onsemi (ON)

We’re wary of onsemi. Its weak revenue growth and gross margin show it not only lacks demand but also decent unit economics.― StockStory Analyst Team

1. News

2. Summary

Why We Think onsemi Will Underperform

Spun out of Motorola in 1999 and built through a series of acquisitions, onsemi (NASDAQ:ON) is a global provider of analog chips specializing in autos, industrial applications, and power management in cloud data centers.

- Anticipated sales growth of 4.9% for the next year implies demand will be shaky

- High input costs result in an inferior gross margin of 40% that must be offset through higher volumes

- On the bright side, its earnings per share have outperformed the peer group average over the last five years, increasing by 22.8% annually

onsemi doesn’t meet our quality standards. There are superior opportunities elsewhere.

Why There Are Better Opportunities Than onsemi

onsemi is trading at $57.92 per share, or 19.8x forward P/E. onsemi’s valuation may seem like a bargain, especially when stacked up against other semiconductor companies. We remind you that you often get what you pay for, though.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. onsemi (ON) Research Report: Q4 CY2025 Update

Analog chips maker onsemi (NASDAQ:ON) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 11.2% year on year to $1.53 billion. On the other hand, next quarter’s revenue guidance of $1.49 billion was less impressive, coming in 1.4% below analysts’ estimates. Its non-GAAP profit of $0.64 per share was 2.5% above analysts’ consensus estimates.

onsemi (ON) Q4 CY2025 Highlights:

- Revenue: $1.53 billion vs analyst estimates of $1.54 billion (11.2% year-on-year decline, in line)

- Adjusted EPS: $0.64 vs analyst estimates of $0.62 (2.5% beat)

- Revenue Guidance for Q1 CY2026 is $1.49 billion at the midpoint, below analyst estimates of $1.51 billion

- Adjusted EPS guidance for Q1 CY2026 is $0.47 at the midpoint, below analyst estimates of $0.61

- Operating Margin: 13.1%, down from 23.7% in the same quarter last year

- Free Cash Flow Margin: 31.7%, up from 24.5% in the same quarter last year

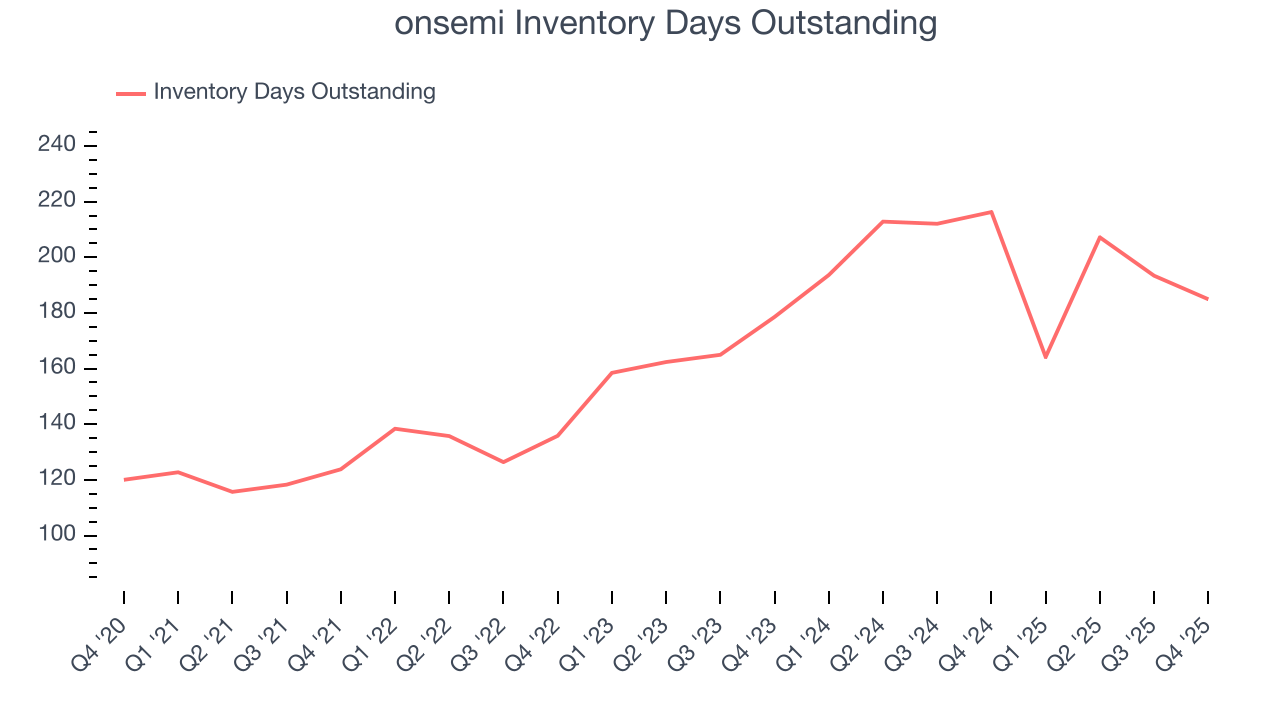

- Inventory Days Outstanding: 185, down from 193 in the previous quarter

- Market Capitalization: $26.24 billion

Company Overview

Spun out of Motorola in 1999 and built through a series of acquisitions, onsemi (NASDAQ:ON) is a global provider of analog chips specializing in autos, industrial applications, and power management in cloud data centers.

The company's business is organized into three segments that address different market needs. The Power Solutions Group (PSG) produces components like silicon carbide products, discrete semiconductors, and power modules that manage electricity flow in devices. These components are crucial for electric vehicles, solar energy systems, and data centers, where efficient power management directly impacts performance and energy consumption. The Advanced Solutions Group (ASG) creates analog and mixed-signal products that interface between the physical and digital worlds, converting real-world signals into digital data. The Intelligent Sensing Group (ISG) develops imaging sensors and processors that enable machines to "see" their environment.

In automotive applications, onsemi's technologies power electric vehicle drivetrains, enabling longer range and faster charging. A car manufacturer might use the company's silicon carbide power modules to increase the efficiency of its electric motors, extending driving range while reducing battery size and weight. In industrial settings, onsemi's sensors and power management solutions support factory automation, with components that enable precise motor control in robotic systems or image sensors that allow machines to identify and manipulate objects.

The company generates revenue primarily through semiconductor sales to both distributors (about 53% of revenue) and direct customers (47%). Its global manufacturing and logistics network allows customers to source multiple components from a single supplier, simplifying their supply chains. Beyond component sales, onsemi offers product development services and custom solutions, though these represent a smaller portion of its business.

onsemi’s peers and competitors include Analog Devices (NASDAQ:ADI), Texas Instruments (NASDAQ:TXN), Skyworks (NASDAQ:SWKS), Infineon (XTRA:IFX), NXP Semiconductors NV (NASDAQ:NXPI), Monolithic Power Systems (NASDAQ:MPWR), Marvell Technology (NASDAQ:MRVL), and Microchip (NASDAQ:MCHP).

4. Analog Semiconductors

Longer manufacturing duration allows analog chip makers to generate greater efficiencies, leading to structurally higher gross margins than their fabless digital peers. The downside of vertical integration is that cyclicality can be more pronounced for analog chipmakers, as capacity utilization upsides work in reverse during down periods.

5. Revenue Growth

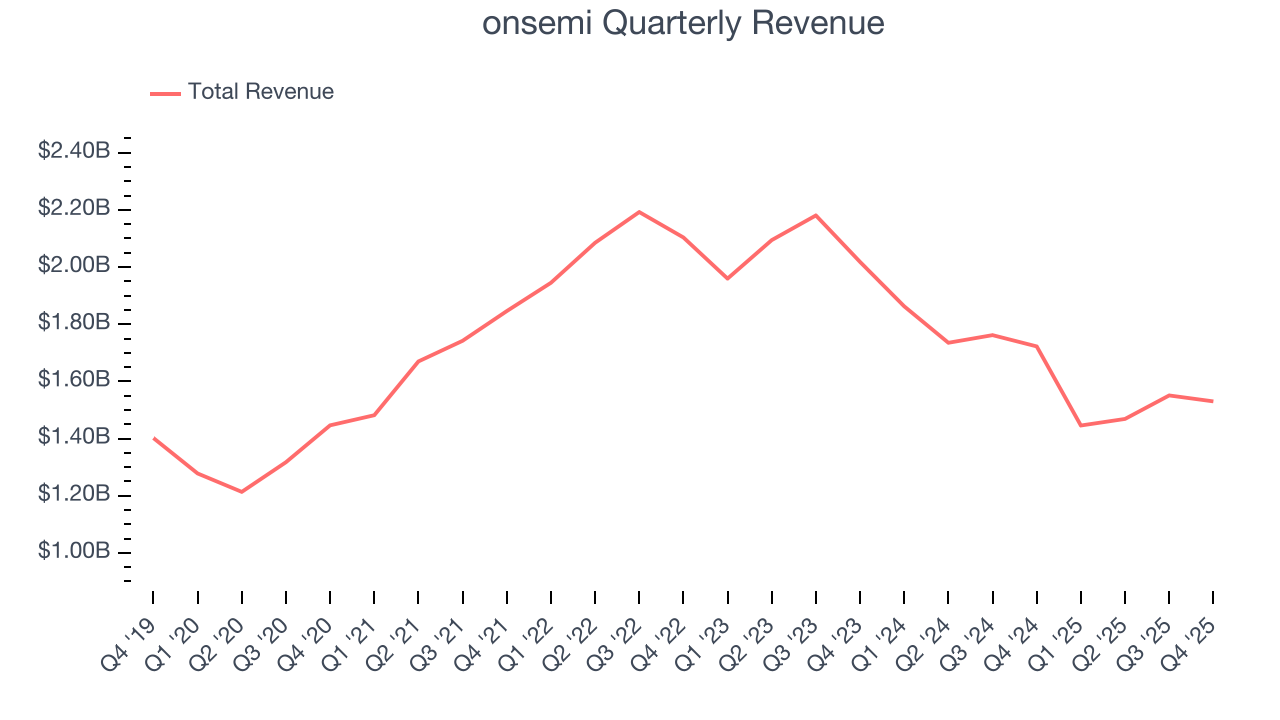

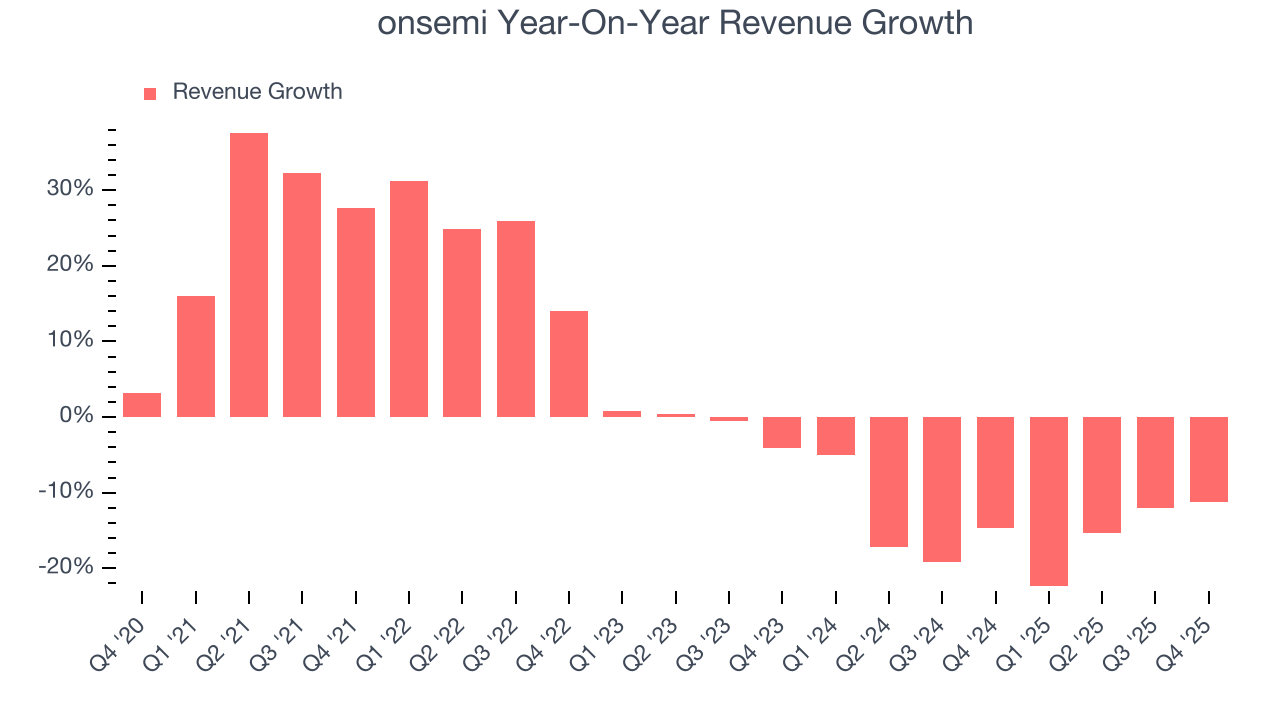

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, onsemi grew its sales at a tepid 2.7% compounded annual growth rate. This was below our standards and is a poor baseline for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. onsemi’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 14.8% annually.

This quarter, onsemi reported a rather uninspiring 11.2% year-on-year revenue decline to $1.53 billion of revenue, in line with Wall Street’s estimates. Despite meeting estimates, the drop in sales could mean that the current downcycle is deepening. Company management is currently guiding for a 2.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.5% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

6. Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, onsemi’s DIO came in at 185, which is 22 days above its five-year average. These numbers suggest that despite the recent decrease, the company’s inventory levels are higher than what we’ve seen in the past.

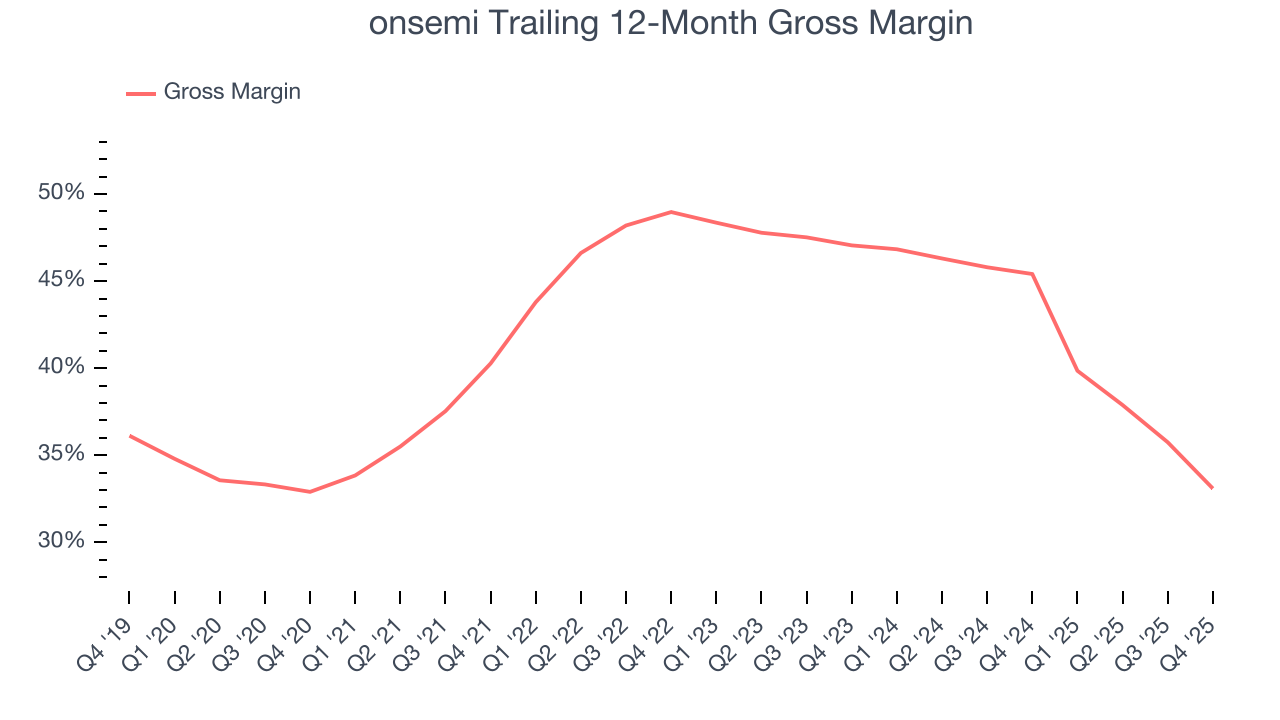

7. Gross Margin & Pricing Power

In the semiconductor industry, a company’s gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

onsemi’s gross margin is well below other semiconductor companies, indicating a lack of pricing power and a competitive market. As you can see below, it averaged a 39.8% gross margin over the last two years. Said differently, onsemi had to pay a chunky $60.24 to its suppliers for every $100 in revenue.

onsemi’s gross profit margin came in at 36% this quarter, down 9.2 percentage points year on year. onsemi’s full-year margin has also been trending down over the past 12 months, decreasing by 12.3 percentage points. If this move continues, it could suggest deteriorating pricing power and higher input costs (such as raw materials and manufacturing expenses).

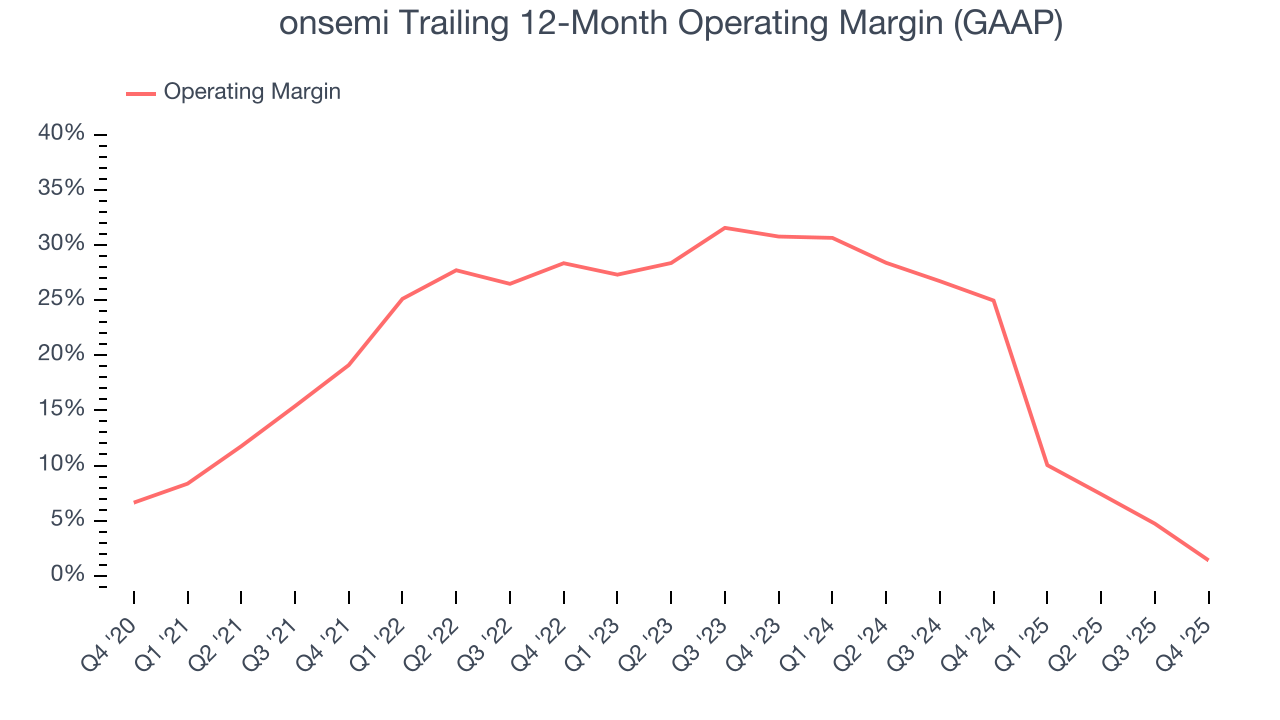

8. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

onsemi has done a decent job managing its cost base over the last two years. The company has produced an average operating margin of 14.2%, higher than the broader semiconductor sector.

Looking at the trend in its profitability, onsemi’s operating margin decreased by 17.7 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, onsemi generated an operating margin profit margin of 13.1%, down 10.6 percentage points year on year. Since onsemi’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

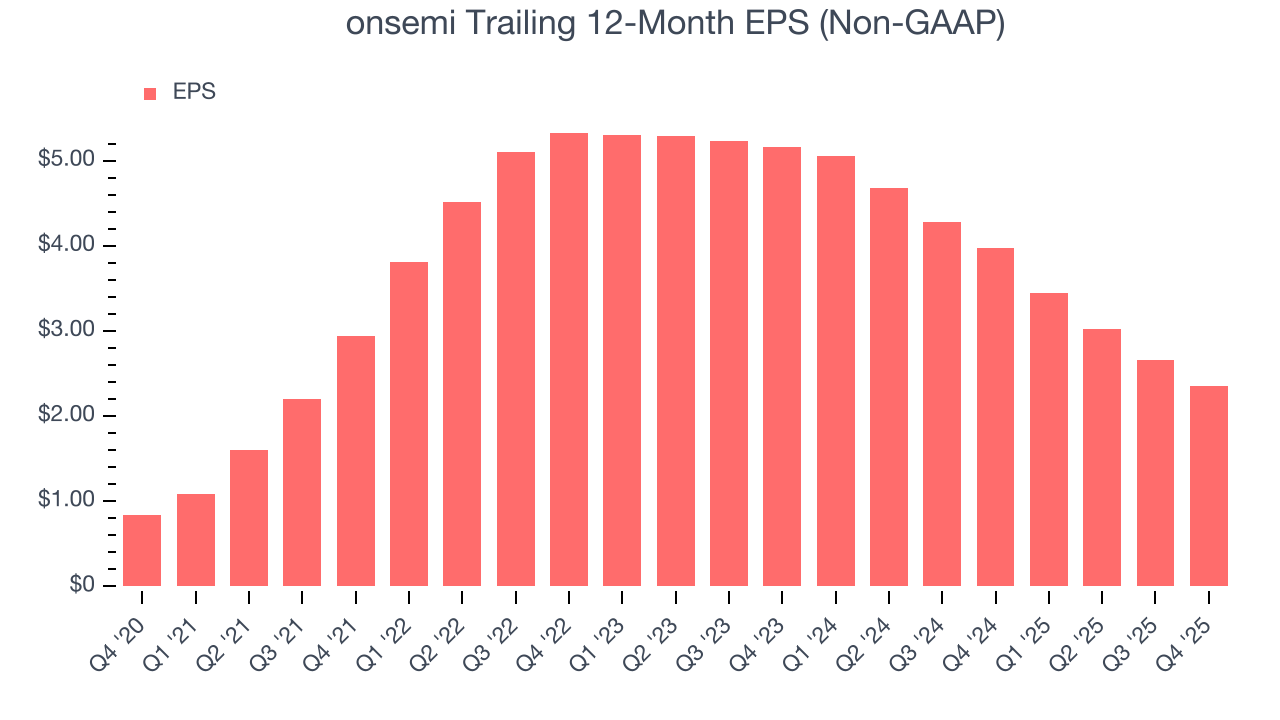

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

onsemi’s EPS grew at a remarkable 22.8% compounded annual growth rate over the last five years, higher than its 2.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into onsemi’s earnings to better understand the drivers of its performance. A five-year view shows that onsemi has repurchased its stock, shrinking its share count by 6.8%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, onsemi reported adjusted EPS of $0.64, down from $0.95 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 2.5%. Over the next 12 months, Wall Street expects onsemi’s full-year EPS of $2.35 to grow 24%.

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

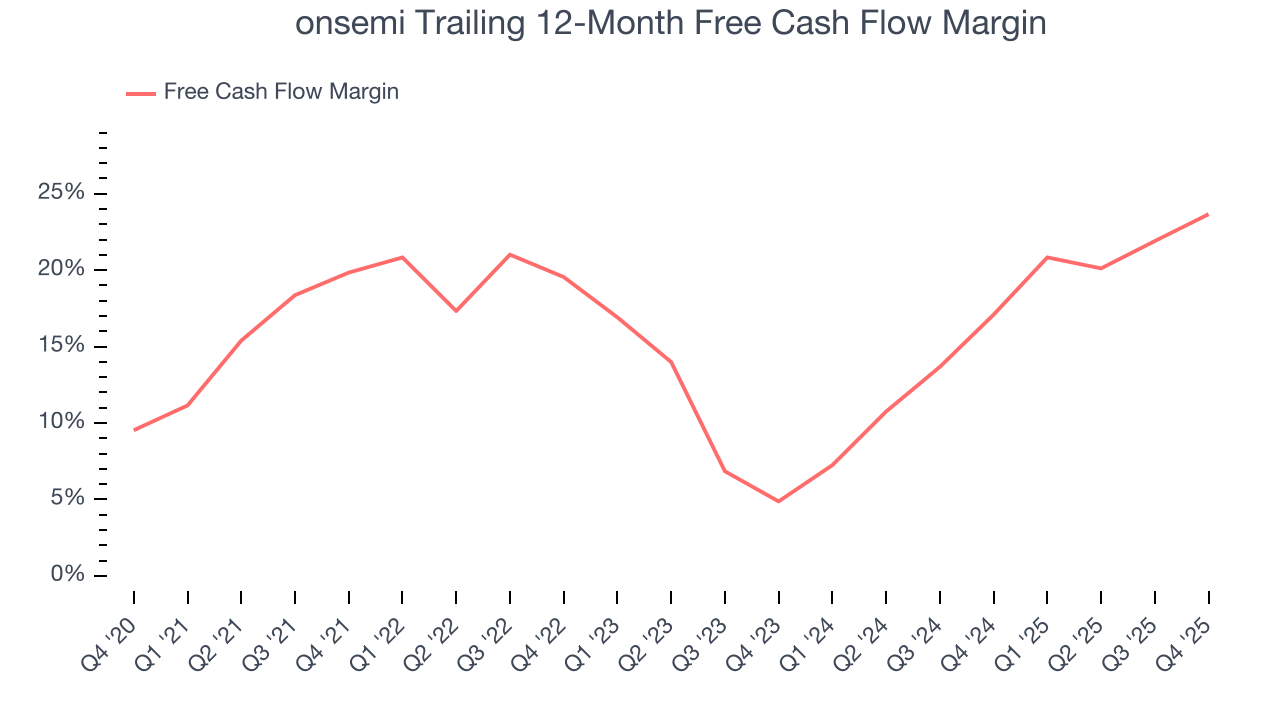

onsemi has shown impressive cash profitability, and if maintainable, will be in a position to ride out cyclical downturns more easily while continuing to invest in new and existing products. The company’s free cash flow margin averaged 20.1% over the last two years, better than the broader semiconductor sector.

Taking a step back, we can see that onsemi’s margin expanded by 3.8 percentage points over the last five years. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

onsemi’s free cash flow clocked in at $485.4 million in Q4, equivalent to a 31.7% margin. This result was good as its margin was 7.2 percentage points higher than in the same quarter last year, building on its favorable historical trend.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

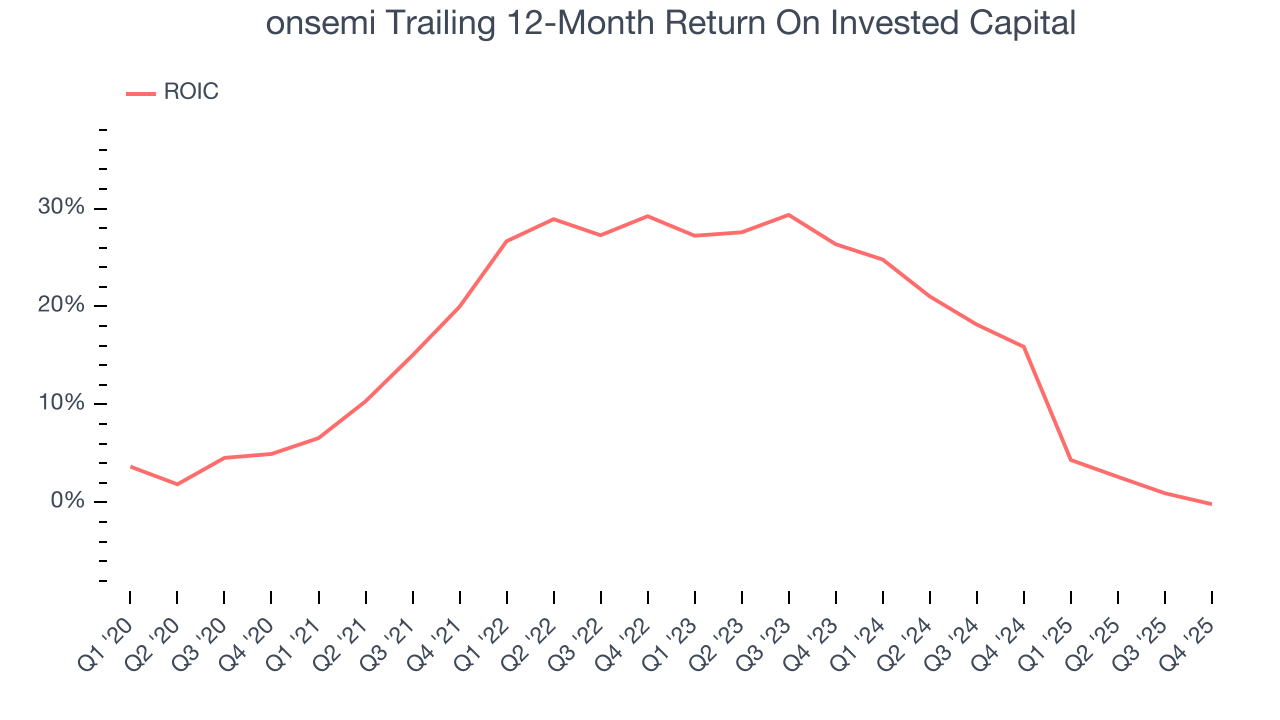

onsemi’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 18.3%, slightly better than typical semiconductor business.

12. Balance Sheet Assessment

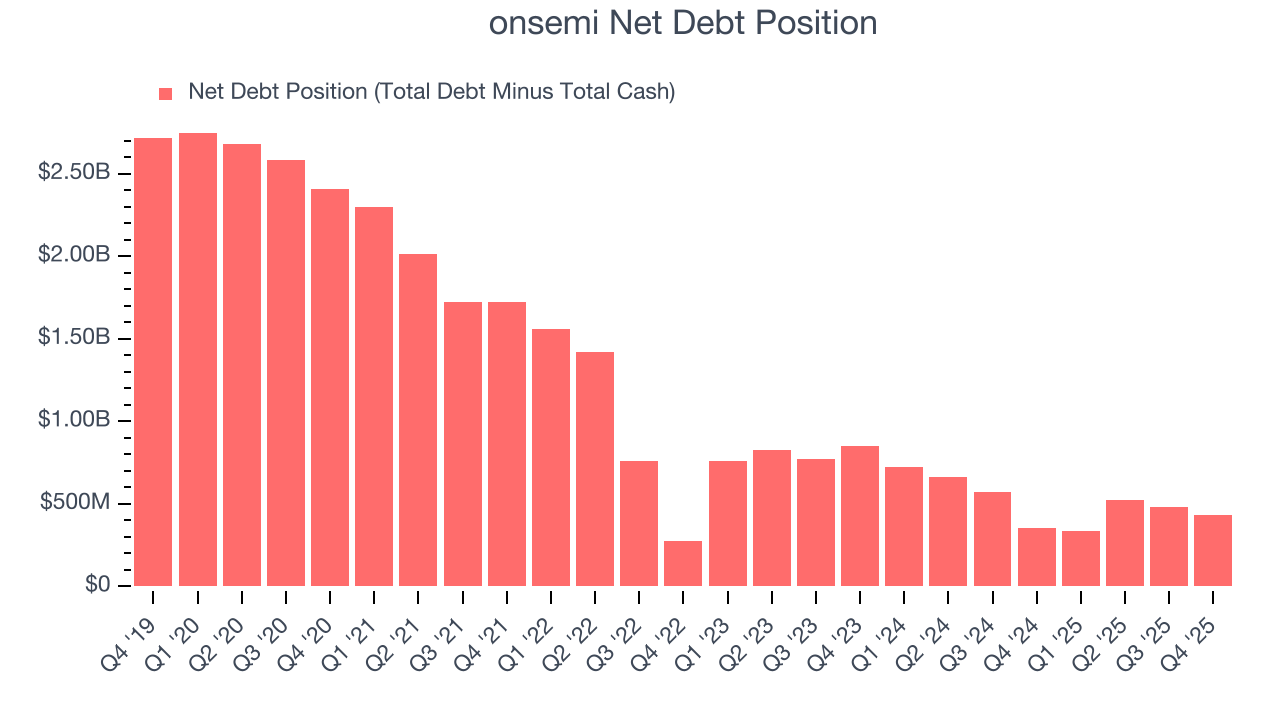

onsemi reported $2.55 billion of cash and $2.98 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.81 billion of EBITDA over the last 12 months, we view onsemi’s 0.2× net-debt-to-EBITDA ratio as safe. We also see its $17.6 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from onsemi’s Q4 Results

A highlight during the quarter was onsemi’s improvement in inventory levels. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter slightly missed and its revenue was in line with Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4.6% to $62.23 immediately following the results.

14. Is Now The Time To Buy onsemi?

Updated: March 15, 2026 at 10:29 PM EDT

Are you wondering whether to buy onsemi or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

onsemi isn’t a terrible business, but it isn’t one of our picks. To kick things off, its revenue growth was uninspiring over the last five years. While its remarkable EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its declining operating margin shows the business has become less efficient. On top of that, its gross margins are lower than its semiconductor peers.

onsemi’s P/E ratio based on the next 12 months is 19.8x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $67.28 on the company (compared to the current share price of $57.92).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.