Vital Farms (VITL)

We see potential in Vital Farms. Its impressive sales growth and high returns on capital tee it up for fast and profitable expansion.― StockStory Analyst Team

1. News

2. Summary

Why Vital Farms Is Interesting

With an emphasis on ethically produced products, Vital Farms (NASDAQ:VITL) specializes in pasture-raised eggs and butter.

- Earnings per share grew by 288% annually over the last three years and trumped its peers

- Products are flying off the shelves as its unit sales averaged 25.3% growth over the past two years

- One pitfall is its subscale operations are evident in its revenue base of $759.4 million, meaning it has fewer distribution channels than its larger rivals (but more room for growth)

Vital Farms shows some promise. If you’re a believer, the price seems fair.

Why Is Now The Time To Buy Vital Farms?

At $17.32 per share, Vital Farms trades at 13.2x forward P/E. Vital Farms’s valuation is lower than that of many in the consumer staples space. Even so, we think it is justified for the revenue growth characteristics.

If you think the market is not giving the company enough credit for its fundamentals, now could be a good time to invest.

3. Vital Farms (VITL) Research Report: Q4 CY2025 Update

Egg and butter company Vital Farms (NASDAQ:VITL) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 28.7% year on year to $213.6 million. On the other hand, the company’s full-year revenue guidance of $910 million at the midpoint came in 3.1% below analysts’ estimates. Its GAAP profit of $0.35 per share was 11% below analysts’ consensus estimates.

Vital Farms (VITL) Q4 CY2025 Highlights:

- Revenue: $213.6 million vs analyst estimates of $213.3 million (28.7% year-on-year growth, in line)

- EPS (GAAP): $0.35 vs analyst expectations of $0.39 (11% miss)

- Adjusted EBITDA: $29.24 million vs analyst estimates of $30.59 million (13.7% margin, 4.4% miss)

- EBITDA guidance for the upcoming financial year 2026 is $110 million at the midpoint, below analyst estimates of $133.7 million

- Operating Margin: 10%, up from 7.8% in the same quarter last year

- Free Cash Flow was -$32.15 million compared to -$3.38 million in the same quarter last year

- Market Capitalization: $1.11 billion

Company Overview

With an emphasis on ethically produced products, Vital Farms (NASDAQ:VITL) specializes in pasture-raised eggs and butter.

The company was founded in 2007 by Matt O'Hare, who had a vision of transforming and championing ethical food practices. Vital Farms started with just 20 hens, and over the years, the company grew organically rather than through the acquisitions that are common for farm-based or agricultural businesses.

Today, Vital Farms is renowned for its pasture-raised eggs. Unlike conventional "free-range" or "cage-free" labels, pasture-raised labels mean that chickens genuinely spend significant time outdoors. Vital Farms also offers butter, egg bites, and ghee.

Vital Farms' core customer is the conscious consumer. This customer cares about where their food comes from, how it's produced, and the impact it has on the environment and animal welfare. These individuals often pay a premium for products they trust and believe in.

Vital Farms enjoys widespread distribution with its products stocked in national grocery chains and local health-conscious food stores.

4. Perishable Food

The perishable food industry is diverse, encompassing large-scale producers and distributors to specialty and artisanal brands. These companies sell produce, dairy products, meats, and baked goods and have become integral to serving modern American consumers who prioritize freshness, quality, and nutritional value. Investing in perishable food stocks presents both opportunities and challenges. While the perishable nature of products can introduce risks related to supply chain management and shelf life, it also creates a constant demand driven by the necessity for fresh food. Companies that can efficiently manage inventory, distribution, and quality control are well-positioned to thrive in this competitive market. Navigating the perishable food industry requires adherence to strict food safety standards, regulations, and labeling requirements.

Cal-Maine Foods (NASDAQ:CALM) is a publicly-traded competitor and dominant player in the egg industry. Private competitors include Rose Acre Farms Hillandale Farms, but Cal-Maine’s scale and market share are unique.

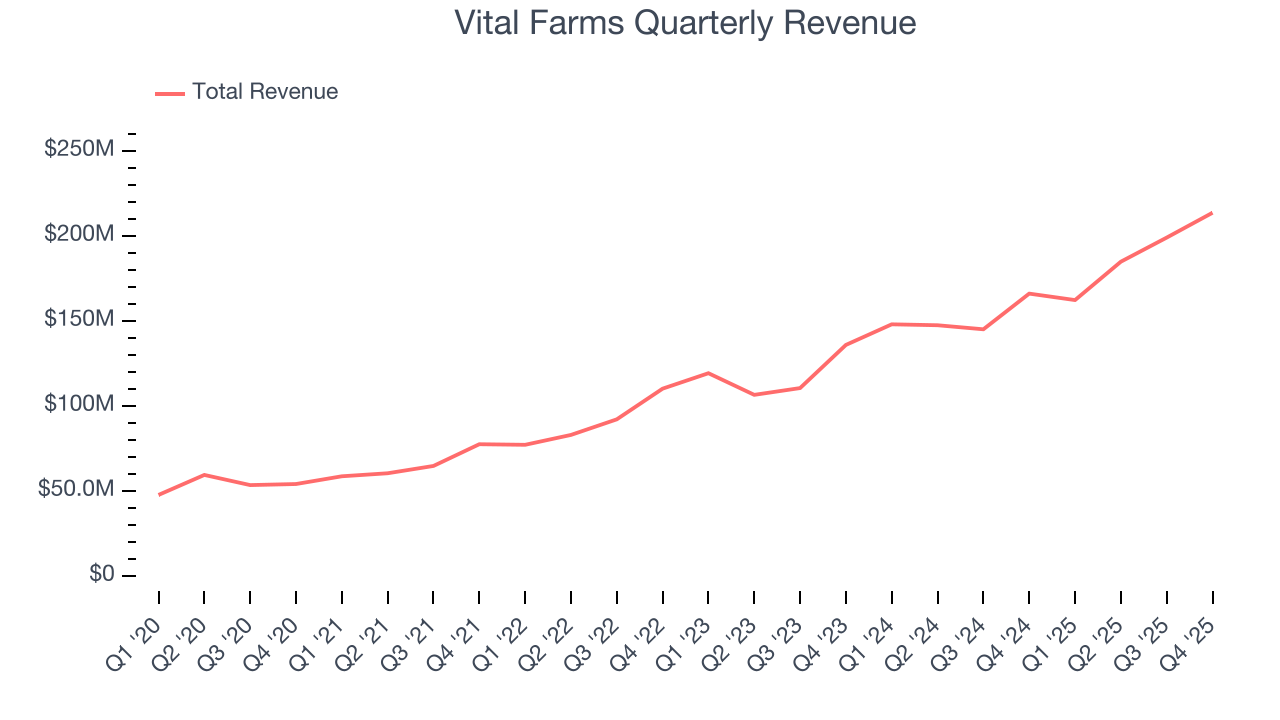

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $759.4 million in revenue over the past 12 months, Vital Farms is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, Vital Farms’s sales grew at an exceptional 28% compounded annual growth rate over the last three years as consumers bought more of its products.

This quarter, Vital Farms’s year-on-year revenue growth of 28.7% was excellent, and its $213.6 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 23.8% over the next 12 months, a deceleration versus the last three years. Still, this projection is healthy and implies the market is forecasting success for its products.

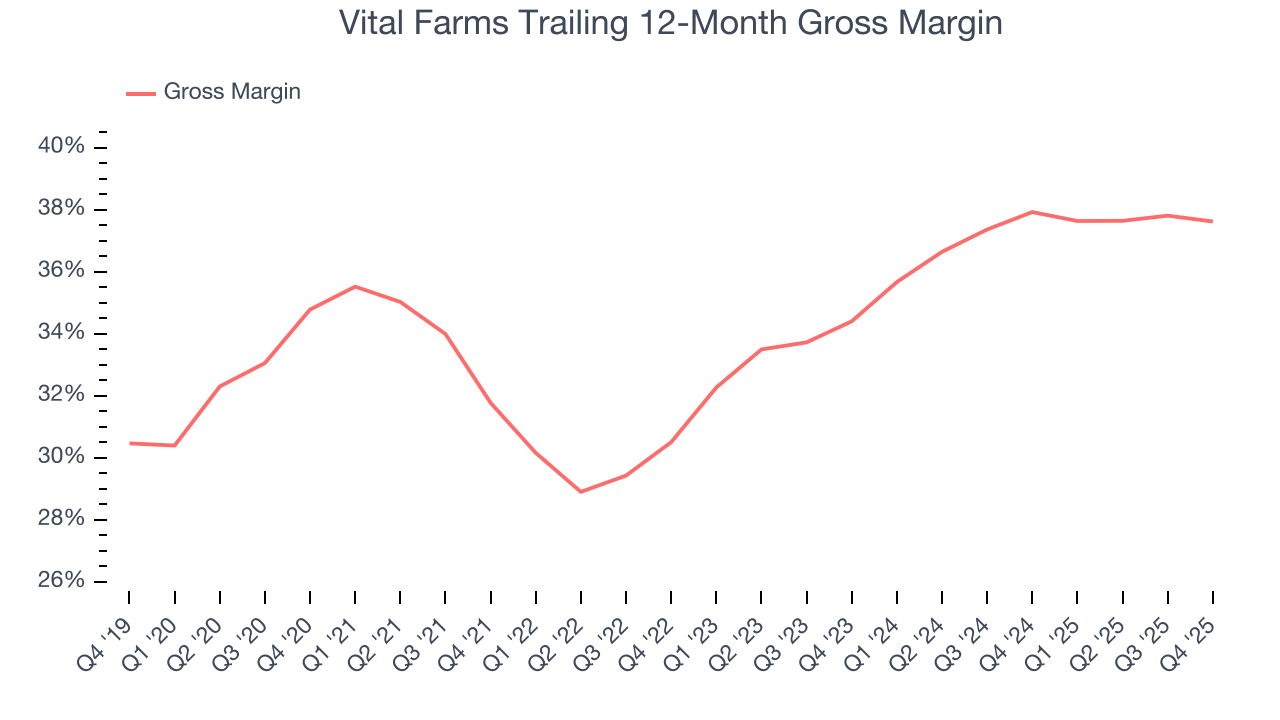

6. Gross Margin & Pricing Power

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products, has a stronger brand, and commands pricing power.

Vital Farms has good unit economics for a consumer staples company, giving it the opportunity to invest in areas such as marketing and talent to stay competitive. As you can see below, it averaged an impressive 37.8% gross margin over the last two years. That means for every $100 in revenue, $62.25 went towards paying for raw materials, production of goods, transportation, and distribution.

Vital Farms’s gross profit margin came in at 35.8% this quarter, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

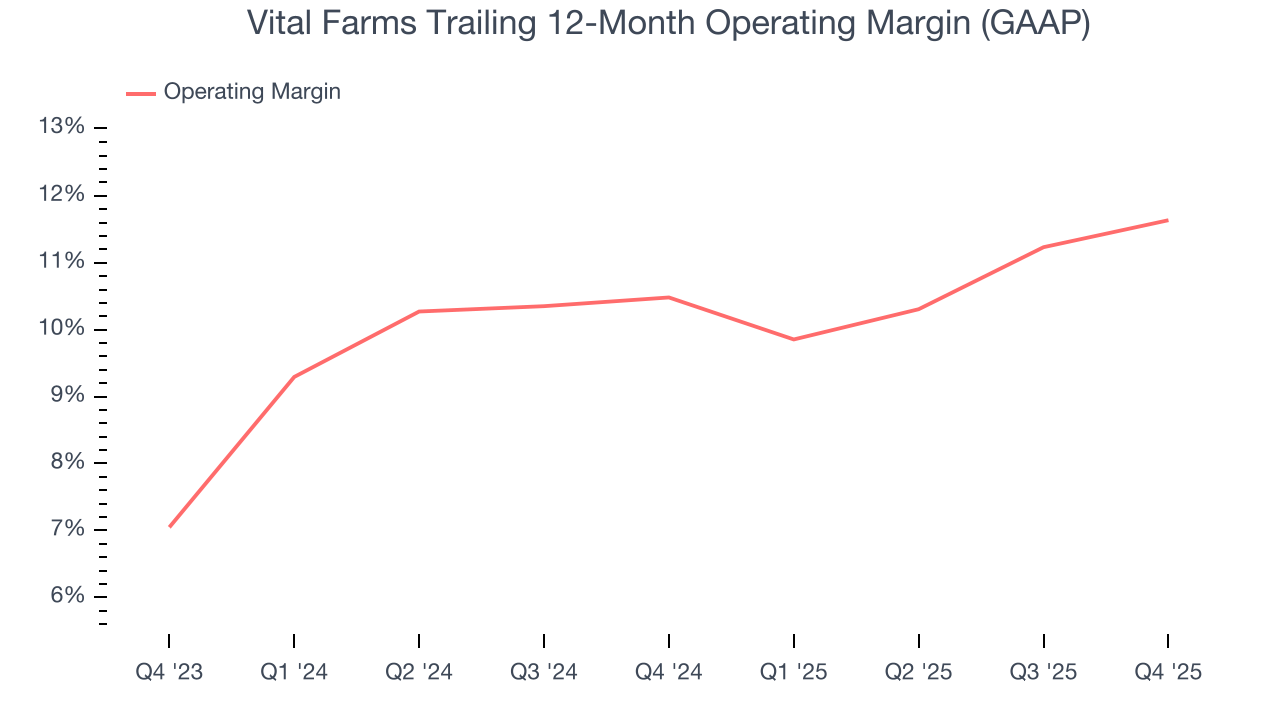

7. Operating Margin

Vital Farms has managed its cost base well over the last two years. It demonstrated solid profitability for a consumer staples business, producing an average operating margin of 11.1%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Vital Farms’s operating margin rose by 1.2 percentage points over the last year, as its sales growth gave it operating leverage.

This quarter, Vital Farms generated an operating margin profit margin of 10%, up 2.2 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

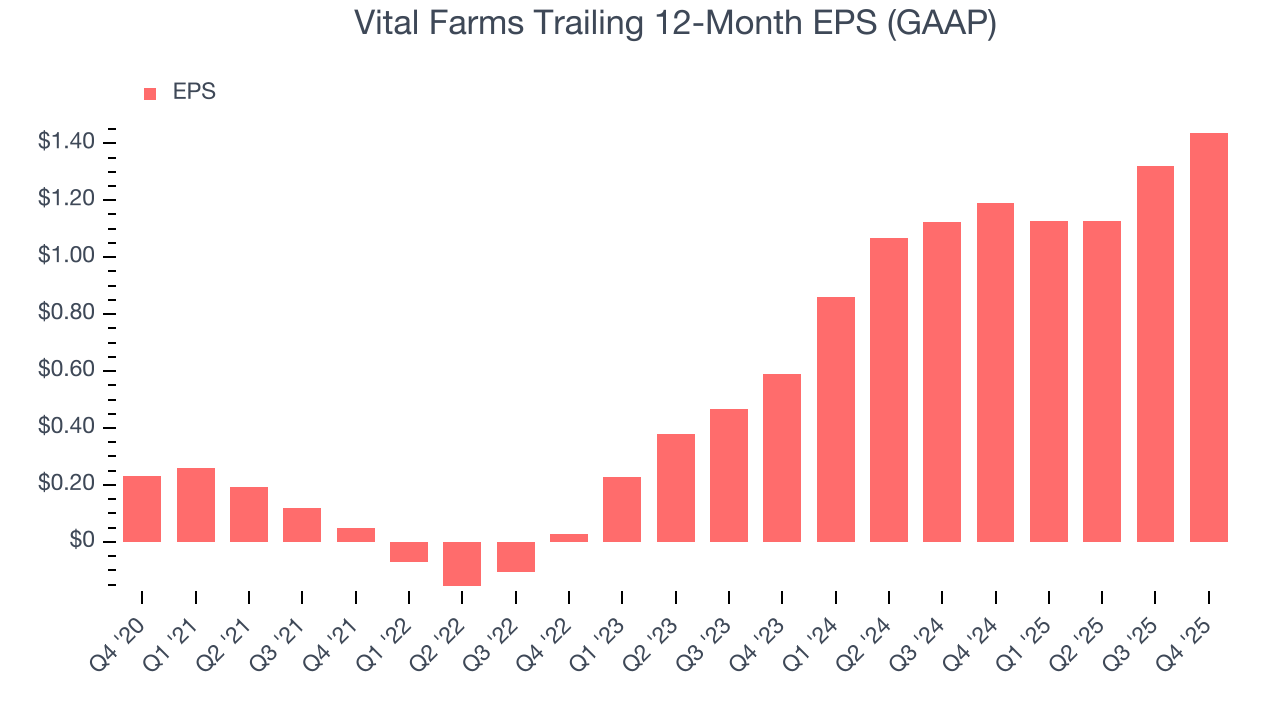

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Vital Farms’s EPS grew at an astounding 278% compounded annual growth rate over the last three years, higher than its 28% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q4, Vital Farms reported EPS of $0.35, up from $0.23 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Vital Farms’s full-year EPS of $1.44 to grow 18%.

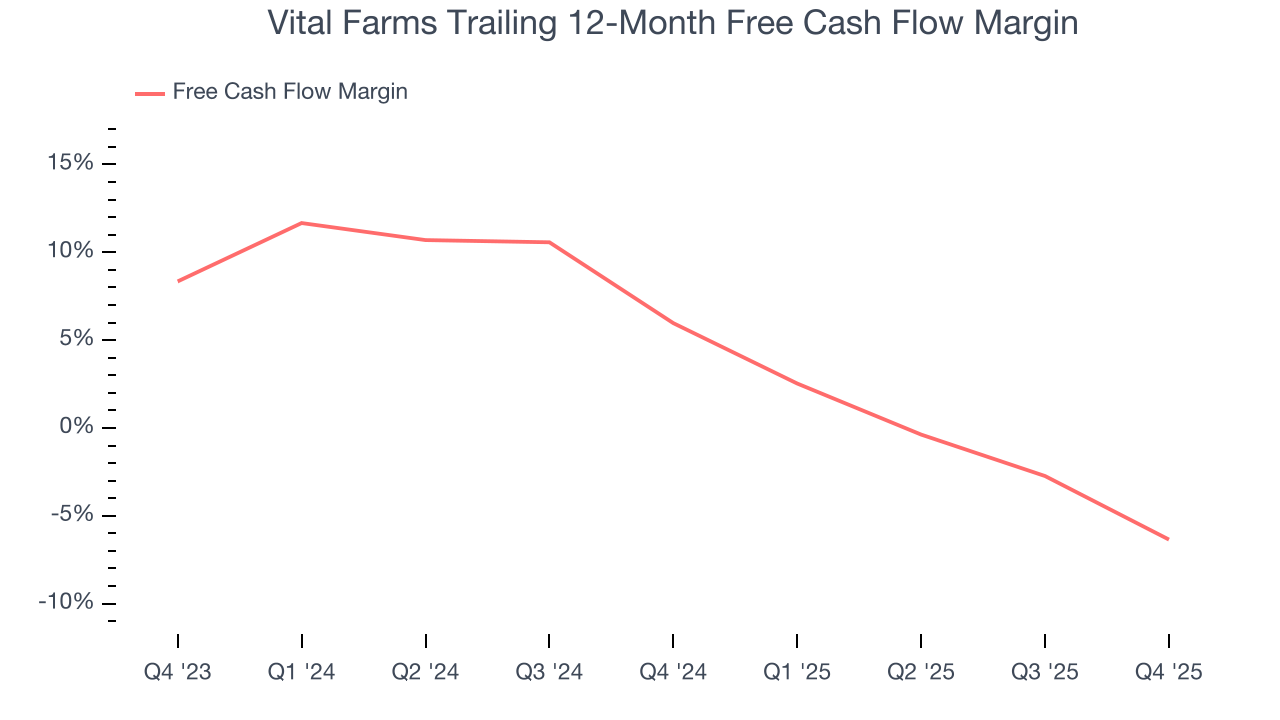

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Vital Farms broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders. The divergence from its good operating margin stems from its capital-intensive business model, which requires Vital Farms to make large cash investments in working capital and capital expenditures.

Taking a step back, we can see that Vital Farms’s margin dropped by 12.3 percentage points over the last year. If the trend continues, it could signal it’s in the middle of a big investment cycle.

Vital Farms burned through $32.15 million of cash in Q4, equivalent to a negative 15.1% margin. The company’s cash burn increased from $3.38 million of lost cash in the same quarter last year.

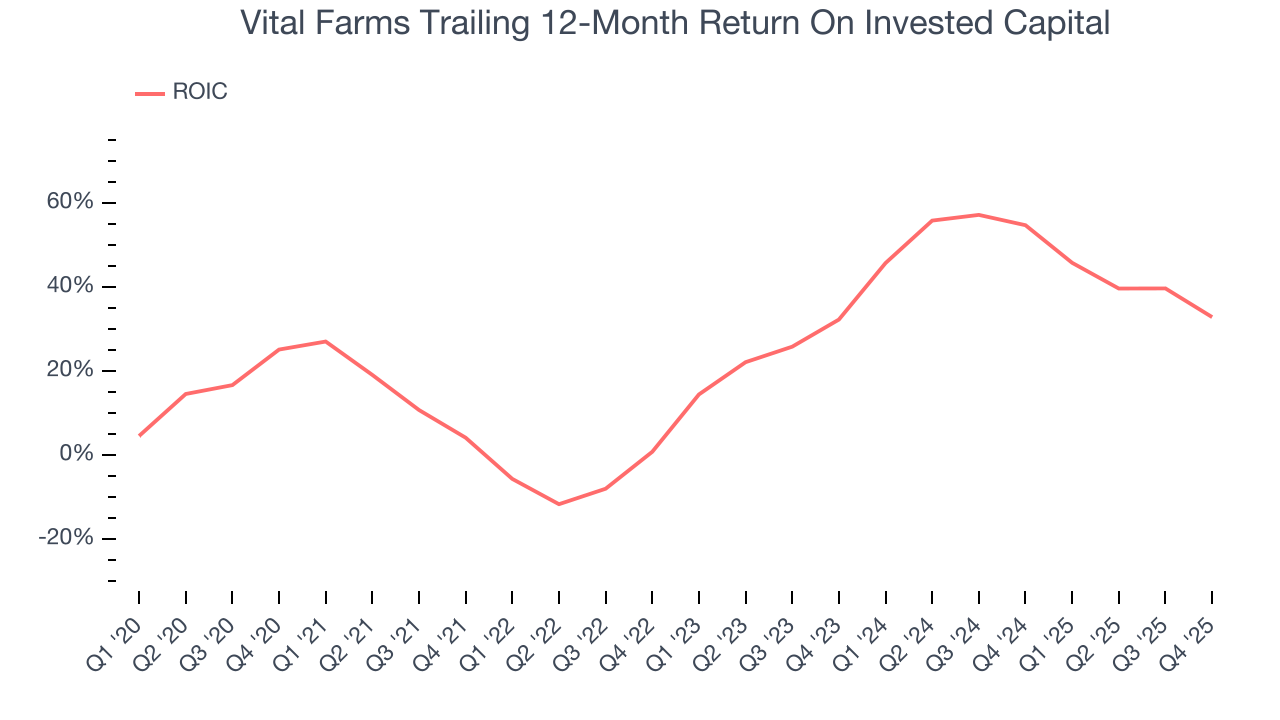

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Vital Farms’s five-year average ROIC was 25%, beating other consumer staples companies by a wide margin. This illustrates its management team’s ability to invest in attractive growth opportunities and produce tangible results for shareholders.

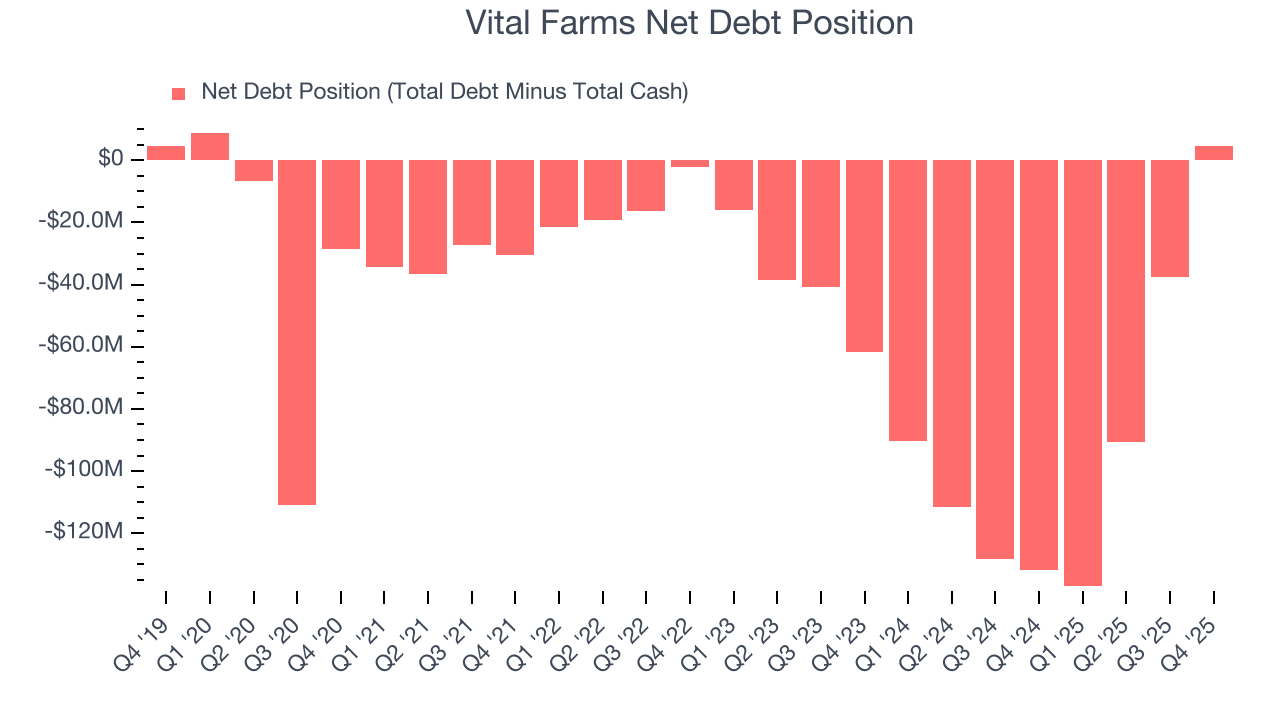

11. Balance Sheet Assessment

Vital Farms reported $48.83 million of cash and $53.49 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $114 million of EBITDA over the last 12 months, we view Vital Farms’s 0.0× net-debt-to-EBITDA ratio as safe. We also see its $2.16 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Vital Farms’s Q4 Results

We struggled to find many positives in these results. Its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.9% to $24.08 immediately after reporting.

13. Is Now The Time To Buy Vital Farms?

Updated: March 15, 2026 at 10:52 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Vital Farms, you should also grasp the company’s longer-term business quality and valuation.

There are some positives when it comes to Vital Farms’s fundamentals. To kick things off, its revenue growth was exceptional over the last three years. And while its cash profitability fell over the last year, its volume growth has been in a league of its own. On top of that, its EPS growth over the last three years has been fantastic.

Vital Farms’s P/E ratio based on the next 12 months is 13.2x. Looking at the consumer staples space right now, Vital Farms trades at a compelling valuation. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $36.50 on the company (compared to the current share price of $17.32), implying they see 111% upside in buying Vital Farms in the short term.