LifeStance Health Group (LFST)

We’re not sold on LifeStance Health Group. Its negative returns on capital raise questions about its ability to allocate resources and generate profits.― StockStory Analyst Team

1. News

2. Summary

Why LifeStance Health Group Is Not Exciting

With over 6,600 licensed mental health professionals treating more than 880,000 patients annually, LifeStance Health (NASDAQ:LFST) provides outpatient mental health services through a network of clinicians offering psychiatric evaluations, psychological testing, and therapy across 33 states.

- Negative returns on capital show management lost money while trying to expand the business

- Smaller revenue base of $1.42 billion means it hasn’t achieved the economies of scale that some industry juggernauts enjoy

- A positive is that its impressive 30.4% annual revenue growth over the last five years indicates it’s winning market share this cycle

LifeStance Health Group falls below our quality standards. Better businesses are for sale in the market.

Why There Are Better Opportunities Than LifeStance Health Group

LifeStance Health Group’s stock price of $6.92 implies a valuation ratio of 23.4x forward P/E. Not only does LifeStance Health Group trade at a premium to companies in the healthcare space, but this multiple is also high for its fundamentals.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. LifeStance Health Group (LFST) Research Report: Q4 CY2025 Update

Behavioral health company LifeStance Health (NASDAQ:LFST) announced better-than-expected revenue in Q4 CY2025, with sales up 17.4% year on year to $382.2 million. Guidance for next quarter’s revenue was optimistic at $390 million at the midpoint, 2.4% above analysts’ estimates. Its GAAP profit of $0.03 per share was significantly above analysts’ consensus estimates.

LifeStance Health Group (LFST) Q4 CY2025 Highlights:

- Revenue: $382.2 million vs analyst estimates of $378.6 million (17.4% year-on-year growth, 1% beat)

- EPS (GAAP): $0.03 vs analyst estimates of $0 (significant beat)

- Adjusted EBITDA: $157.7 million vs analyst estimates of $40.31 million (41.3% margin, significant beat)

- Revenue Guidance for Q1 CY2026 is $390 million at the midpoint, above analyst estimates of $380.9 million

- EBITDA guidance for the upcoming financial year 2026 is $195 million at the midpoint, above analyst estimates of $181.5 million

- Operating Margin: 4.7%, up from 0.3% in the same quarter last year

- Free Cash Flow Margin: 12.2%, down from 17.2% in the same quarter last year

- Sales Volumes rose 8.3% year on year (11.7% in the same quarter last year)

- Market Capitalization: $2.78 billion

Company Overview

With over 6,600 licensed mental health professionals treating more than 880,000 patients annually, LifeStance Health (NASDAQ:LFST) provides outpatient mental health services through a network of clinicians offering psychiatric evaluations, psychological testing, and therapy across 33 states.

LifeStance operates through a hybrid care delivery model, allowing patients to access treatment either virtually through its digital platform or in-person at one of its 575 centers nationwide. This flexibility enables patients to seamlessly transition between virtual and in-person care based on their needs and circumstances, which is particularly valuable for conditions requiring close monitoring like medication adjustments or disorders that benefit from face-to-face interaction.

The company employs a multidisciplinary approach to mental healthcare, with a team that includes psychiatrists, advanced practice nurses (APNs), psychologists, and therapists. This comprehensive clinical capability allows LifeStance to treat a wide range of mental health conditions including anxiety, depression, bipolar disorder, eating disorders, and post-traumatic stress disorder without needing to refer patients outside its network.

LifeStance generates revenue primarily through insurance reimbursements, maintaining contracts with national, regional, and local insurance providers that allow patients to use their in-network benefits. UnitedHealthcare and Elevance Health represent significant portions of the company's revenue, accounting for 19% and 13% respectively. The company's payor contracts typically operate on a fee-for-service model, with clinicians compensated based largely on the number of patient visits they complete.

Patient acquisition occurs through insurance network participation, physician referral relationships (particularly with primary care providers), and direct-to-consumer marketing. The company's digital infrastructure supports the entire patient journey, from initial appointment scheduling to treatment delivery and follow-up care, creating a streamlined experience that aims to increase access to mental healthcare services.

Founded in 2017, LifeStance has expanded rapidly through both acquisitions and the development of new centers (de novos). The company's business structure navigates state corporate practice of medicine laws by directly employing clinicians in some locations while operating "supported practices" in others, where clinicians are employed by the practice while LifeStance provides management services.

4. Outpatient & Specialty Care

The outpatient and specialty care industry delivers targeted medical services in non-hospital settings that are often cost-effective compared to inpatient alternatives. This means that they are more desired as rising healthcare costs and ways to combat them become more and more top-of-mind. Outpatient and specialty care providers boast revenue streams that are stable due to the recurring nature of treatment for chronic conditions and long-term patient relationships. However, their reliance on government reimbursement programs like Medicare means stroke-of-the-pen risk. Additionally, scaling a network of facilities can be capital-intensive with uneven return profiles amid competition from integrated healthcare systems. Looking ahead, the industry is positioned to grow as demand for outpatient services expands, driven by aging populations, a rising prevalence of chronic diseases, and a shift toward value-based care models. Tailwinds include advancements in medical technology that support more complex procedures in outpatient settings and the increasing focus on preventive care, which can be aided by data and AI. However, headwinds such as reimbursement rate cuts, labor shortages, and the financial strain of digitization may temper growth.

LifeStance Health competes with other outpatient mental health providers including Talkspace (NASDAQ: TALK), Acadia Healthcare (NASDAQ: ACHC), and Universal Health Services (NYSE: UHS), as well as private companies like Lyra Health and Headspace Health, and traditional private practice networks.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.42 billion in revenue over the past 12 months, LifeStance Health Group is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

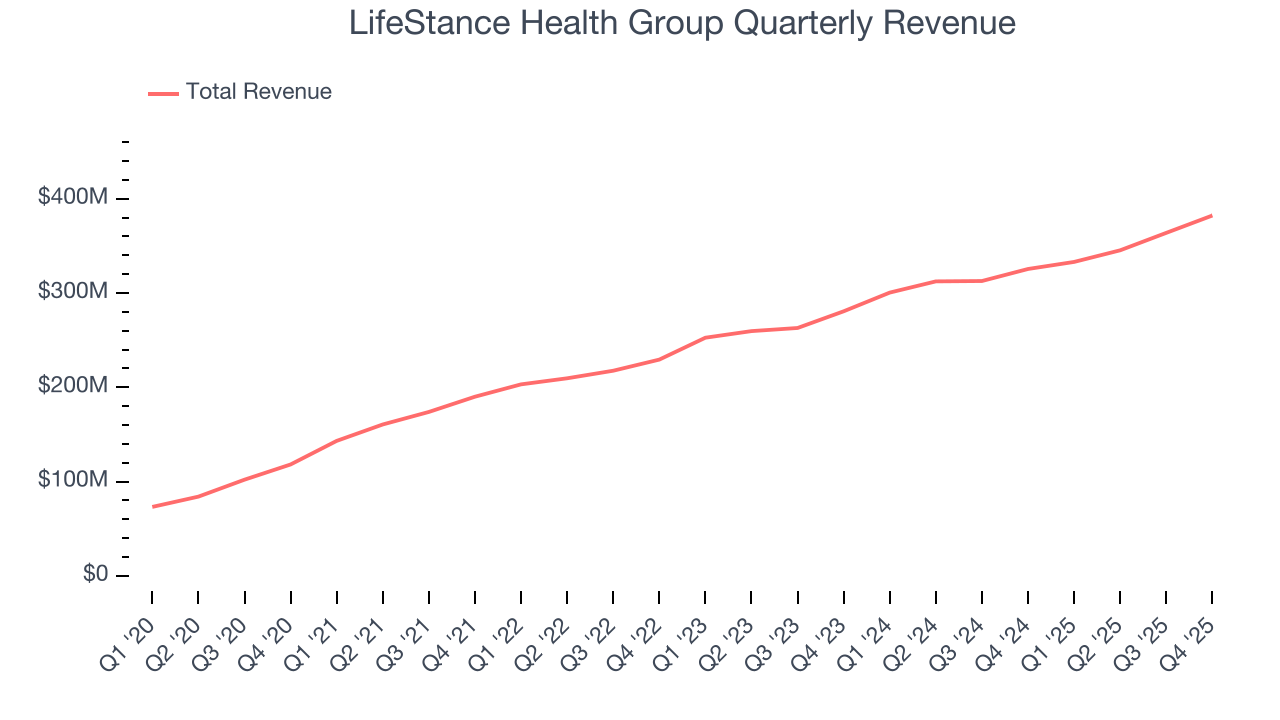

6. Revenue Growth

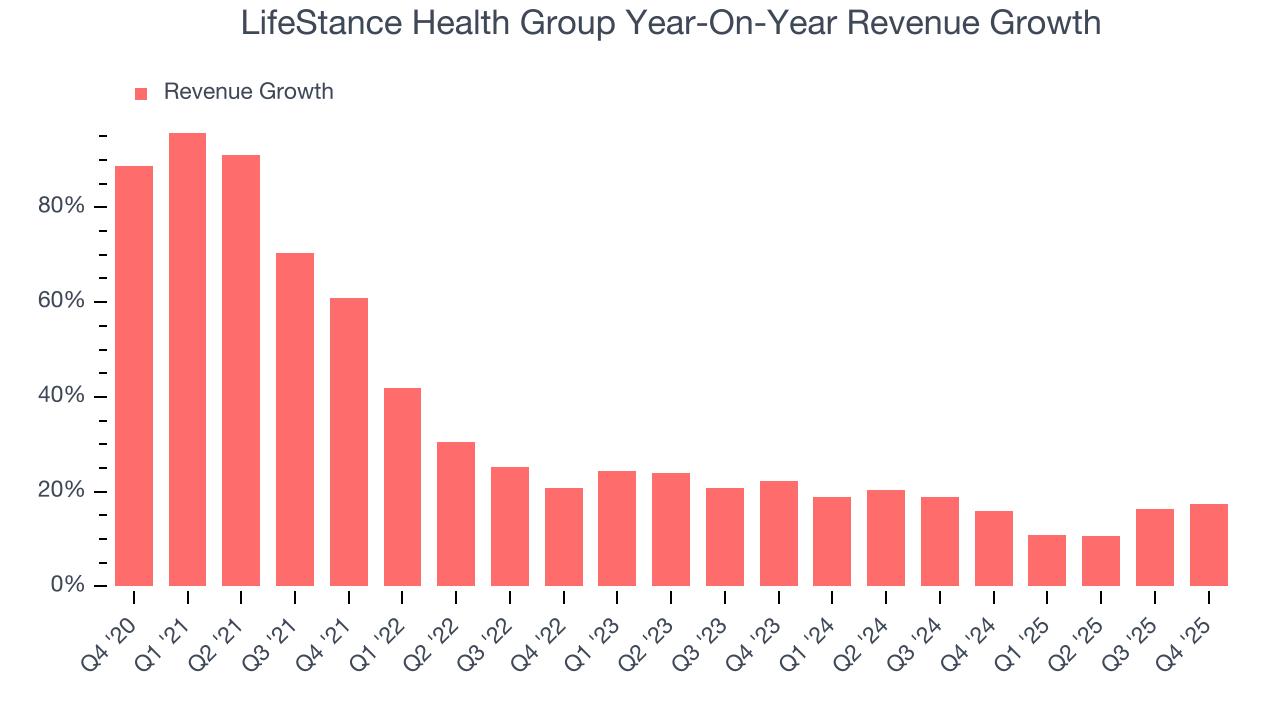

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, LifeStance Health Group’s sales grew at an incredible 30.4% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. LifeStance Health Group’s annualized revenue growth of 16.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

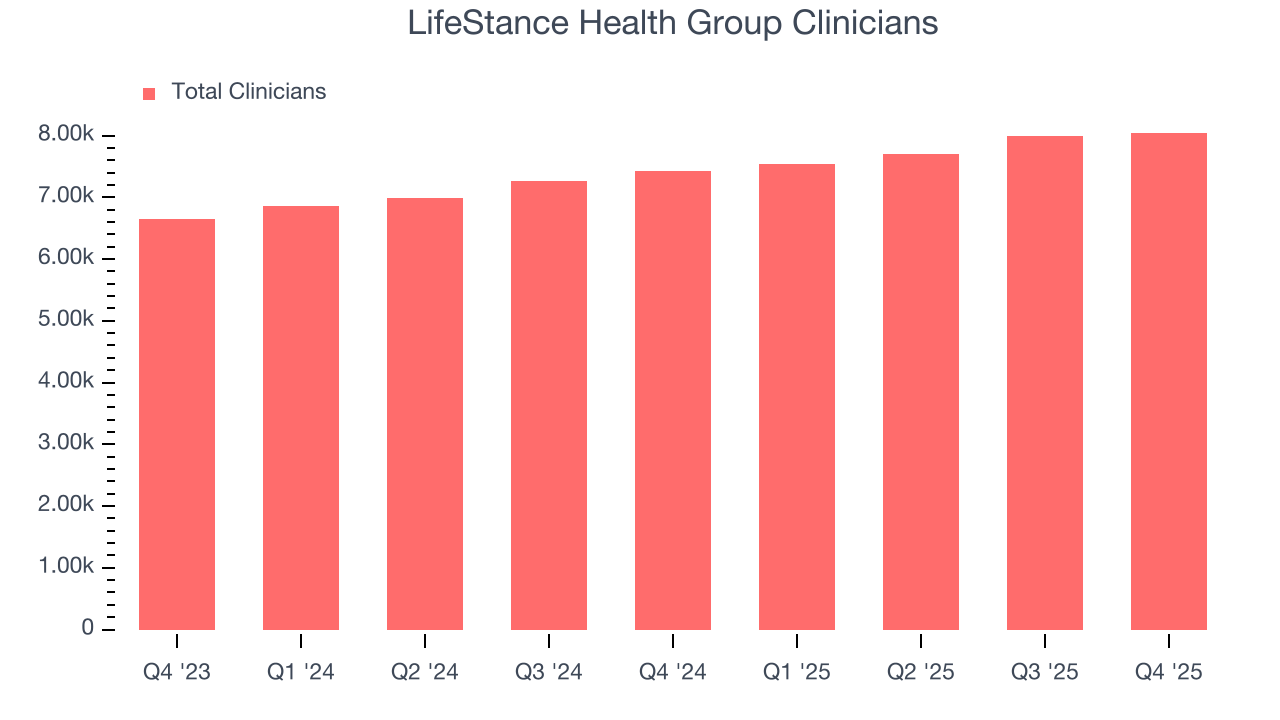

We can better understand the company’s revenue dynamics by analyzing its number of clinicians, which reached 8,040 in the latest quarter. Over the last two years, LifeStance Health Group’s clinicians averaged 10% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, LifeStance Health Group reported year-on-year revenue growth of 17.4%, and its $382.2 million of revenue exceeded Wall Street’s estimates by 1%. Company management is currently guiding for a 17.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.9% over the next 12 months, a slight deceleration versus the last two years. Despite the slowdown, this projection is admirable and implies the market is forecasting success for its products and services.

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

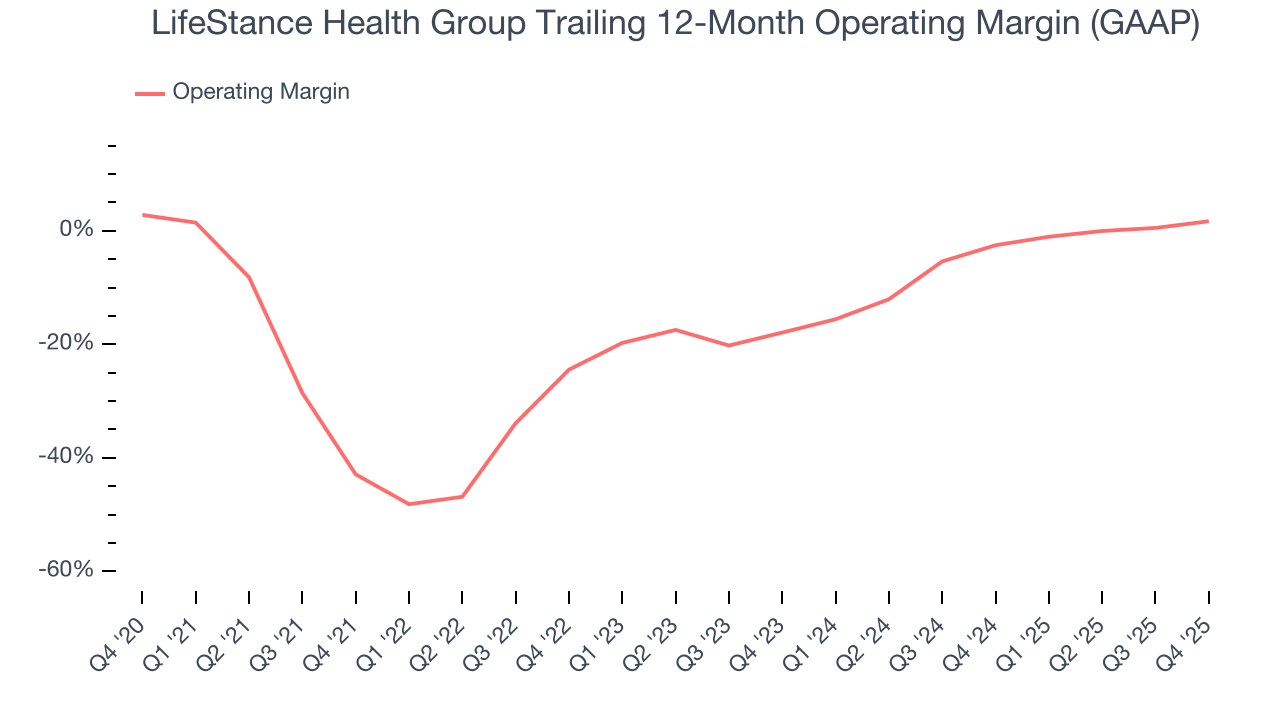

Although LifeStance Health Group was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 13.2% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, LifeStance Health Group’s operating margin rose by 44.6 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 19.6 percentage points on a two-year basis.

In Q4, LifeStance Health Group generated an operating margin profit margin of 4.7%, up 4.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

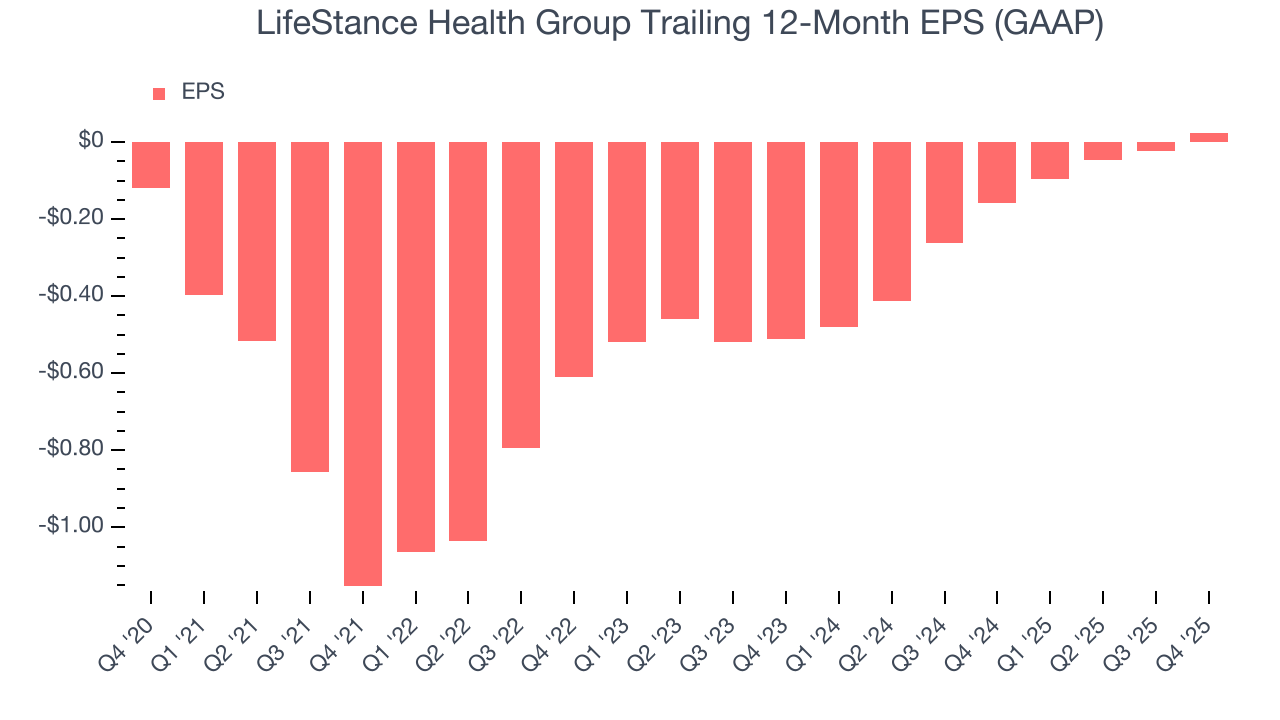

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

LifeStance Health Group’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, LifeStance Health Group reported EPS of $0.03, up from negative $0.02 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects LifeStance Health Group’s full-year EPS of $0.02 to grow 108%.

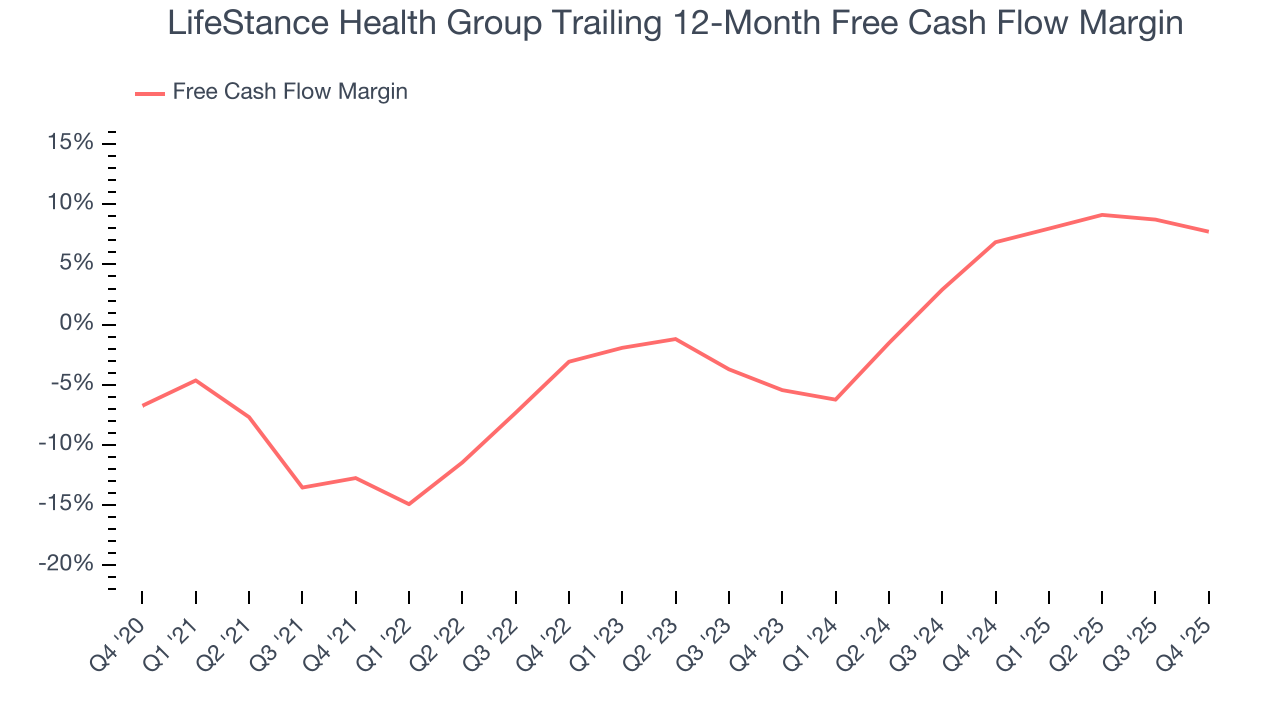

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

LifeStance Health Group broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, an encouraging sign is that LifeStance Health Group’s margin expanded by 20.5 percentage points during that time. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

LifeStance Health Group’s free cash flow clocked in at $46.65 million in Q4, equivalent to a 12.2% margin. The company’s cash profitability regressed as it was 5 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends trump temporary fluctuations.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

LifeStance Health Group’s five-year average ROIC was negative 10.3%, meaning management lost money while trying to expand the business. Its returns were among the worst in the healthcare sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, LifeStance Health Group’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

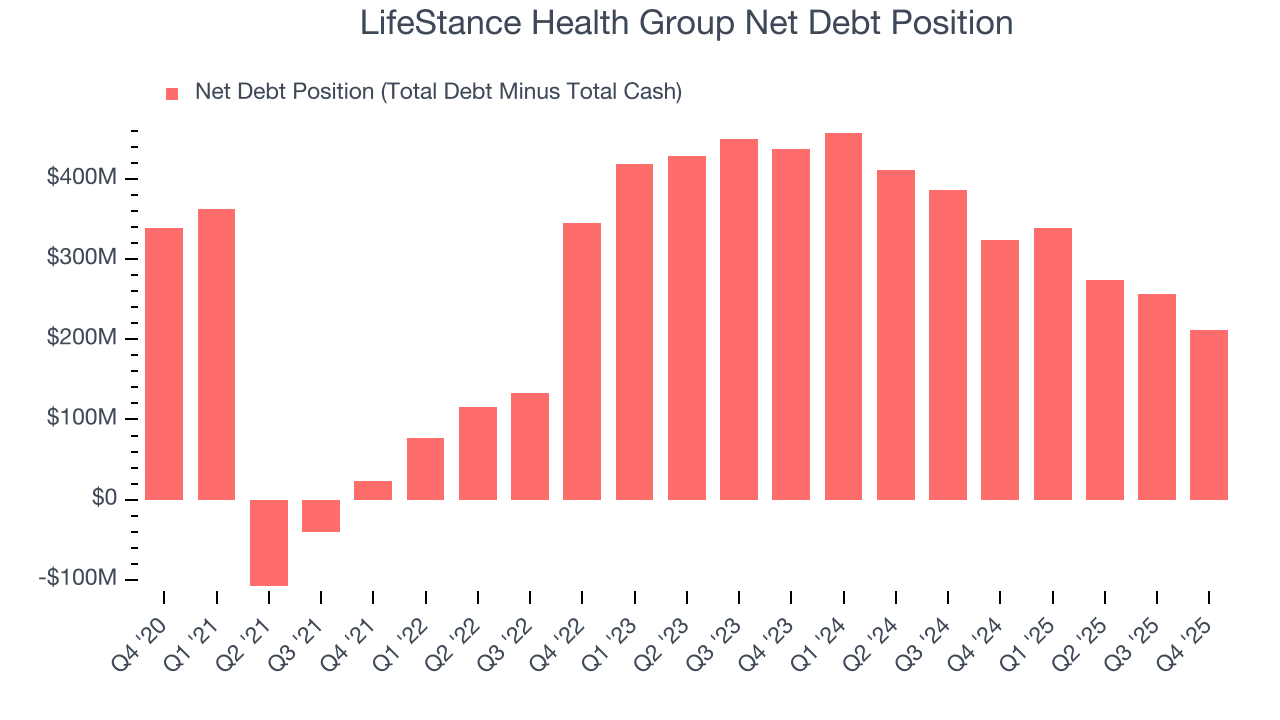

11. Balance Sheet Assessment

LifeStance Health Group reported $248.6 million of cash and $460 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $266.5 million of EBITDA over the last 12 months, we view LifeStance Health Group’s 0.8× net-debt-to-EBITDA ratio as safe. We also see its $8.79 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from LifeStance Health Group’s Q4 Results

It was good to see LifeStance Health Group beat analysts’ EPS expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 12.7% to $8.05 immediately following the results.

13. Is Now The Time To Buy LifeStance Health Group?

Updated: March 6, 2026 at 11:21 PM EST

Are you wondering whether to buy LifeStance Health Group or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

There are some bright spots in LifeStance Health Group’s fundamentals, but its business quality ultimately falls short. First off, its revenue growth was exceptional over the last five years. And while LifeStance Health Group’s relatively low ROIC suggests management has struggled to find compelling investment opportunities, its rising cash profitability gives it more optionality.

LifeStance Health Group’s P/E ratio based on the next 12 months is 23.4x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $9.83 on the company (compared to the current share price of $6.92).