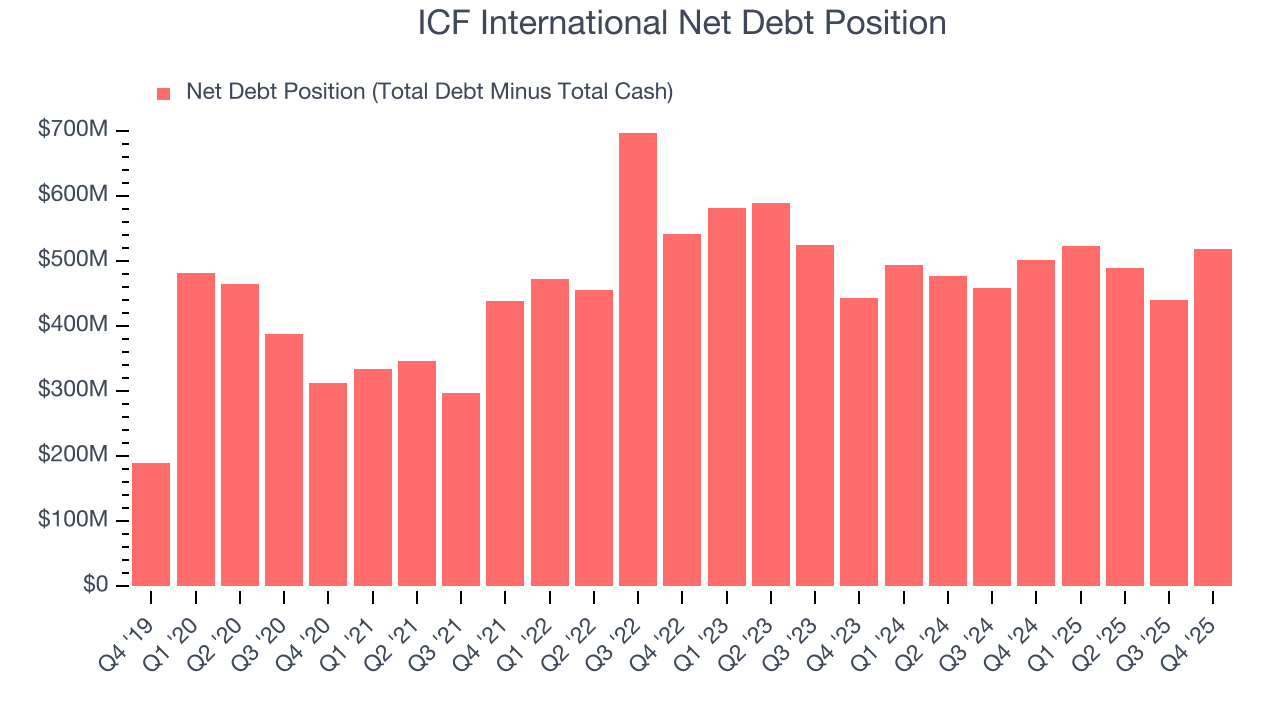

10. Balance Sheet Assessment

ICF International reported $53.28 million of cash and $571.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $207.2 million of EBITDA over the last 12 months, we view ICF International’s 2.5× net-debt-to-EBITDA ratio as safe. We also see its $30.83 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from ICF International’s Q4 Results

It was good to see ICF International narrowly top analysts’ revenue expectations this quarter. On the other hand, its EPS slightly missed. Overall, this quarter could have been better. The stock remained flat at $79.58 immediately after reporting.

12. Is Now The Time To Buy ICF International?

Updated: March 17, 2026 at 11:08 PM EDT

Are you wondering whether to buy ICF International or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

ICF International falls short of our quality standards. To kick things off, its revenue growth was mediocre over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its solid EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its backlog declined. On top of that, its mediocre ROIC lags the market and is a headwind for its stock price.

ICF International’s P/E ratio based on the next 12 months is 9.8x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $105.25 on the company (compared to the current share price of $67.60).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.