Lattice Semiconductor (LSCC)

We aren’t fans of Lattice Semiconductor. Its weak sales growth shows demand is soft and its low margins are a cause for concern.― StockStory Analyst Team

1. News

2. Summary

Why Lattice Semiconductor Is Not Exciting

A global leader in its category, Lattice Semiconductor (NASDAQ:LSCC) is a semiconductor designer specializing in customer-programmable chips that enhance CPU performance for intensive tasks such as machine learning.

- Subpar operating margin has withered over the last five years, constraining its ability to invest in process improvements or effectively respond to new competitive threats

- A consolation is that its offerings are difficult to replicate at scale and result in a best-in-class gross margin of 68.2%

Lattice Semiconductor’s quality is lacking. We see more favorable opportunities in the market.

Why There Are Better Opportunities Than Lattice Semiconductor

Lattice Semiconductor’s stock price of $85.72 implies a valuation ratio of 55.4x forward P/E. This valuation multiple seems a bit much considering the quality you get.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Lattice Semiconductor (LSCC) Research Report: Q4 CY2025 Update

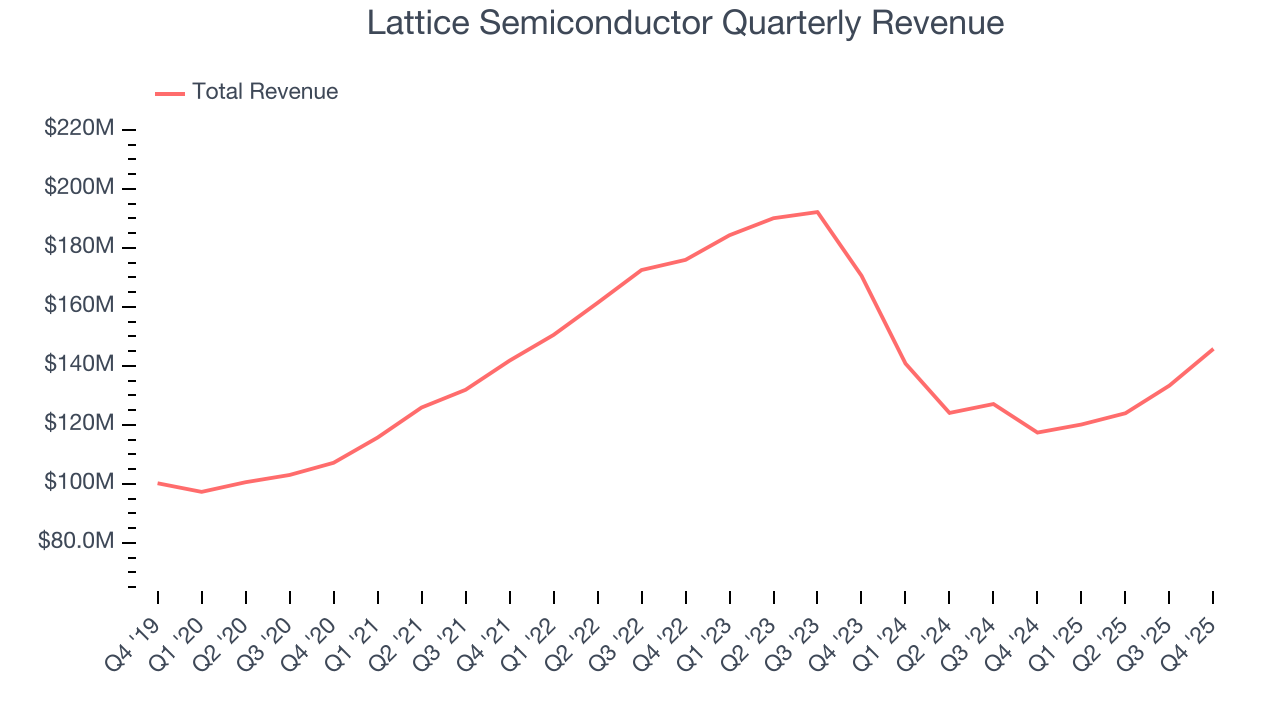

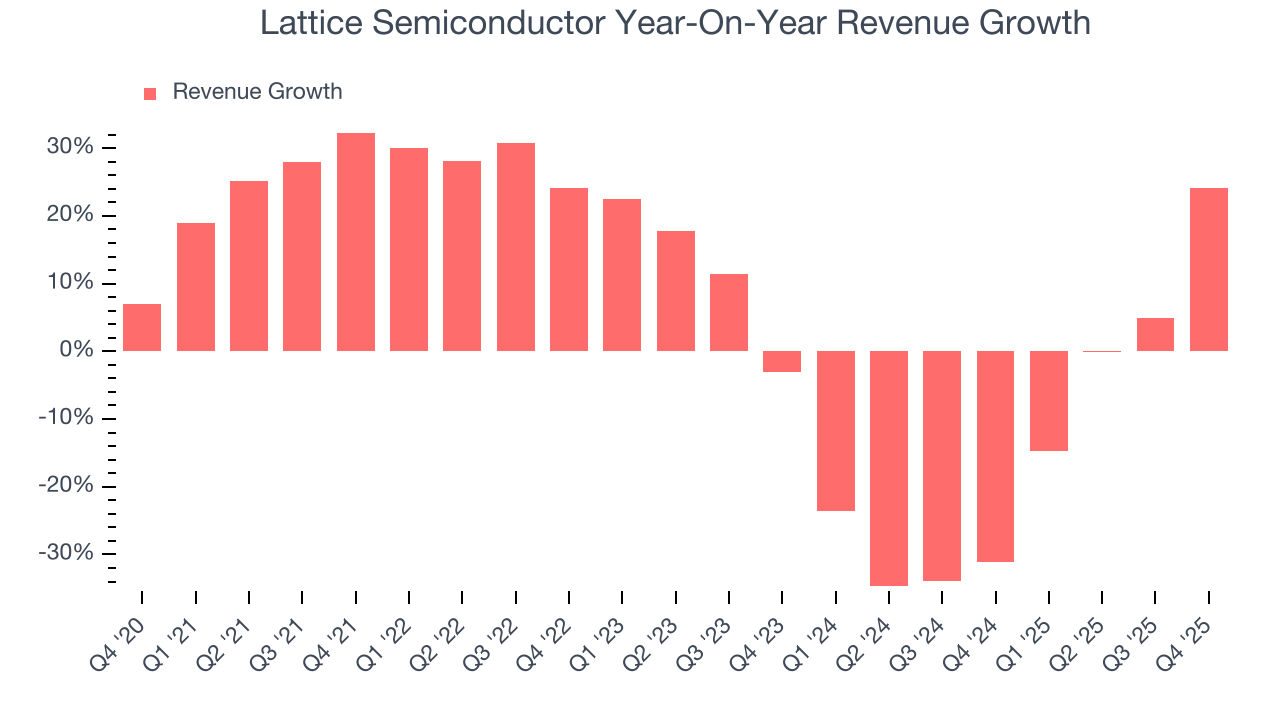

Semiconductor designer Lattice Semiconductor (NASDAQ:LSCC) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 24.2% year on year to $145.8 million. On top of that, next quarter’s revenue guidance ($165 million at the midpoint) was surprisingly good and 11.6% above what analysts were expecting. Its non-GAAP profit of $0.32 per share was in line with analysts’ consensus estimates.

Lattice Semiconductor (LSCC) Q4 CY2025 Highlights:

- Revenue: $145.8 million vs analyst estimates of $143.2 million (24.2% year-on-year growth, 1.8% beat)

- Adjusted EPS: $0.32 vs analyst estimates of $0.32 (in line)

- Adjusted EBITDA: $53.2 million vs analyst estimates of $50.81 million (36.5% margin, 4.7% beat)

- Revenue Guidance for Q1 CY2026 is $165 million at the midpoint, above analyst estimates of $147.8 million

- Adjusted EPS guidance for Q1 CY2026 is $0.36 at the midpoint, above analyst estimates of $0.33

- Operating Margin: 0.7%, up from -10.4% in the same quarter last year

- Free Cash Flow Margin: 30.2%, down from 33.8% in the same quarter last year

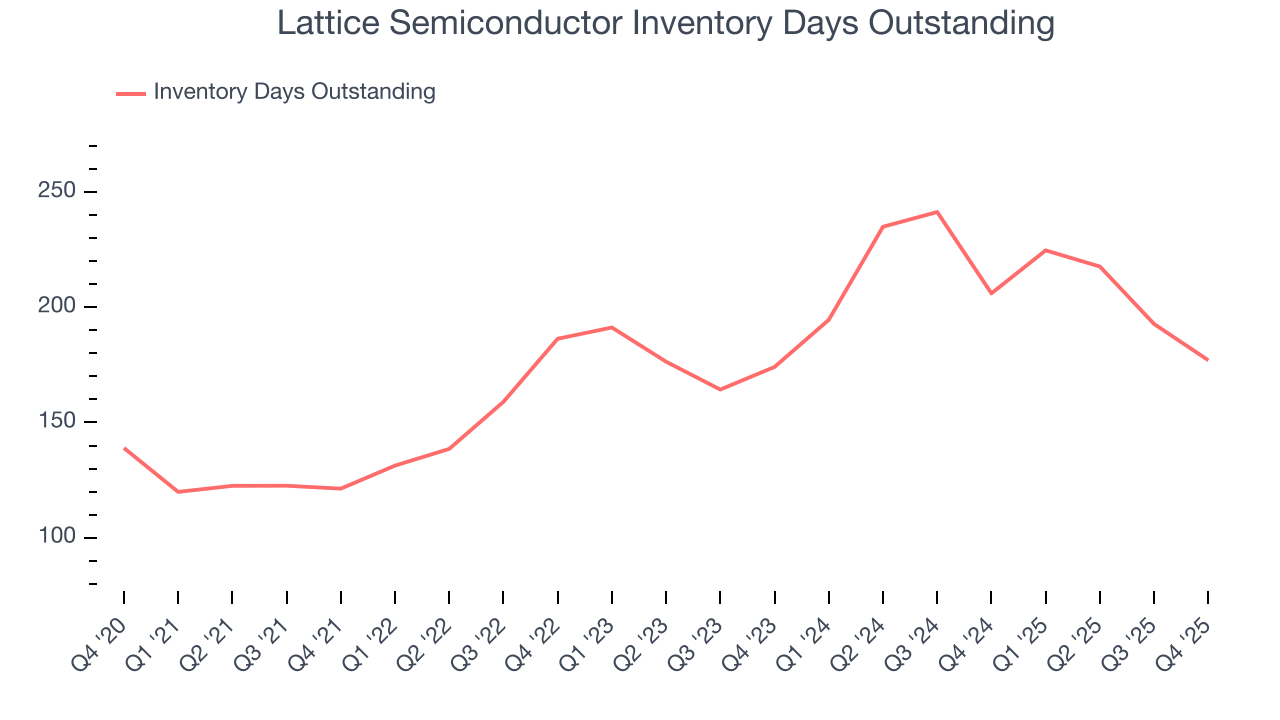

- Inventory Days Outstanding: 177, down from 193 in the previous quarter

- Market Capitalization: $11.97 billion

Company Overview

A global leader in its category, Lattice Semiconductor (NASDAQ:LSCC) is a semiconductor designer specializing in customer-programmable chips that enhance CPU performance for intensive tasks such as machine learning.

Lattice Semiconductor was founded in 1983 by Rahul Sud and Ray Capece. After initial struggles led to a 1987 bankruptcy, Lattice promptly emerged from Chapter 11 and went public in 1989.

Traditionally, field-programmable gate arrays (FPGAs) have been reserved for specific use-cases where the volume of production is small. For these low-volume applications, the premium that companies pay in hardware cost per unit for a chip they can program themselves is more affordable than the development resources spent on creating an application-specific integrated circuit (ASIC).

New cost and performance dynamics have recently broadened the range of viable applications and FPGAs are now used for cases such as accelerating artificial neural networks for machine learning, video processing or 3D MRI imaging. Lattice makes general-purpose FPGAs but also dedicated chips optimized for security and video connectivity applications.

Competitors in the field-programmable gate array (FPGA) market include longtime leaders Xilinx which was acquired by AMD (NASDAQ:AMD) in early 2022, and Altera that was acquired by Intel (NASDAQ:INTC) in 2015. Samsung and QuickLogic (NASDAQ:QUIK) are other competitors.

4. Revenue Growth

A company’s top-line performance can indicate its business quality. Rapid growth can signal it’s benefiting from an innovative new product or burgeoning market trend. Lattice Semiconductor struggled to generate demand over the last two years as its sales dropped by 15.7% annually, a rough starting point for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Lattice Semiconductor’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 15.7% annually.

This quarter, Lattice Semiconductor reported robust year-on-year revenue growth of 24.2%, and its $145.8 million of revenue topped Wall Street estimates by 1.8%. Company management is currently guiding for a 37.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 20.9% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and suggests its newer products and services will spur better top-line performance.

5. Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Lattice Semiconductor’s DIO came in at 177, which is 2 more days than its five-year average. These numbers suggest that despite the recent decrease, the company’s inventory levels are slightly above the long-term average.

6. Gross Margin & Pricing Power

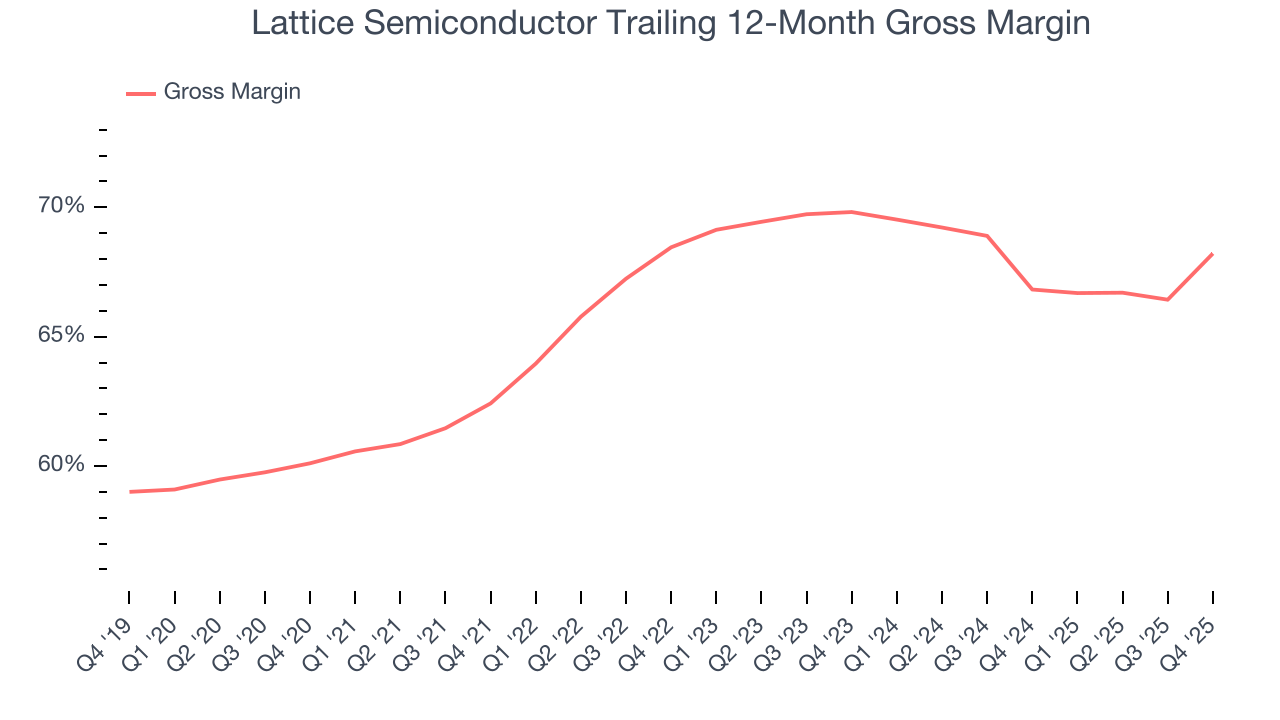

In the semiconductor industry, a company’s gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Lattice Semiconductor’s gross margin is one of the best in the semiconductor sector, and its strong pricing power is a direct result of its differentiated products and technological expertise. As you can see below, it averaged an elite 67.5% gross margin over the last two years. That means Lattice Semiconductor only paid its suppliers $32.47 for every $100 in revenue.

This quarter, Lattice Semiconductor’s gross profit margin was 68.5%, marking a 7.4 percentage point increase from 61.1% in the same quarter last year. Lattice Semiconductor’s full-year margin has also been trending up over the past 12 months, increasing by 1.4 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

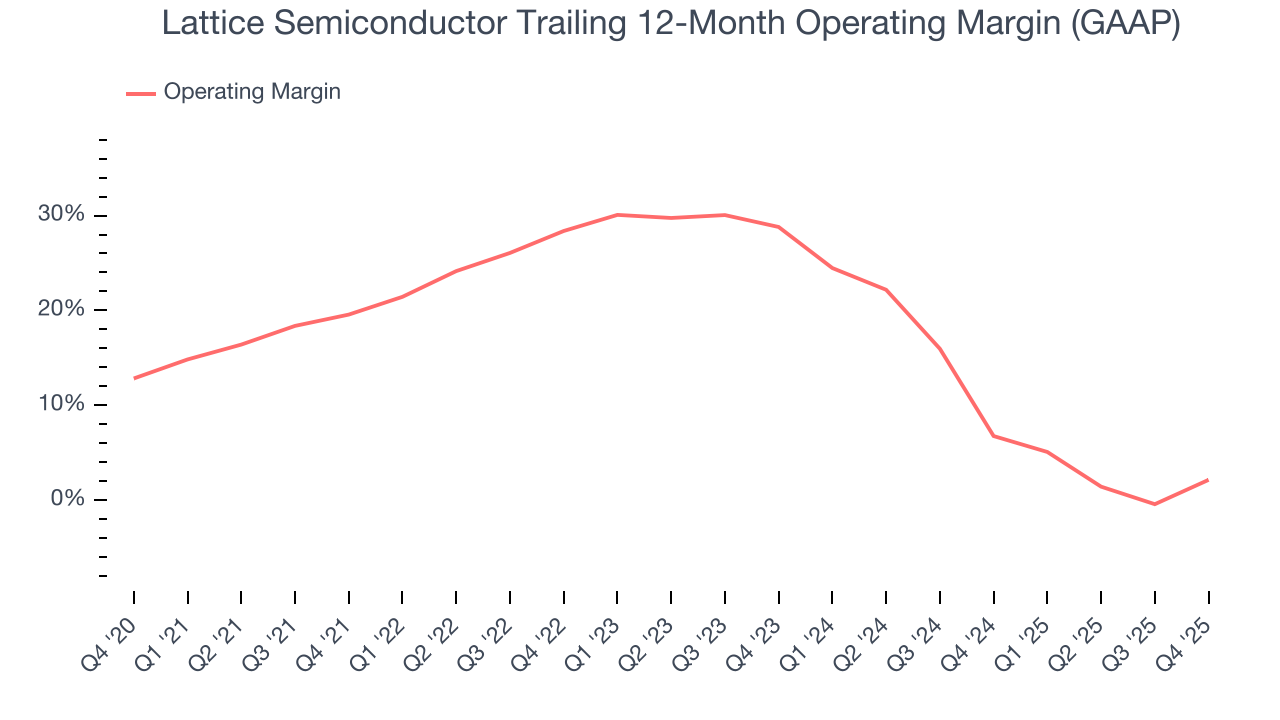

7. Operating Margin

Lattice Semiconductor was profitable over the last two years but held back by its large cost base. Its average operating margin of 4.4% was weak for a semiconductor business. This result is surprising given its high gross margin as a starting point.

Analyzing the trend in its profitability, Lattice Semiconductor’s operating margin decreased by 17.4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Lattice Semiconductor’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Lattice Semiconductor’s breakeven margin was 0.7%, up 11.1 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

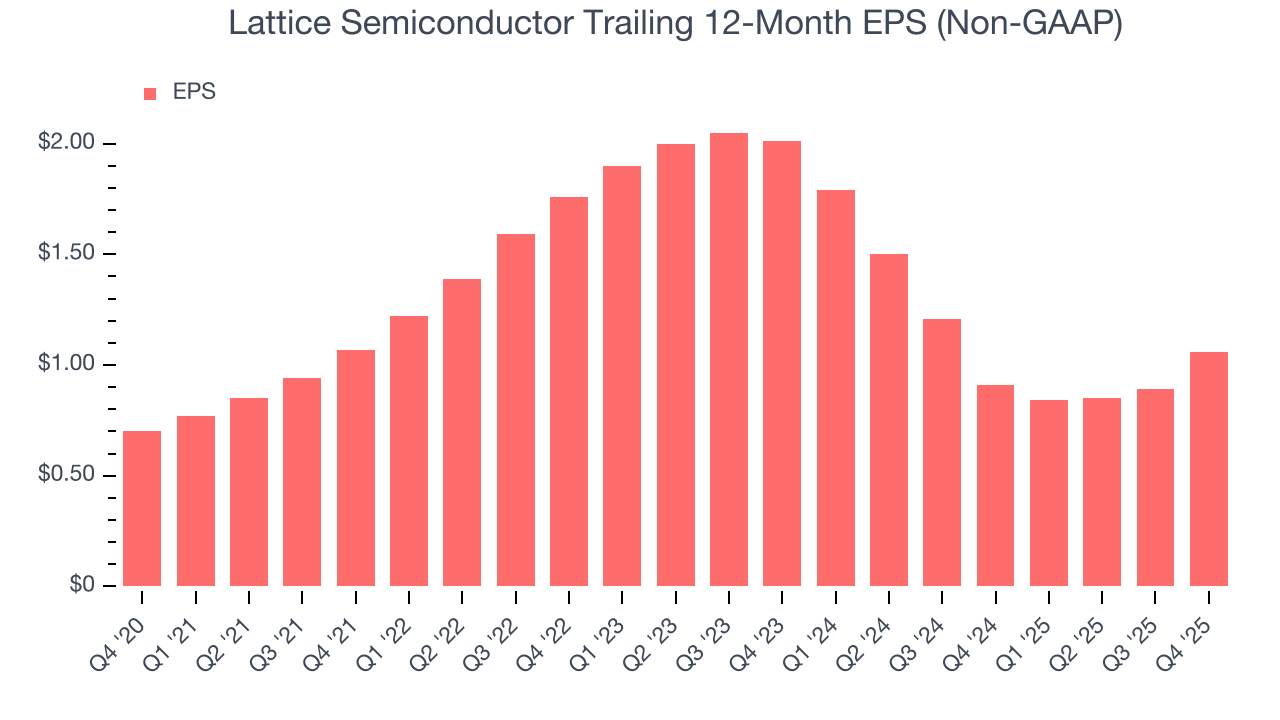

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Lattice Semiconductor’s EPS grew at an unimpressive 8.7% compounded annual growth rate over the last five years. This performance was better than its flat revenue but doesn’t tell us much about its business quality because its operating margin didn’t improve.

We can take a deeper look into Lattice Semiconductor’s earnings to better understand the drivers of its performance. A five-year view shows that Lattice Semiconductor has repurchased its stock, shrinking its share count by 3.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Lattice Semiconductor reported adjusted EPS of $0.32, up from $0.15 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Lattice Semiconductor’s full-year EPS of $1.06 to grow 38.2%.

9. Cash Is King

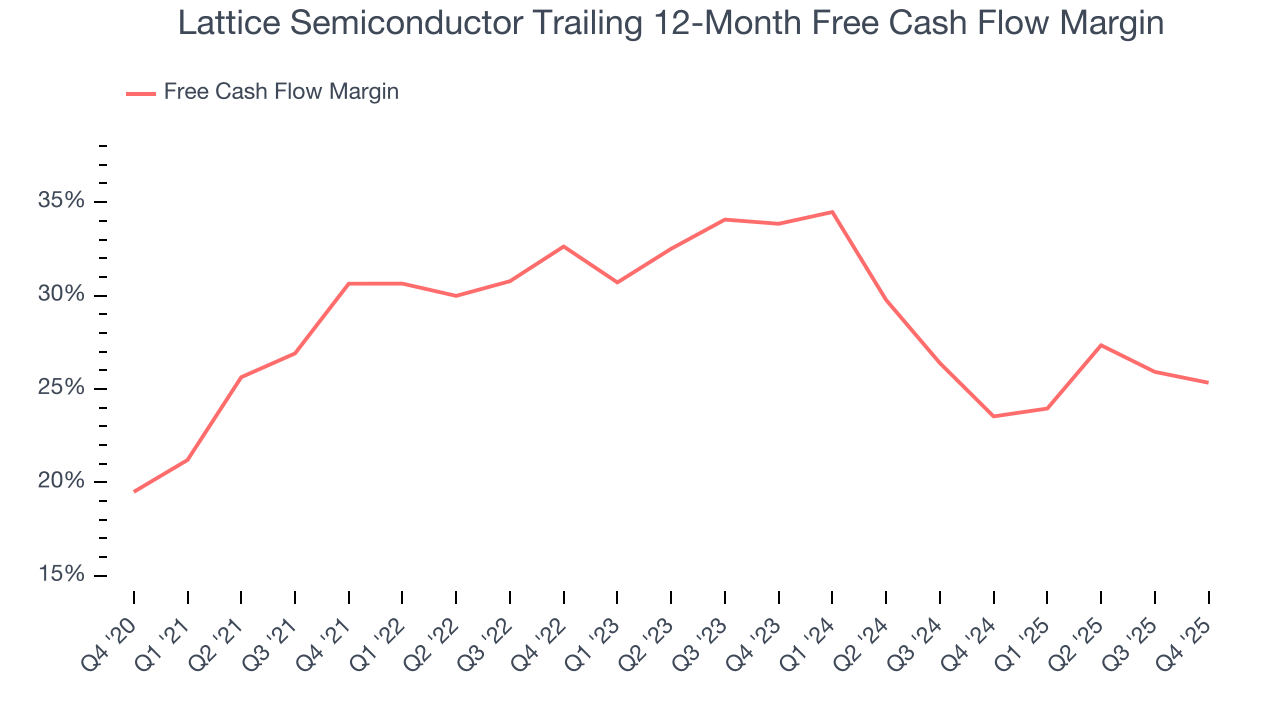

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Lattice Semiconductor has shown robust cash profitability, and if it can maintain this level of cash generation, will be in a fine position to ride out cyclical downturns while investing in plenty of new products and returning capital to investors. The company’s free cash flow margin averaged 24.4% over the last two years, quite impressive for a semiconductor business.

Taking a step back, we can see that Lattice Semiconductor’s margin dropped by 5.3 percentage points over the last five years. Continued declines could signal it is in the middle of an investment cycle.

Lattice Semiconductor’s free cash flow clocked in at $43.98 million in Q4, equivalent to a 30.2% margin. The company’s cash profitability regressed as it was 3.6 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, leading to short-term swings. Long-term trends trump temporary fluctuations.

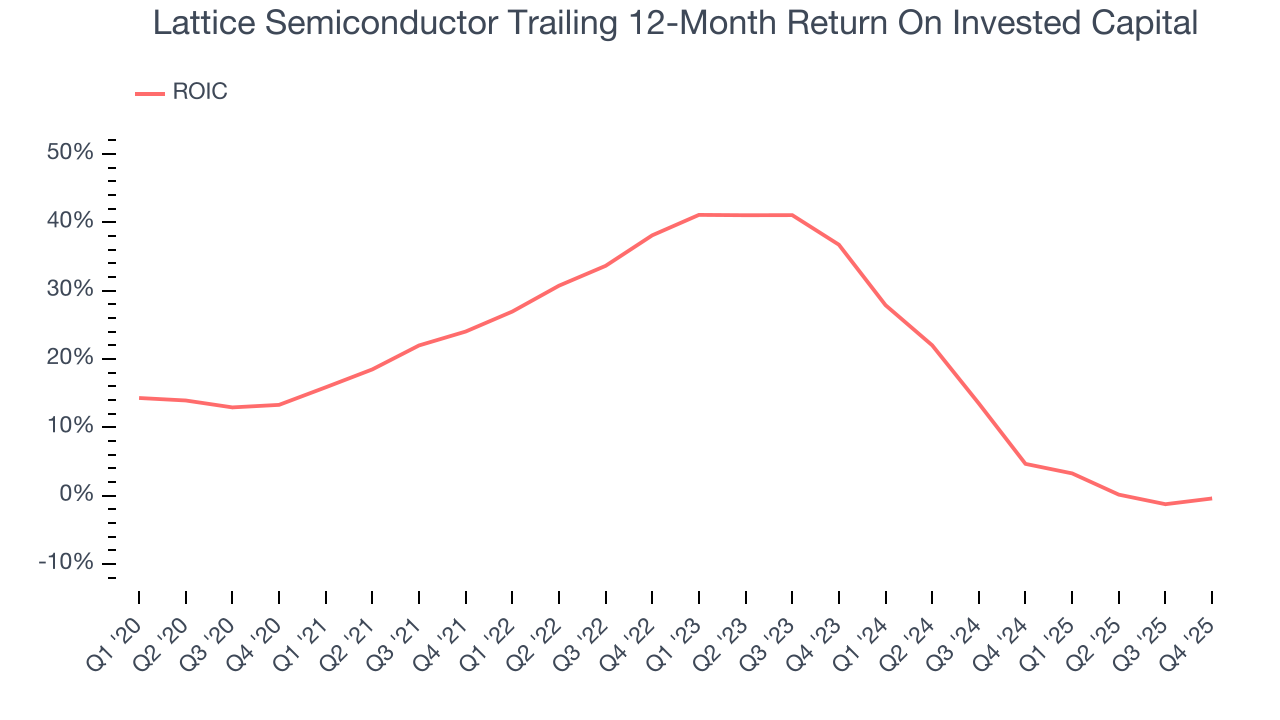

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Lattice Semiconductor’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 20.6%, slightly better than typical semiconductor business.

11. Balance Sheet Assessment

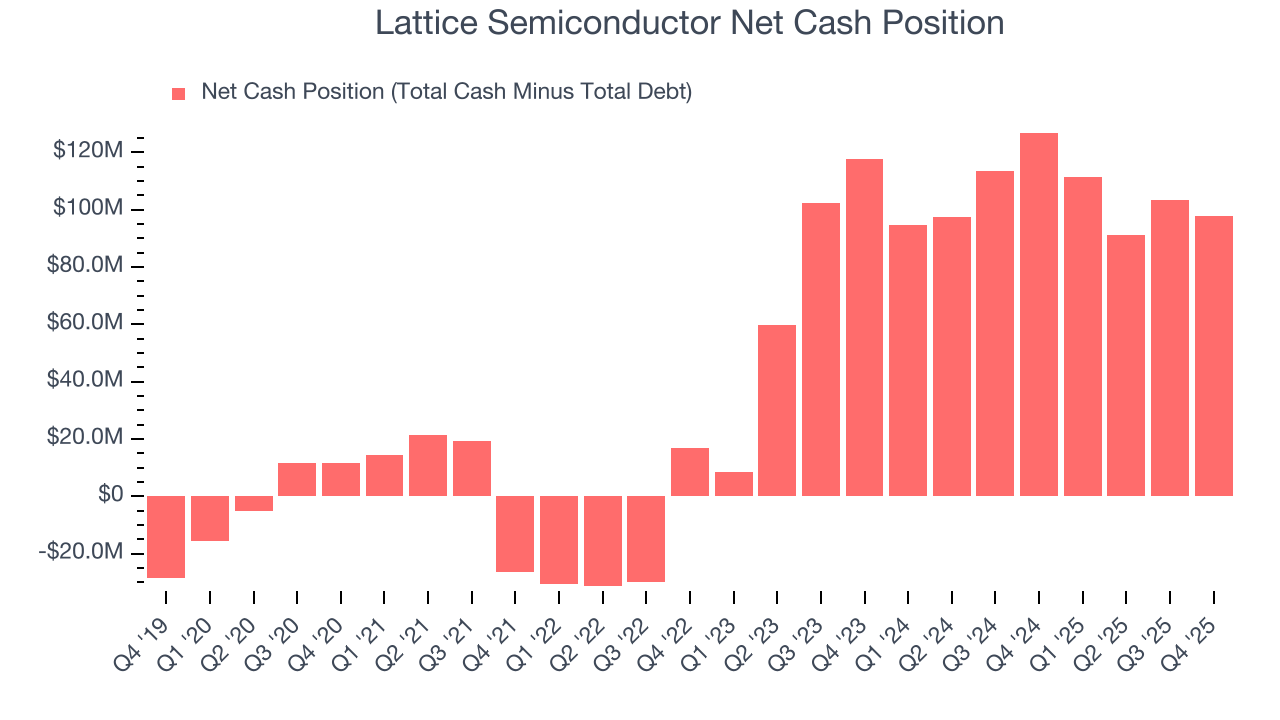

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Lattice Semiconductor is a profitable, well-capitalized company with $133.9 million of cash and $36.13 million of debt on its balance sheet. This $97.76 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Lattice Semiconductor’s Q4 Results

We were impressed by Lattice Semiconductor’s optimistic revenue and EPS guidance for next quarter, both of which exceeded analysts’ expectations. We were also glad its revenue in the quarter beat and inventory levels shrunk. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $94.27 immediately following the results.

13. Is Now The Time To Buy Lattice Semiconductor?

Updated: March 15, 2026 at 10:39 PM EDT

Before investing in or passing on Lattice Semiconductor, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Lattice Semiconductor has a few positive attributes, but it doesn’t top our wishlist. Although its revenue growth was mediocre over the last five years, its growth over the next 12 months is expected to be higher. And while Lattice Semiconductor’s declining operating margin shows the business has become less efficient, its admirable gross margins indicate robust pricing power.

Lattice Semiconductor’s P/E ratio based on the next 12 months is 55.4x. Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $114.71 on the company (compared to the current share price of $85.72).