Target Hospitality (TH)

We wouldn’t recommend Target Hospitality. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Target Hospitality Will Underperform

Building mini-communities at places such as oil drilling sites, Target Hospitality (NASDAQ:TH) is a provider of specialty workforce lodging accommodations and services.

- Muted 7.3% annual revenue growth over the last five years shows its demand lagged behind its consumer discretionary peers

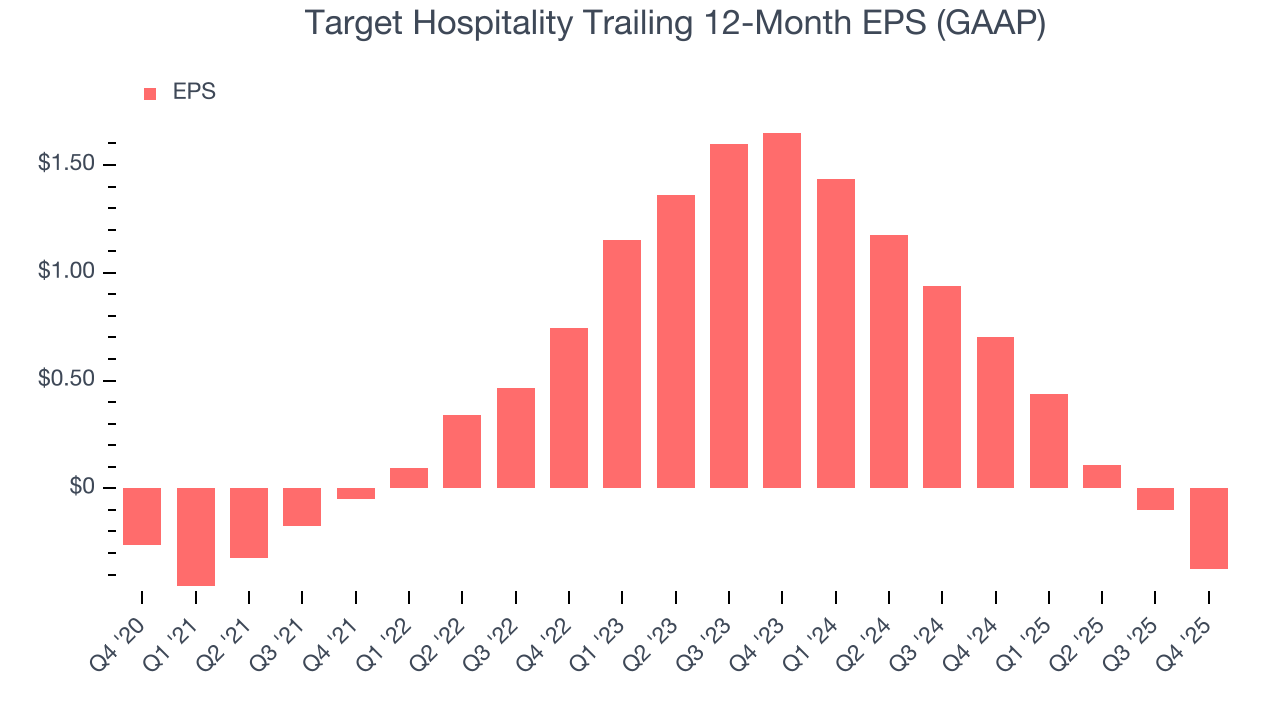

- Performance over the past five years shows its incremental sales were much less profitable, as its earnings per share fell by 3.7% annually

- Operating margin falls short of the industry average, and the smaller profit dollars make it harder to react to unexpected market developments

Target Hospitality doesn’t fulfill our quality requirements. We’re looking for better stocks elsewhere.

Why There Are Better Opportunities Than Target Hospitality

Target Hospitality’s stock price of $9.32 implies a valuation ratio of 15.4x forward EV-to-EBITDA. This multiple is higher than that of consumer discretionary peers; it’s also rich for the top-line growth of the company. Not a great combination.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Target Hospitality (TH) Research Report: Q4 CY2025 Update

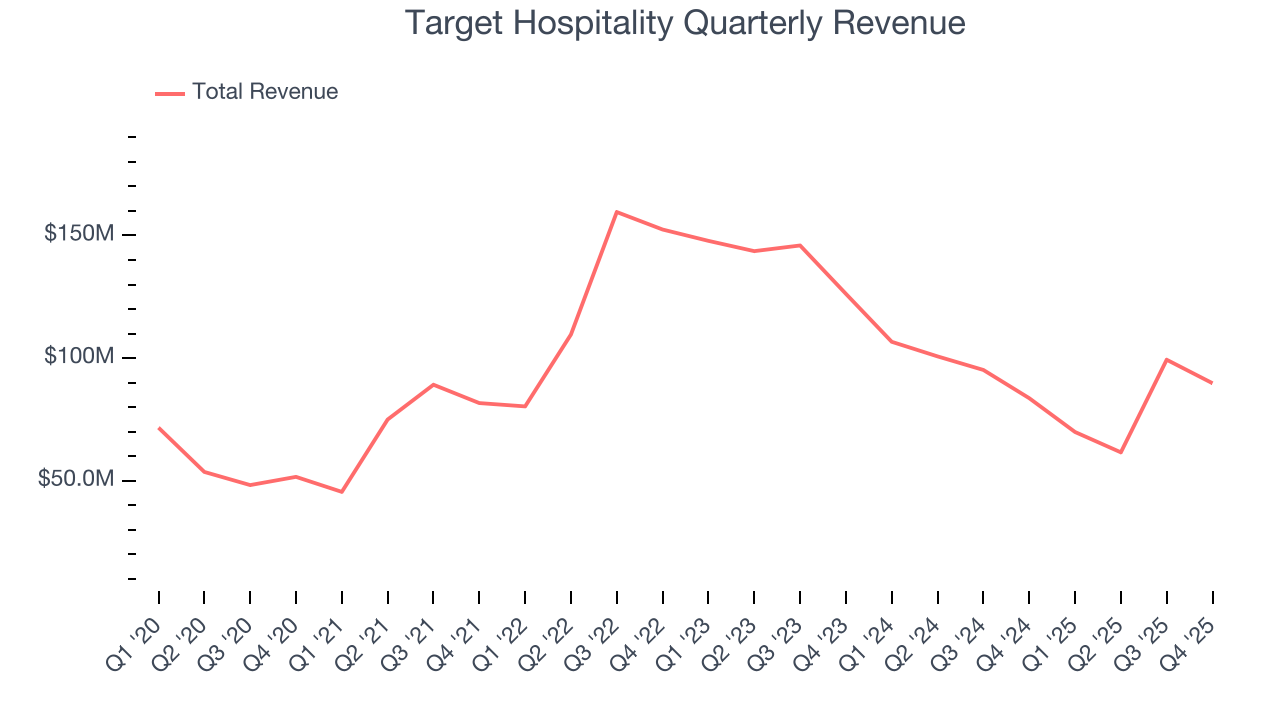

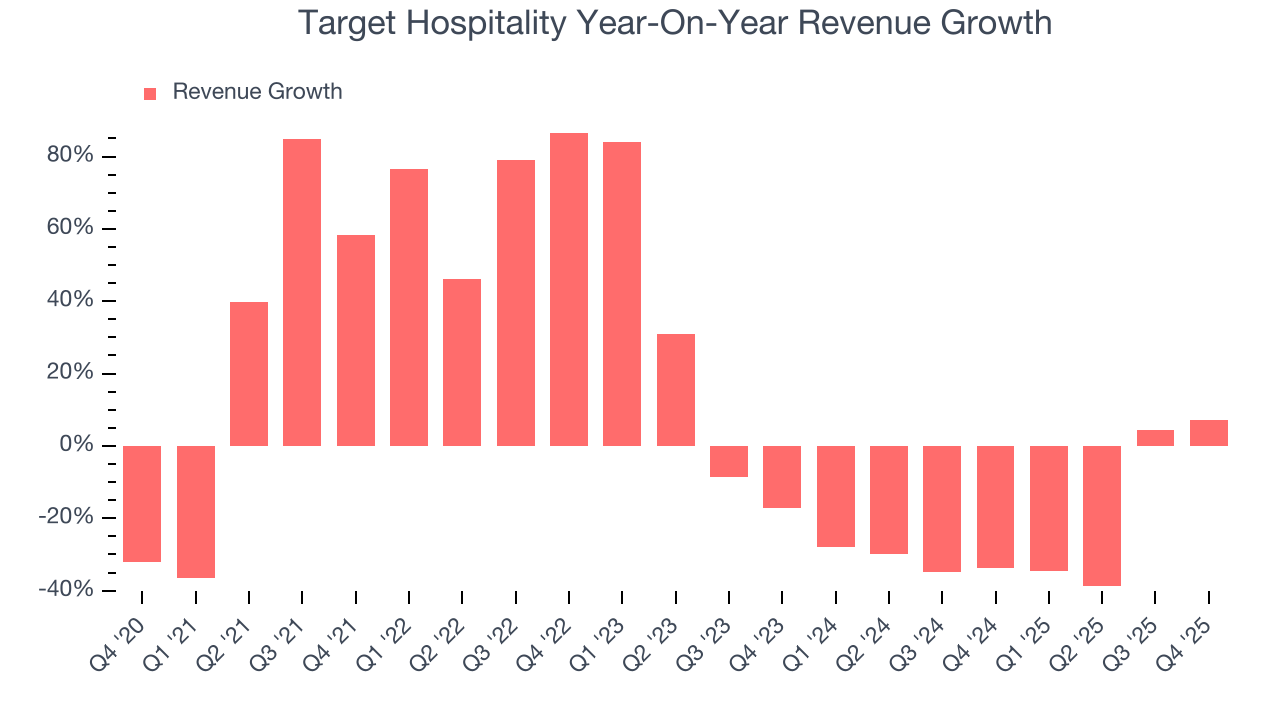

Workforce housing company Target Hospitality (NASDAQ:TH) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 7.3% year on year to $89.78 million. The company’s full-year revenue guidance of $325 million at the midpoint came in 17.7% above analysts’ estimates. Its GAAP loss of $0.15 per share was 45.2% below analysts’ consensus estimates.

Target Hospitality (TH) Q4 CY2025 Highlights:

- Announced multiple new multi-year committed revenue contracts

- Revenue: $89.78 million vs analyst estimates of $85.84 million (7.3% year-on-year growth, 4.6% beat)

- EPS (GAAP): -$0.15 vs analyst expectations of -$0.10 (45.2% miss)

- Adjusted EBITDA: $6.54 million vs analyst estimates of $7.43 million (7.3% margin, 12% miss)

- EBITDA guidance for the upcoming financial year 2026 is $65 million at the midpoint, above analyst estimates of $58 million

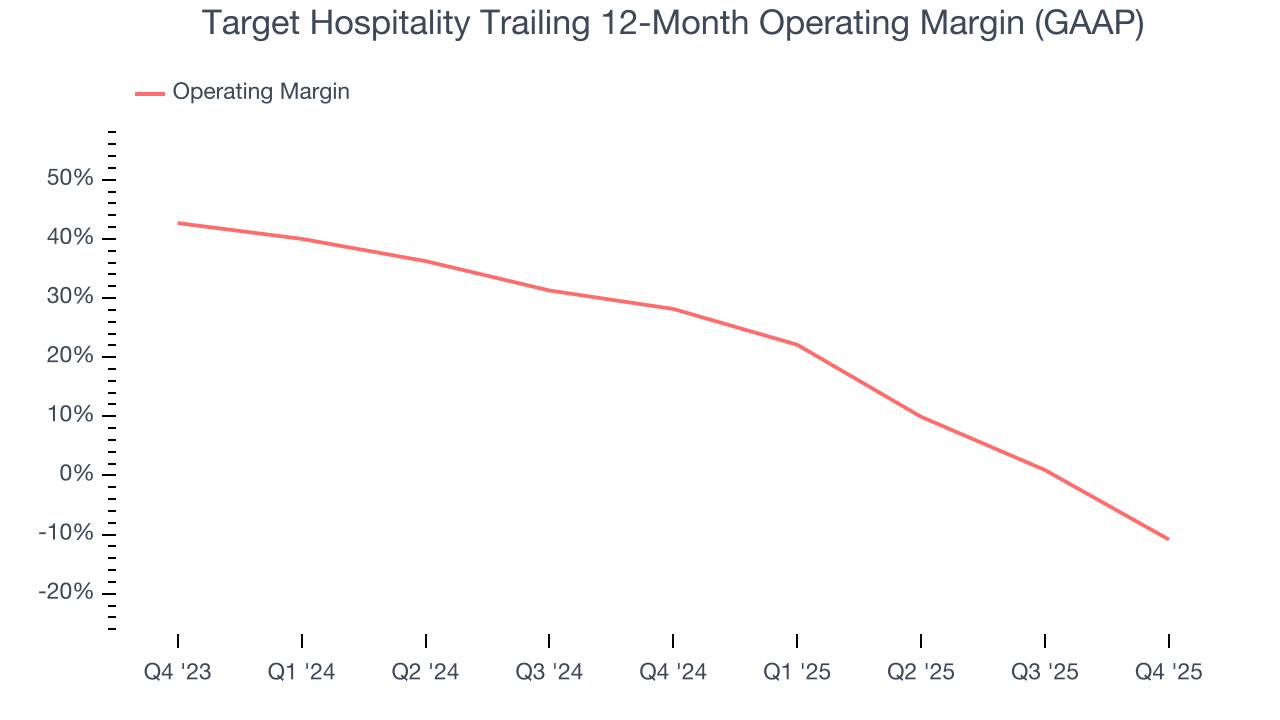

- Operating Margin: -18.7%, down from 24.9% in the same quarter last year

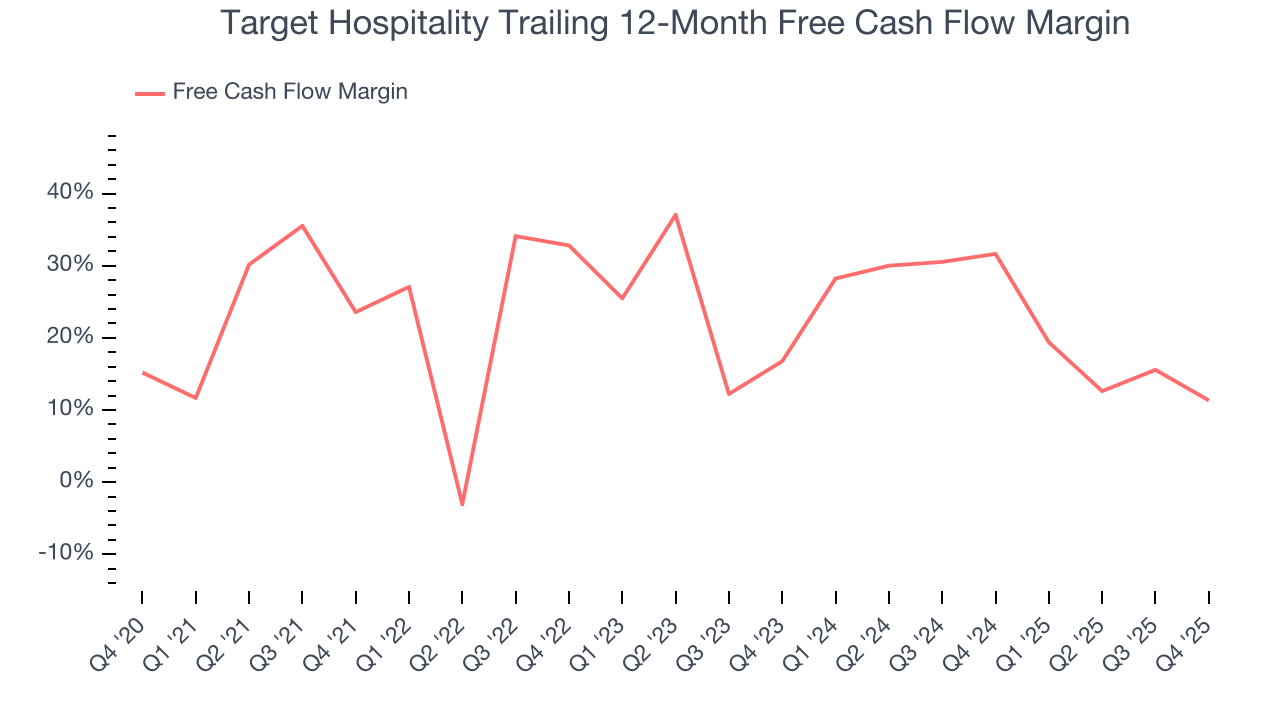

- Free Cash Flow Margin: 13.4%, down from 29.4% in the same quarter last year

- Utilized Beds: 8,466, down 3,445 year on year

- Market Capitalization: $796.2 million

Company Overview

Building mini-communities at places such as oil drilling sites, Target Hospitality (NASDAQ:TH) is a provider of specialty workforce lodging accommodations and services.

The company creates and manages "man camps" or workforce housing communities, which provide temporary accommodations for workers in remote or underserved areas. Its main customers are energy companies, and its facilities are typically located in or near shale plays (areas with petroleum and natural gas components) and other industrial projects across North America, particularly in the Permian Basin, the most prolific oil-producing area in the United States.

Target Hospitality also offers a comprehensive suite of hospitality services, including catering, housekeeping, laundry, security, and recreational facilities, ensuring a comfortable and productive living environment. This holistic approach to workforce housing solutions is a key differentiator for Target Hospitality, allowing it to meet its clients' complex needs.

The company mostly develops and operates its own properties, occasionally enlisting third parties to help run its locations. This hybrid approach allows Target Hospitality to scale rapidly and provide flexible solutions. Its accommodation solutions range from single-occupancy rooms to larger communal living facilities, all designed with a focus on safety, comfort, and efficiency.

4. Consumer Discretionary - Travel and Vacation Providers

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Travel and vacation providers operate tour packages, cruise lines, online travel agencies, and vacation rental platforms, connecting consumers with leisure and business travel experiences. Tailwinds include robust post-pandemic travel demand, a consumer preference shift toward experiences over goods, and technology-enabled personalization improving conversion and loyalty. However, headwinds are significant: the industry is acutely sensitive to macroeconomic cycles, geopolitical instability, and fuel price volatility. Low switching costs mean fierce price competition, while capacity additions in segments like cruises can lead to oversupply. Regulatory burdens, weather disruptions, and public health risks further create episodic but potentially severe demand shocks.

Target Hospitality's primary competitors include Civeo (NYSE:CVEO), Black Diamond Group (TSX:BDI), ATCO (TSX:ACO.X), ProPetro Holding (NYSE:PUMP), and Halliburton (NYSE:HAL).

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Target Hospitality’s 7.3% annualized revenue growth over the last five years was weak. This was below our standard for the consumer discretionary sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Target Hospitality’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 24.6% annually.

We can dig further into the company’s revenue dynamics by analyzing its number of utilized beds, which reached 8,466 in the latest quarter. Over the last two years, Target Hospitality’s utilized beds averaged 36.2% year-on-year declines. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Target Hospitality reported year-on-year revenue growth of 7.3%, and its $89.78 million of revenue exceeded Wall Street’s estimates by 4.6%.

Looking ahead, sell-side analysts expect revenue to decline by 11.2% over the next 12 months. While this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Target Hospitality’s operating margin has been trending down over the last 12 months and averaged 10.5% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Target Hospitality generated an operating margin profit margin of negative 18.7%, down 43.6 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Target Hospitality’s earnings losses deepened over the last five years as its EPS dropped 7.4% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. Consumer Discretionary companies are particularly exposed to this, and if the tide turns unexpectedly, Target Hospitality’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Target Hospitality reported EPS of negative $0.15, down from $0.12 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Target Hospitality to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.37 will advance to negative $0.21.

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Target Hospitality has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 22.4%, below what we’d expect for a consumer discretionary business.

Target Hospitality’s free cash flow clocked in at $12 million in Q4, equivalent to a 13.4% margin. The company’s cash profitability regressed as it was 16.1 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Target Hospitality historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 20.1%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Target Hospitality’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

10. Balance Sheet Assessment

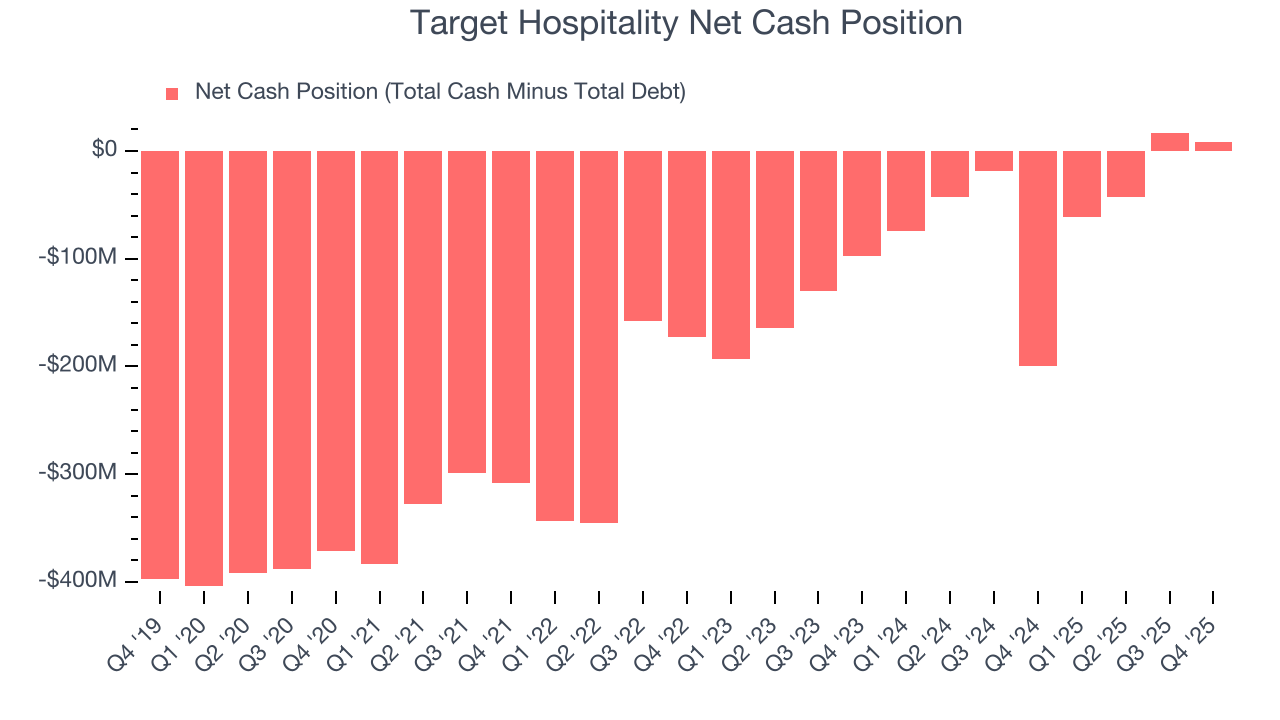

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Target Hospitality is a well-capitalized company with $8.35 million of cash and no debt. This position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Target Hospitality’s Q4 Results

Revenue beat convincingly, which is a good start. We were also impressed by Target Hospitality’s optimistic full-year revenue and EBITDA guidance, both of which exceeded analysts’ expectations. On the other hand, its EPS missed and its EBITDA fell short of Wall Street’s estimates. Still, we think this was still a decent quarter with some key metrics above expectations. The stock traded up 4.7% to $8.35 immediately after reporting.

12. Is Now The Time To Buy Target Hospitality?

Updated: March 15, 2026 at 10:54 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Target Hospitality, you should also grasp the company’s longer-term business quality and valuation.

Target Hospitality falls short of our quality standards. On top of that, Target Hospitality’s number of utilized beds has disappointed, and its declining EPS over the last five years makes it a less attractive asset to the public markets.

Target Hospitality’s EV-to-EBITDA ratio based on the next 12 months is 15.4x. This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $11 on the company (compared to the current share price of $9.32).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.