The Real Brokerage (REAX)

We wouldn’t buy The Real Brokerage. Its growth has decelerated and its failure to generate meaningful free cash flow makes us question its prospects.― StockStory Analyst Team

1. News

2. Summary

Why We Think The Real Brokerage Will Underperform

Founded in Toronto, Canada in 2014, The Real Brokerage (NASDAQ:REAX) is a technology-driven real estate brokerage firm combining a tech-centric model with an agent-centric philosophy.

- Earnings growth underperformed the sector average over the last four years as its EPS grew by just 8.9% annually

- Operating margin falls short of the industry average, and the smaller profit dollars make it harder to react to unexpected market developments

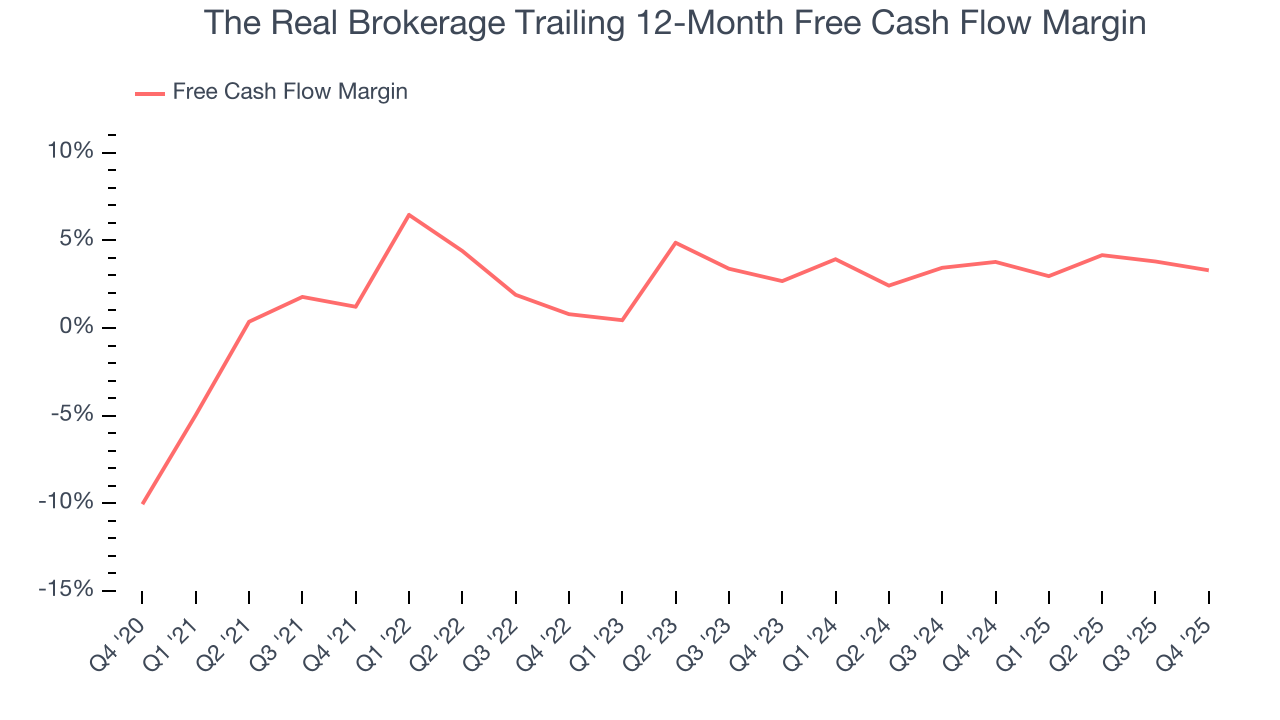

- Low free cash flow margin gives it little breathing room, constraining its ability to self-fund growth or return capital to shareholders

The Real Brokerage’s quality is lacking. We’re redirecting our focus to better businesses.

Why There Are Better Opportunities Than The Real Brokerage

At $2.37 per share, The Real Brokerage trades at 6.2x forward EV-to-EBITDA. The current valuation may be fair, but we’re still passing on this stock due to better alternatives out there.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. The Real Brokerage (REAX) Research Report: Q4 CY2025 Update

Real estate technology company The Real Brokerage (NASDAQ:REAX) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 44.1% year on year to $505.1 million. Its GAAP loss of $0.02 per share was $0.01 above analysts’ consensus estimates.

The Real Brokerage (REAX) Q4 CY2025 Highlights:

- Revenue: $505.1 million vs analyst estimates of $469.5 million (44.1% year-on-year growth, 7.6% beat)

- EPS (GAAP): -$0.02 vs analyst estimates of -$0.03 ($0.01 beat)

- Adjusted EBITDA: $14.16 million vs analyst estimates of $10.63 million (2.8% margin, 33.2% beat)

- Operating Margin: -1%, in line with the same quarter last year

- Free Cash Flow was -$16,000, down from $4 million in the same quarter last year

- Market Capitalization: $577.9 million

Company Overview

Founded in Toronto, Canada in 2014, The Real Brokerage (NASDAQ:REAX) is a technology-driven real estate brokerage firm combining a tech-centric model with an agent-centric philosophy.

Unlike traditional brokerages that often rely on physical office spaces, The Real Brokerage operates an online platform. This approach significantly reduces overhead costs and enables the company to offer more competitive commission splits to its agents with equity incentives, fostering a more collaborative and rewarding environment.

The company's platform provides agents with tools and resources to streamline their workflows, from marketing and lead generation to transaction management. These tools facilitate efficient communication and transaction processing, allowing agents to focus more on client service and less on administrative tasks.

The Real Brokerage's growth strategy has been marked by expansion across the United States and Canada. The company places a strong emphasis on providing continuous training, professional development opportunities, and supportive leadership to help agents grow their businesses.

4. Consumer Discretionary - Real Estate Services

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Real estate services companies provide brokerage, property management, appraisal, and advisory services, earning transaction-based commissions and recurring management fees. Tailwinds include long-term housing demand driven by demographic growth, technology platforms that expand market access, and commercial real estate complexity that sustains advisory needs. Headwinds are pronounced: rising interest rates directly suppress transaction volumes by reducing housing affordability and commercial deal activity. Commission-rate compression, driven by discount brokerages and regulatory changes, erodes per-transaction revenue. The industry is highly cyclical, with revenue swings amplified by leverage. PropTech (property technology) disruptors threaten traditional intermediary models.

The Real Brokerage’s primary competitors include eXp World (NASDAQ:EXPI), Redfin (NASDAQ:RDFN), Zillow (NASDAQ:ZG), and Compass (NYSE:COMP).

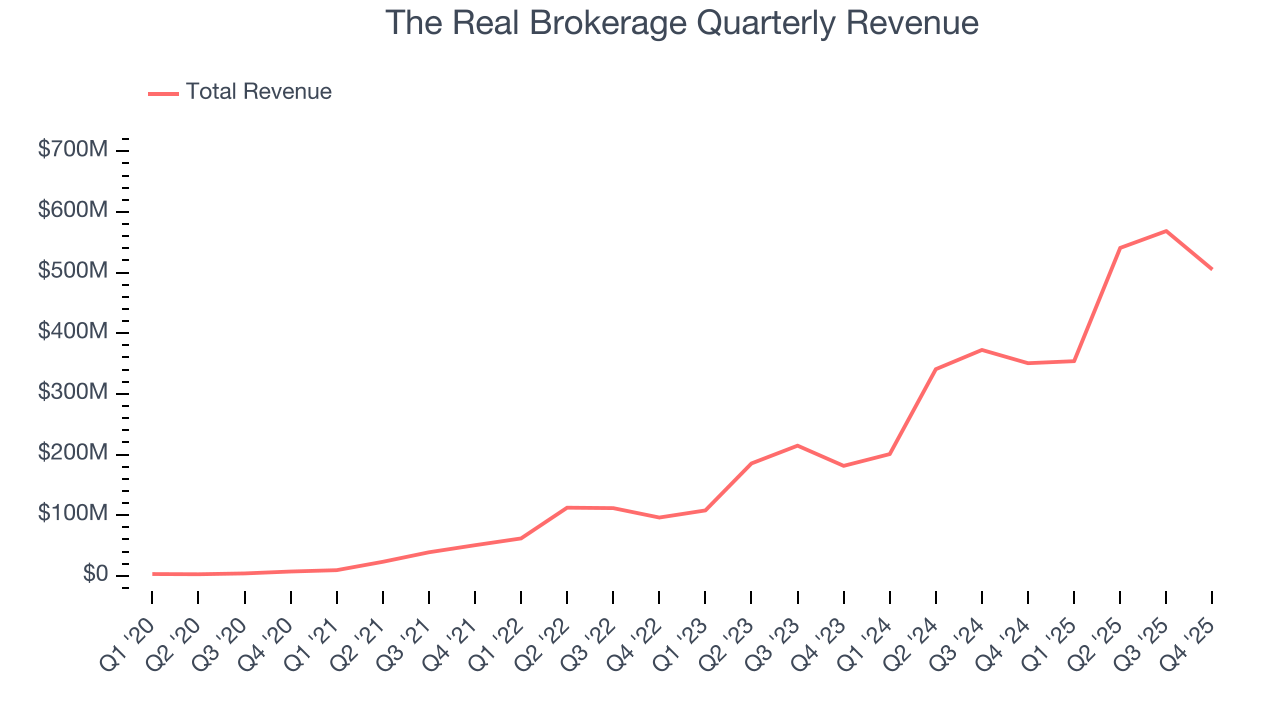

5. Revenue Growth

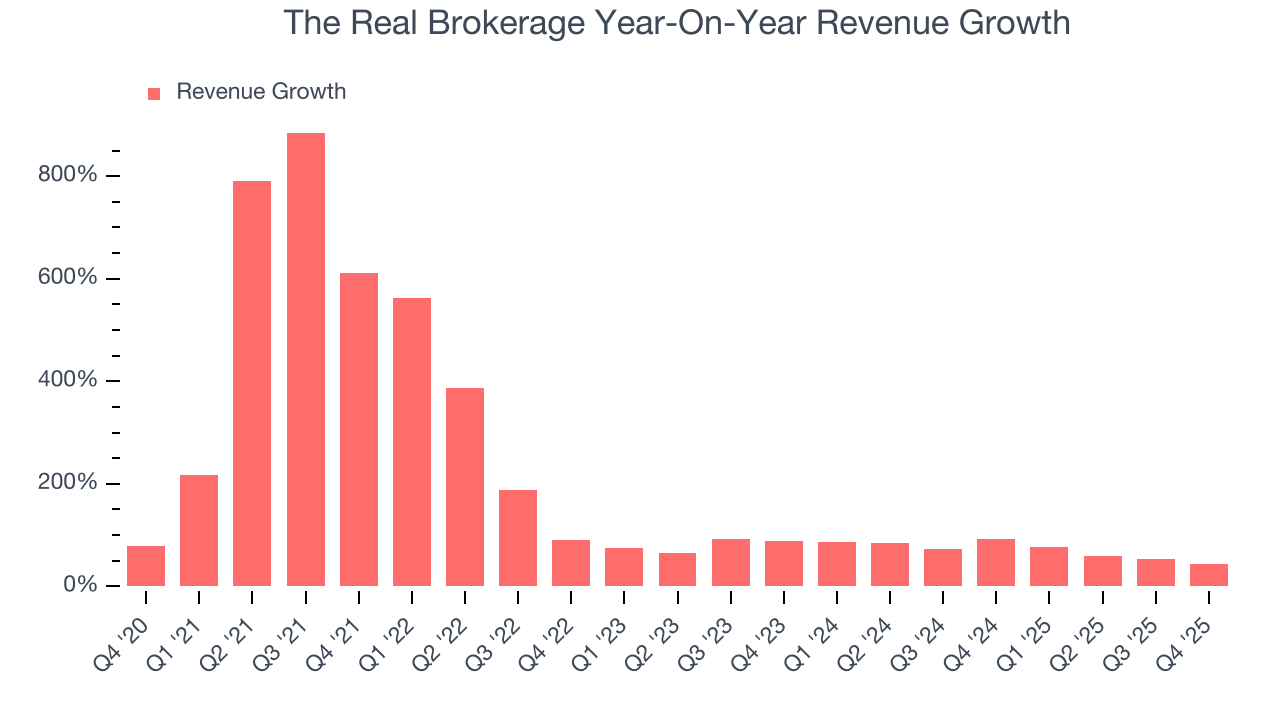

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, The Real Brokerage grew its sales at an incredible 160% compounded annual growth rate. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. The Real Brokerage’s annualized revenue growth of 69% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, The Real Brokerage reported magnificent year-on-year revenue growth of 44.1%, and its $505.1 million of revenue beat Wall Street’s estimates by 7.6%.

Looking ahead, sell-side analysts expect revenue to grow 19.9% over the next 12 months, a deceleration versus the last two years. Still, this projection is commendable and indicates the market is baking in success for its products and services.

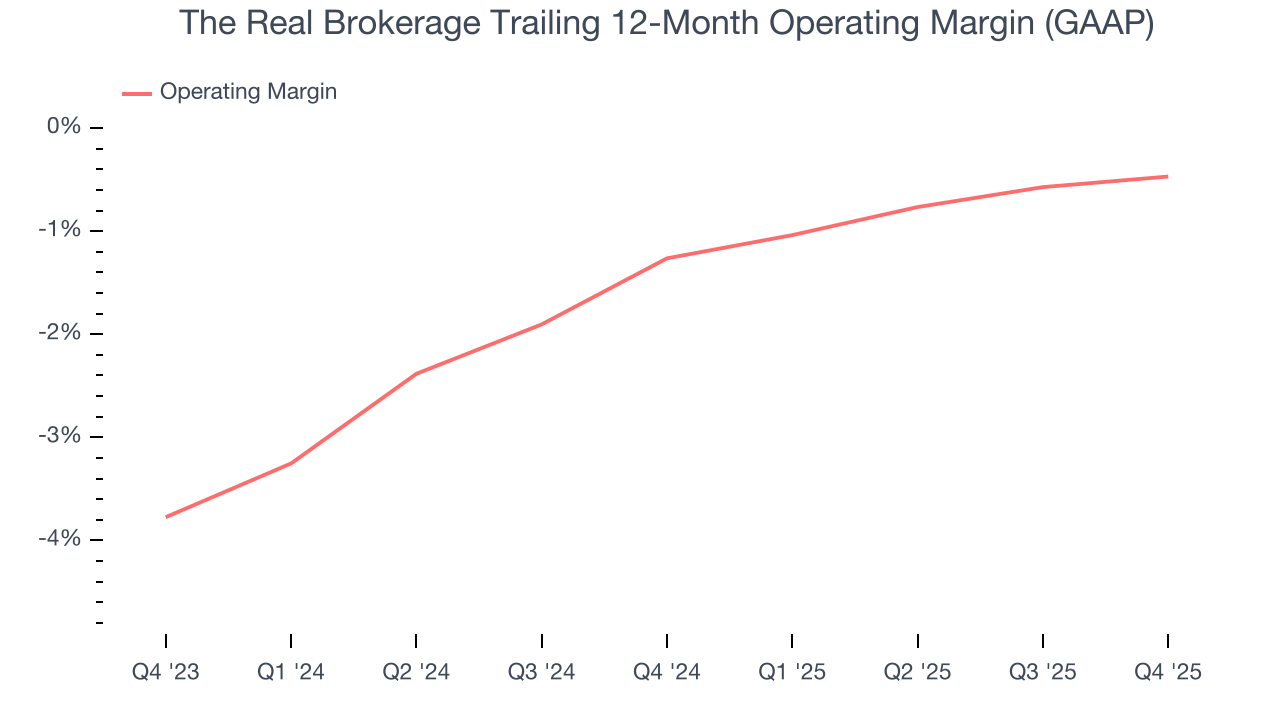

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

The Real Brokerage’s operating margin has generally stayed the same over the last 12 months. The company broke even over the last two years, inadequate for a consumer discretionary business. Its large expense base and inefficient cost structure were the main culprits behind this performance.

This quarter, The Real Brokerage generated a negative 1% operating margin.

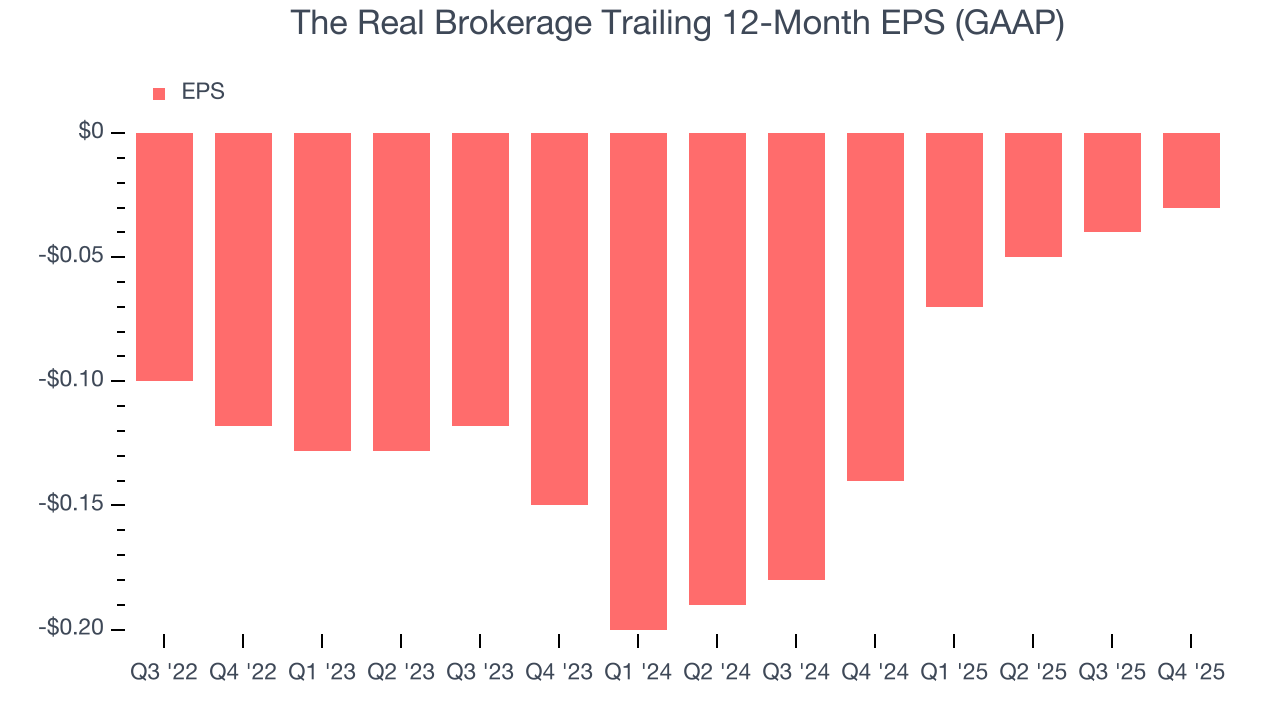

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although The Real Brokerage’s full-year earnings are still negative, it reduced its losses and improved its EPS by 8.9% annually over the last four years. The next few quarters will be critical for assessing its long-term profitability.

In Q4, The Real Brokerage reported EPS of negative $0.02, in line with the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects The Real Brokerage to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.03 will advance to negative $0.03.

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

The Real Brokerage has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 3.5%, below what we’d expect for a consumer discretionary business.

The Real Brokerage broke even from a free cash flow perspective in Q4. The company’s cash profitability regressed as it was 1.1 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts’ consensus estimates show they’re expecting The Real Brokerage’s free cash flow margin of 3.3% for the last 12 months to remain the same.

9. Balance Sheet Assessment

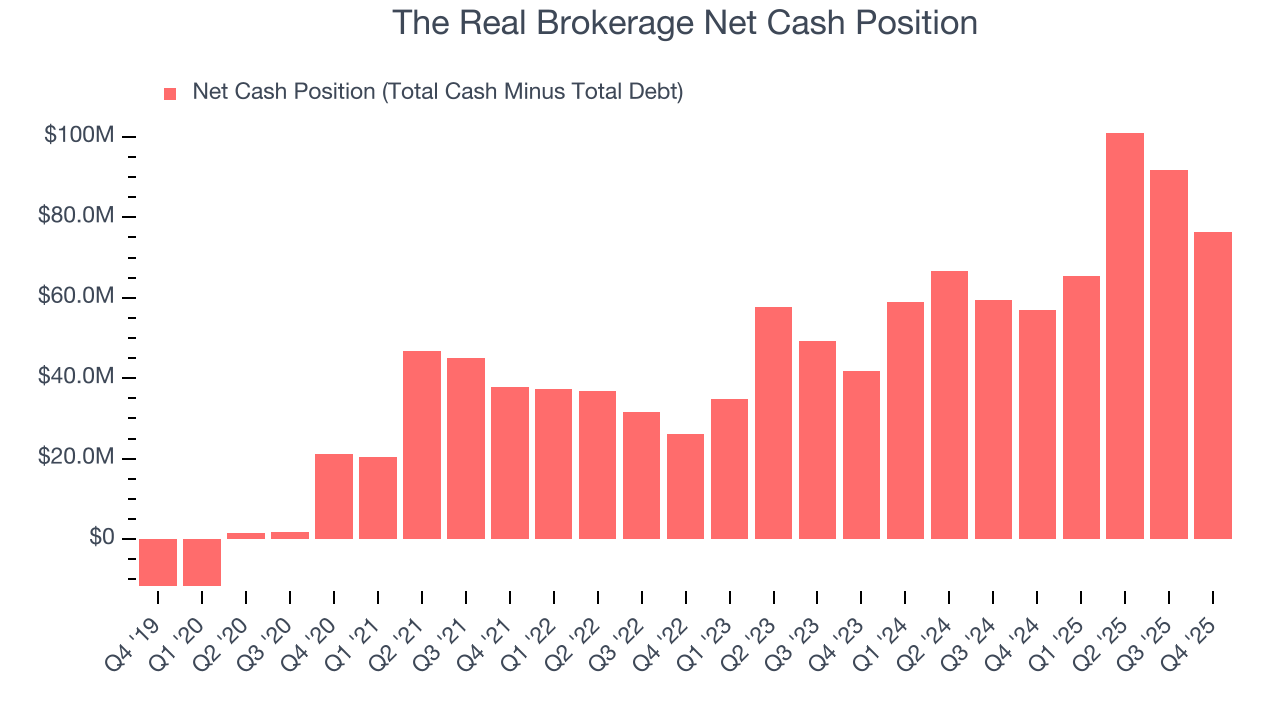

Companies with more cash than debt have lower bankruptcy risk.

The Real Brokerage is a well-capitalized company with $76.28 million of cash and no debt. This position is 13.2% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

10. Key Takeaways from The Real Brokerage’s Q4 Results

It was good to see The Real Brokerage beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 1.5% to $2.78 immediately following the results.

11. Is Now The Time To Buy The Real Brokerage?

Updated: March 15, 2026 at 11:13 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own The Real Brokerage, you should also grasp the company’s longer-term business quality and valuation.

We cheer for all companies serving everyday consumers, but in the case of The Real Brokerage, we’ll be cheering from the sidelines. Although its revenue growth was exceptional over the last five years, it’s expected to deteriorate over the next 12 months and its Forecasted free cash flow margin for next year suggests the company will fail to improve its cash conversion. And while the company’s projected EPS for the next year implies the company’s fundamentals will improve, the downside is its weak EPS growth over the last four years shows it’s failed to produce meaningful profits for shareholders.

The Real Brokerage’s EV-to-EBITDA ratio based on the next 12 months is 6.2x. While this valuation is reasonable, we don’t see a big opportunity at the moment. There are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $5.55 on the company (compared to the current share price of $2.37).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.