Udemy (UDMY)

We’re wary of Udemy. Its sluggish sales growth shows demand is soft, a worrisome sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why We Think Udemy Will Underperform

With courses ranging from investing to cooking to computer programming, Udemy (NASDAQ:UDMY) is an online learning platform that connects learners with expert instructors who specialize in a wide range of topics.

- Demand has fallen off a cliff over the last two years as its average revenue per buyer fell by 2.2% annually while it struggled to expand its customer base

- Expensive marketing campaigns hurt its profitability and make us wonder what would happen if it let up on the gas

- A silver lining is that its incremental sales significantly boosted profitability as its annual earnings per share growth of 45.5% over the last three years outstripped its revenue performance

Udemy doesn’t satisfy our quality benchmarks. We see more favorable opportunities in the market.

Why There Are Better Opportunities Than Udemy

Udemy’s stock price of $4.80 implies a valuation ratio of 3.6x forward EV/EBITDA. Udemy’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Udemy (UDMY) Research Report: Q4 CY2025 Update

Online learning platform Udemy (NASDAQ:UDMY) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 3% year on year to $194 million. Its non-GAAP profit of $0.12 per share was 19% above analysts’ consensus estimates.

Udemy (UDMY) Q4 CY2025 Highlights:

- On December 17, 2025, Udemy and Coursera entered into a definitive merger agreement under which Coursera will combine with Udemy in an all-stock transaction. Under the terms of the definitive agreement, Udemy stockholders will receive 0.800 shares of Coursera common stock for each share of Udemy common stock. Upon the closing of the transaction, existing Coursera stockholders are expected to own approximately 59% and existing Udemy stockholders are expected to own approximately 41% of the combined company, on a fully diluted basis.

- Revenue: $194 million vs analyst estimates of $193.2 million (3% year-on-year decline, in line)

- Adjusted EPS: $0.12 vs analyst estimates of $0.10 (19% beat)

- Adjusted EBITDA: $21.45 million vs analyst estimates of $19.67 million (11.1% margin, 9% beat)

- Free Cash Flow Margin: 6.1%, similar to the previous quarter

- Market Capitalization: $696.2 million

Company Overview

With courses ranging from investing to cooking to computer programming, Udemy (NASDAQ:UDMY) is an online learning platform that connects learners with expert instructors who specialize in a wide range of topics.

The company’s key offering is its marketplace of diverse courses. Consumers turn to the platform to learn new skills or brush up on existing ones for professional or leisure purposes. You can take a data analysis course in the morning to improve your performance at work and a photography class at night because it’s a hobby!

Udemy addresses two customer pain points of learning: convenience and selection. First, learning traditionally involved a physical presence. Some people don’t have the time or resources to go to the local community college three times a week in the afternoon to learn music production, for example. Secondly, it is sometimes hard to find a high-quality instructor in a local area. Udemy digitizes learning and acts as a marketplace, allowing consumers to learn from anywhere they have an internet connection and to choose from a vast selection of instructors all over the world.

Udemy generates revenue through a revenue-sharing model with instructors. Instructors create courses and upload them to the platform, and Udemy takes a percentage of the revenue generated from the course sales. In addition, Udemy also offers a subscription service called Udemy Pro, which provides access to a curated selection of courses along with exclusive features and benefits.

4. Consumer Subscription

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

Competitors offering online educational services include Coursera (NYSE:COUR), Microsoft’s LinkedIn Learning (NYSE:MSFT), and Skillsoft (NYSE:SKIL).

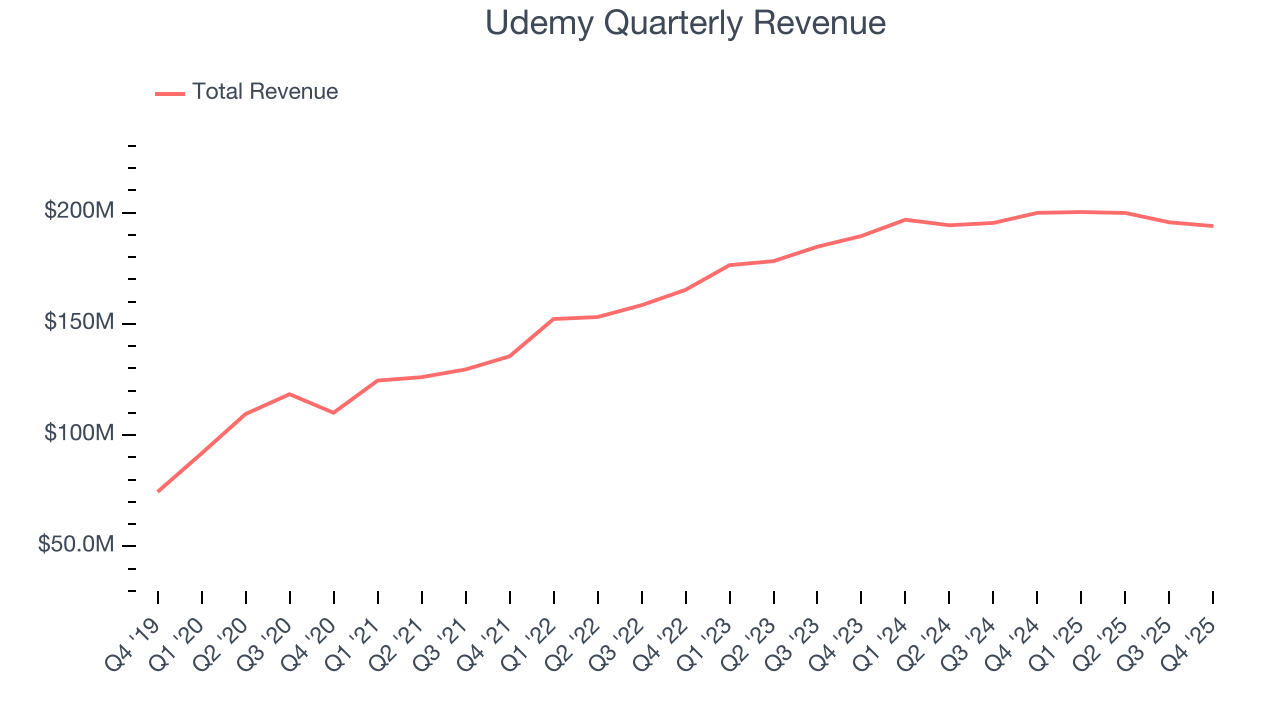

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Udemy’s 7.9% annualized revenue growth over the last three years was tepid. This was below our standard for the consumer internet sector and is a tough starting point for our analysis.

This quarter, Udemy reported a rather uninspiring 3% year-on-year revenue decline to $194 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 1.9% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and indicates its products and services will face some demand challenges.

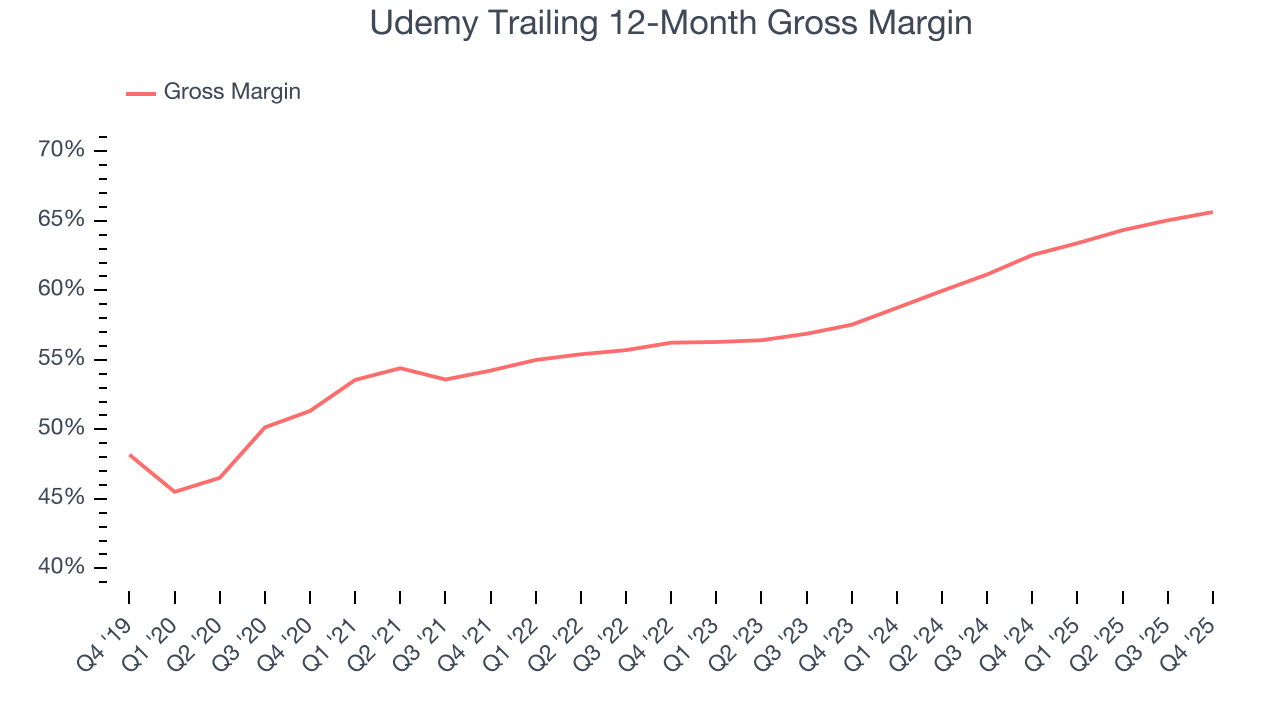

6. Gross Margin & Pricing Power

For internet subscription businesses like Udemy, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include customer service, data center and infrastructure expenses, royalties, and other content-related costs if the company’s offerings include features such as video or music.

Udemy’s gross margin is ahead of the broader industry and points to its solid unit economics, competitive products and services, and lack of meaningful pricing pressure. As you can see below, it averaged an impressive 64.1% gross margin over the last two years. That means for every $100 in revenue, roughly $64.09 was left to spend on selling, marketing, and R&D.

This quarter, Udemy’s gross profit margin was 66%, marking a 2.4 percentage point increase from 63.6% in the same quarter last year. Udemy’s full-year margin has also been trending up over the past 12 months, increasing by 3.1 percentage points. If this move continues, it could suggest better unit economics due to some combination of stable to improving pricing power and input costs.

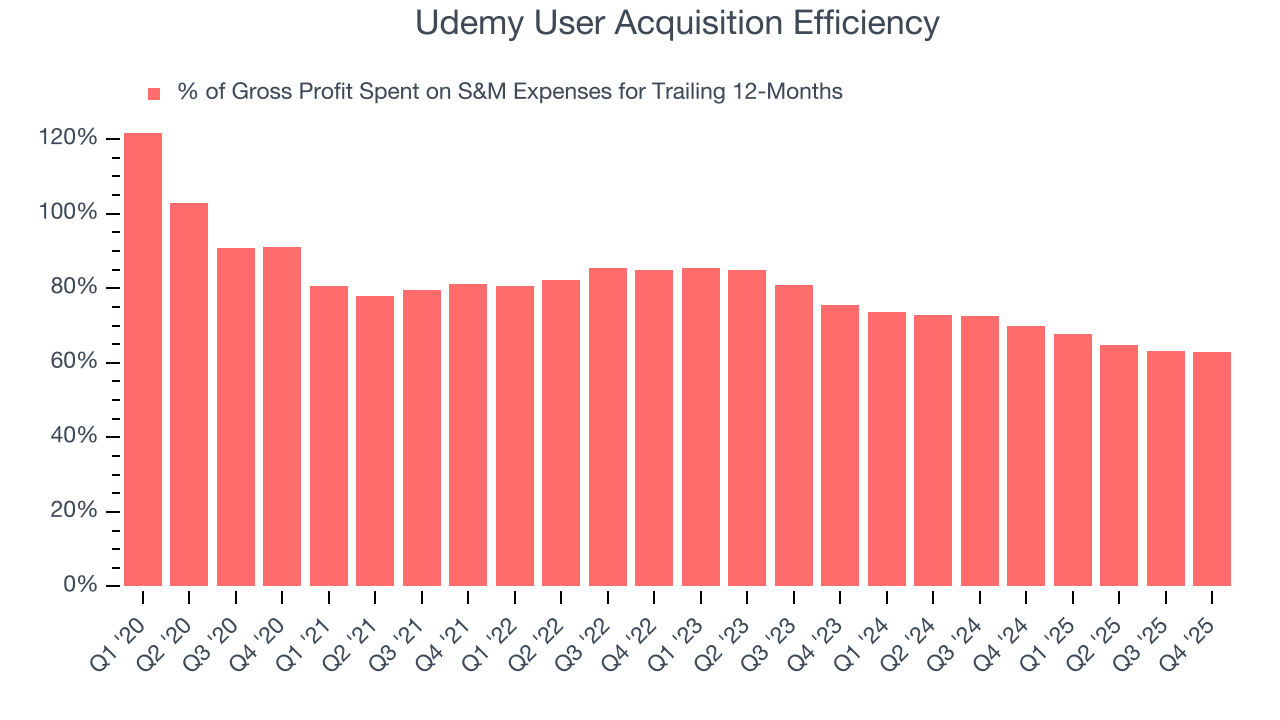

7. User Acquisition Efficiency

Consumer internet businesses like Udemy grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

It’s very expensive for Udemy to acquire new users as the company has spent 63% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates a highly competitive environment with little differentiation between Udemy and its peers.

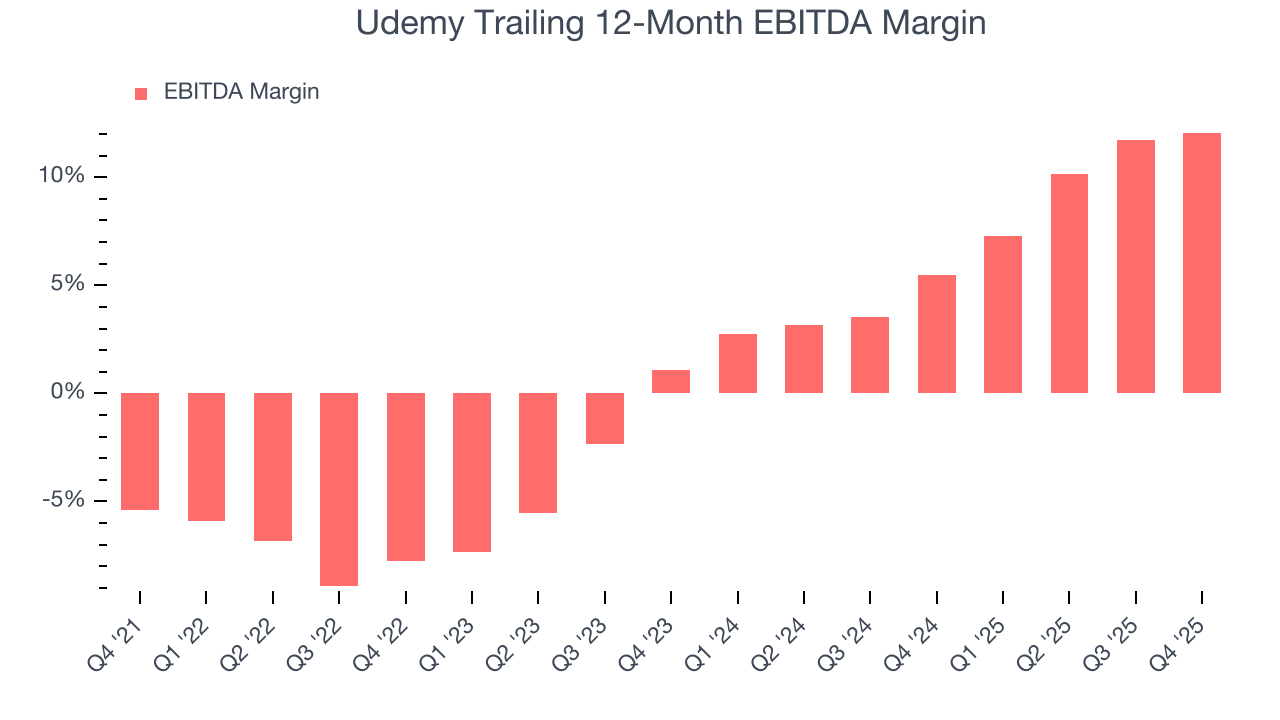

8. EBITDA

Investors frequently analyze operating income to understand a business’s core profitability. Similar to operating income, EBITDA is a common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of profit potential.

Udemy has been an efficient company over the last two years. It was one of the more profitable businesses in the consumer internet sector, boasting an average EBITDA margin of 8.8%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Udemy’s EBITDA margin rose by 19.8 percentage points over the last few years, as its sales growth gave it operating leverage.

In Q4, Udemy generated an EBITDA margin profit margin of 11.1%, up 1.3 percentage points year on year. Since its gross margin expanded more than its EBITDA margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

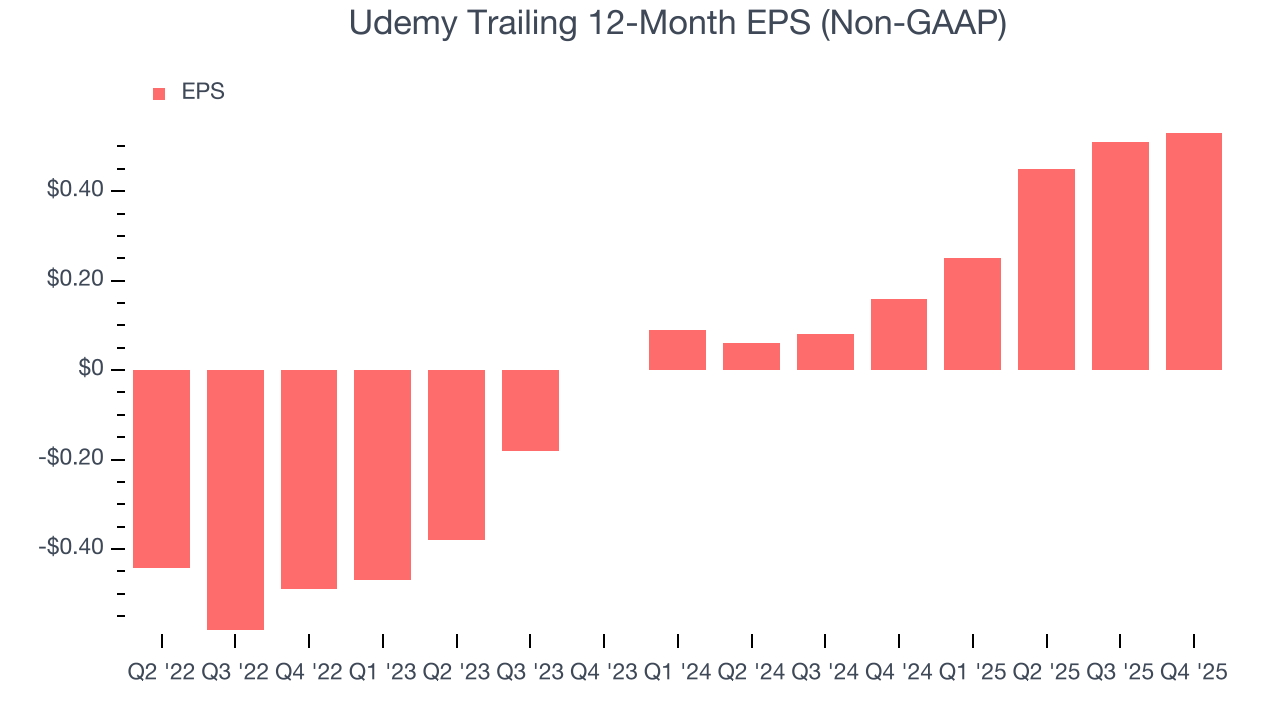

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Udemy’s full-year EPS flipped from negative to positive over the last three years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Udemy reported adjusted EPS of $0.12, up from $0.10 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Udemy’s full-year EPS of $0.53 to shrink by 12.6%.

10. Cash Is King

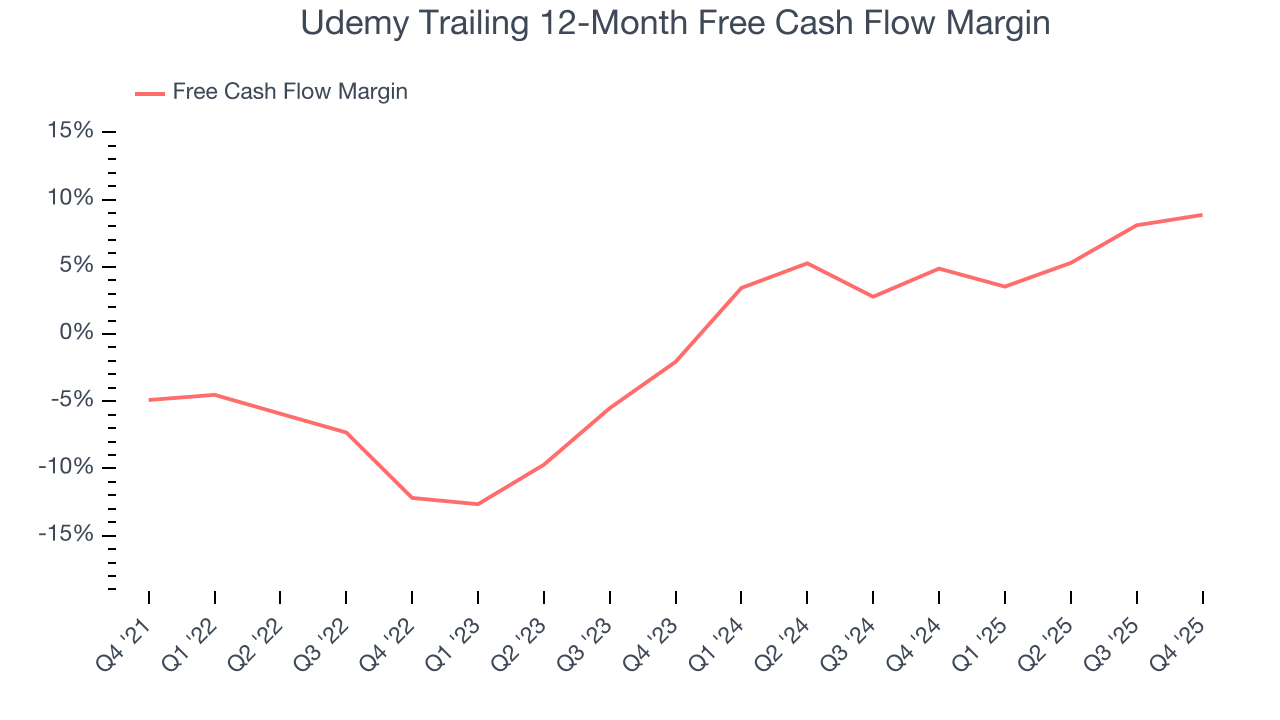

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Udemy has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.9% over the last two years, slightly better than the broader consumer internet sector.

Taking a step back, we can see that Udemy’s margin expanded by 21 percentage points over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Udemy’s free cash flow clocked in at $11.79 million in Q4, equivalent to a 6.1% margin. This result was good as its margin was 3 percentage points higher than in the same quarter last year, building on its favorable historical trend.

11. Balance Sheet Assessment

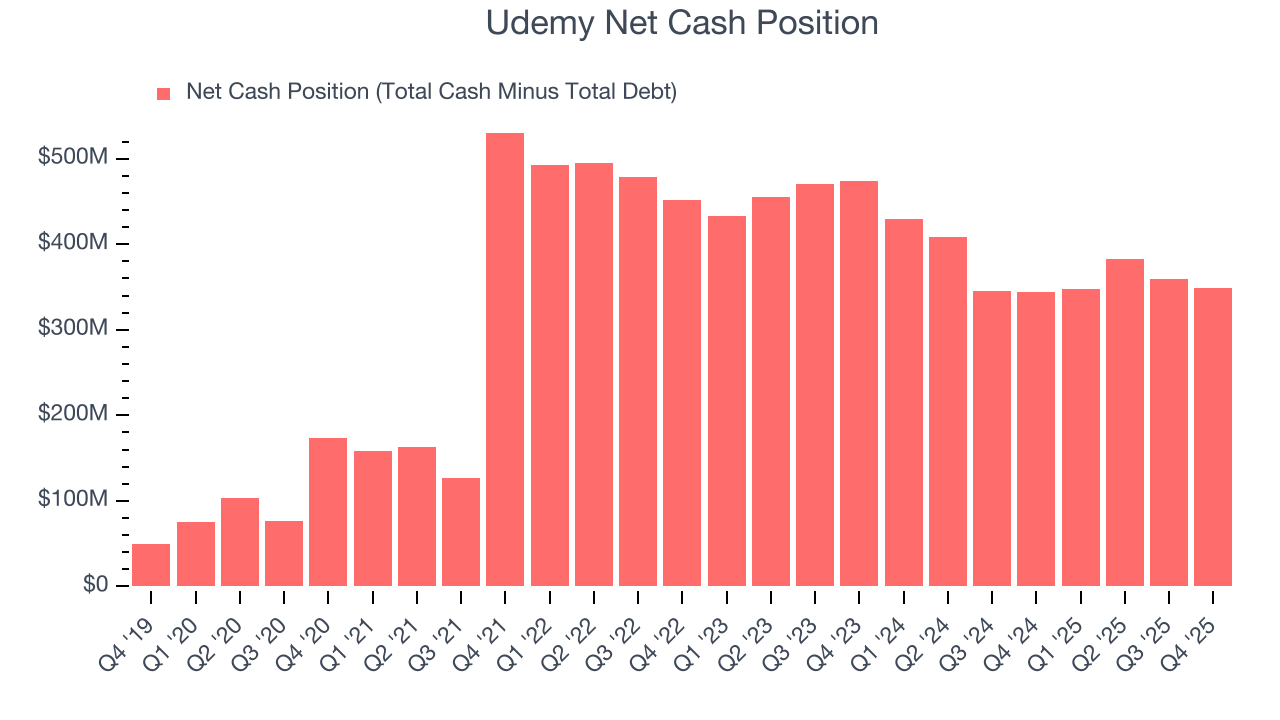

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Udemy is a well-capitalized company with $358.9 million of cash and $10.23 million of debt on its balance sheet. This $348.7 million net cash position is 50.1% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Udemy’s Q4 Results

We were impressed by how significantly Udemy blew past analysts’ EBITDA expectations this quarter. Zooming out, we think this was a solid print. The stock traded up 2.5% to $4.83 immediately after reporting.

On December 17, 2025, Udemy and Coursera entered into a definitive merger agreement under which Coursera will combine with Udemy in an all-stock transaction. Under the terms of the definitive agreement, Udemy stockholders will receive 0.800 shares of Coursera common stock for each share of Udemy common stock. Upon the closing of the transaction, existing Coursera stockholders are expected to own approximately 59% and existing Udemy stockholders are expected to own approximately 41% of the combined company, on a fully diluted basis.

13. Is Now The Time To Buy Udemy?

Updated: February 5, 2026 at 9:37 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Udemy.

Udemy isn’t a terrible business, but it isn’t one of our picks. To begin with, its revenue growth was uninspiring over the last three years, and analysts expect its demand to deteriorate over the next 12 months. And while its rising cash profitability gives it more optionality, the downside is its projected EPS for the next year is lacking. On top of that, its ARPU has declined over the last two years.

Udemy’s EV/EBITDA ratio based on the next 12 months is 3.6x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $8 on the company (compared to the current share price of $4.80).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.