Meta (META)

Not many stocks excite us like Meta. Its fusion of growth, outstanding profitability, and encouraging prospects makes it a beloved asset.― StockStory Analyst Team

1. News

2. Summary

Why We Like Meta

Famously founded by Mark Zuckerberg in his Harvard dorm, Meta Platforms (NASDAQ:META) operates a collection of the largest social networks in the world - Facebook, Instagram, WhatsApp, and Messenger, along with its metaverse focused Reality Labs.

- Disciplined cost controls and effective management have materialized in a strong EBITDA margin, and it turbocharged its profits by achieving some fixed cost leverage

- Strong free cash flow margin of 26.2% gives it the option to reinvest, repurchase shares, or pay dividends, and its improved cash conversion implies it’s becoming a less capital-intensive business

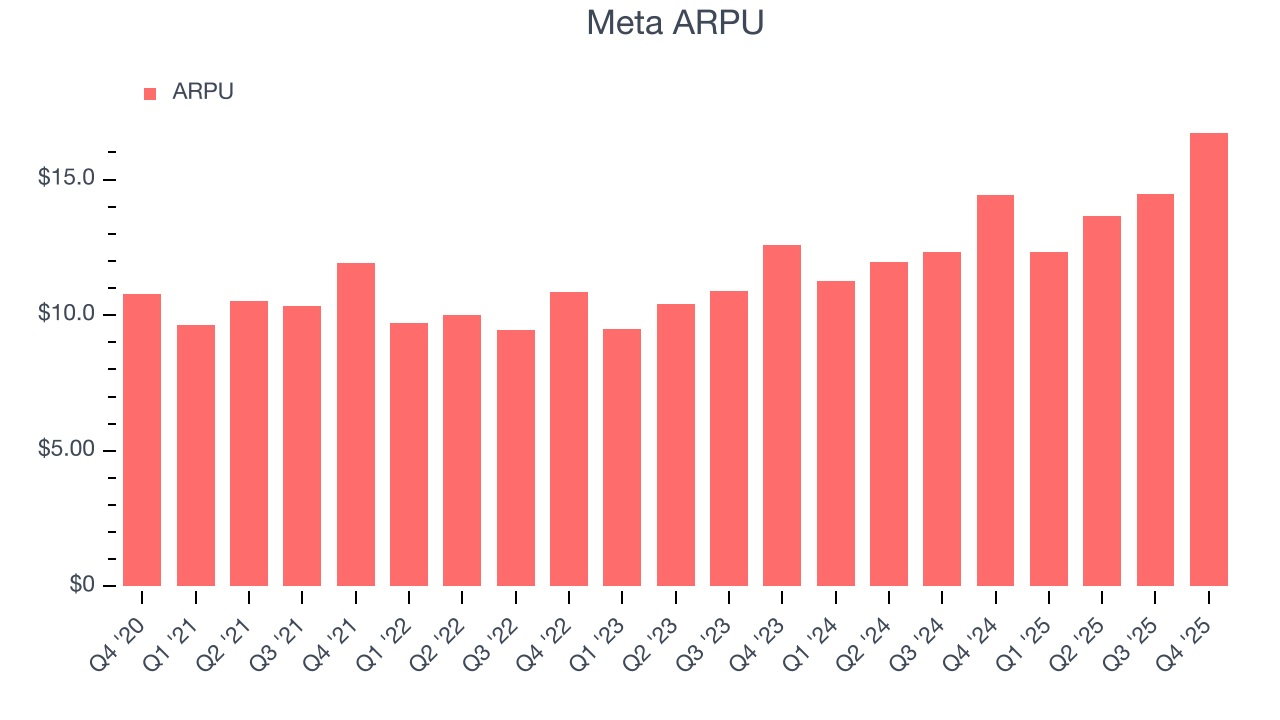

- Customers are spending more money on its platform as its average revenue per user has increased by 29.9% annually over the last two years

We’re fond of companies like Meta. The valuation seems fair based on its quality, and we think now is a prudent time to buy.

Why Is Now The Time To Buy Meta?

Meta is trading at $610.90 per share, or 11.5x forward EV/EBITDA. This valuation is fair - even cheap depending on how much you like the story - for the quality you get.

By definition, where you buy a stock impacts returns. Compared to entry price, business quality matters much more for long-term market outperformance. Buying in at a great price helps, nevertheless.

3. Meta (META) Research Report: Q4 CY2025 Update

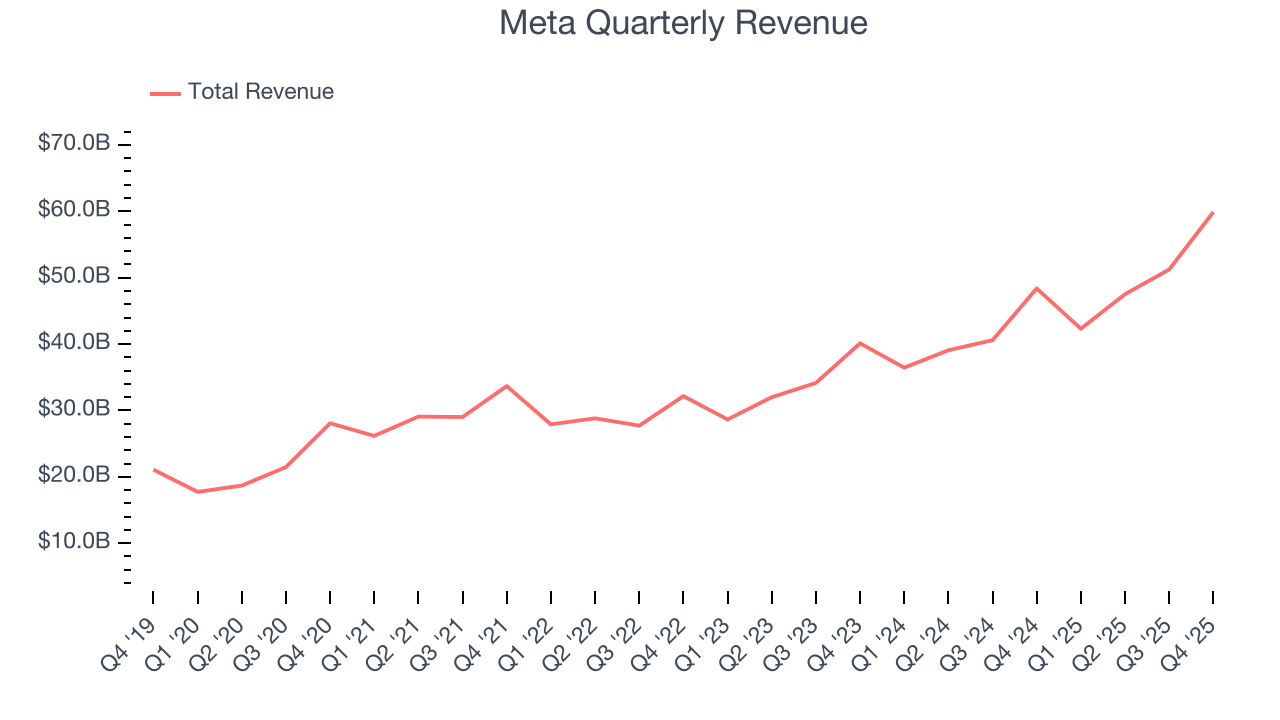

Social network operator Meta Platforms (NASDAQ:META) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 23.8% year on year to $59.89 billion. On top of that, next quarter’s revenue guidance ($55 billion at the midpoint) was surprisingly good and 7.1% above what analysts were expecting. Its GAAP profit of $8.88 per share was 8% above analysts’ consensus estimates.

Meta (META) Q4 CY2025 Highlights:

- Revenue: $59.89 billion vs analyst estimates of $58.45 billion (23.8% year-on-year growth, 2.5% beat)

- EPS (GAAP): $8.88 vs analyst estimates of $8.22 (8% beat)

- Adjusted EBITDA: $36.05 billion vs analyst estimates of $35.09 billion (60.2% margin, 2.7% beat)

- Revenue Guidance for Q1 CY2026 is $55 billion at the midpoint, above analyst estimates of $51.34 billion

- Operating Margin: 41.3%, down from 48.3% in the same quarter last year

- Free Cash Flow Margin: 23.5%, up from 20.7% in the previous quarter

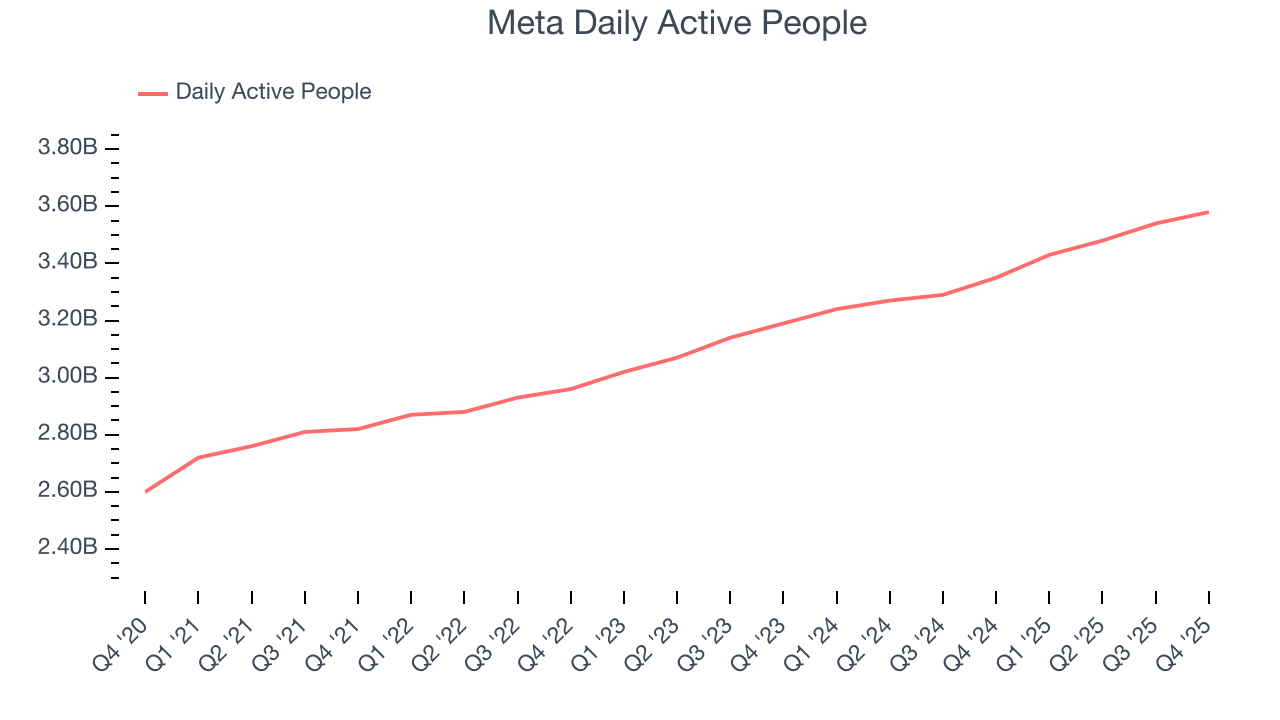

- Daily Active People: 3.58 billion, up 230 million year on year (slight beat)

- Market Capitalization: $1.70 trillion

Company Overview

Famously founded by Mark Zuckerberg in his Harvard dorm, Meta Platforms (NASDAQ:META) operates a collection of the largest social networks in the world - Facebook, Instagram, WhatsApp, and Messenger, along with its metaverse focused Reality Labs.

The need for connection is foundational to human experience and remains the driver of Meta’s mission. Through its platforms, users can connect, share, discover, and communicate with family and friends on almost any connected device. Its massive global aggregated audience of over 3 billion users spends over two hours daily on its properties.

Meta’s innovative digital ad tools, scale, and demographic data have also transformed how businesses operate, allowing a much more granular targeted approach to interacting with consumers. Its high return on investment advertising tools have allowed millions of new small businesses to spring up by aggregating potential customers online who were previously dispersed and hard to identify.

Meta’s product offerings to businesses have continued to evolve to include commerce and payment functionality. Long term, it's focused on creating new ad formats and ways for users to interact, as seen by its new product segment, Reality Labs, whose focus is to develop immersive technologies (AR/VR) that provide unique ways to socialize, work, shop, and game.

Consistent with its evolution, the company changed its name to Meta Platforms in October 2021 to signal its increased emphasis on building a new computing platform that will evolve how Meta connects people (and advertisers) from a place to share experiences to a place of shared experiences. In 2024, Meta reinvented itself once again by launching Meta AI, an artificial intelligence assistant integrated into its various platforms that helps users and content creators be more productive. The underlying technology powering Meta AI is the company's open-source large language model, Llama, which is a direct competitor to OpenAI/Microsoft's ChatGPT.

4. Social Networking

Businesses must meet their customers where they are, which over the past decade has come to mean on social networks. In 2020, users spent over 2.5 hours a day on social networks, a figure that has increased every year since measurement began. As a result, businesses continue to shift their advertising and marketing dollars online.

Meta Platforms competes with fellow social media advertising platforms like Google (NASDAQ:GOOGL), Snapchat (NYSE:SNAP), Twitter (NYSE:TWTR), and Pinterest (NASDAQ:PINS)

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Meta’s 19.9% annualized revenue growth over the last three years was impressive. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Meta reported robust year-on-year revenue growth of 23.8%, and its $59.89 billion of revenue topped Wall Street estimates by 2.5%. Company management is currently guiding for a 30% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 17.9% over the next 12 months, a slight deceleration versus the last three years. We still think its growth trajectory is attractive given its scale and implies the market is forecasting success for its products and services.

6. Daily Active People

User Growth

As a social network, Meta generates revenue growth by increasing its user base and charging advertisers more for the ads each user is shown.

Over the last two years, Meta’s daily active people, a key performance metric for the company, increased by 6.3% annually to 3.58 billion in the latest quarter. This growth rate is slightly below average for a consumer internet business and is largely a function of its already massive scale and penetrated market. If Meta wants to reach the next level, it likely needs to innovate with new products.

In Q4, Meta added 230 million daily active people, leading to 6.9% year-on-year growth. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Meta’s audience and its ad-targeting capabilities.

Meta’s ARPU growth has been exceptional over the last two years, averaging 14.8%. Its ability to increase monetization while growing its daily active people demonstrates its platform’s value, as its users are spending significantly more than last year.

This quarter, Meta’s ARPU clocked in at $16.73. It grew by 15.8% year on year, faster than its daily active people.

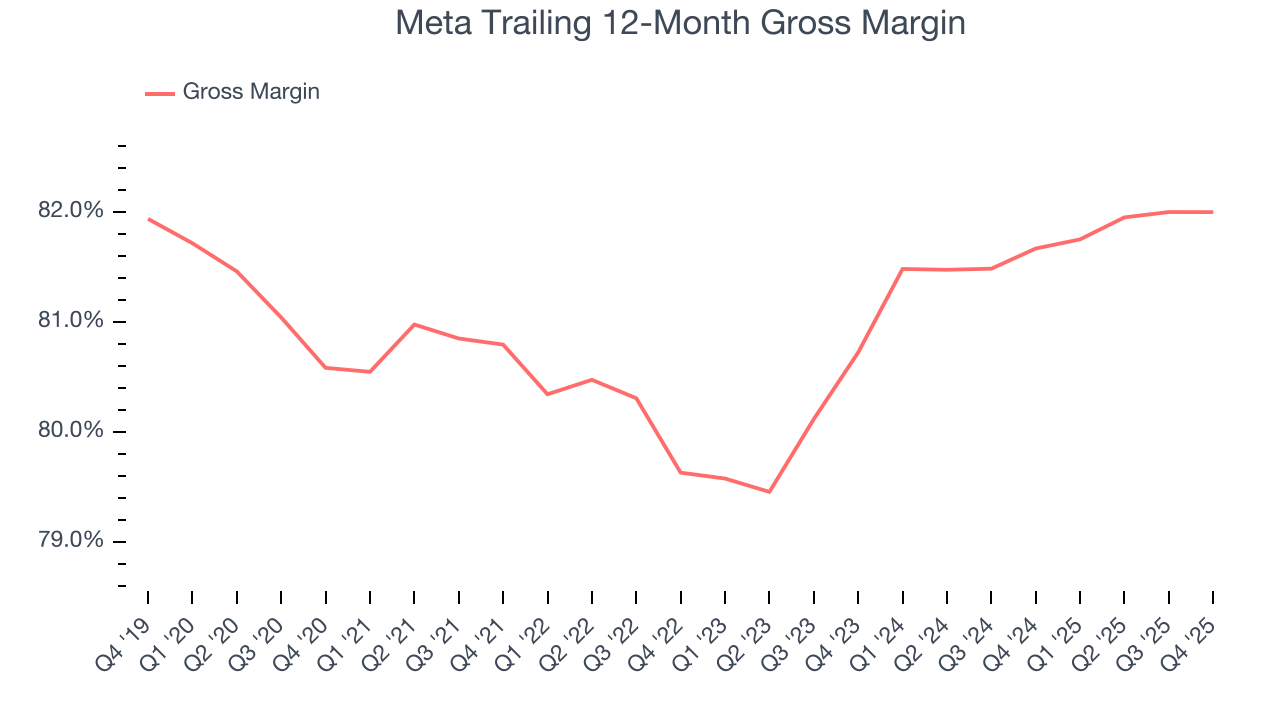

7. Gross Margin & Pricing Power

A company’s gross profit margin has a significant impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors can determine the winner in a competitive market.

For social network businesses like Meta, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include customer service, data center, and other infrastructure expenses.

Meta’s gross margin is one of the best in the consumer internet sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 81.9% gross margin over the last two years. Said differently, roughly $81.85 was left to spend on selling, marketing, and R&D for every $100 in revenue.

Meta produced a 81.8% gross profit margin in Q4, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

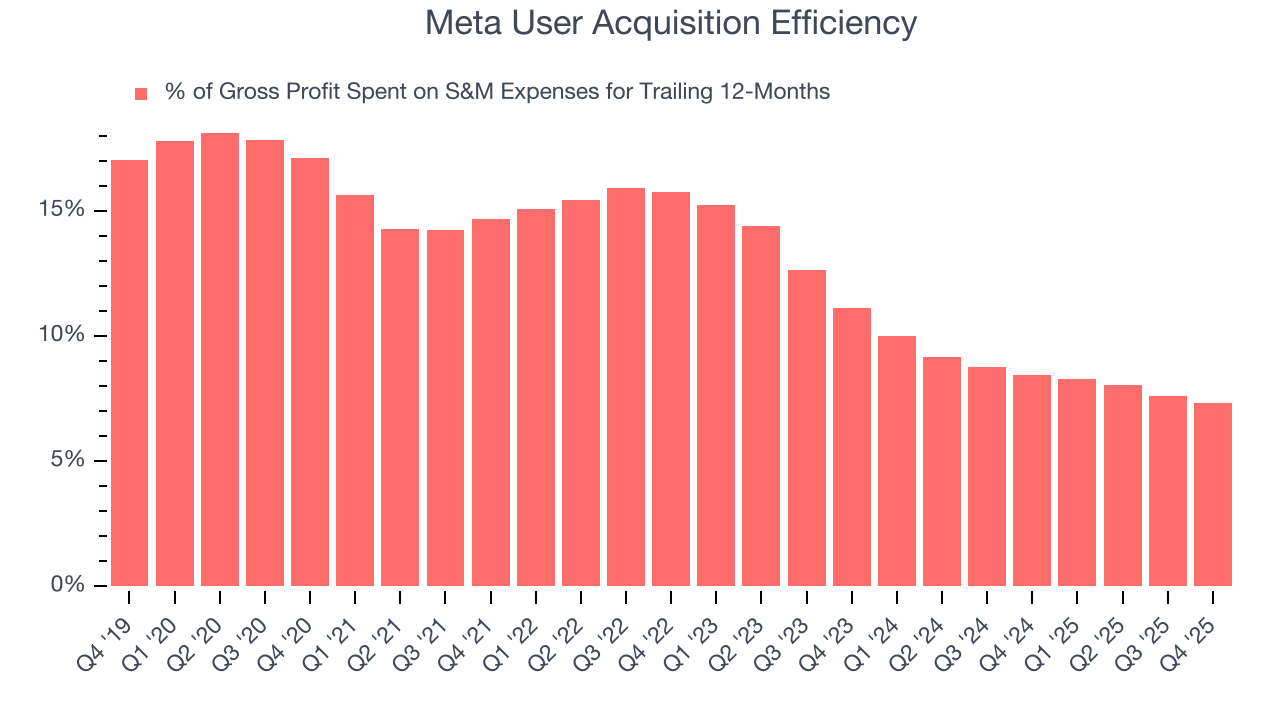

8. User Acquisition Efficiency

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like Meta grow from a combination of product virality, paid advertisement, and incentives.

Meta is extremely efficient at acquiring new users, spending only 7.3% of its gross profit on sales and marketing expenses over the last year. This efficiency indicates that it has a highly differentiated product offering and strong brand reputation from scale, giving Meta the freedom to invest its resources into new growth initiatives while maintaining optionality.

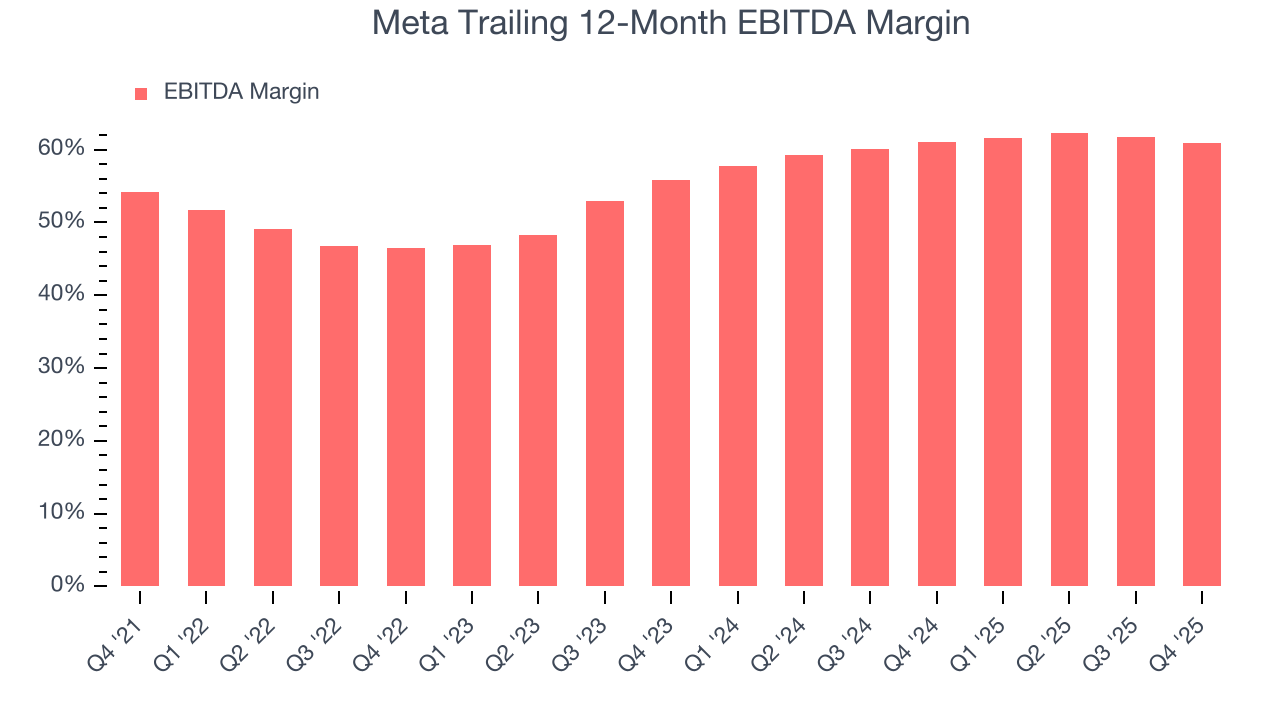

9. EBITDA

Meta has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer internet business, boasting an average EBITDA margin of 60.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Meta’s EBITDA margin rose by 14.4 percentage points over the last few years, as its sales growth gave it operating leverage.

This quarter, Meta generated an EBITDA margin profit margin of 60.2%, down 3.1 percentage points year on year. Since Meta’s EBITDA margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

10. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

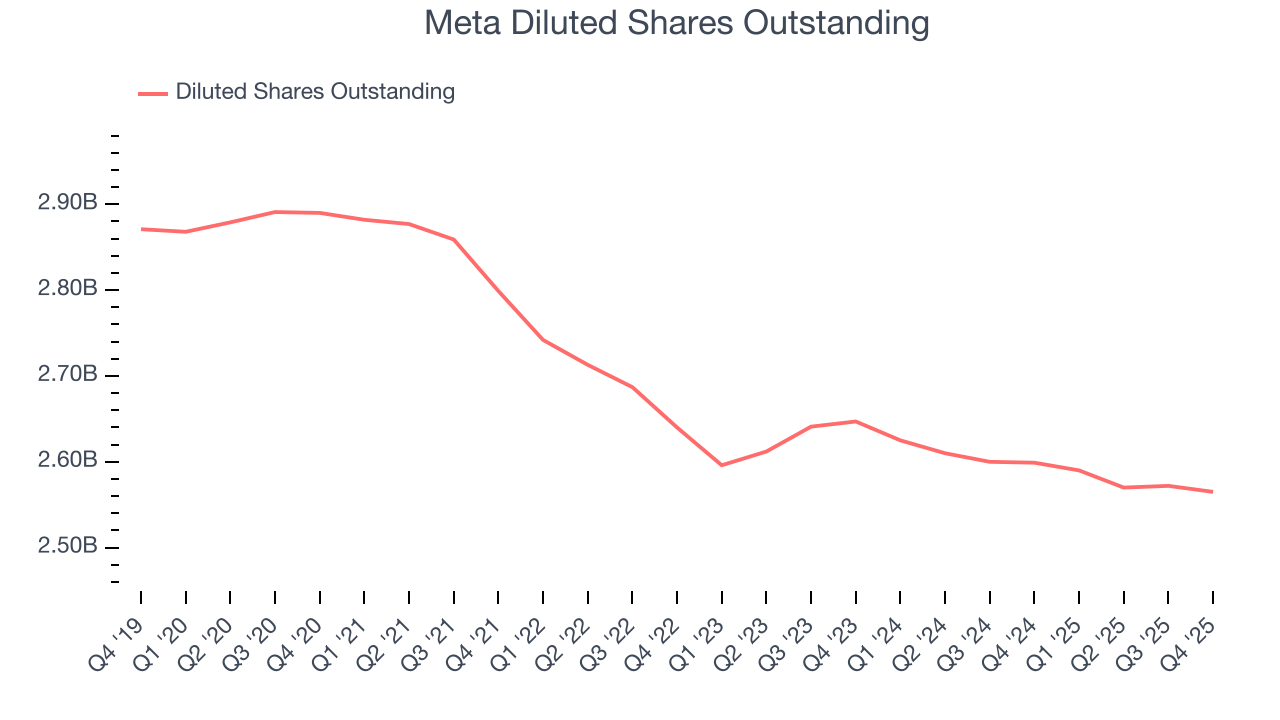

Meta’s EPS grew at an astounding 39.9% compounded annual growth rate over the last three years, higher than its 19.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Meta’s earnings to better understand the drivers of its performance. As we mentioned earlier, Meta’s EBITDA margin declined this quarter but expanded by 14.4 percentage points over the last three years. Its share count also shrank by 2.8%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q4, Meta reported EPS of $8.88, up from $8.02 in the same quarter last year. This print beat analysts’ estimates by 8%. Over the next 12 months, Wall Street expects Meta’s full-year EPS of $23.50 to grow 26.4%.

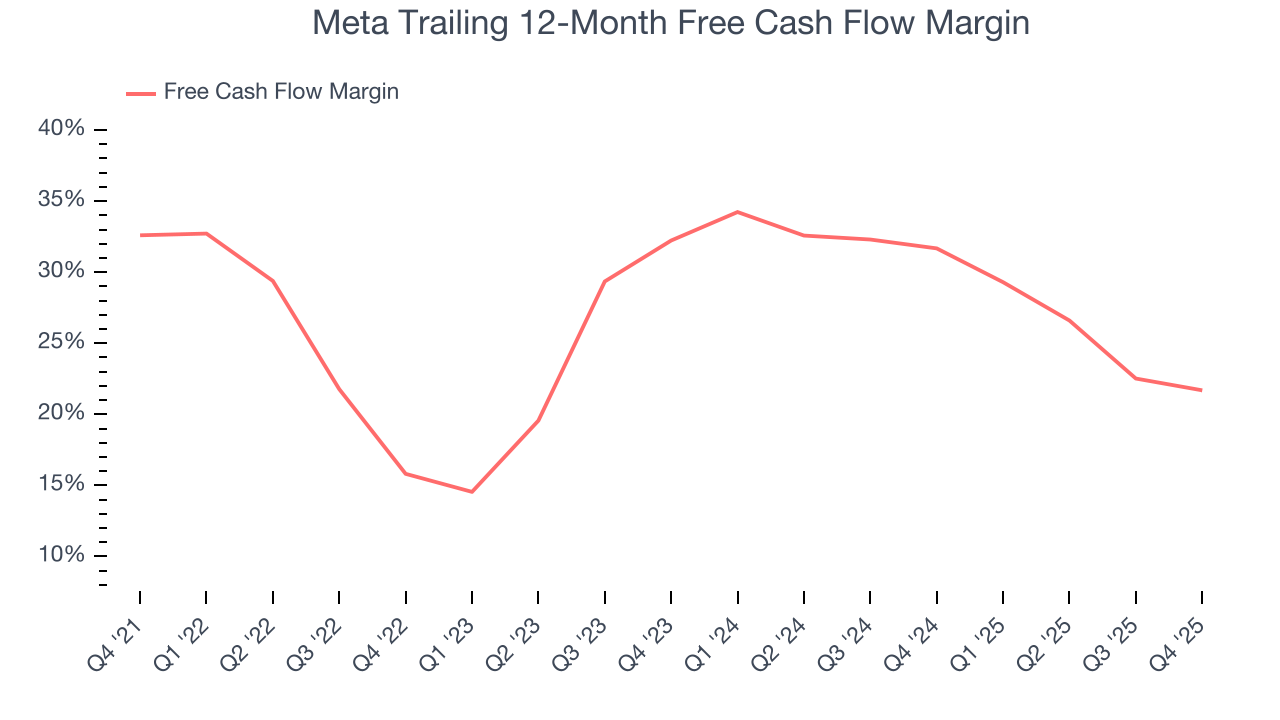

11. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Meta has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging 26.2% over the last two years.

Taking a step back, we can see that Meta’s margin expanded by 5.9 percentage points over the last few years. This is encouraging because it gives the company more optionality.

Meta’s free cash flow clocked in at $14.08 billion in Q4, equivalent to a 23.5% margin. The company’s cash profitability regressed as it was 3.7 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

12. Balance Sheet Assessment

Big corporations like Meta are attractive to many investors in times of instability thanks to their fortress balance sheets that buffer pockets of soft demand.

Meta has an eye-popping $81.59 billion of cash on its balance sheet (that’s no typo) compared to $58.74 billion of debt. This $22.85 billion net cash position is 1.3% of its market cap and shockingly larger than the value of most public companies, giving it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from Meta’s Q4 Results

We were impressed by Meta’s optimistic revenue guidance for next quarter, which blew past analysts’ expectations. As for the quarter, Daily Active People, revenue and EPS both outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 3.7% to $692.30 immediately following the results.

14. Is Now The Time To Buy Meta?

Updated: March 15, 2026 at 10:02 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Meta.

Meta is truly a cream-of-the-crop consumer internet company. For starters, its revenue growth was impressive over the last three years and is expected to accelerate over the next 12 months. And while its daily active users have declined, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits. On top of that, Meta’s impressive EBITDA margins show it has a highly efficient business model.

Meta’s EV/EBITDA ratio based on the next 12 months is 11.5x. Looking across the spectrum of consumer internet businesses, Meta’s fundamentals clearly illustrate it’s a special business. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $862.25 on the company (compared to the current share price of $610.90), implying they see 41.1% upside in buying Meta in the short term.