VSE Corporation (VSEC)

VSE Corporation piques our interest. Its revenue is growing quickly while its profitability is rising, giving it multiple ways to win.― StockStory Analyst Team

1. News

2. Summary

Why VSE Corporation Is Interesting

With roots dating back to 1959 and a strategic focus on extending the life of transportation assets, VSE Corporation (NASDAQ:VSEC) provides aftermarket parts distribution and maintenance, repair, and overhaul services for aircraft and vehicle fleets in commercial and government markets.

- Demand for the next 12 months is expected to accelerate above its two-year trend as Wall Street forecasts robust revenue growth of 44%

- Incremental sales over the last five years boosted profitability as its annual earnings per share growth of 13.8% outstripped its revenue performance

- A blemish is its cash-burning history makes us doubt the long-term viability of its business model

VSE Corporation shows some potential. The stock is up 395% over the last five years.

Why Should You Watch VSE Corporation

VSE Corporation is trading at $208.52 per share, or 44.2x forward P/E. The rich valuation multiple means there is a lot of good news priced into the stock; short-term price swings could result if anything bursts that bubble.

If VSE Corporation strings together a few solid quarters and proves it can be a high-quality company, we’d be more open to investing.

3. VSE Corporation (VSEC) Research Report: Q4 CY2025 Update

Aviation and fleet aftermarket services provider VSE Corporation (NASDAQ:VSEC) announced better-than-expected revenue in Q4 CY2025, but sales were flat year on year at $301.2 million. Its non-GAAP profit of $1.16 per share was 29.9% above analysts’ consensus estimates.

VSE Corporation (VSEC) Q4 CY2025 Highlights:

- Revenue: $301.2 million vs analyst estimates of $289.2 million (flat year on year, 4.2% beat)

- Adjusted EPS: $1.16 vs analyst estimates of $0.89 (29.9% beat)

- Adjusted EBITDA: $51.77 million vs analyst estimates of $47.1 million (17.2% margin, 9.9% beat)

- Operating Margin: 10.8%, up from 9.2% in the same quarter last year

- Free Cash Flow Margin: 10.3%, down from 17.4% in the same quarter last year

- Market Capitalization: $6.27 billion

Company Overview

With roots dating back to 1959 and a strategic focus on extending the life of transportation assets, VSE Corporation (NASDAQ:VSEC) provides aftermarket parts distribution and maintenance, repair, and overhaul services for aircraft and vehicle fleets in commercial and government markets.

VSE operates through two primary business segments: Aviation and Fleet. The Aviation segment serves as a critical link in the aerospace supply chain, providing aftermarket parts distribution and maintenance, repair, and overhaul (MRO) services for aircraft components and engine accessories. This segment caters to a diverse clientele including commercial airlines, regional carriers, cargo transporters, business and general aviation operators, and fixed-base operators (FBOs). When an aircraft requires maintenance or component replacement, VSE's Aviation segment supplies the necessary parts and provides repair services to minimize aircraft downtime.

The Fleet segment, operating under the Wheeler Fleet Solutions brand, specializes in parts distribution, engineering solutions, and supply chain management for medium and heavy-duty vehicle fleets. For instance, when a commercial trucking company needs to maintain its fleet of delivery vehicles, VSE can provide the necessary parts and inventory management services to keep those trucks operational. This segment primarily serves government agencies and commercial fleet operators who rely on VSE to extend the service life of their vehicles.

VSE's business model revolves around creating value by sustaining and extending the life of transportation assets. The company maintains global distribution centers strategically positioned to ensure expedient delivery of parts, while its repair facilities are designed to minimize turnaround time for serviced components. This infrastructure allows VSE to help customers maximize the operational availability of their aircraft and vehicle fleets.

Revenue is generated through parts sales, distribution services, supply chain management, and MRO services. The company's customer base spans from commercial airlines and corporate aircraft owners to government agencies and commercial truck fleets. VSE's operations are subject to extensive regulation, including oversight from agencies such as the Federal Aviation Administration (FAA).

Until recently, VSE also operated a Federal and Defense segment providing services to the Department of Defense, but announced plans to divest this business in 2023, completing the sale of substantially all these assets in early 2024 to focus on its core Aviation and Fleet segments.

4. Maintenance and Repair Distributors

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Maintenance and repair distributors that boast reliable selection and quickly deliver products to customers can benefit from this theme. While e-commerce hasn’t disrupted industrial distribution as much as consumer retail, it is still a real threat, forcing investment in omnichannel capabilities to serve customers everywhere. Additionally, maintenance and repair distributors are at the whim of economic cycles that impact the capital spending and construction projects that can juice demand.

VSE Corporation competes with several aftermarket parts and MRO service providers including AAR Corp (NYSE: AIR), Heico Corporation (NYSE: HEI), and TransDigm Group (NYSE: TDG) in the aviation segment, while its Fleet segment faces competition from companies like Genuine Parts Company (NYSE: GPC) and LKQ Corporation (NASDAQ: LKQ).

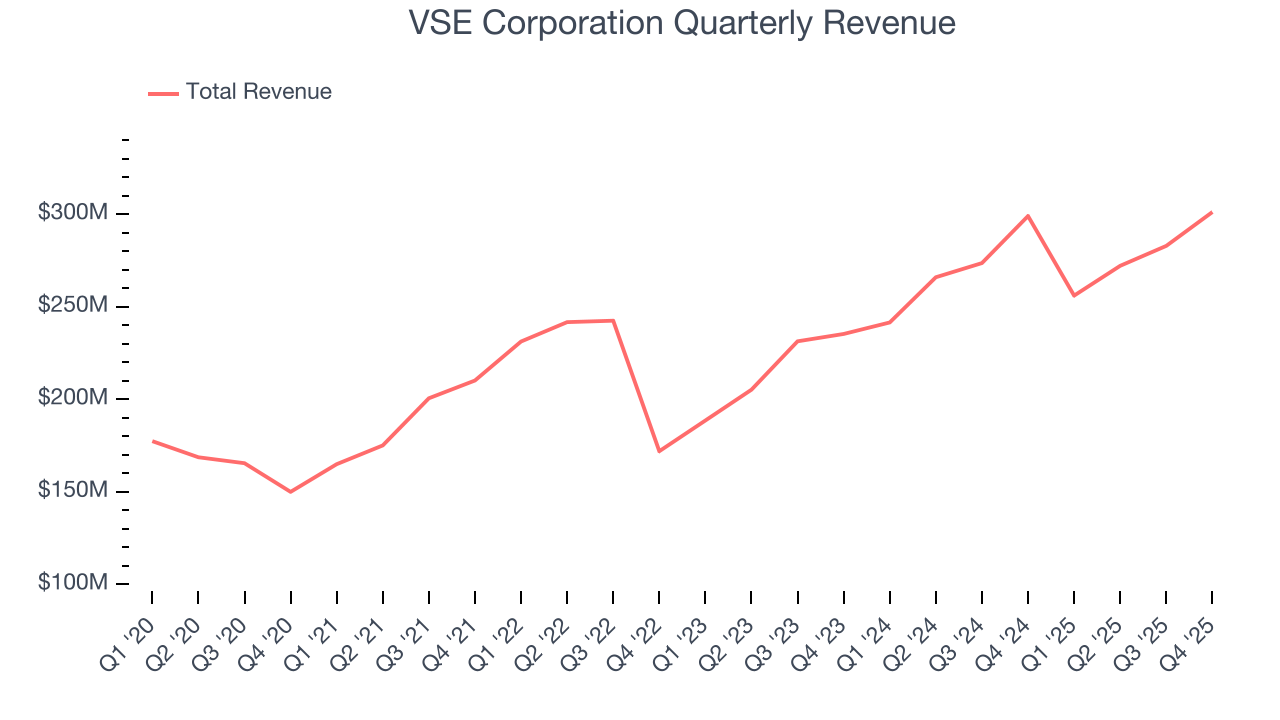

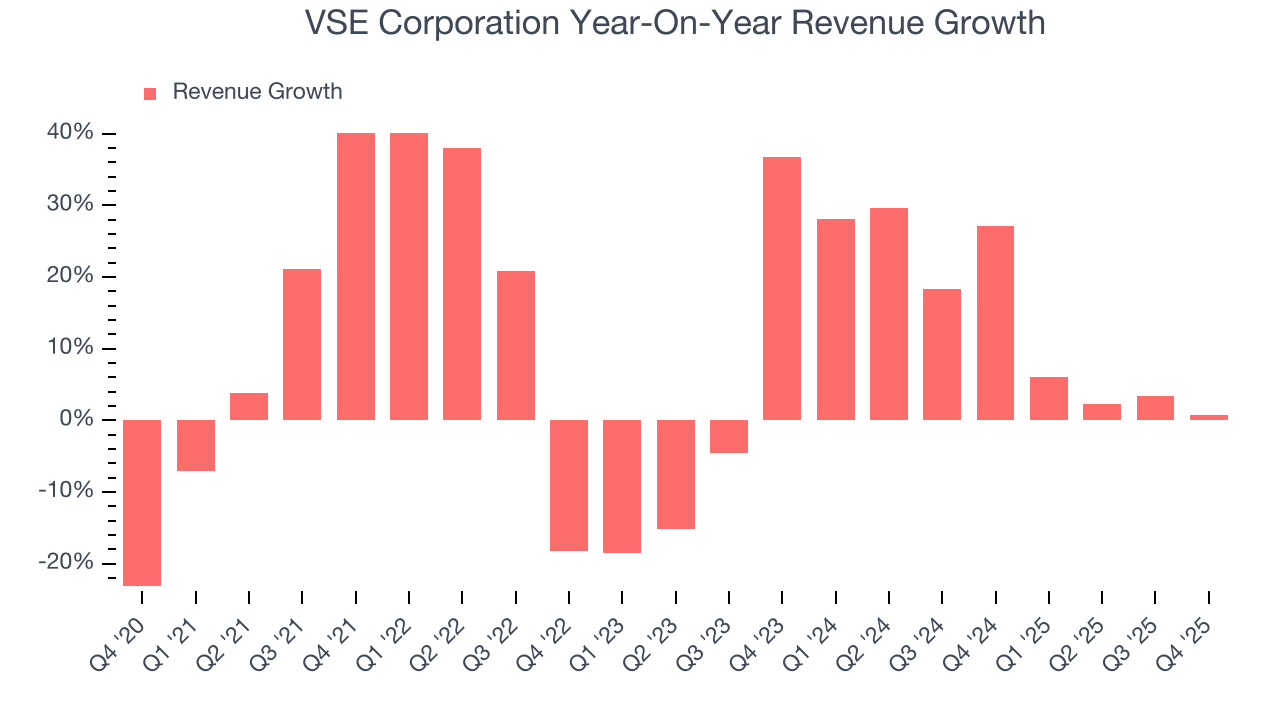

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, VSE Corporation’s 10.9% annualized revenue growth over the last five years was impressive. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. VSE Corporation’s annualized revenue growth of 13.7% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, VSE Corporation’s $301.2 million of revenue was flat year on year but beat Wall Street’s estimates by 4.2%.

Looking ahead, sell-side analysts expect revenue to grow 29.7% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and implies its newer products and services will spur better top-line performance.

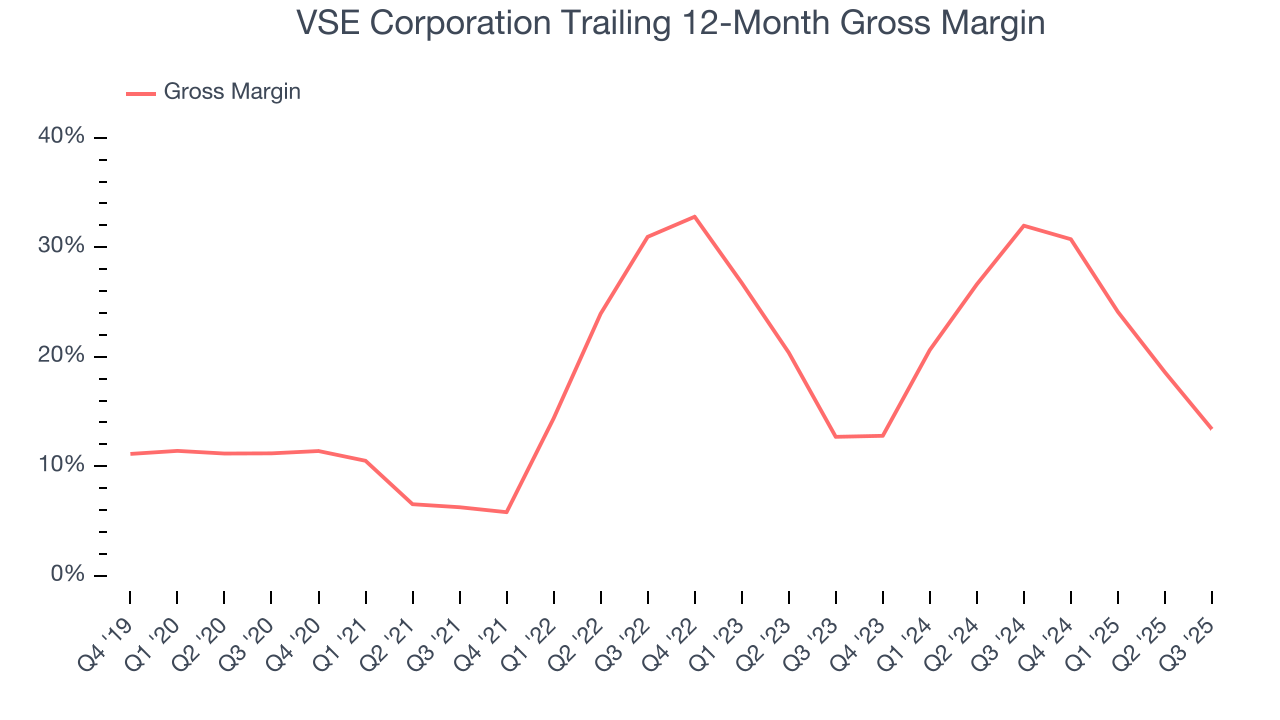

6. Gross Margin & Pricing Power

VSE Corporation has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 20.2% gross margin over the last five years. Said differently, VSE Corporation had to pay a chunky $79.78 to its suppliers for every $100 in revenue.

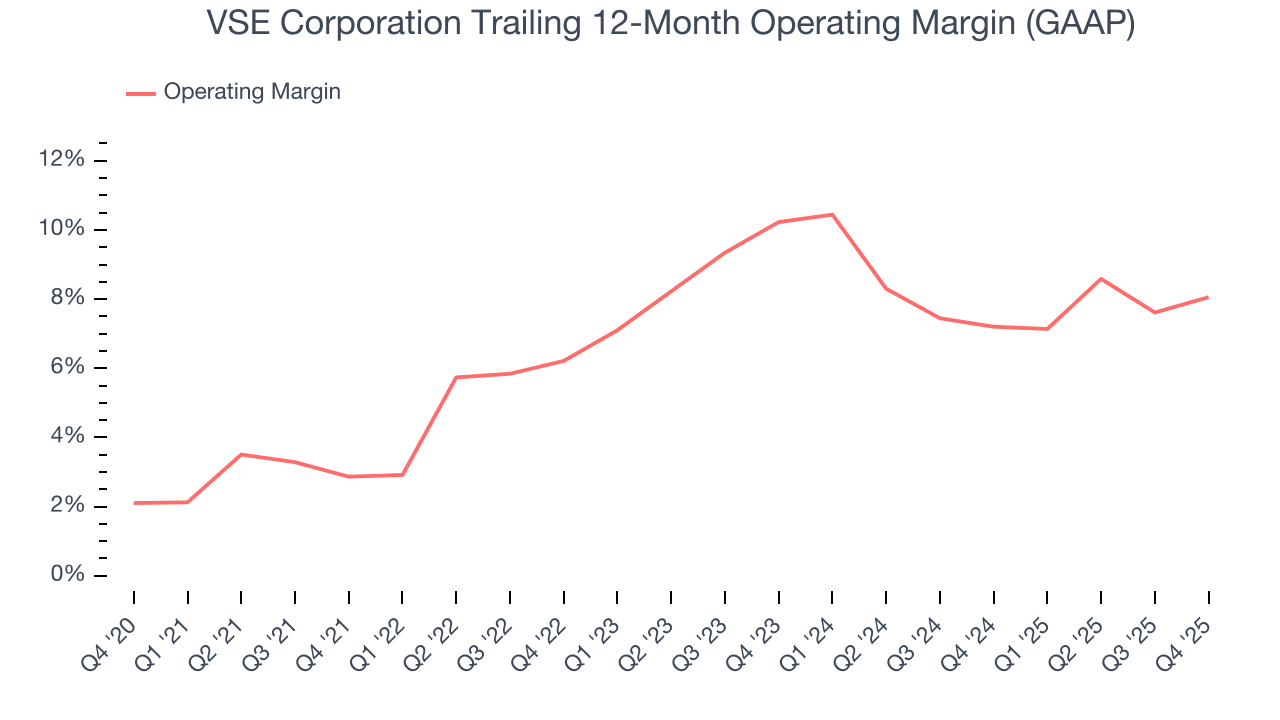

7. Operating Margin

VSE Corporation was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.1% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, VSE Corporation’s operating margin rose by 5.2 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, VSE Corporation generated an operating margin profit margin of 10.8%, up 1.6 percentage points year on year. The increase was a welcome development and shows its expenses recently grew slower than its revenue, leading to higher efficiency.

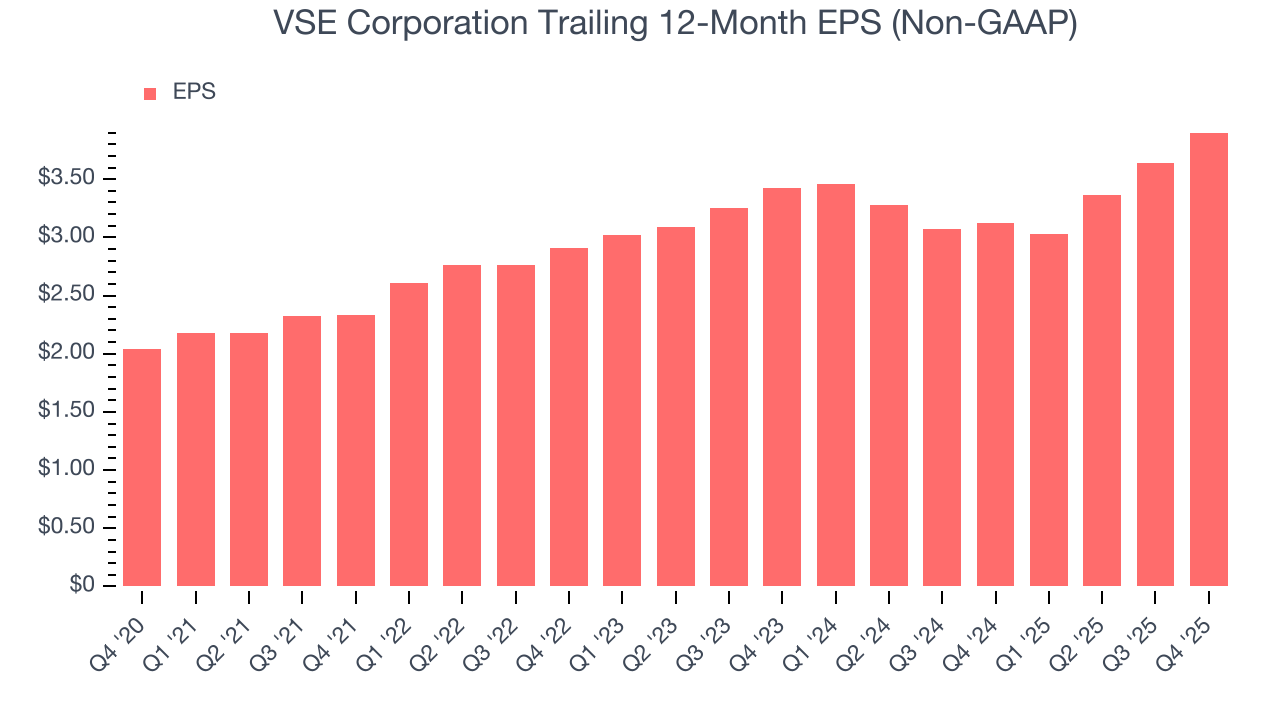

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

VSE Corporation’s EPS grew at a remarkable 13.8% compounded annual growth rate over the last five years, higher than its 10.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of VSE Corporation’s earnings can give us a better understanding of its performance. As we mentioned earlier, VSE Corporation’s operating margin expanded by 5.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For VSE Corporation, its two-year annual EPS growth of 6.8% was lower than its five-year trend. This wasn’t great, but at least the company was successful in other measures of financial health.

In Q4, VSE Corporation reported adjusted EPS of $1.16, up from $0.90 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects VSE Corporation’s full-year EPS of $3.90 to grow 10.9%.

9. Cash Is King

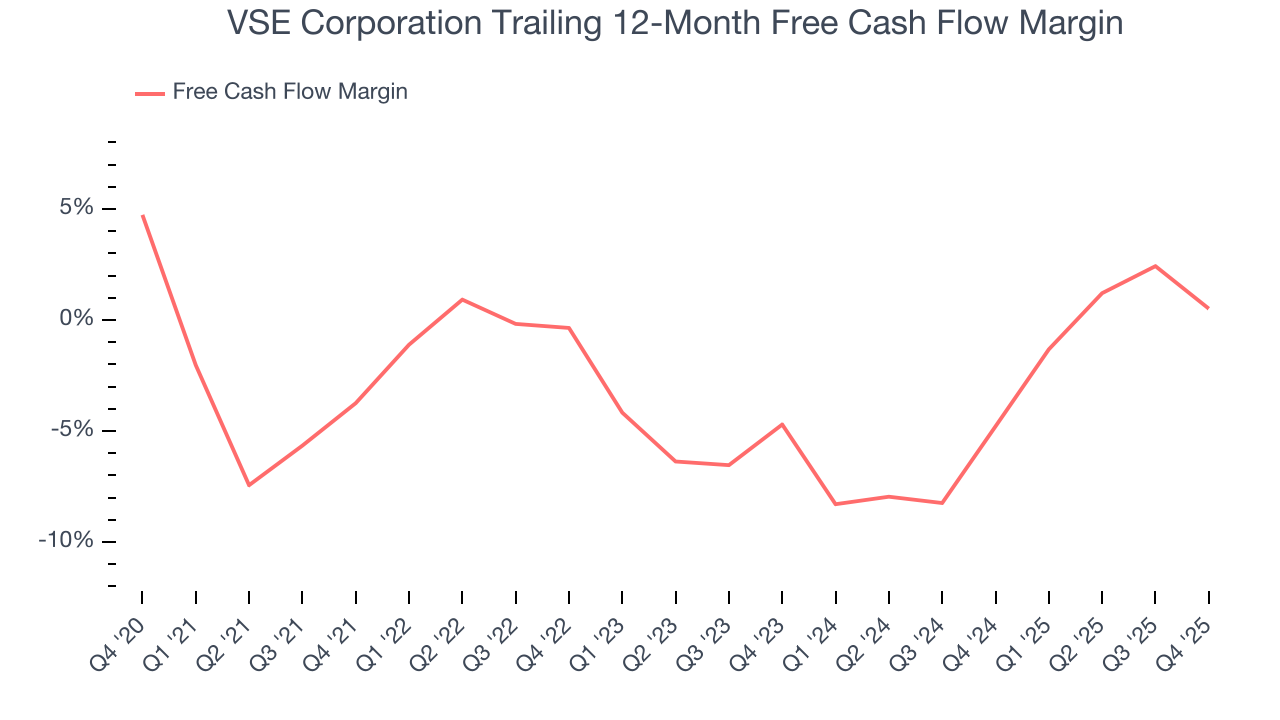

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While VSE Corporation posted positive free cash flow this quarter, the broader story hasn’t been so clean. VSE Corporation’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 2.5%, meaning it lit $2.51 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that VSE Corporation’s margin expanded by 4.3 percentage points during that time. The company’s improvement and free cash flow generation this quarter show it’s heading in the right direction, and continued increases could help it achieve long-term cash profitability.

VSE Corporation’s free cash flow clocked in at $30.87 million in Q4, equivalent to a 10.3% margin. The company’s cash profitability regressed as it was 7.2 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t put too much weight on this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing short-term swings. Long-term trends are more important.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although VSE Corporation has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.5%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, VSE Corporation’s ROIC averaged 1.9 percentage point increases each year. its rising ROIC is a good sign and could suggest its competitive advantage or profitable growth opportunities are expanding.

11. Balance Sheet Assessment

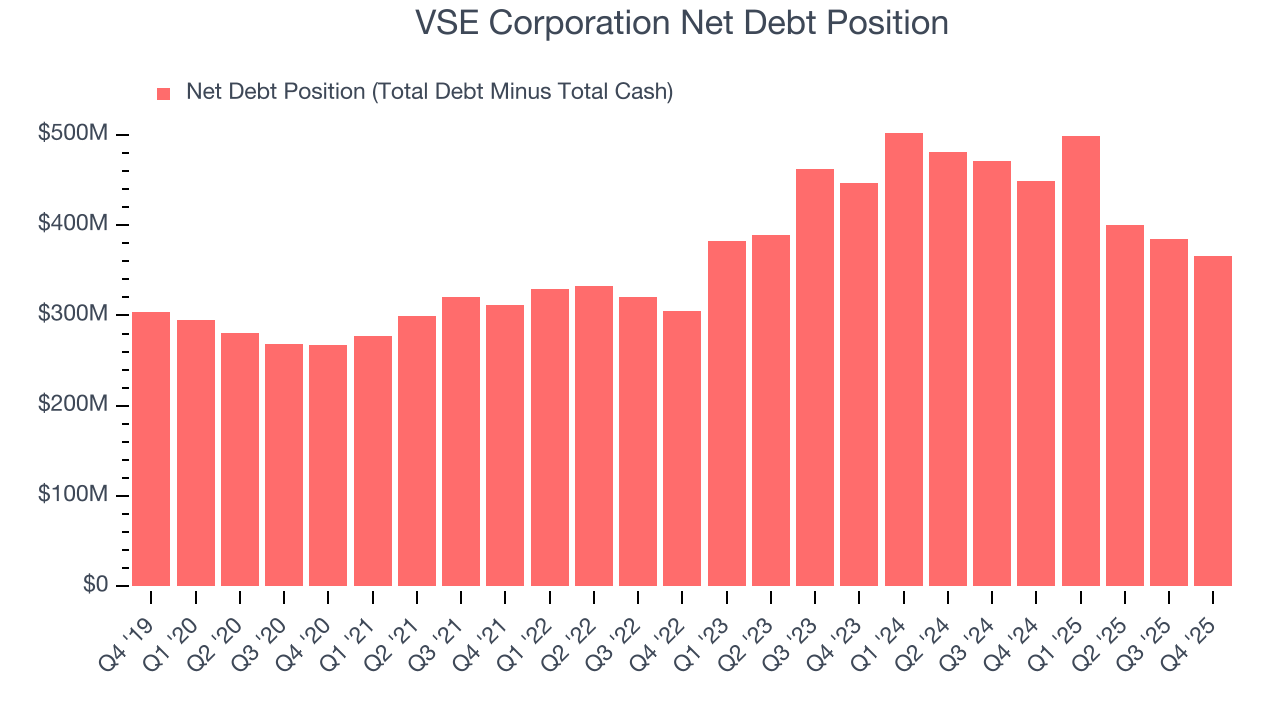

VSE Corporation reported -$69.36 million of cash and $296.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $182.9 million of EBITDA over the last 12 months, we view VSE Corporation’s 2.0× net-debt-to-EBITDA ratio as safe. We also see its $18.72 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from VSE Corporation’s Q4 Results

It was good to see VSE Corporation beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $219.44 immediately after reporting.

13. Is Now The Time To Buy VSE Corporation?

Updated: March 14, 2026 at 11:33 PM EDT

Before making an investment decision, investors should account for VSE Corporation’s business fundamentals and valuation in addition to what happened in the latest quarter.

There are a lot of things to like about VSE Corporation. First off, its revenue growth was impressive over the last five years and is expected to accelerate over the next 12 months. And while its cash burn raises the question of whether it can sustainably maintain growth, its expanding operating margin shows the business has become more efficient. On top of that, its projected EPS for the next year implies the company’s fundamentals will improve.

VSE Corporation’s P/E ratio based on the next 12 months is 44.2x. At this valuation, there’s a lot of good news priced in. VSE Corporation is a good one to add to your watchlist - there are companies featuring superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $262 on the company (compared to the current share price of $208.52).