Simply Good Foods (SMPL)

We’re skeptical of Simply Good Foods. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Simply Good Foods Will Underperform

Best known for its Atkins brand that was inspired by the popular diet of the same name, Simply Good Foods (NASDAQ:SMPL) is a packaged food company whose offerings help customers achieve their healthy eating or weight loss goals.

- Demand is forecasted to shrink as its estimated sales for the next 12 months are flat

- Revenue base of $1.45 billion puts it at a disadvantage compared to larger competitors exhibiting economies of scale

- A positive is that its strong free cash flow margin of 13.1% gives it the option to reinvest, repurchase shares, or pay dividends

Simply Good Foods lacks the business quality we seek. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than Simply Good Foods

Simply Good Foods is trading at $14.65 per share, or 7.1x forward P/E. Simply Good Foods’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Simply Good Foods (SMPL) Research Report: Q4 CY2025 Update

Packaged food company Simply Good Foods (NASDAQ:SMPL) announced better-than-expected revenue in Q4 CY2025, but sales were flat year on year at $340.2 million. Its non-GAAP profit of $0.39 per share was 8.2% above analysts’ consensus estimates.

Simply Good Foods (SMPL) Q4 CY2025 Highlights:

- Revenue: $340.2 million vs analyst estimates of $336.1 million (flat year on year, 1.2% beat)

- Adjusted EPS: $0.39 vs analyst estimates of $0.36 (8.2% beat)

- Adjusted EBITDA: $55.62 million vs analyst estimates of $55.72 million (16.4% margin, in line)

- Operating Margin: 11%, down from 16% in the same quarter last year

- Free Cash Flow Margin: 14.1%, up from 9.3% in the same quarter last year

- Market Capitalization: $1.84 billion

Company Overview

Best known for its Atkins brand that was inspired by the popular diet of the same name, Simply Good Foods (NASDAQ:SMPL) is a packaged food company whose offerings help customers achieve their healthy eating or weight loss goals.

The Atkins brand, which spans bars, shakes, and frozen meals, emphasizes low-carb and low-sugar foods for weight loss and weight management. The company’s other major brand is Quest, which it acquired for roughly $1 billion in 2019 to broaden its addressable market. Quest offers high-protein cookies, chips, and bars to help consumers maintain a healthy diet or build muscle.

The Simply Good Foods core customer is a health-conscious individual who prioritizes nutritious eating or someone who wants to become that health-conscious person. This individual, however, doesn’t want to completely sacrifice good-tasting foods and treats.

Simply Good Foods' products are available in general retailers such as grocery stores and club warehouse stores as well as in specialty retailers. Consumers have the option to buy single bars or cookies or boxes of them for more regular consumption. The company also has a direct-to-consumer e-commerce site where consumers can buy any Atkins or Quest product.

4. Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Competitors include established consumer staples companies that are increasing their healthy food and snack offerings such as Kellogg (NYSE:K) and General Mills (NYSE:GIS) as well as companies solely focused on wellness and nutrition such as Bellring Brands (NYSE:BRBR) and Herbalife (NYSE:HLF).

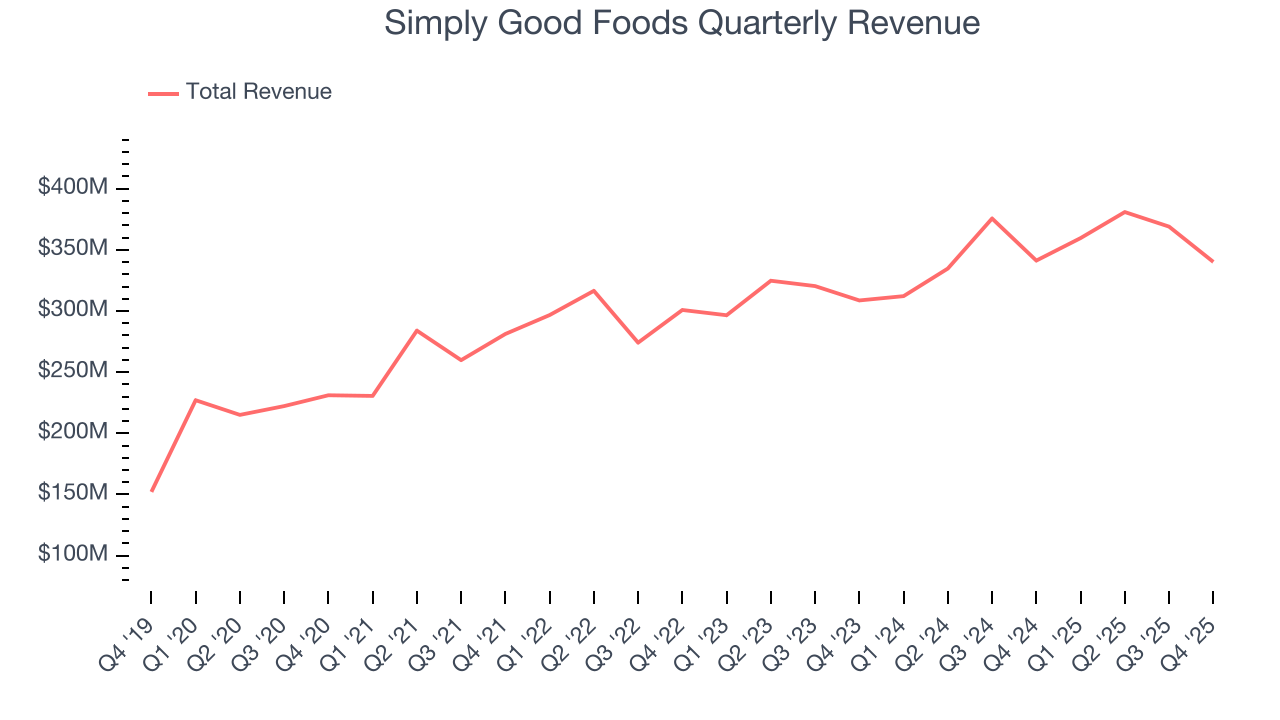

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $1.45 billion in revenue over the past 12 months, Simply Good Foods is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Simply Good Foods grew its sales at a mediocre 6.9% compounded annual growth rate over the last three years. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

This quarter, Simply Good Foods’s $340.2 million of revenue was flat year on year but beat Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and implies its products will see some demand headwinds.

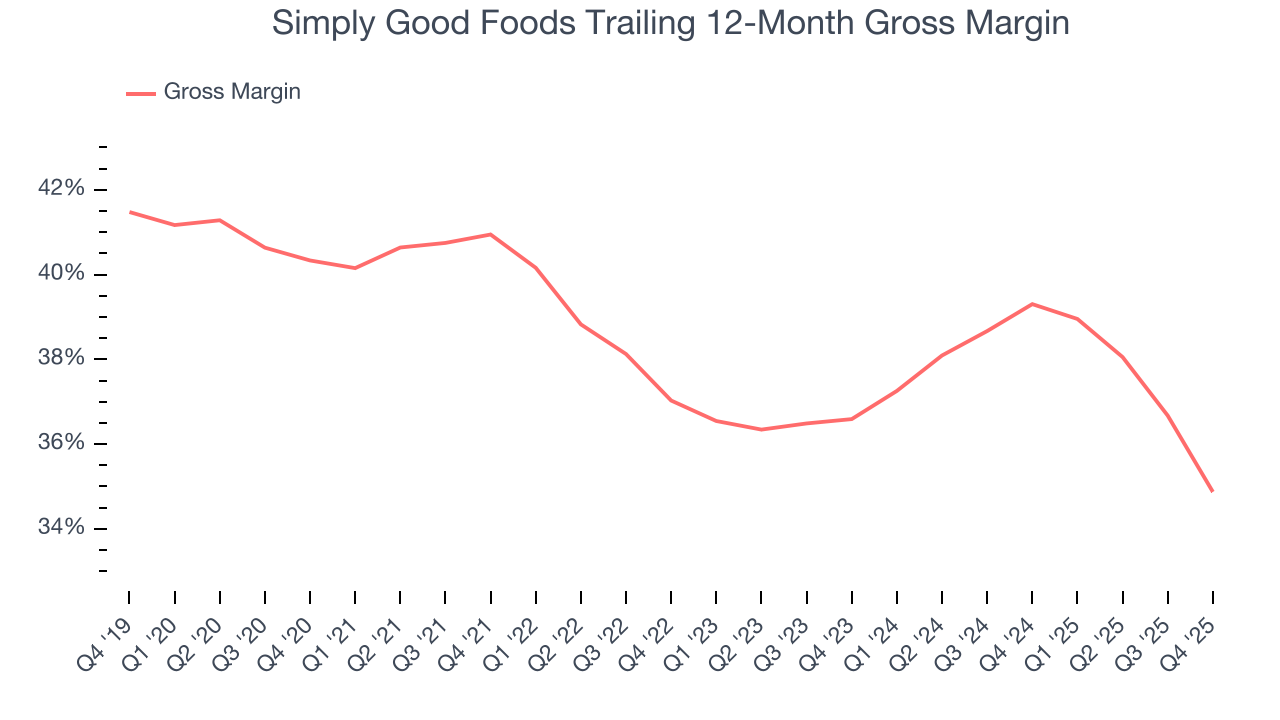

6. Gross Margin & Pricing Power

Simply Good Foods has good unit economics for a consumer staples company, giving it the opportunity to invest in areas such as marketing and talent to stay competitive. As you can see below, it averaged an impressive 37% gross margin over the last two years. Said differently, Simply Good Foods paid its suppliers $62.98 for every $100 in revenue.

This quarter, Simply Good Foods’s gross profit margin was 32.3%, down 7.7 percentage points year on year. Simply Good Foods’s full-year margin has also been trending down over the past 12 months, decreasing by 4.4 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

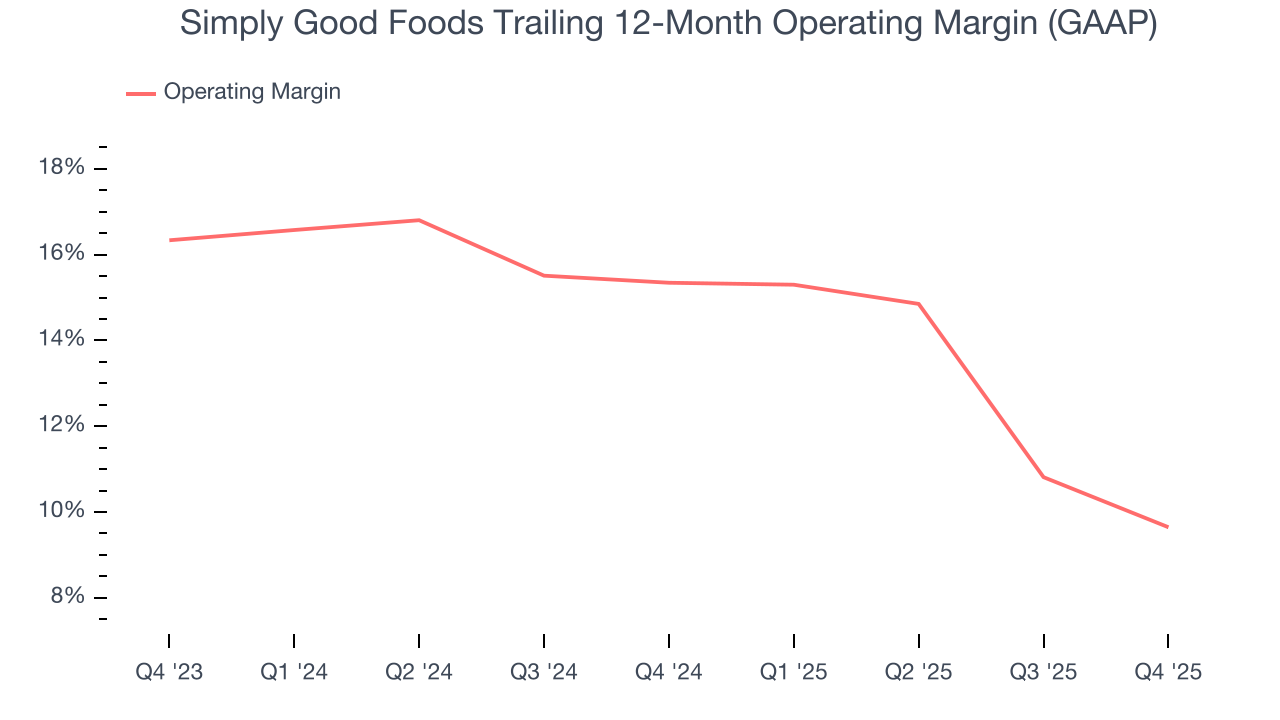

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Simply Good Foods has managed its cost base well over the last two years. It demonstrated solid profitability for a consumer staples business, producing an average operating margin of 12.4%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Simply Good Foods’s operating margin decreased by 5.7 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Simply Good Foods generated an operating margin profit margin of 11%, down 5 percentage points year on year. Since Simply Good Foods’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, and administrative overhead expenses.

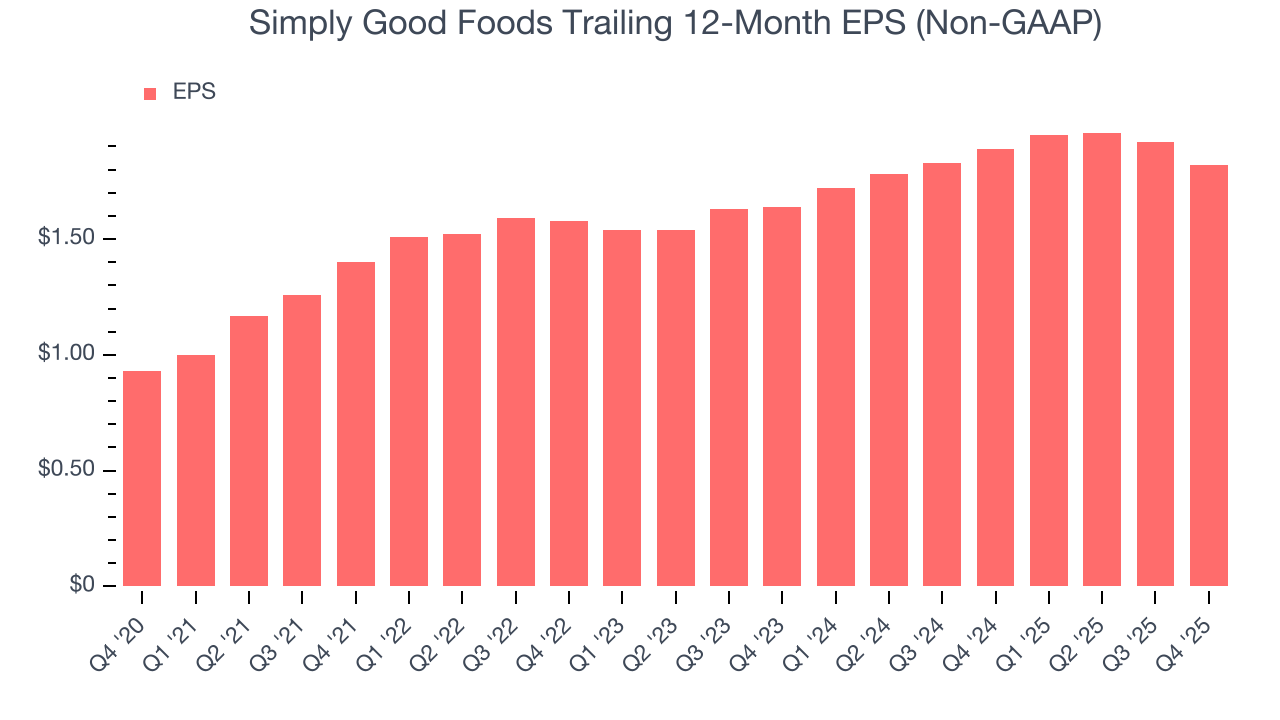

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Simply Good Foods’s EPS grew at an unimpressive 4.8% compounded annual growth rate over the last three years, lower than its 6.9% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

In Q4, Simply Good Foods reported adjusted EPS of $0.39, down from $0.49 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 8.2%. Over the next 12 months, Wall Street expects Simply Good Foods’s full-year EPS of $1.82 to grow 9.1%.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

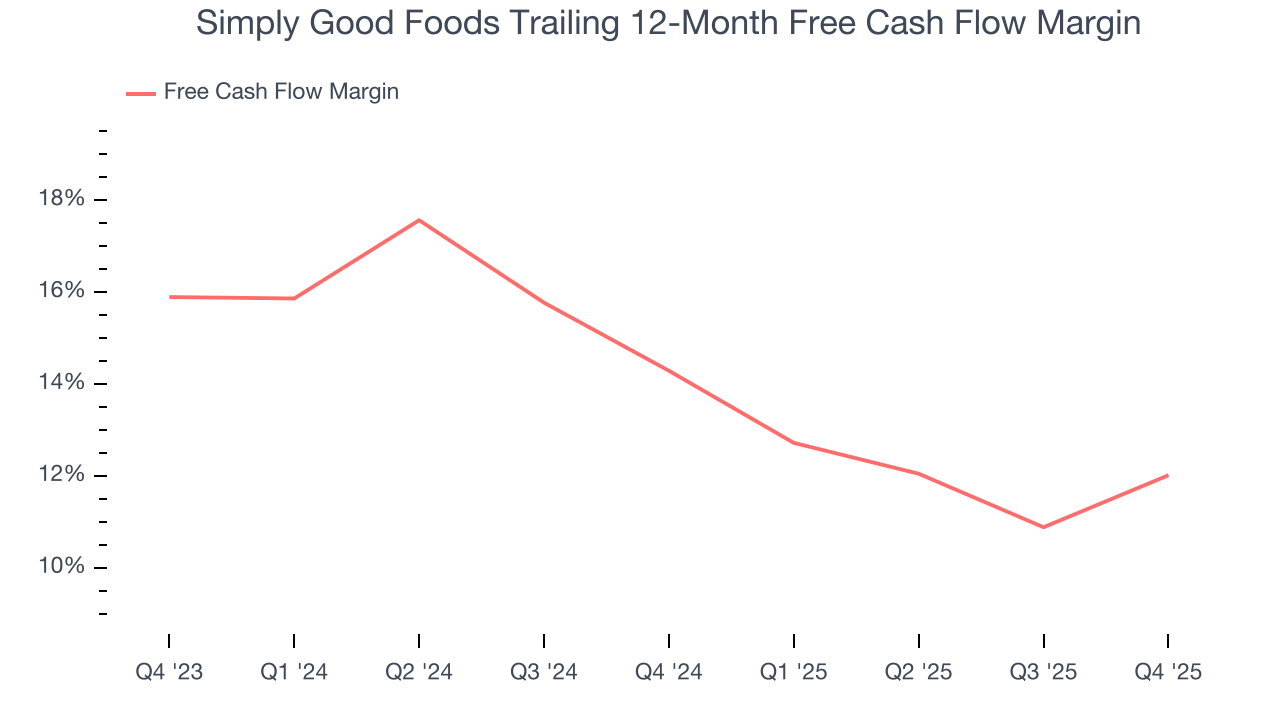

Simply Good Foods has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging 13.1% over the last two years.

Taking a step back, we can see that Simply Good Foods’s margin dropped by 2.3 percentage points over the last year. Continued declines could signal it is in the middle of an investment cycle.

Simply Good Foods’s free cash flow clocked in at $48 million in Q4, equivalent to a 14.1% margin. This result was good as its margin was 4.8 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

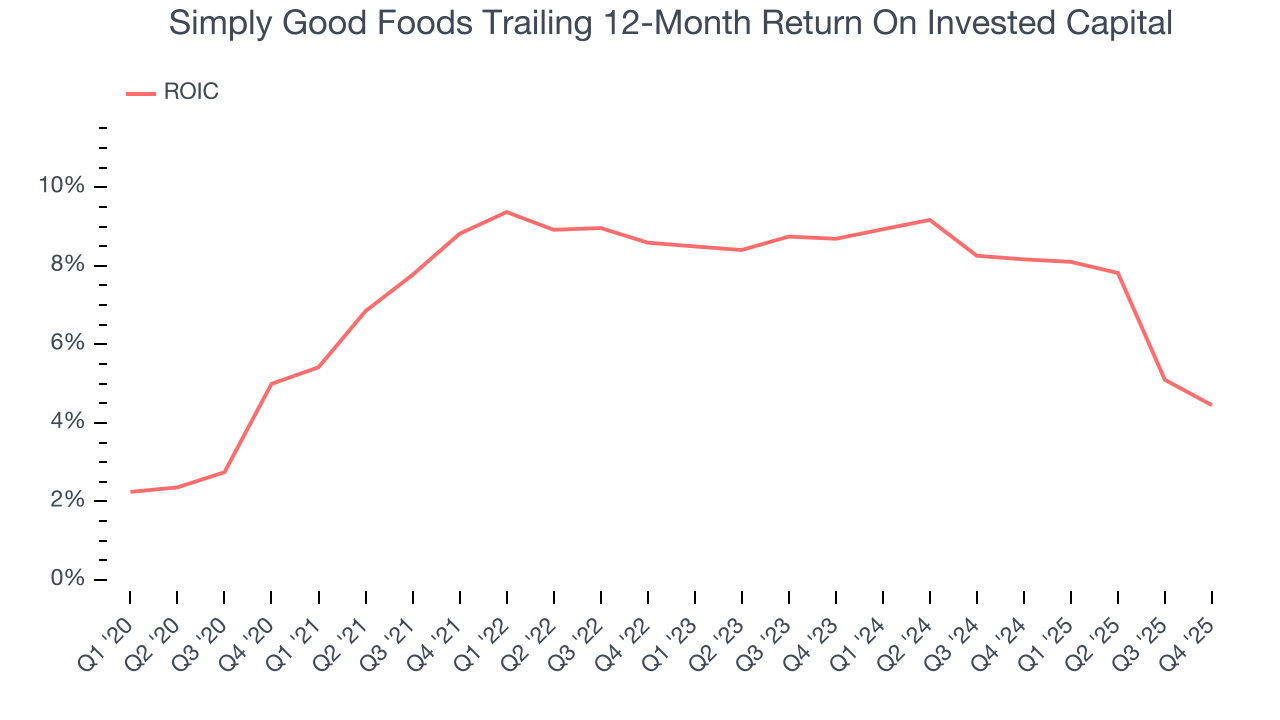

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Simply Good Foods historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 7.7%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+.

11. Balance Sheet Assessment

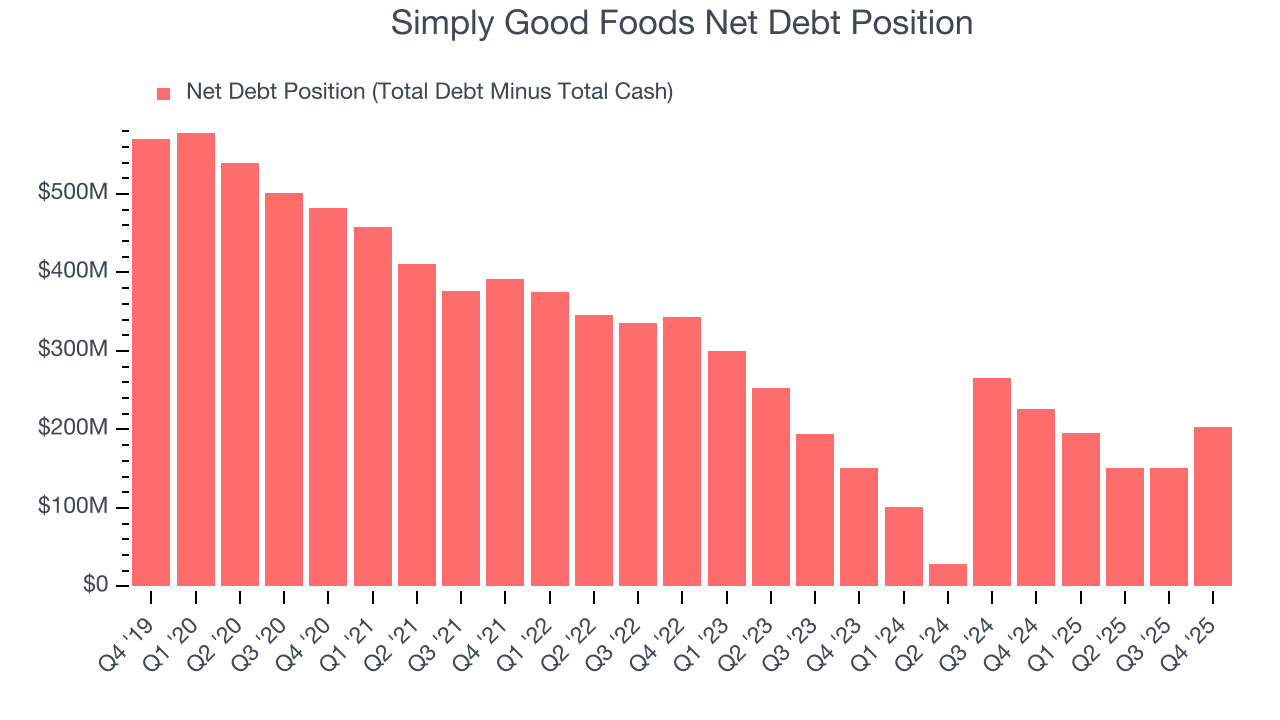

Simply Good Foods reported $194.1 million of cash and $396.7 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $263.7 million of EBITDA over the last 12 months, we view Simply Good Foods’s 0.8× net-debt-to-EBITDA ratio as safe. We also see its $9.71 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Simply Good Foods’s Q4 Results

It was good to see Simply Good Foods beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its gross margin missed. Zooming out, we think this was a mixed quarter. The stock remained flat at $19.56 immediately following the results.

13. Is Now The Time To Buy Simply Good Foods?

Updated: March 30, 2026 at 10:51 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Simply Good Foods isn’t a terrible business, but it isn’t one of our picks. To kick things off, its revenue growth was mediocre over the last three years, and analysts expect its demand to deteriorate over the next 12 months. While its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits, the downside is its declining operating margin shows the business has become less efficient. On top of that, its brand caters to a niche market.

Simply Good Foods’s P/E ratio based on the next 12 months is 7.1x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $27.20 on the company (compared to the current share price of $14.65).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.