El Pollo Loco (LOCO)

We wouldn’t buy El Pollo Loco. Its weak revenue growth and gross margin show it not only lacks demand but also decent unit economics.― StockStory Analyst Team

1. News

2. Summary

Why We Think El Pollo Loco Will Underperform

With a name that translates into ‘The Crazy Chicken’, El Pollo Loco (NASDAQ:LOCO) is a fast food chain known for its citrus-marinated, fire-grilled chicken recipe that hails from the coastal town of Sinaloa, Mexico.

- Sales trends were unexciting over the last six years as its 1.7% annual growth was below the typical restaurant company

- Demand will likely be soft over the next 12 months as Wall Street’s estimates imply tepid growth of 1.4%

- Modest revenue base of $490 million gives it less fixed cost leverage and fewer distribution channels than larger companies

El Pollo Loco’s quality is insufficient. There are superior stocks for sale in the market.

Why There Are Better Opportunities Than El Pollo Loco

El Pollo Loco’s stock price of $14.15 implies a valuation ratio of 14.7x forward P/E. Yes, this valuation multiple is lower than that of other restaurant peers, but we’ll remind you that you often get what you pay for.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. El Pollo Loco (LOCO) Research Report: Q4 CY2025 Update

Fast food chain El Pollo Loco (NASDAQ:LOCO) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 8.1% year on year to $123.5 million. Its non-GAAP profit of $0.25 per share was 25% above analysts’ consensus estimates.

El Pollo Loco (LOCO) Q4 CY2025 Highlights:

- Revenue: $123.5 million vs analyst estimates of $124 million (8.1% year-on-year growth, in line)

- Adjusted EPS: $0.25 vs analyst estimates of $0.20 (25% beat)

- Adjusted EBITDA: $16.9 million vs analyst estimates of $14.65 million (13.7% margin, 15.3% beat)

- Operating Margin: 8.3%, in line with the same quarter last year

- Locations: 503 at quarter end, up from 498 in the same quarter last year

- Same-Store Sales rose 2.1% year on year (0.5% in the same quarter last year)

- Market Capitalization: $333.4 million

Company Overview

With a name that translates into ‘The Crazy Chicken’, El Pollo Loco (NASDAQ:LOCO) is a fast food chain known for its citrus-marinated, fire-grilled chicken recipe that hails from the coastal town of Sinaloa, Mexico.

The company was founded in 1980 in Los Angeles, California. While it started with that signature chicken dish, the chain has expanded its offering to include a variety of Mexican-inspired dishes like tacos, burritos, and quesadillas. In response to changing consumer tastes, El Pollo Loco now offers a ‘fit’ menu featuring items such as Keto burritos and salads.

The core El Pollo Loco customer is diverse but principally a middle-income individual or family seeking a tasty and unique menu that is also affordable. More specifically, the core customer is likely someone who appreciates the depths of Mexican food beyond just the simple taco.

El Pollo Loco locations are moderate in size, catering to the fast food and casual segments. There's often seating available, but it's typically limited compared to large sit-down restaurants. There are booths, tables, and sometimes outdoor patios. The vibe inside mirrors its Californian roots with a modern, relaxed atmosphere featuring hues of orange and earth tones. Artwork or motifs hinting at its Mexican culinary heritage complete the look. In all, it is a laid back, casual atmosphere where no one minds if things get lively or even celebratory.

4. Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Competitors offering Mexican-inspired fare or specialty chicken dishes include Chipotle (NYSE:CMG), Fiesta Restaurant Group (NASDAQ:FRGI), Chuy’s (NASDAQ:CHUY), and private company Qdoba.

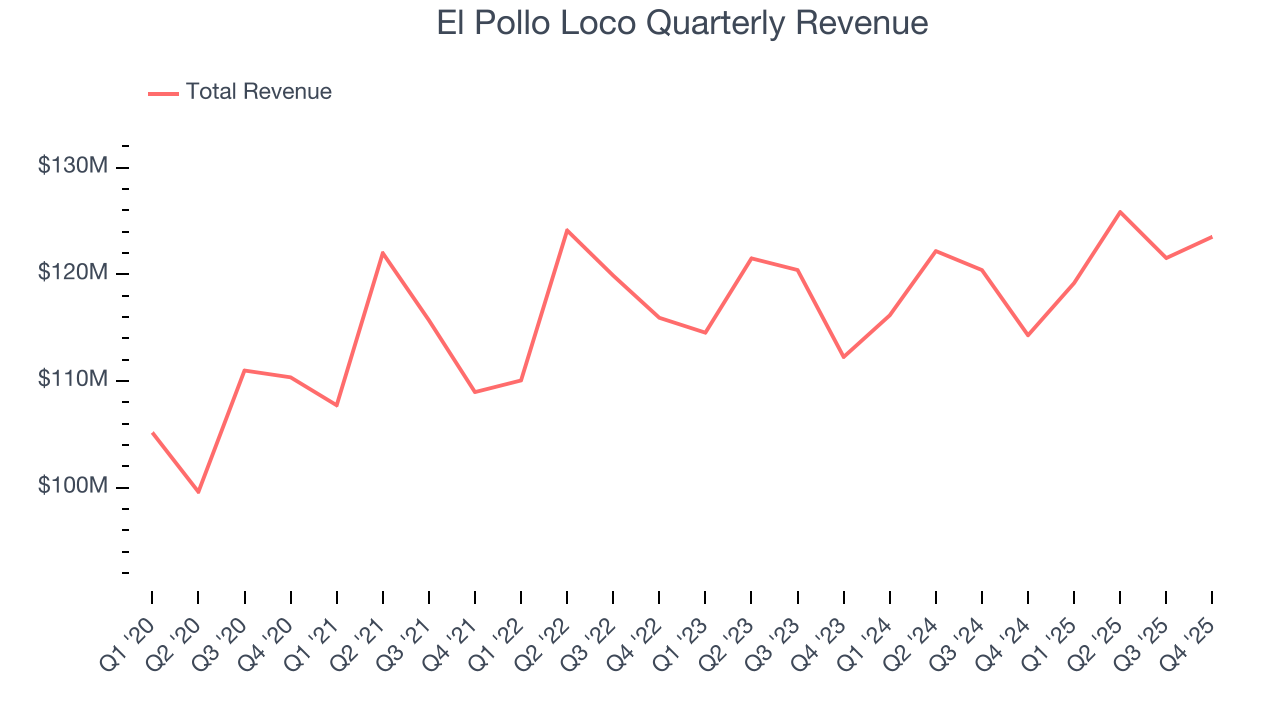

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $490 million in revenue over the past 12 months, El Pollo Loco is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, El Pollo Loco grew its sales at a weak 1.7% compounded annual growth rate over the last six years as its restaurant footprint remained unchanged and it barely increased sales at existing, established dining locations.

This quarter, El Pollo Loco grew its revenue by 8.1% year on year, and its $123.5 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 1.1% over the next 12 months, similar to its six-year rate. This projection is underwhelming and suggests its newer menu offerings will not accelerate its top-line performance yet.

6. Restaurant Performance

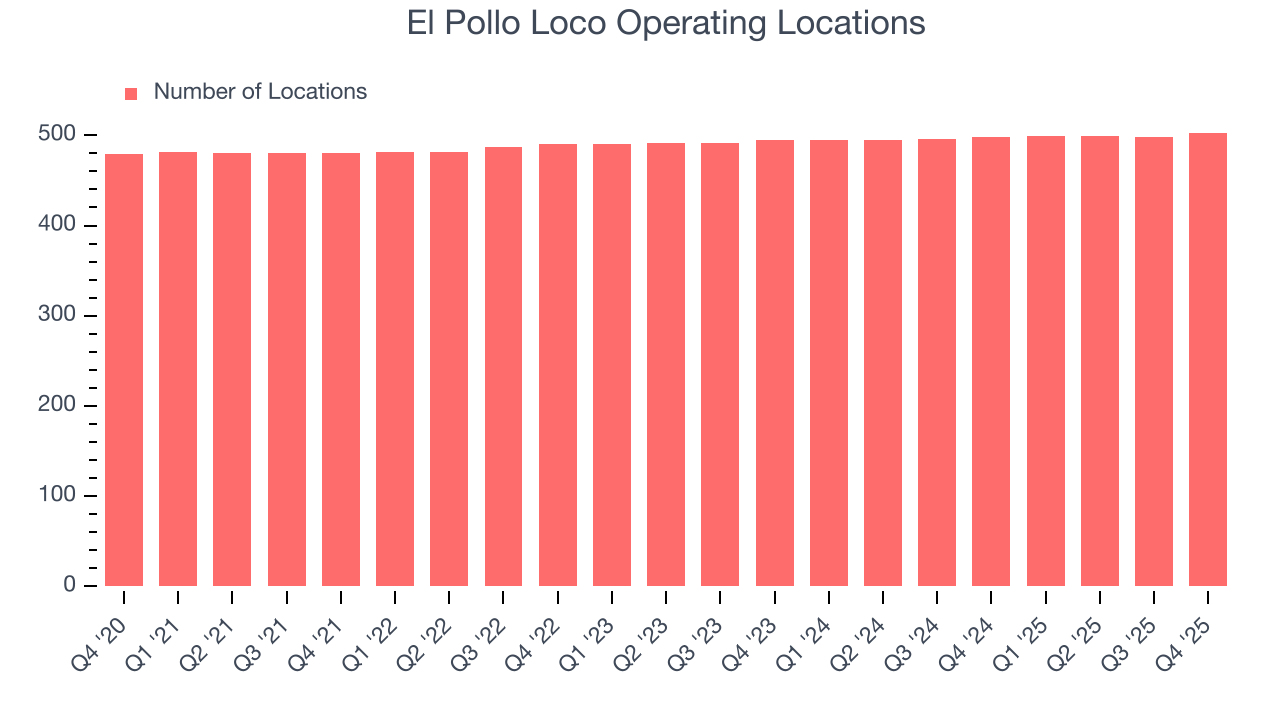

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

El Pollo Loco operated 503 locations in the latest quarter, and over the last two years, has kept its restaurant count flat while other restaurant businesses have opted for growth.

When a chain doesn’t open many new restaurants, it usually means there’s stable demand for its meals and it’s focused on improving operational efficiency to increase profitability.

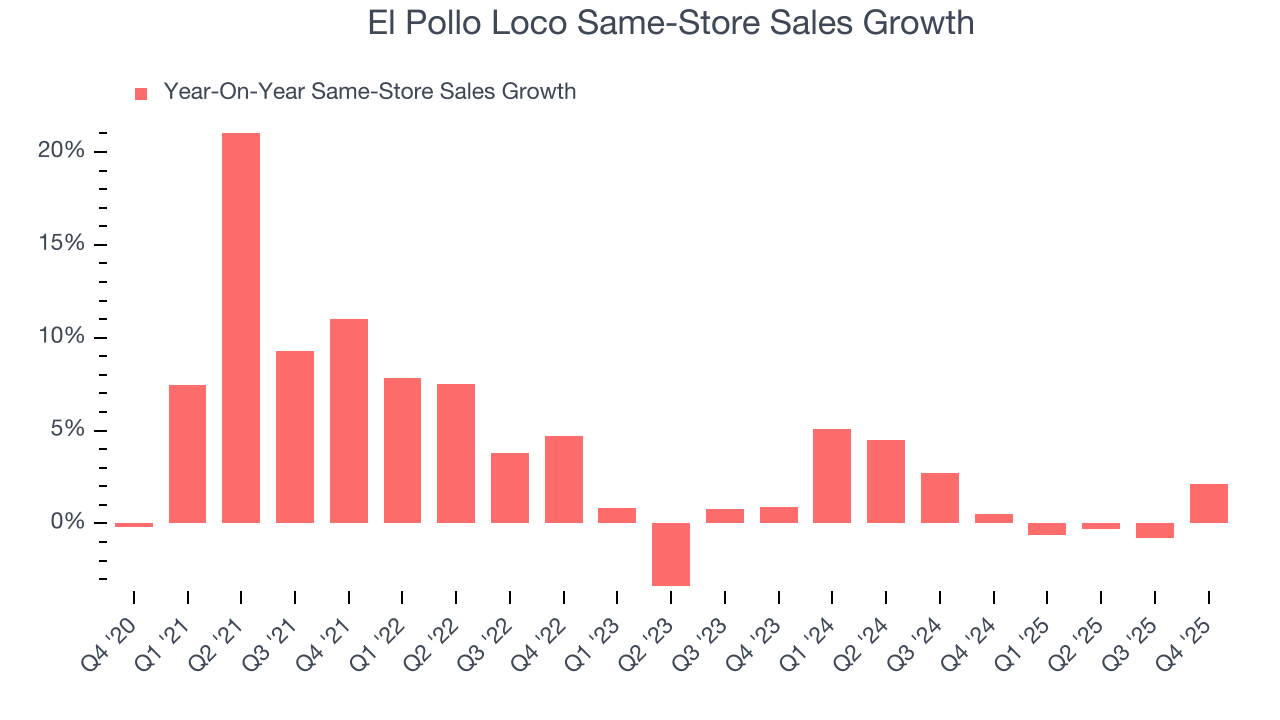

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing restaurants and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

El Pollo Loco’s demand within its existing dining locations has been relatively stable over the last two years but was below most restaurant chains. On average, the company’s same-store sales have grown by 1.7% per year. Given its flat restaurant base over the same period, this performance stems from a mixture of higher prices and increased foot traffic at existing locations.

In the latest quarter, El Pollo Loco’s same-store sales rose 2.1% year on year. This performance was more or less in line with its historical levels.

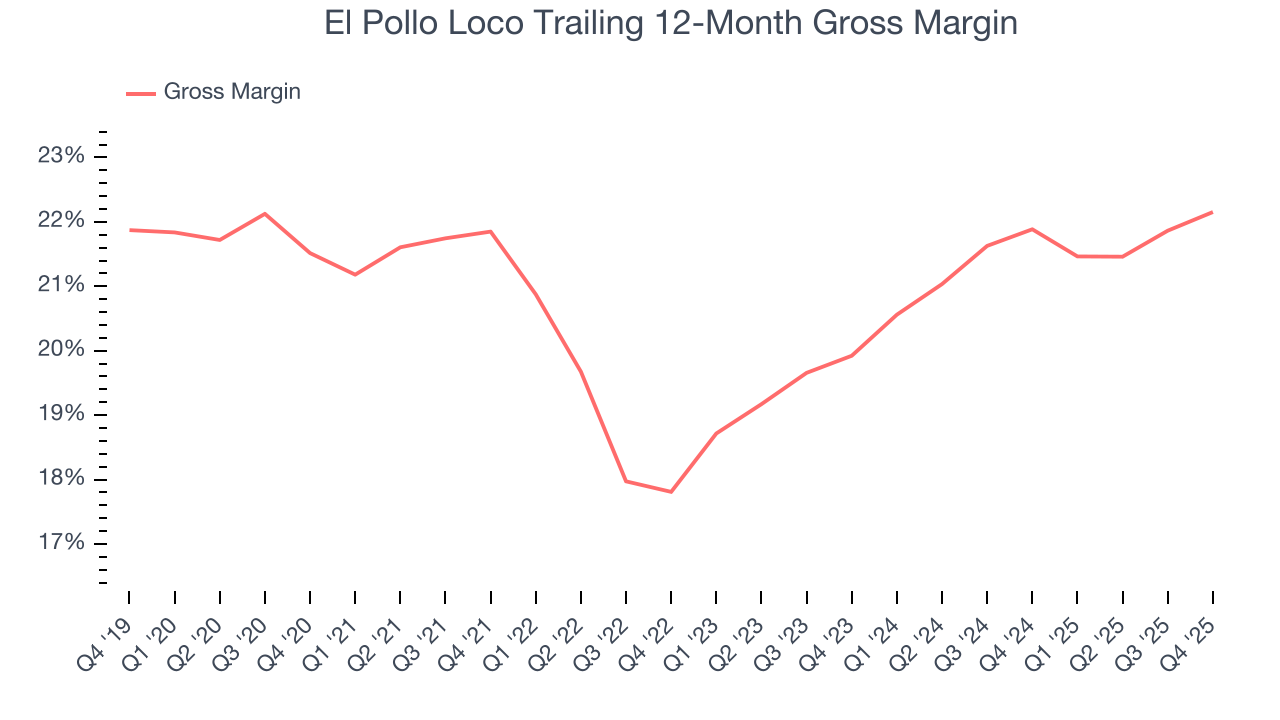

7. Gross Margin & Pricing Power

El Pollo Loco has bad unit economics for a restaurant company, giving it less room to reinvest and grow its presence. As you can see below, it averaged a 22% gross margin over the last two years. Said differently, El Pollo Loco had to pay a chunky $77.98 to its suppliers for every $100 in revenue.

In Q4, El Pollo Loco produced a 22.5% gross profit margin, marking a 1.2 percentage point increase from 21.3% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as ingredients and transportation expenses) have been stable and it isn’t under pressure to lower prices.

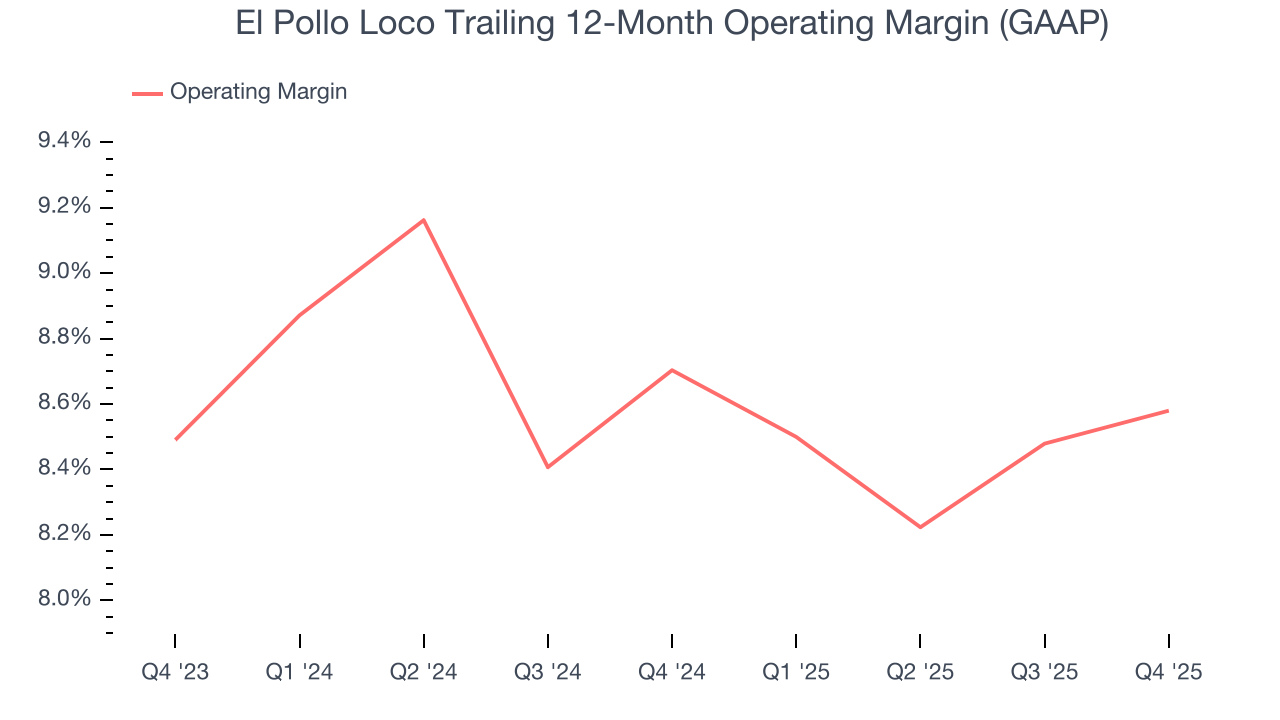

8. Operating Margin

El Pollo Loco’s operating margin has more or less stayed the same over the last 12 months , averaging 8.6% over the last two years. This profitability was higher than the broader restaurant sector, showing it did a decent job managing its expenses.

Analyzing the trend in its profitability, El Pollo Loco’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, El Pollo Loco generated an operating margin profit margin of 8.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

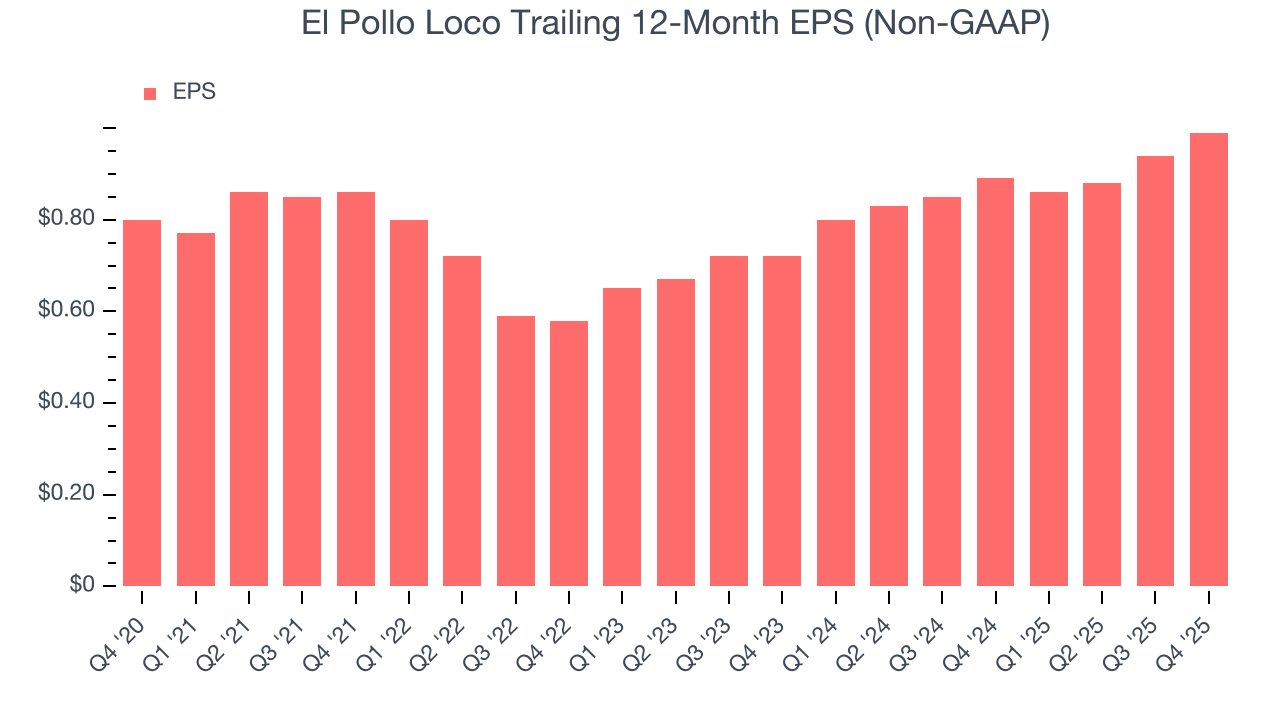

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

El Pollo Loco’s EPS grew at 4.5% compounded annual growth rate over the last six years. On the bright side, this performance was better than its 1.7% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

In Q4, El Pollo Loco reported adjusted EPS of $0.25, up from $0.20 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects El Pollo Loco’s full-year EPS of $0.99 to shrink by 4%.

10. Cash Is King

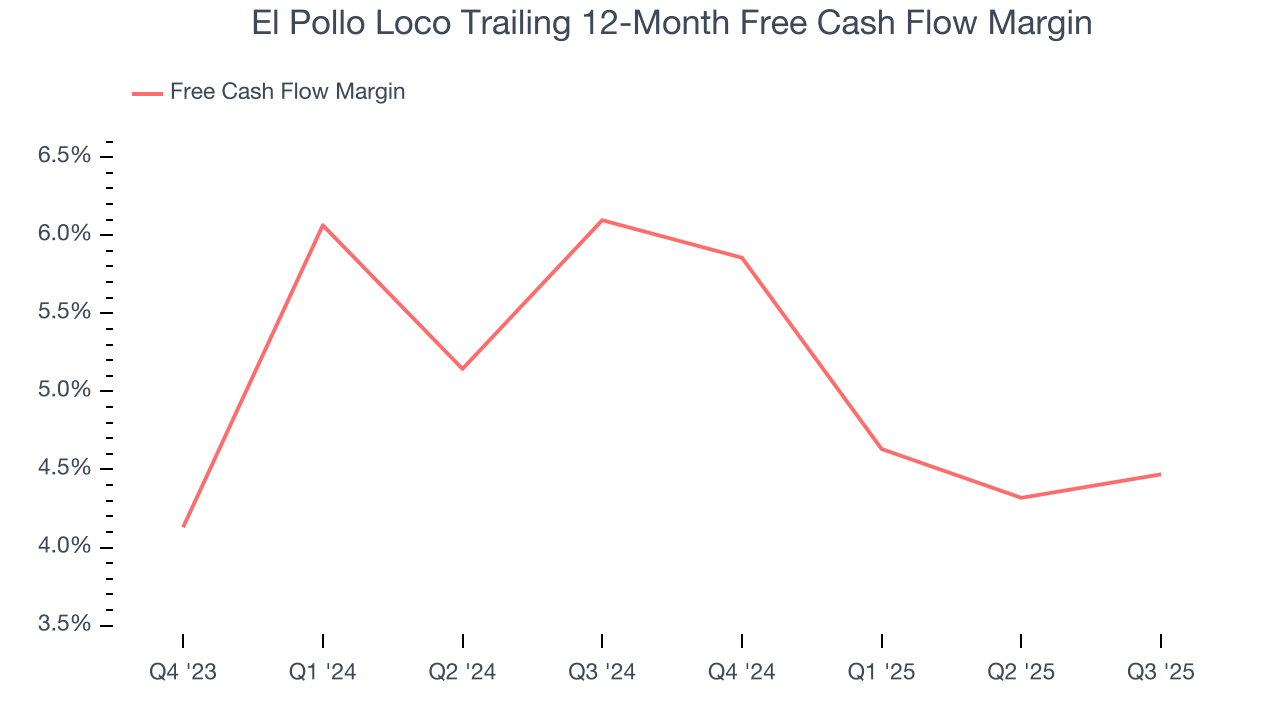

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

El Pollo Loco has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.7% over the last two years, better than the broader restaurant sector.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

El Pollo Loco’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 8.4%, slightly better than typical restaurant business.

12. Balance Sheet Assessment

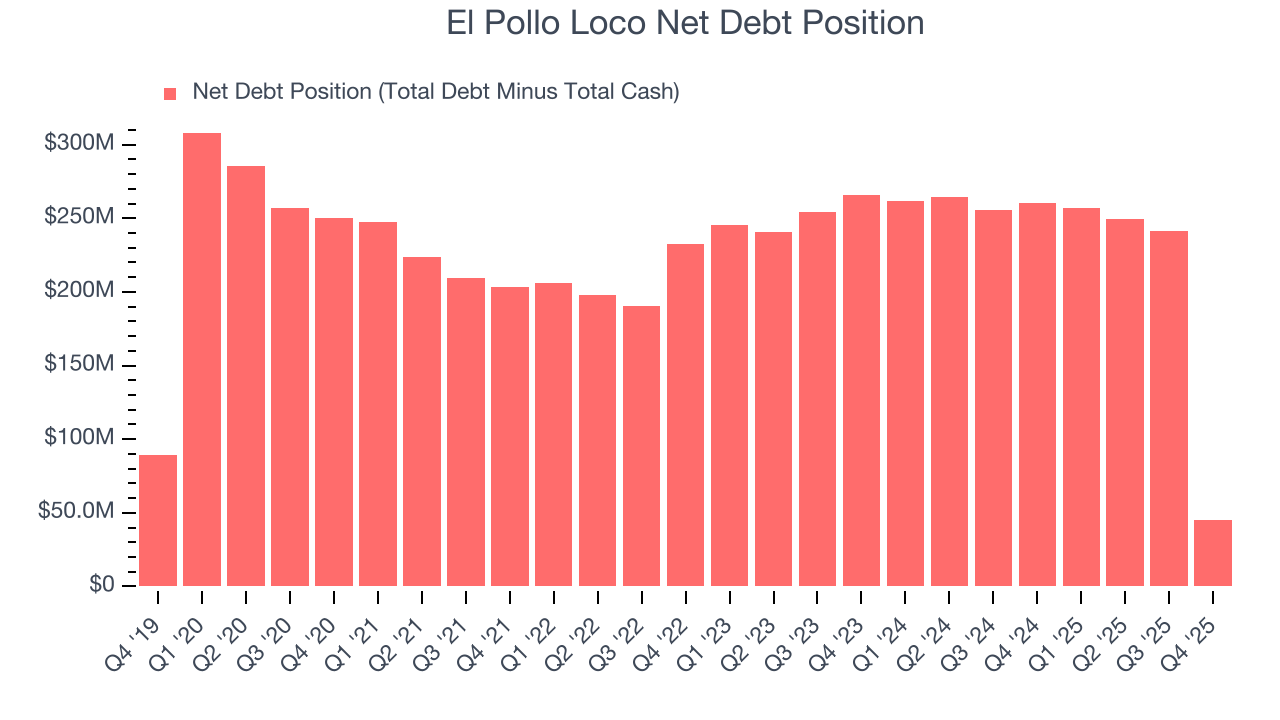

El Pollo Loco reported $6.23 million of cash and $51 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $66.71 million of EBITDA over the last 12 months, we view El Pollo Loco’s 0.7× net-debt-to-EBITDA ratio as safe. We also see its $2.54 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from El Pollo Loco’s Q4 Results

We were impressed by how significantly El Pollo Loco blew past analysts’ EBITDA expectations this quarter. We were also glad its same-store sales outperformed Wall Street’s estimates. On the other hand, its revenue was in line. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 3.3% to $11.23 immediately following the results.

14. Is Now The Time To Buy El Pollo Loco?

Updated: March 21, 2026 at 10:54 PM EDT

Before investing in or passing on El Pollo Loco, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

El Pollo Loco falls short of our quality standards. To kick things off, its revenue growth was weak over the last six years, and analysts don’t see anything changing over the next 12 months. While its stable growth in new restaurants shows it has steady demand, the downside is its brand caters to a niche market. On top of that, its projected EPS for the next year is lacking.

El Pollo Loco’s P/E ratio based on the next 12 months is 14.7x. This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $15.13 on the company (compared to the current share price of $14.15).