Dick's (DKS)

Dick's is a sound business. Its demand is through the roof, as seen by its rapid growth in same-store sales and physical locations.― StockStory Analyst Team

1. News

2. Summary

Why Dick's Is Interesting

Started as a hunting supply store, Dick’s Sporting Goods (NYSE:DKS) is a retailer that sells merchandise for traditional sports as well as for fitness and outdoor activities.

- Projected revenue growth of 29.5% for the next 12 months is above its three-year trend, pointing to accelerating demand

- Fast expansion of new stores to reach markets with few or no locations is justified by its same-store sales growth

- A downside is its gross margin of 34.9% is an output of its commoditized inventory

Dick's has some noteworthy aspects. If you believe in the company, the price seems reasonable.

Why Is Now The Time To Buy Dick's?

Dick’s stock price of $192.17 implies a valuation ratio of 13.8x forward P/E. Scanning companies across the consumer retail space, we think that Dick’s valuation is appropriate for the business quality.

It could be a good time to invest if you see something the market doesn’t.

3. Dick's (DKS) Research Report: Q4 CY2025 Update

Sporting goods retailer Dick’s Sporting Goods (NYSE:DKS) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 59.9% year on year to $6.23 billion. The company’s full-year revenue guidance of $22.25 billion at the midpoint came in 2.2% above analysts’ estimates. Its non-GAAP profit of $3.45 per share was 17.4% above analysts’ consensus estimates.

Dick's (DKS) Q4 CY2025 Highlights:

- Revenue: $6.23 billion vs analyst estimates of $6.08 billion (59.9% year-on-year growth, 2.5% beat)

- Adjusted EPS: $3.45 vs analyst estimates of $2.94 (17.4% beat)

- Adjusted EBITDA: $465.3 million vs analyst estimates of $466.4 million (7.5% margin, in line)

- Adjusted EPS guidance for the upcoming financial year 2026 is $14 at the midpoint, missing analyst estimates by 5.6%

- Operating Margin: 3%, down from 9.9% in the same quarter last year

- Free Cash Flow Margin: 11.3%, up from 10.1% in the same quarter last year

- Same-Store Sales were flat year on year (6.4% in the same quarter last year)

- Market Capitalization: $17.59 billion

Company Overview

Started as a hunting supply store, Dick’s Sporting Goods (NYSE:DKS) is a retailer that sells merchandise for traditional sports as well as for fitness and outdoor activities.

The core customer is anyone in need of balls, bats, rackets, or other equipment for traditional sports such as basketball, baseball, or tennis. Dick’s also addresses the needs of fitness and outdoor enthusiasts due to their selection of exercise equipment such as weights and hunting, fishing, and camping equipment such as binoculars. The breadth of sports and activities covered and the depth of product in each category is what differentiates Dick’s. Sporting goods can be large and cumbersome, so general merchandise retailers who devote limited space will have limited selection.

A Dick's store ranges from around 30,000 to 70,000 square feet, with some larger flagship locations exceeding 100,000 square feet. At the entrance is usually a large, open space that features seasonal displays and promotions. The store is then typically divided into sections such as athletic/casual apparel, sneakers/footwear, then sections based on specific sports. The company also has a developed e-commerce presence, which Dick’s launched in 1997 as an early adopter of online shopping. Many customers choose to order online and pick up at their nearest store.

4. Sports & Outdoor Equipment Retailer

Some of us spend our leisure time vegging out, but many others take to the courts, fields, beaches, and campsites; sports equipment retailers cater to the avid sportsman as well as the weekend warrior. Shoppers can find everything from tents to lawn games to baseball bats to satisfy their athletic and leisure needs along with competitive prices and helpful store associates that can talk through brands, sizing, and product quality. This is a category that has moved rapidly online over the last few decades, so these sports and outdoor equipment retailers have needed to be nimble and aggressive with their e-commerce and omnichannel presences.

Retailers offering sporting and outdoor goods include Academy Sports and Outdoor (NASDAQ:ASO), Sportsman’s Warehouse (NASDAQ:SPWH), and Hibbett (NASDAQ:HIBB).

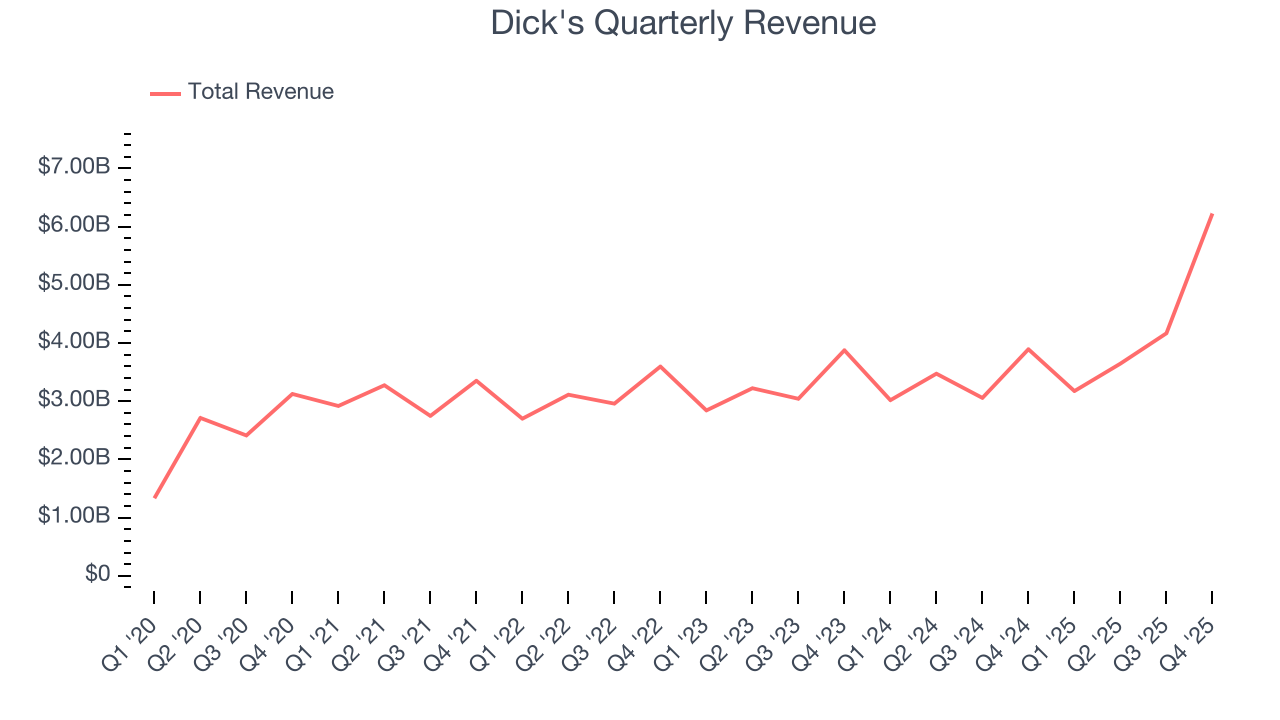

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $17.22 billion in revenue over the past 12 months, Dick's is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences purchasing decisions.

As you can see below, Dick’s 11.7% annualized revenue growth over the last three years was decent as it opened new stores and increased sales at existing, established locations.

This quarter, Dick's reported magnificent year-on-year revenue growth of 59.9%, and its $6.23 billion of revenue beat Wall Street’s estimates by 2.5%.

Looking ahead, sell-side analysts expect revenue to grow 28% over the next 12 months, an acceleration versus the last three years. This projection is eye-popping for a company of its scale and implies its newer products will fuel better top-line performance.

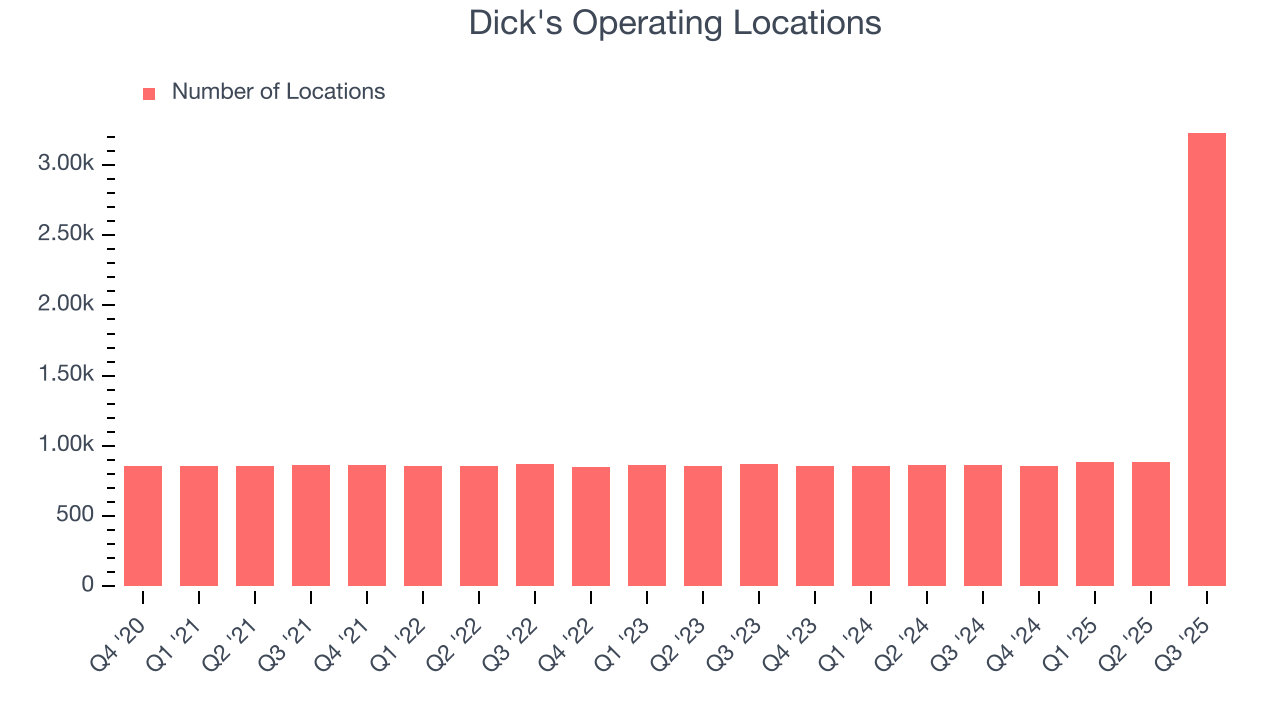

6. Store Performance

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Dick's opened new stores at a rapid clip over the last two years, averaging 39.9% annual growth, much faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Note that Dick's reports its store count intermittently, so some data points are missing in the chart below.

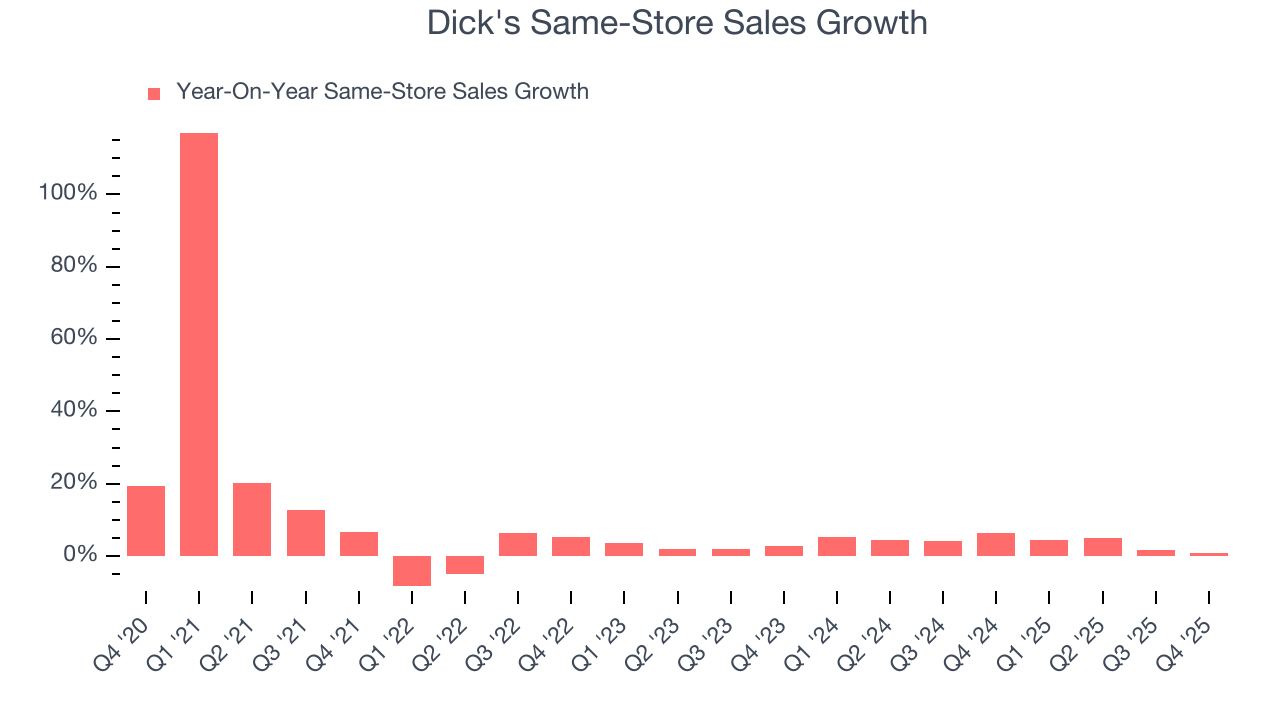

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Dick’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 4.1% per year. This performance along with its meaningful buildout of new stores suggest it’s playing some aggressive offense.

In the latest quarter, Dick’s year on year same-store sales were flat. This was a meaningful deceleration from its historical levels. We’ll be watching closely to see if Dick's can reaccelerate growth.

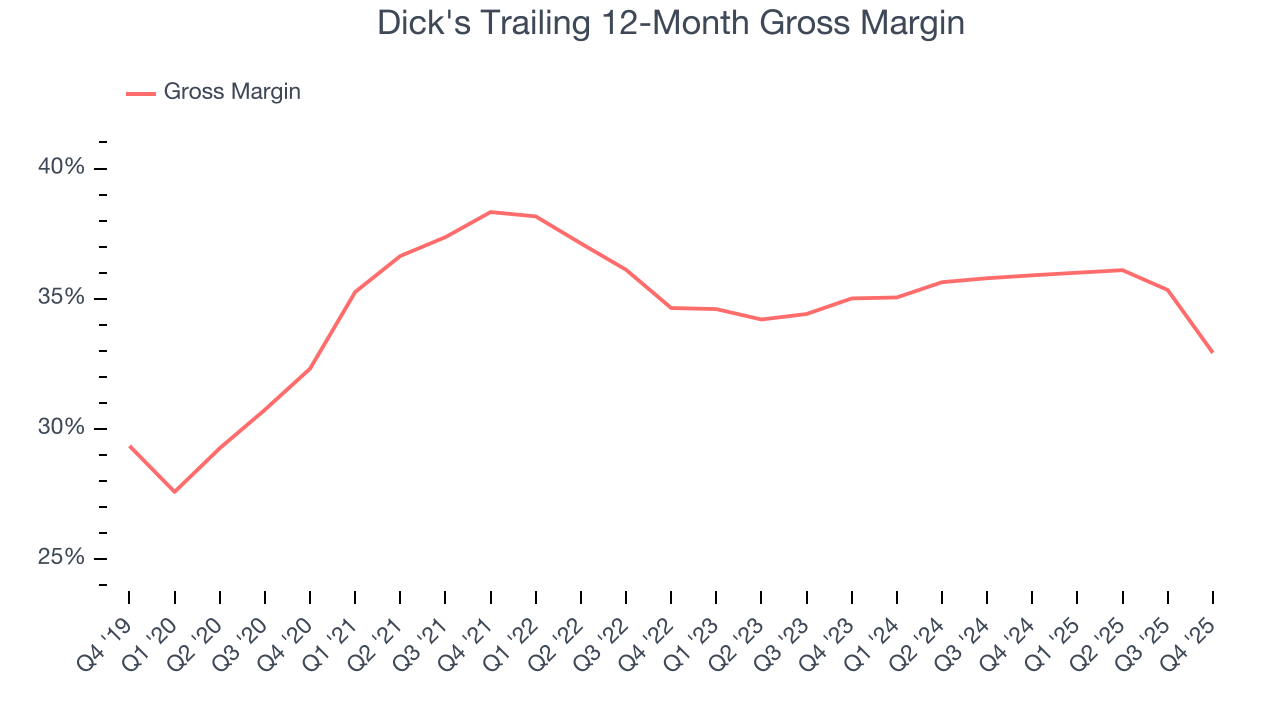

7. Gross Margin & Pricing Power

Dick's has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 34.2% gross margin over the last two years. Said differently, Dick's had to pay a chunky $65.77 to its suppliers for every $100 in revenue.

In Q4, Dick's produced a 28.4% gross profit margin , marking a 6.5 percentage point decrease from 35% in the same quarter last year. Dick’s full-year margin has also been trending down over the past 12 months, decreasing by 3 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to discount products and higher input costs (such as labor and freight expenses to transport goods).

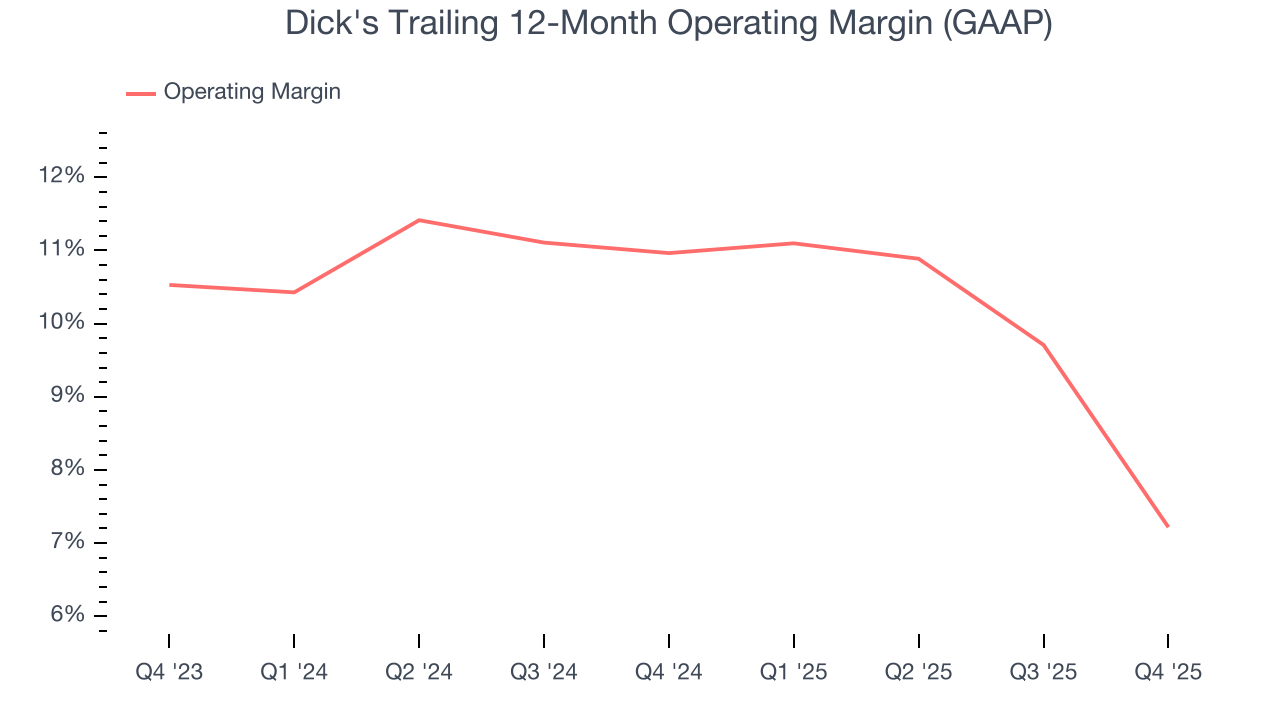

8. Operating Margin

Operating margin is an important measure of profitability for retailers as it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

Dick's has done a decent job managing its cost base over the last two years. The company has produced an average operating margin of 8.9%, higher than the broader consumer retail sector.

Looking at the trend in its profitability, Dick’s operating margin decreased by 3.7 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Dick's generated an operating margin profit margin of 3%, down 7 percentage points year on year. Since Dick’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, and administrative overhead increased.

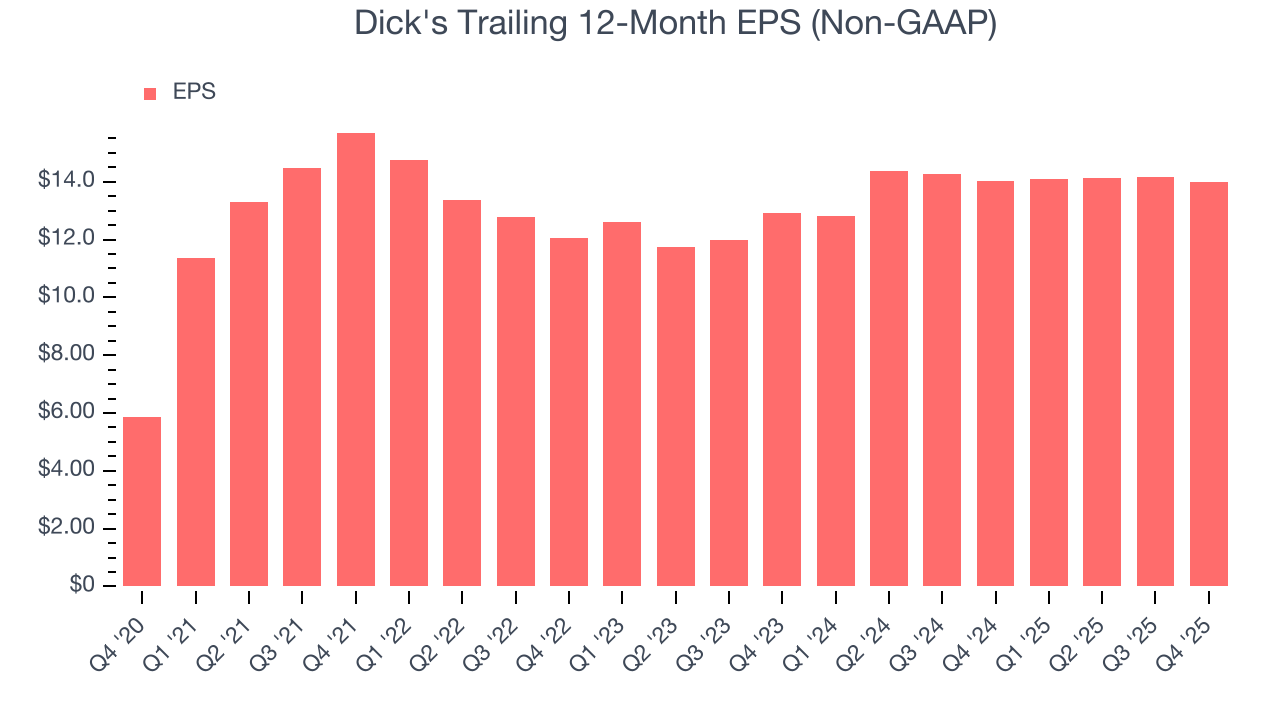

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Dick’s EPS grew at an unimpressive 5% compounded annual growth rate over the last three years, lower than its 11.7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Dick's reported adjusted EPS of $3.45, down from $3.62 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Dick’s full-year EPS of $13.98 to grow 6%.

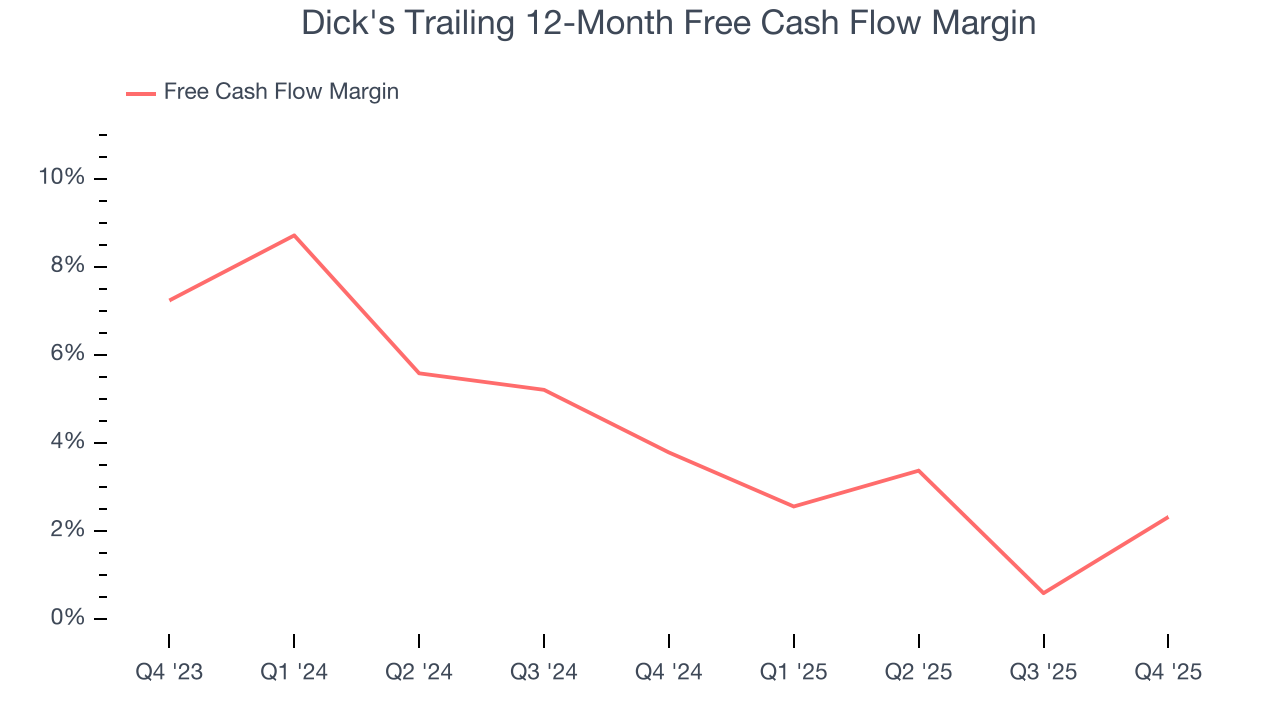

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Dick's has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 3% over the last two years, slightly better than the broader consumer retail sector.

Taking a step back, we can see that Dick’s margin dropped by 1.5 percentage points over the last year. This decrease came from the higher costs associated with opening more stores.

Dick’s free cash flow clocked in at $706.2 million in Q4, equivalent to a 11.3% margin. This result was good as its margin was 1.2 percentage points higher than in the same quarter last year. Its cash profitability was also above its two-year level, and we hope the company can build on this trend.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Dick’s five-year average ROIC was 21.8%, beating other consumer retail companies by a wide margin. This illustrates its management team’s ability to invest in attractive growth opportunities and produce tangible results for shareholders.

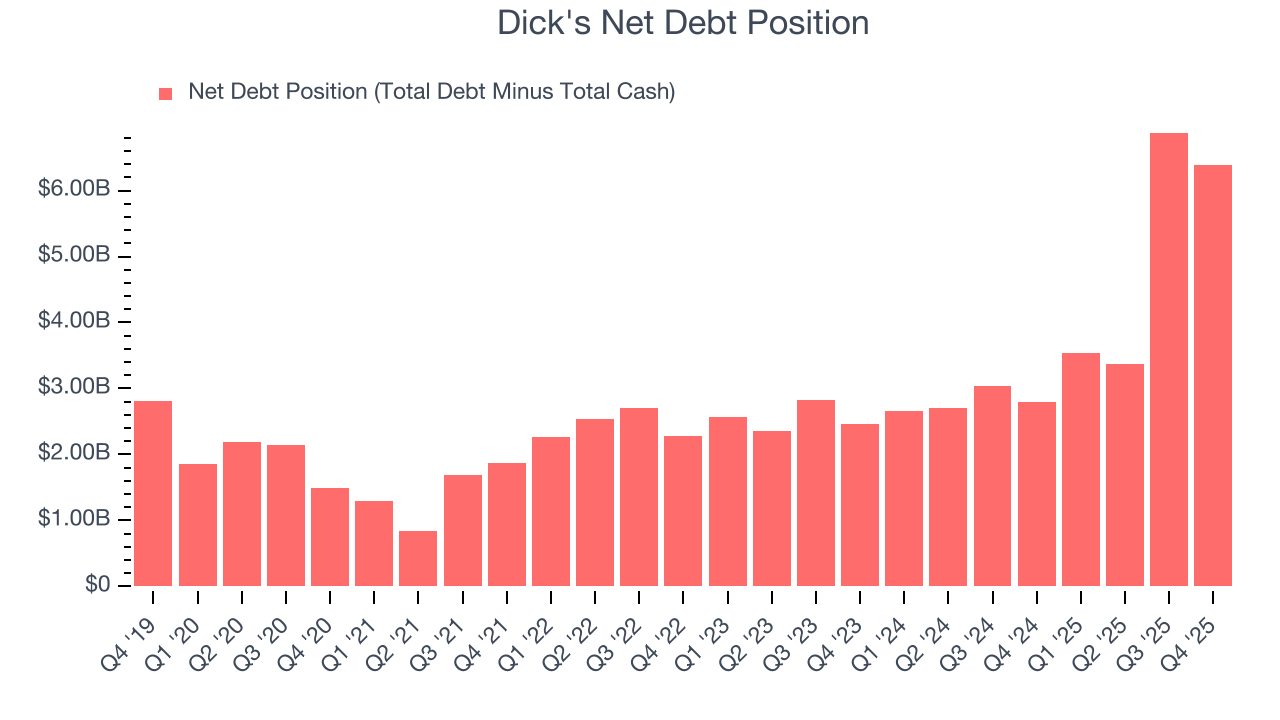

12. Balance Sheet Assessment

Dick's reported $1.35 billion of cash and $7.75 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.87 billion of EBITDA over the last 12 months, we view Dick’s 3.4× net-debt-to-EBITDA ratio as safe. We also see its $4.27 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Dick’s Q4 Results

We enjoyed seeing Dick's beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its gross margin fell short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock traded up 1.8% to $198.49 immediately after reporting.

14. Is Now The Time To Buy Dick's?

Updated: March 14, 2026 at 10:40 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Dick's, you should also grasp the company’s longer-term business quality and valuation.

There are a lot of things to like about Dick's. First off, its revenue growth was solid over the last three years and is expected to accelerate over the next 12 months. And while its gross margins make it more challenging to reach positive operating profits compared to other consumer retail businesses, its new store openings have increased its brand equity. On top of that, its wonderful same-store sales growth is among the best in the consumer retail sector.

Dick’s P/E ratio based on the next 12 months is 13.8x. When scanning the consumer retail space, Dick's trades at a fair valuation. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $234.76 on the company (compared to the current share price of $192.17), implying they see 22.2% upside in buying Dick's in the short term.