Ulta (ULTA)

Ulta is intriguing. Its robust cash flows and returns on capital showcase its management team’s strong investing abilities.― StockStory Analyst Team

1. News

2. Summary

Why Ulta Is Interesting

Offering high-end prestige brands as well as lower-priced, mass-market ones, Ulta Beauty (NASDAQ:ULTA) is an American retailer that sells makeup, skincare, haircare, and fragrance products.

- Industry-leading 32.7% return on capital demonstrates management’s skill in finding high-return investments

- Rapid rollout of new stores to capitalize on market opportunities makes sense given its strong same-store sales performance

- A drawback is its large revenue base makes it harder to increase sales quickly, and its annual revenue growth of 6.7% over the last three years was below our standards for the consumer retail sector

Ulta has some noteworthy aspects. If you like the story, the valuation looks reasonable.

Why Is Now The Time To Buy Ulta?

At $534.50 per share, Ulta trades at 18.7x forward P/E. Looking at the consumer retail landscape, we think the price is reasonable for the quality you get.

If you think the market is not giving the company enough credit for its fundamentals, now could be a good time to invest.

3. Ulta (ULTA) Research Report: Q4 CY2025 Update

Beauty, cosmetics, and personal care retailer Ulta Beauty (NASDAQ:ULTA) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 11.8% year on year to $3.90 billion. Its GAAP profit of $8.01 per share was in line with analysts’ consensus estimates.

Ulta (ULTA) Q4 CY2025 Highlights:

- Revenue: $3.90 billion vs analyst estimates of $3.83 billion (11.8% year-on-year growth, 1.9% beat)

- EPS (GAAP): $8.01 vs analyst expectations of $8.03 (in line)

- Adjusted EBITDA: $596.2 million vs analyst estimates of $561.9 million (15.3% margin, 6.1% beat)

- EPS (GAAP) guidance for the upcoming financial year 2026 is $28.30 at the midpoint, missing analyst estimates by 1%

- Operating Margin: 12.2%, down from 14.8% in the same quarter last year

- Free Cash Flow Margin: 25.4%, down from 27.6% in the same quarter last year

- Locations: 1,591 at quarter end, up from 1,445 in the same quarter last year

- Same-Store Sales rose 5.8% year on year (1.5% in the same quarter last year)

- Market Capitalization: $28.95 billion

Company Overview

Offering high-end prestige brands as well as lower-priced, mass-market ones, Ulta Beauty (NASDAQ:ULTA) is an American retailer that sells makeup, skincare, haircare, and fragrance products.

Given its variety in both price point as well as product, Ulta serves as a one-stop-shop for beauty. The core customer is a middle to higher-income woman across a variety of ages. This customer has specific needs or tastes in beauty that may not be served by the narrower selection of a department store or mass merchandise retailer.

A typical store is around 10,000 square feet. Key sections include fragrance, makeup, skincare, and haircare. The makeup section tends to be the largest, and most sections allow customers to try out a variety of products before purchasing. In addition to these sections, stores may also offer salon and spa services, where customers can receive professional haircuts, color treatments, and waxing. Ulta also has an e-commerce presence, featuring not just products but reviews and tutorials, that the company has been investing in since 2008.

The brand selection in Ulta stores is diverse and constantly evolving based on customer tastes and broader trends in beauty. MAC, Clinique, and Urban Decay are globally-recognized brands that can be found in stores, for example. Additionally, there are brands exclusive to Ulta as well as emerging ones like Fourth Ray Beauty.

4. Beauty and Cosmetics Retailer

Beauty and cosmetics retailers understand that beauty is in the eye of the beholder, but a little lipstick, nail polish, and glowing skin also help the cause. These stores—which mostly cater to consumers but can also garner the attention of salon pros—aim to be a one-stop personal care and beauty products shop with many brands across many categories. E-commerce is changing how consumers buy cosmetics, so these retailers are constantly evolving to meet the customer where and how they want to shop.

Retailers specializing in beauty products include Sally Beauty (NYSE:SBH) and Bath & Body Works while department stores such as Kohl’s (NYSE:KSS) and Macy’s (NYSE:M) typically feature large cosmetics and fragrance sections.

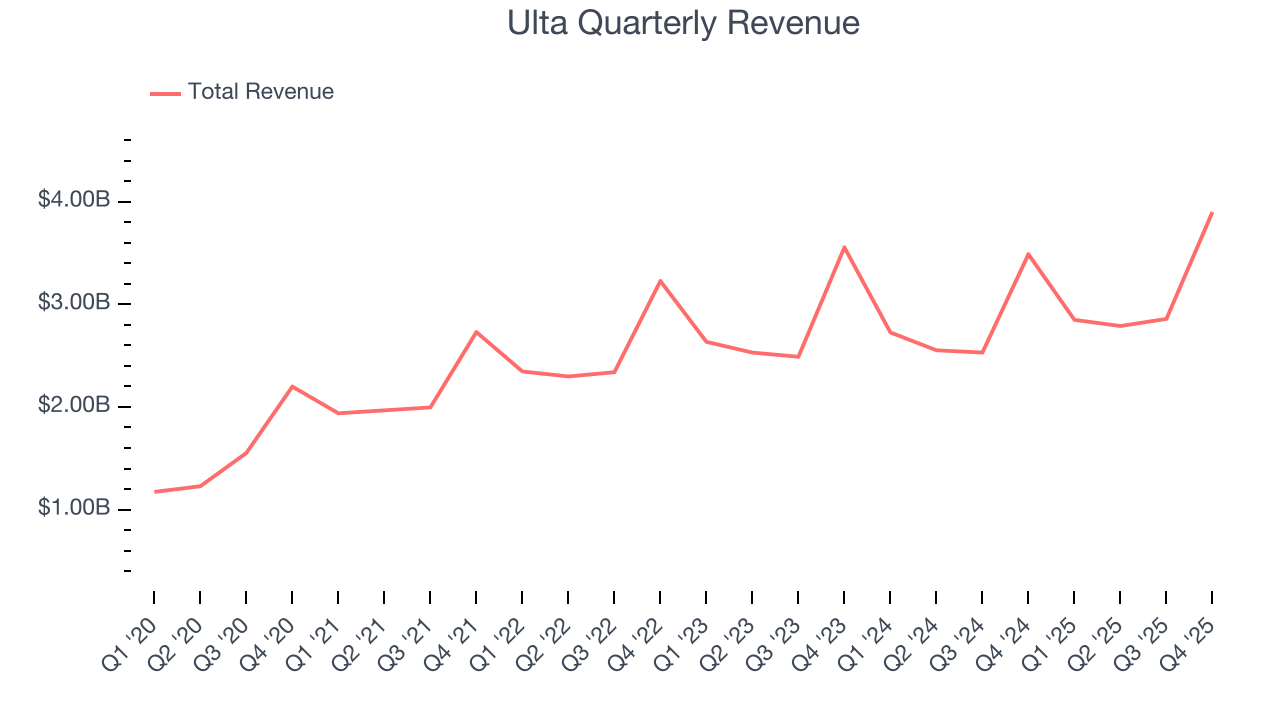

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $12.39 billion in revenue over the past 12 months, Ulta is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Ulta’s 6.7% annualized revenue growth over the last three years was tepid, but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, Ulta reported year-on-year revenue growth of 11.8%, and its $3.90 billion of revenue exceeded Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to grow 6.1% over the next 12 months, similar to its three-year rate. This projection is particularly noteworthy for a company of its scale and indicates the market is baking in success for its products.

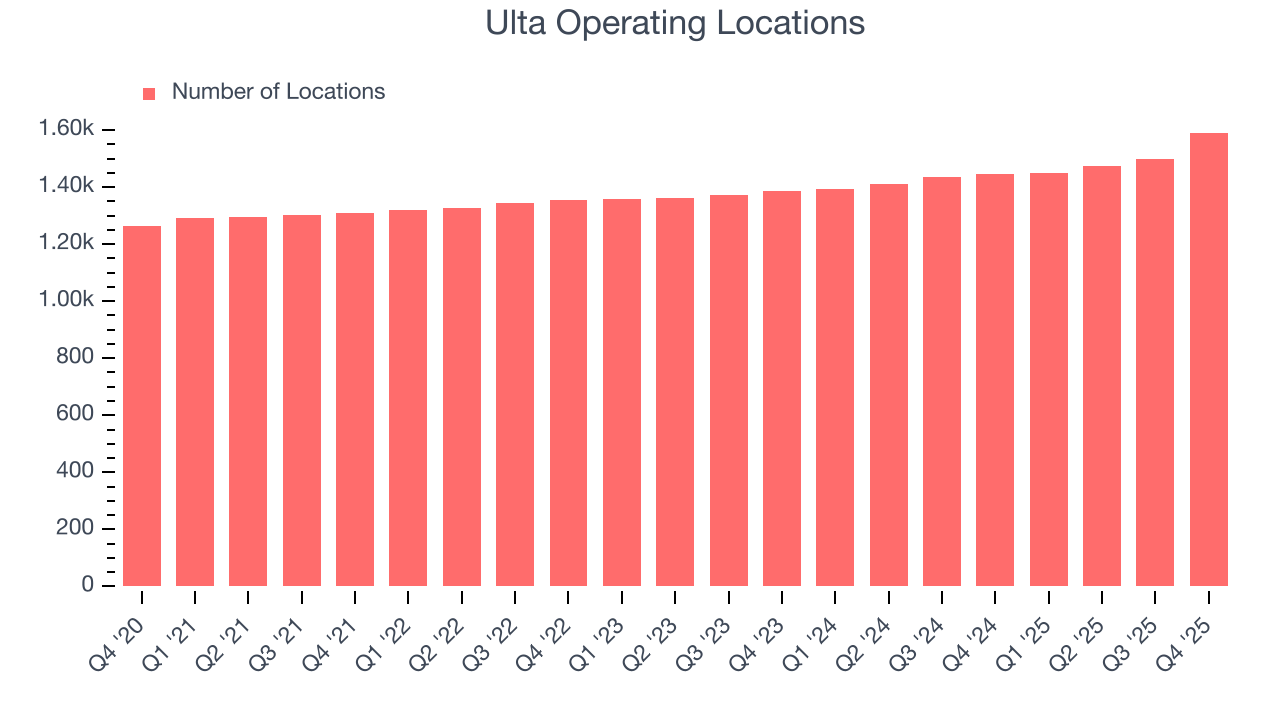

6. Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Ulta sported 1,591 locations in the latest quarter. Over the last two years, it has opened new stores at a rapid clip by averaging 4.8% annual growth, among the fastest in the consumer retail sector. This gives it a chance to become a large, scaled business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

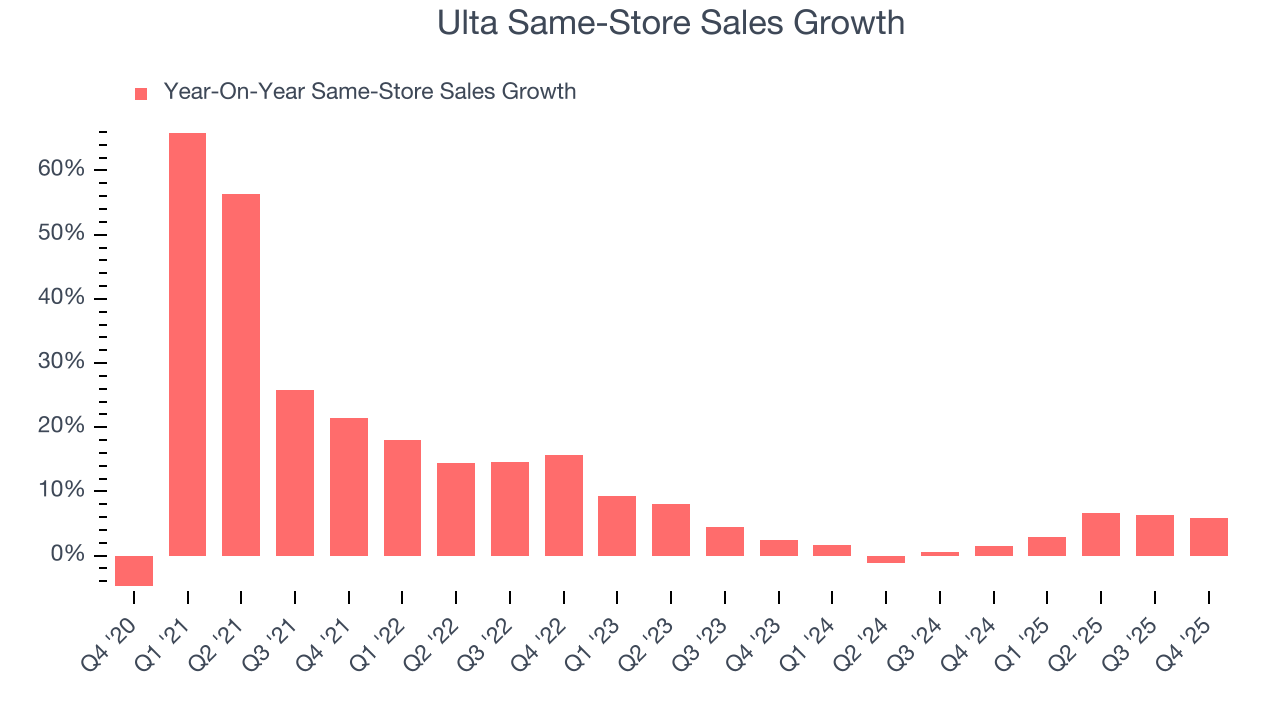

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Ulta’s demand has been healthy for a retailer over the last two years. On average, the company has grown its same-store sales by a robust 3% per year. This performance suggests its rollout of new stores could be beneficial for shareholders. When a retailer has demand, more locations should help it reach more customers and boost revenue growth.

In the latest quarter, Ulta’s same-store sales rose 5.8% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

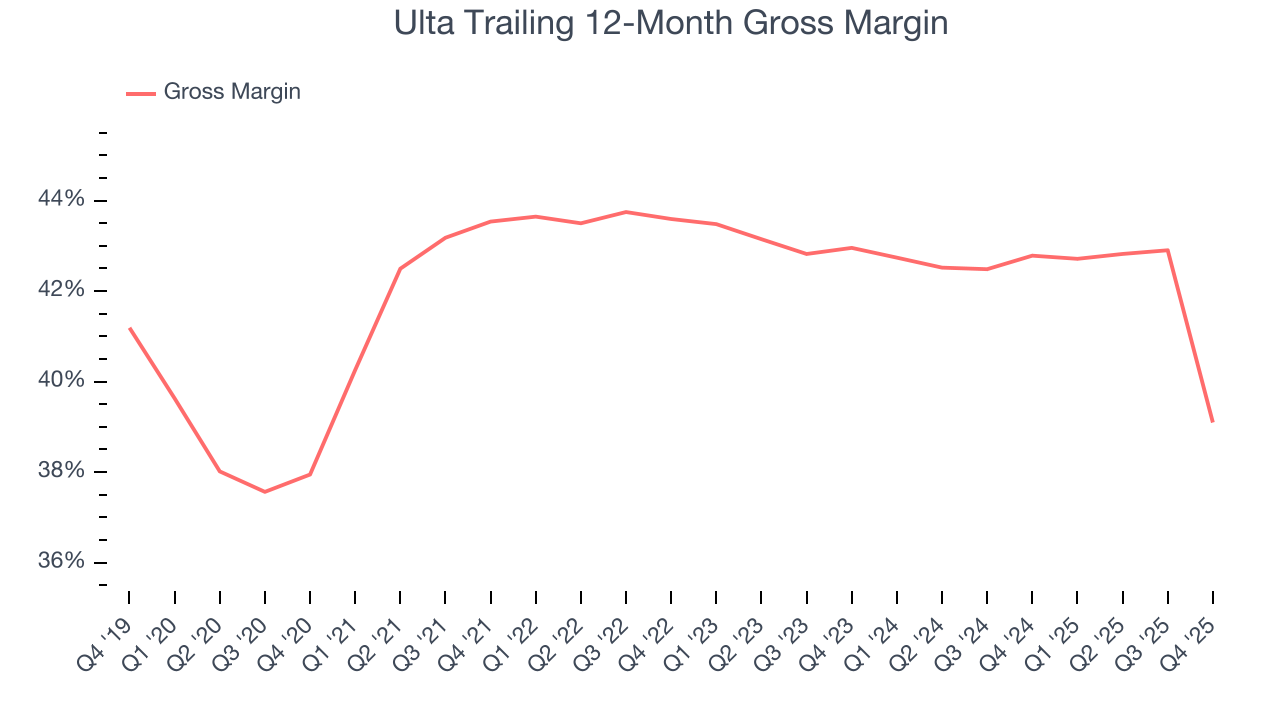

7. Gross Margin & Pricing Power

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

Ulta’s unit economics are higher than the typical retailer, giving it the flexibility to invest in areas such as marketing and talent to reach more consumers. As you can see below, it averaged a decent 40.9% gross margin over the last two years. That means for every $100 in revenue, $59.15 went towards paying for inventory, transportation, and distribution.

Ulta produced a 38.1% gross profit margin in Q4 , marking a 13 percentage point decrease from 51% in the same quarter last year. Ulta’s full-year margin has also been trending down over the past 12 months, decreasing by 3.7 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to discount products and higher input costs (such as labor and freight expenses to transport goods).

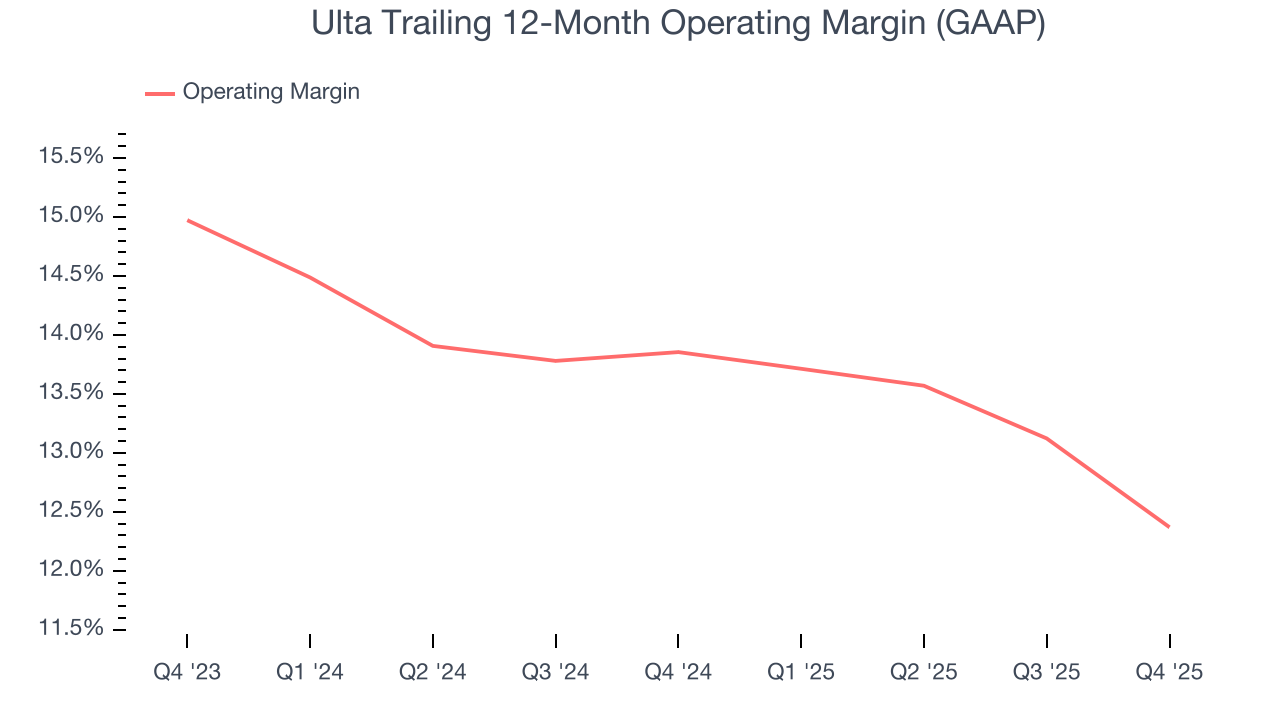

8. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Ulta has been an efficient company over the last two years. It was one of the more profitable businesses in the consumer retail sector, boasting an average operating margin of 13.1%.

Looking at the trend in its profitability, Ulta’s operating margin decreased by 1.5 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Ulta generated an operating margin profit margin of 12.2%, down 2.6 percentage points year on year. Since Ulta’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, and administrative overhead expenses.

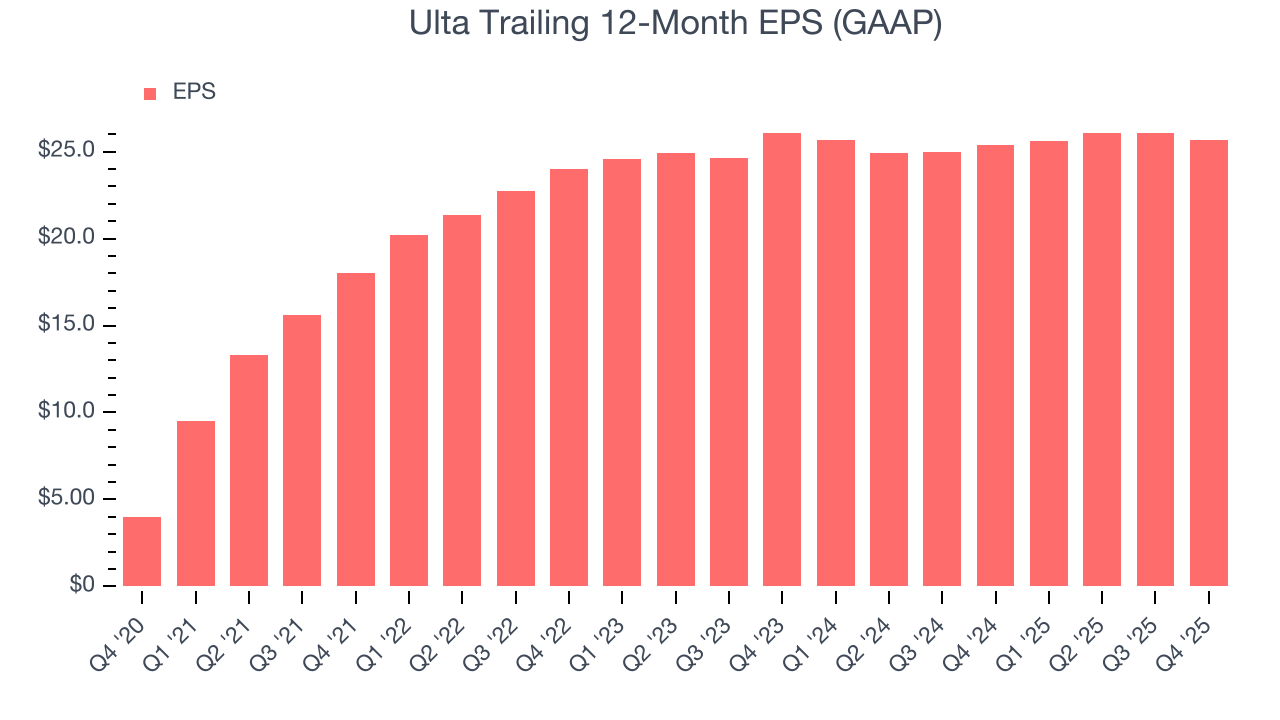

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Ulta’s EPS grew at an unimpressive 2.2% compounded annual growth rate over the last three years, lower than its 6.7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

In Q4, Ulta reported EPS of $8.01, down from $8.46 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Ulta’s full-year EPS of $25.64 to grow 11.6%.

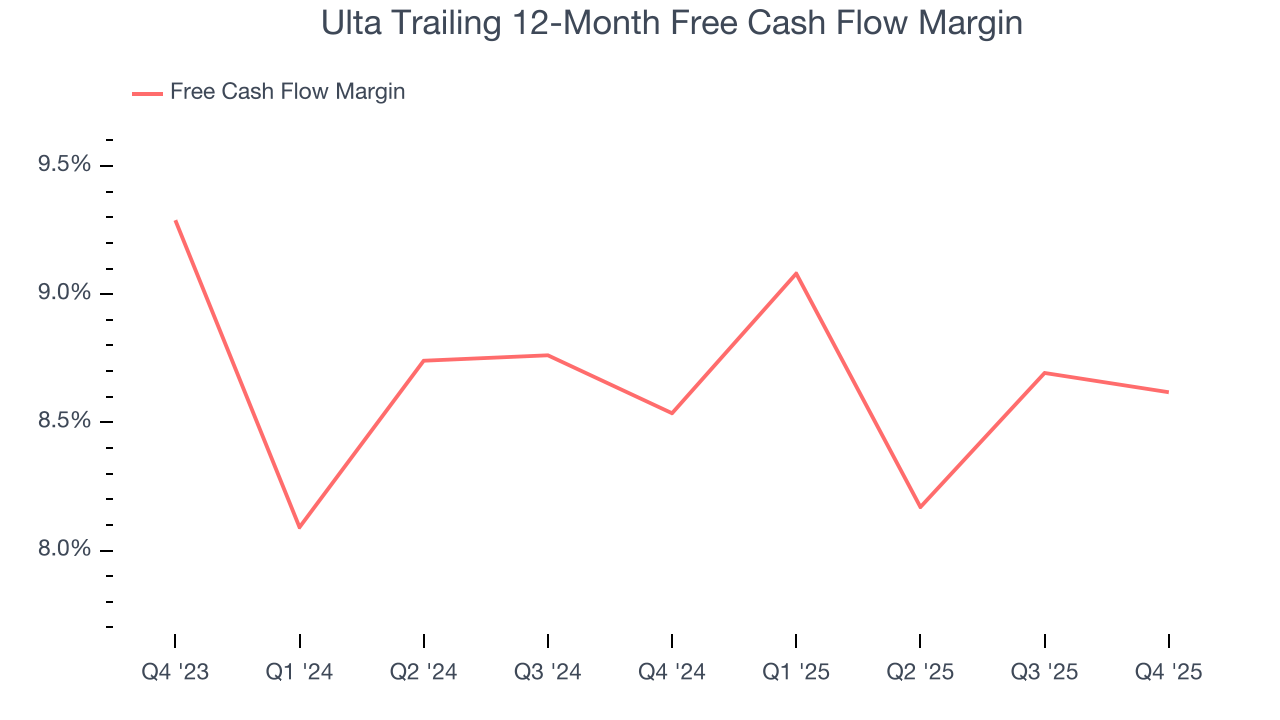

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Ulta has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 8.6% over the last two years, quite impressive for a consumer retail business.

Ulta’s free cash flow clocked in at $989 million in Q4, equivalent to a 25.4% margin. The company’s cash profitability regressed as it was 2.2 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, leading to short-term swings. Long-term trends trump temporary fluctuations.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Ulta’s five-year average ROIC was 32.7%, placing it among the best consumer retail companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

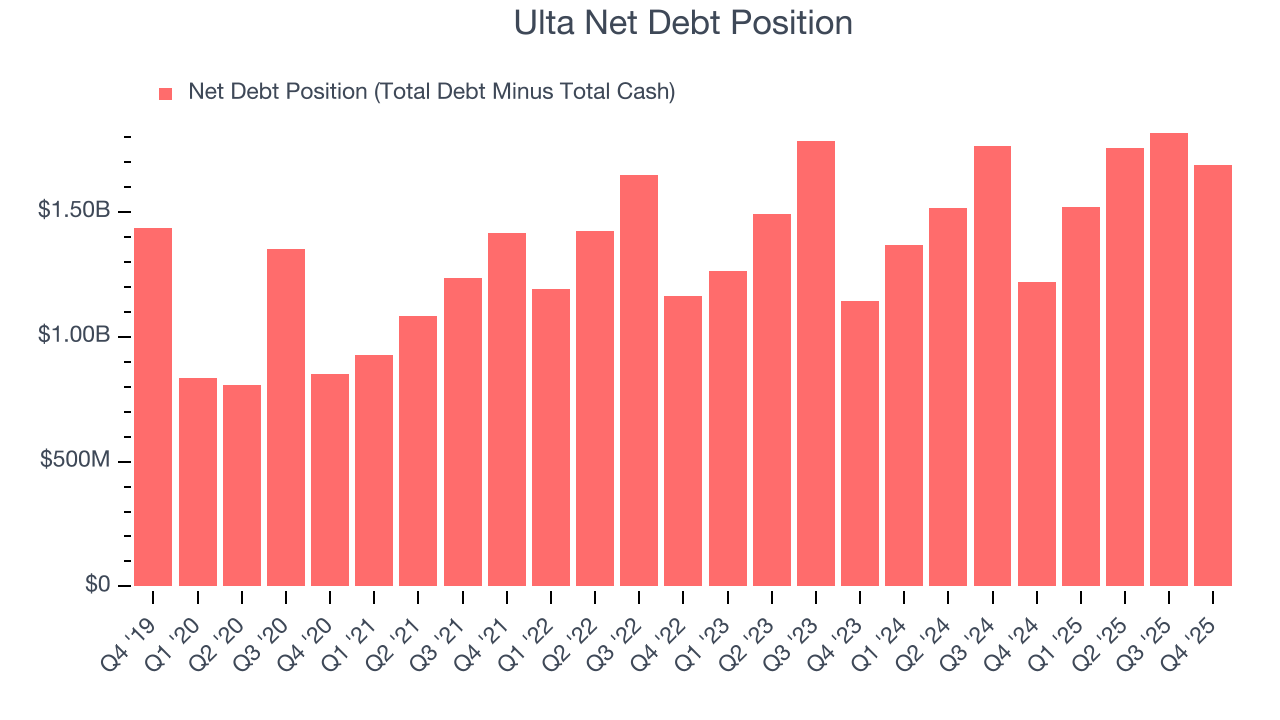

12. Balance Sheet Assessment

Ulta reported $494.2 million of cash and $2.18 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.87 billion of EBITDA over the last 12 months, we view Ulta’s 0.9× net-debt-to-EBITDA ratio as safe. We also see its $3.46 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Ulta’s Q4 Results

We enjoyed seeing Ulta beat analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance slightly missed. Overall, this print had some key positives. The market seemed to be hoping for more, and the stock traded down 9.5% to $570.97 immediately following the results.

14. Is Now The Time To Buy Ulta?

Updated: March 22, 2026 at 10:47 PM EDT

Before making an investment decision, investors should account for Ulta’s business fundamentals and valuation in addition to what happened in the latest quarter.

We think Ulta is a good business. Although its revenue growth was a little slower over the last three years, its new store openings have increased its brand equity. And while its mediocre EPS growth over the last three years shows it’s failed to produce meaningful profits for shareholders, its stellar ROIC suggests it has been a well-run company historically.

Ulta’s P/E ratio based on the next 12 months is 18.7x. Looking at the consumer retail landscape right now, Ulta trades at a pretty interesting price. If you’re a fan of the business and management team, now is a good time to scoop up some shares.

Wall Street analysts have a consensus one-year price target of $679.50 on the company (compared to the current share price of $534.50), implying they see 27.1% upside in buying Ulta in the short term.