Viatris (VTRS)

Viatris faces an uphill battle. Its poor sales growth shows demand is soft and its negative returns on capital suggest it destroyed value.― StockStory Analyst Team

1. News

2. Summary

Why We Think Viatris Will Underperform

Created through the 2020 merger of Mylan and Pfizer's Upjohn division, Viatris (NASDAQ:VTRS) is a healthcare company that develops, manufactures, and distributes branded and generic medicines across more than 165 countries worldwide.

- Incremental sales over the last five years were much less profitable as its earnings per share fell by 9.8% annually while its revenue grew

- Push for growth has led to negative returns on capital, signaling value destruction, and its decreasing returns suggest its historical profit centers are aging

- Sales tumbled by 3.7% annually over the last two years, showing market trends are working against its favor during this cycle

Viatris is in the penalty box. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than Viatris

Viatris’s stock price of $13.48 implies a valuation ratio of 5.6x forward P/E. This sure is a cheap multiple, but you get what you pay for.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Viatris (VTRS) Research Report: Q4 CY2025 Update

Medication company Viatris (NASDAQ:VTRS) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 5% year on year to $3.7 billion. The company’s full-year revenue guidance of $14.7 billion at the midpoint came in 2.3% above analysts’ estimates. Its non-GAAP profit of $0.57 per share was 7.4% above analysts’ consensus estimates.

Viatris (VTRS) Q4 CY2025 Highlights:

- Revenue: $3.7 billion vs analyst estimates of $3.52 billion (5% year-on-year growth, 5.3% beat)

- Adjusted EPS: $0.57 vs analyst estimates of $0.53 (7.4% beat)

- Adjusted EBITDA: $1 billion vs analyst estimates of $950 million (27.1% margin, 5.6% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $2.40 at the midpoint, missing analyst estimates by 3.8%

- EBITDA guidance for the upcoming financial year 2026 is $4.3 billion at the midpoint, in line with analyst expectations

- Operating Margin: -5.2%, in line with the same quarter last year

- Free Cash Flow Margin: 16.7%, up from 9.7% in the same quarter last year

- Market Capitalization: $18.52 billion

Company Overview

Created through the 2020 merger of Mylan and Pfizer's Upjohn division, Viatris (NASDAQ:VTRS) is a healthcare company that develops, manufactures, and distributes branded and generic medicines across more than 165 countries worldwide.

Viatris operates at the intersection of traditional pharmaceuticals and healthcare access, with a portfolio of over 1,400 approved molecules spanning major therapeutic areas including cardiovascular, infectious diseases, oncology, and central nervous system disorders. The company's offerings range from well-known branded medications to complex generics and over-the-counter products.

The company serves diverse customers including retail pharmacies, wholesalers, hospitals, and government health programs. When a hospital needs to stock its pharmacy with reliable medications, or when a retail pharmacy chain requires consistent supply of common prescriptions, Viatris provides these essential medicines through its global distribution network.

Viatris generates revenue through multiple channels. In substitution markets like France and Australia, pharmacists can substitute Viatris' products for prescribed brands. In tender markets such as Sweden and Germany, the company competes for government contracts to be the exclusive supplier of certain medications. In distribution markets like the U.S., Viatris sells directly to major wholesalers and pharmacy chains.

The company operates approximately 40 manufacturing facilities worldwide producing various dosage forms from oral tablets to injectables and complex delivery systems. Its global research and development platform focuses on both extending existing product lifecycles and developing new complex generics and biosimilars.

Through its "Global Healthcare Gateway," Viatris partners with other pharmaceutical companies to expand access to their products using Viatris' established regulatory expertise and distribution channels. This allows smaller innovators to reach global markets they couldn't access independently.

The company has structured its operations into four geographic segments: Developed Markets (North America and Europe), Greater China, JANZ (Japan, Australia, and New Zealand), and Emerging Markets covering over 125 developing countries.

4. Generic Pharmaceuticals

The generic pharmaceutical industry operates on a volume-driven, low-cost business model, producing bioequivalent versions of branded drugs once their patents expire. These companies benefit from consistent demand for affordable medications, as they are critical to reducing healthcare costs. Generics typically face lower R&D expenses and shorter regulatory approval timelines compared to branded drug makers, enabling cost efficiencies. However, the industry is highly competitive, with intense pricing pressures, thin margins, and frequent legal challenges from branded pharmaceutical companies over patent disputes. Looking ahead, the industry is supported by tailwinds such as the role of AI in streamlining drug development (reverse engineering complex formulations) and manufacturing efficiency (optimize processes and remove inefficiencies). Governments and insurers' focus on reducing drug costs can also boost generics' adoption. However, headwinds include escalating pricing pressure from large buyers like pharmacy chains and healthcare distributors as well as evolving regulatory hurdles.

Viatris competes with major pharmaceutical companies including Teva Pharmaceutical Industries (NYSE:TEVA), Novartis' Sandoz division (NYSE:NVS), Pfizer (NYSE:PFE), and Sun Pharmaceutical Industries (NSE:SUNPHARMA) in the global generic and branded generic medication markets.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $14.3 billion in revenue over the past 12 months, Viatris has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

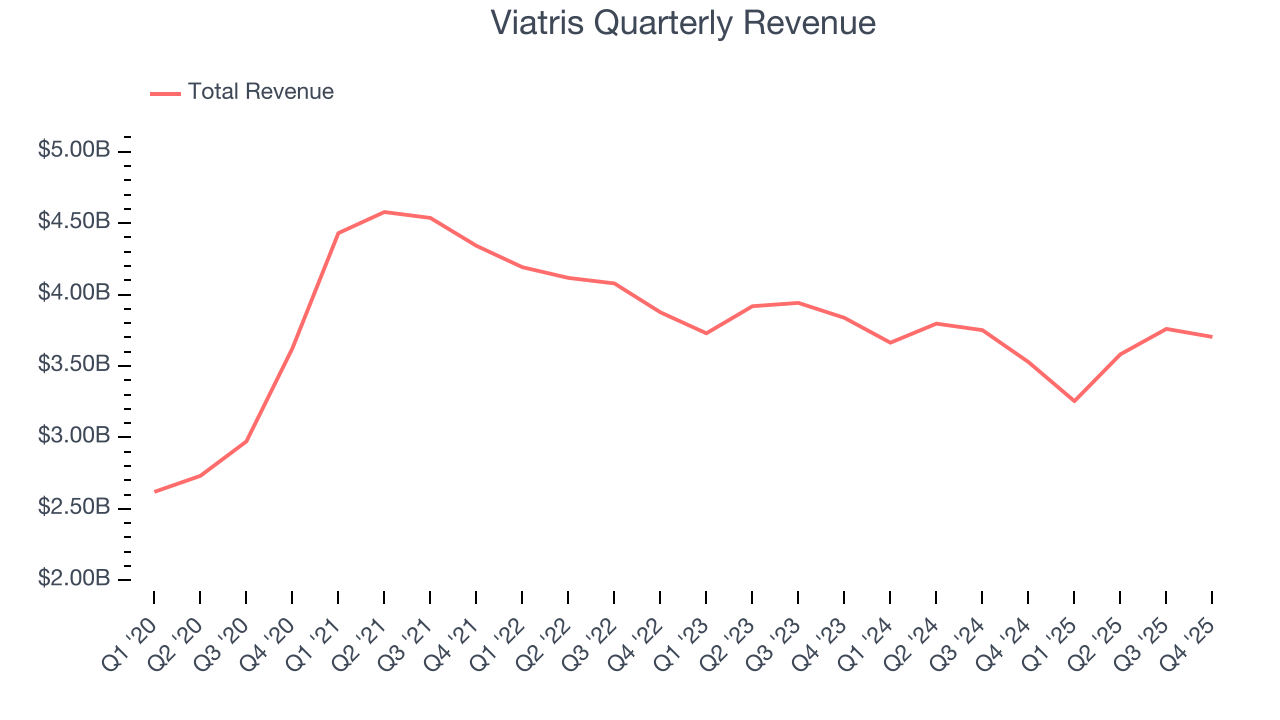

6. Revenue Growth

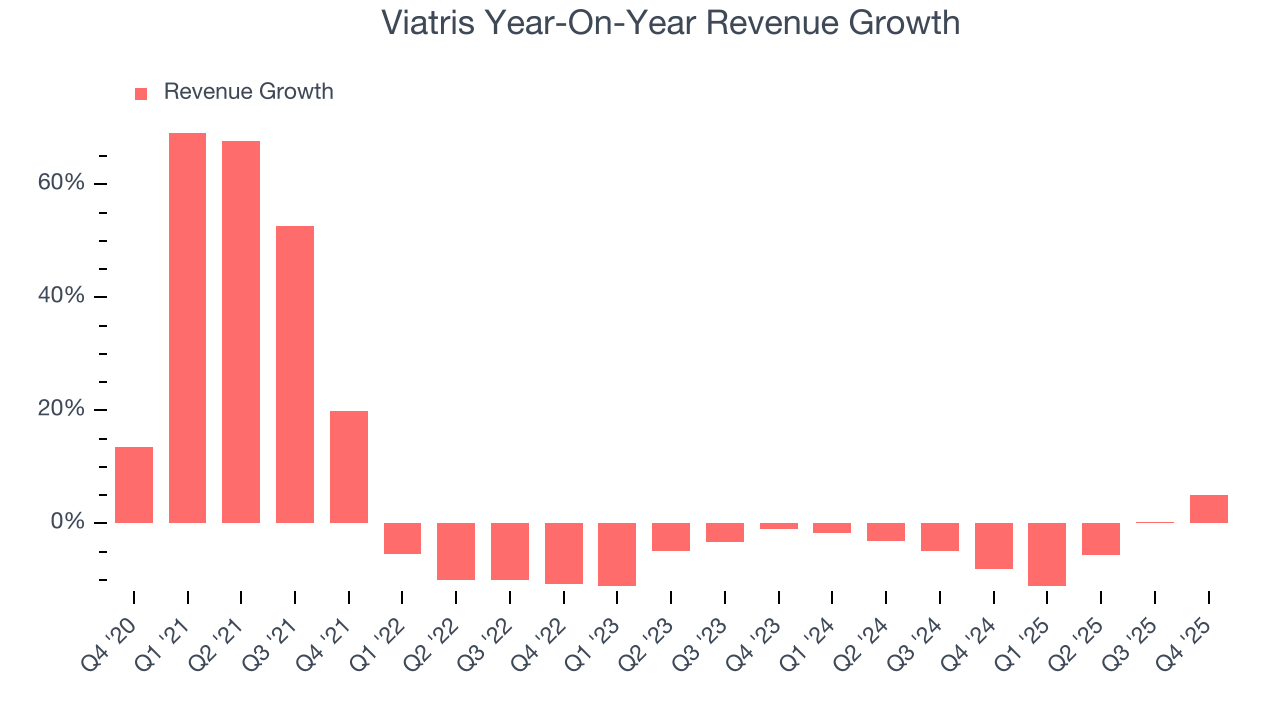

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Viatris’s 3.7% annualized revenue growth over the last five years was tepid. This was below our standard for the healthcare sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Viatris’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 3.7% annually.

This quarter, Viatris reported modest year-on-year revenue growth of 5% but beat Wall Street’s estimates by 5.3%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

7. Operating Margin

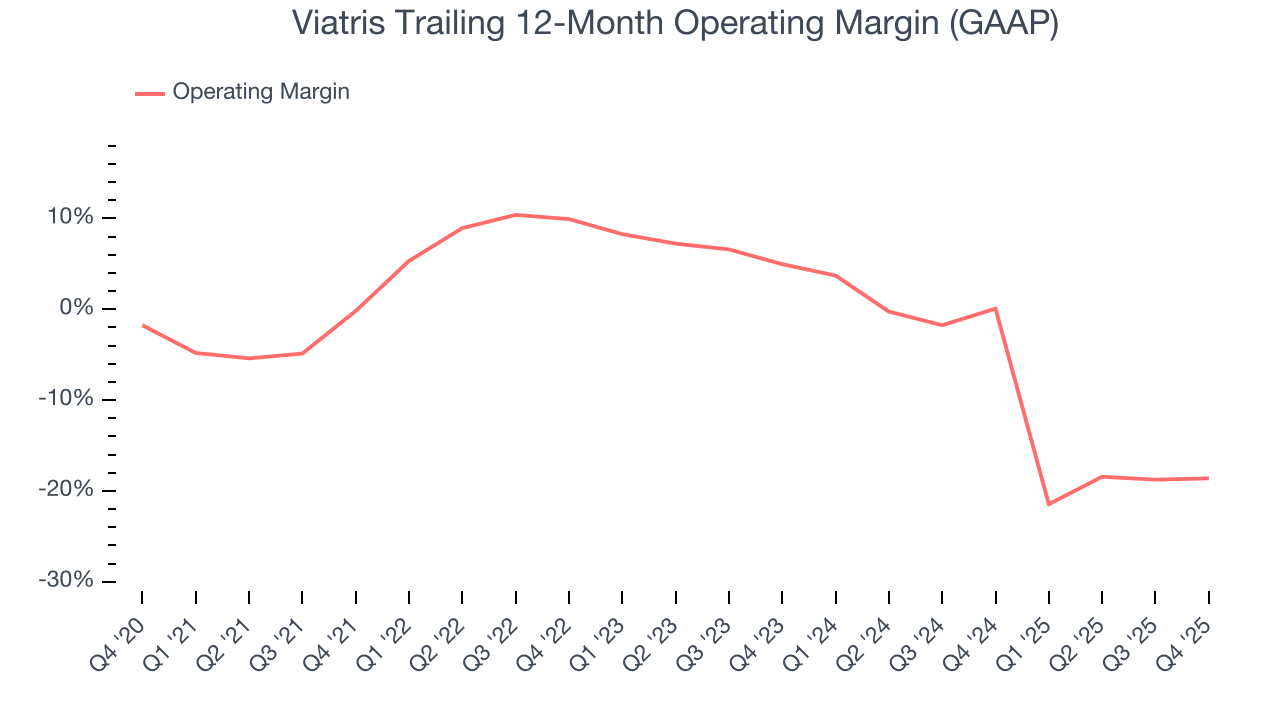

Viatris was roughly breakeven when averaging the last five years of quarterly operating profits, lousy for a healthcare business.

Looking at the trend in its profitability, Viatris’s operating margin decreased by 18.4 percentage points over the last five years. This performance was caused by more recent speed bumps as the company’s margin fell by 23.6 percentage points on a two-year basis. We’re disappointed in these results because it shows its expenses were rising and it couldn’t pass those costs onto its customers.

Viatris’s operating margin was negative 5.2% this quarter. The company's consistent lack of profits raise a flag.

8. Earnings Per Share

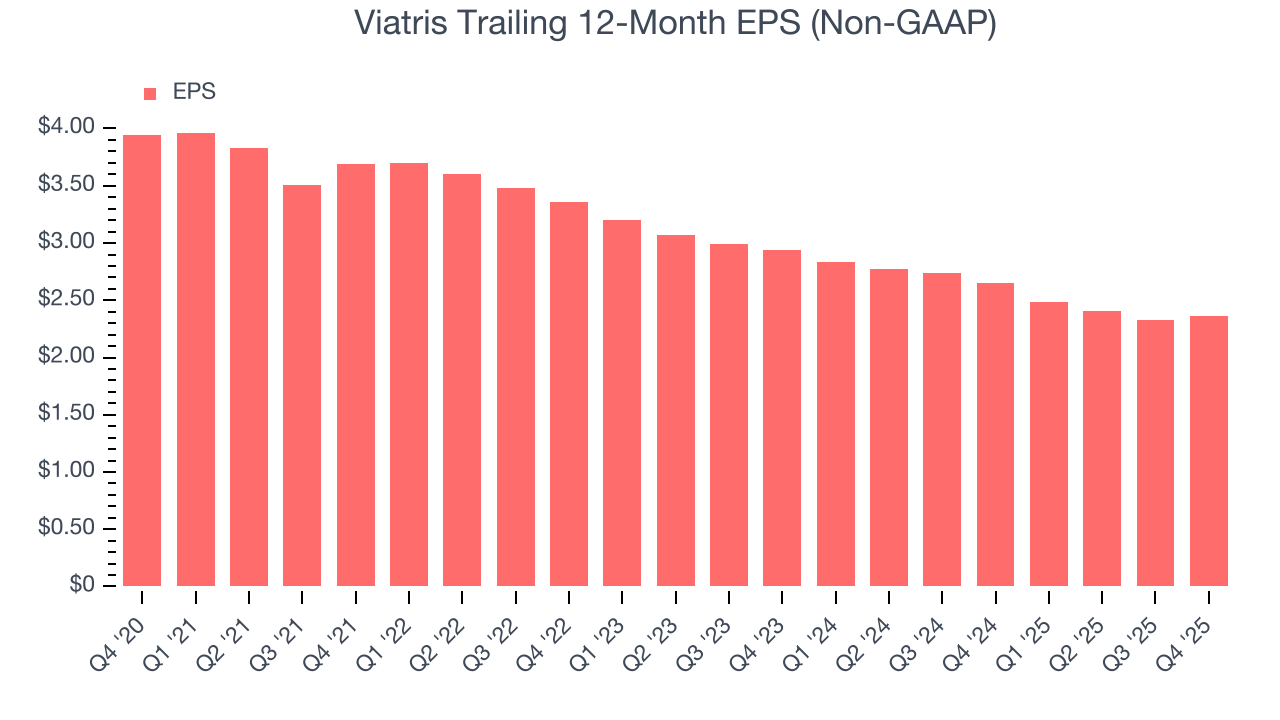

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Viatris, its EPS declined by 9.8% annually over the last five years while its revenue grew by 3.7%. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

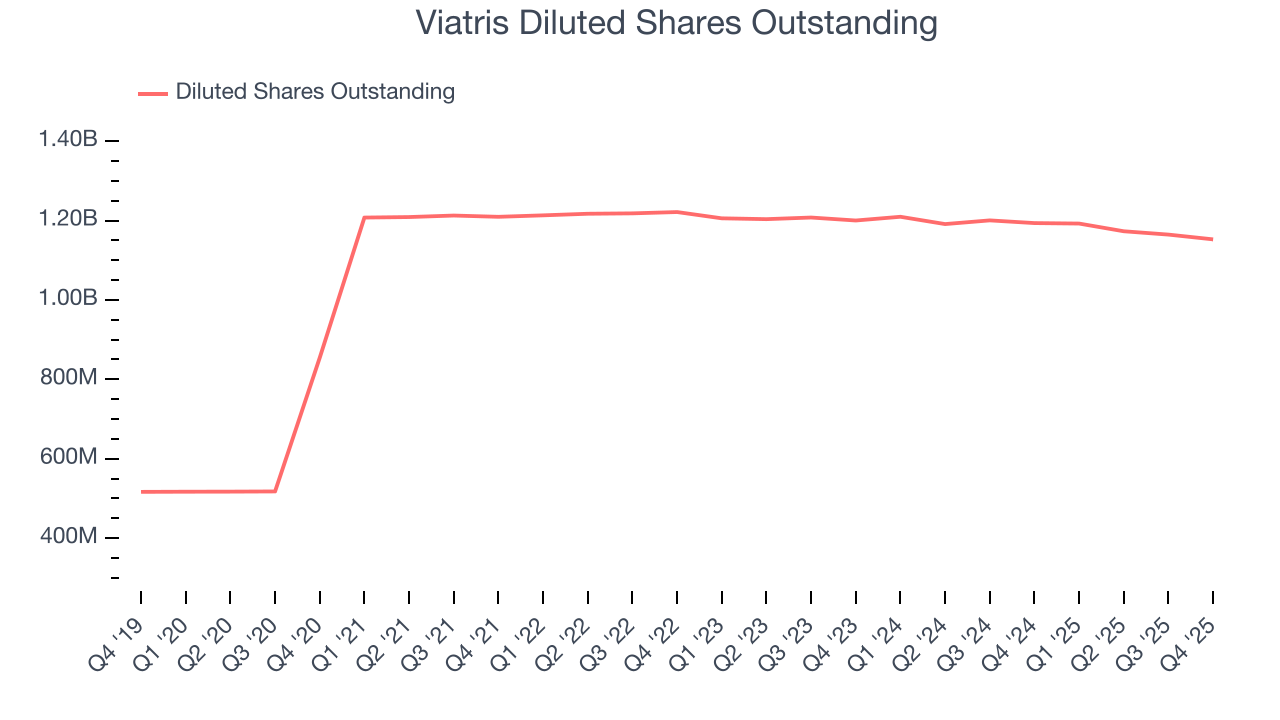

Diving into the nuances of Viatris’s earnings can give us a better understanding of its performance. As we mentioned earlier, Viatris’s operating margin was flat this quarter but declined by 18.4 percentage points over the last five years. Its share count also grew by 34.9%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, Viatris reported adjusted EPS of $0.57, up from $0.54 in the same quarter last year. This print beat analysts’ estimates by 7.4%. Over the next 12 months, Wall Street expects Viatris’s full-year EPS of $2.36 to grow 5.4%.

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

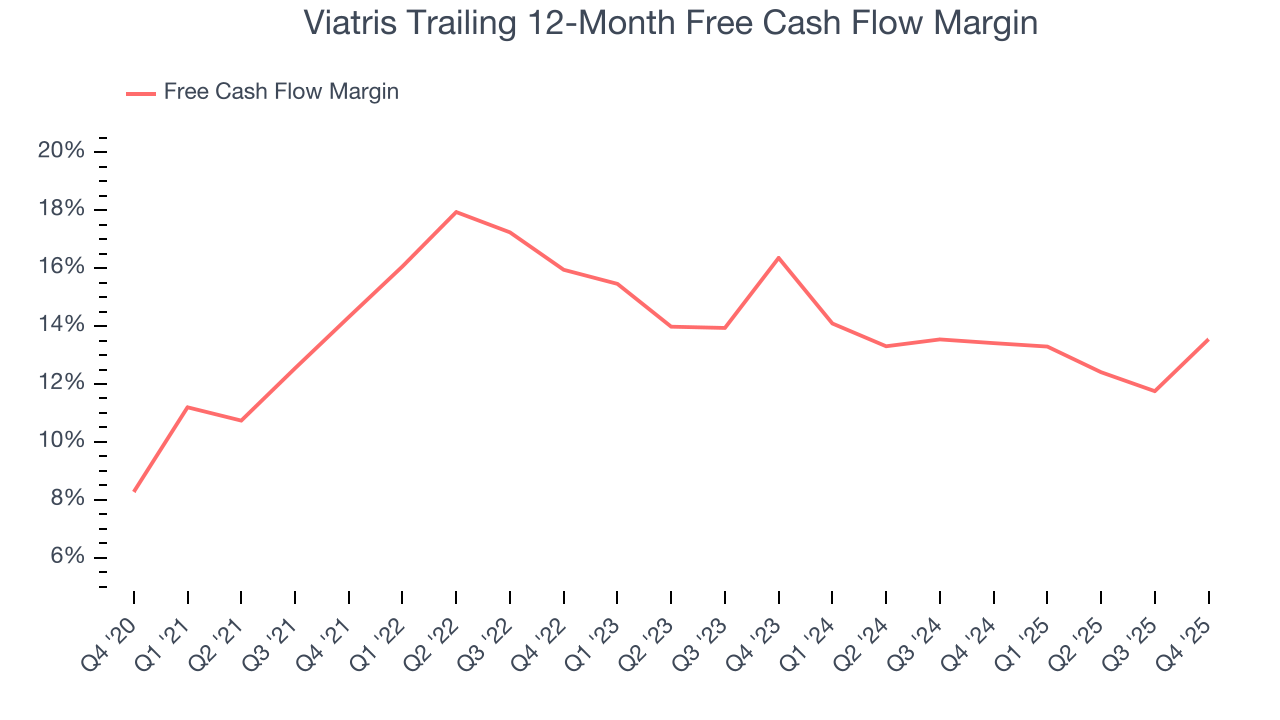

Viatris has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 14.7% over the last five years, better than the broader healthcare sector. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Viatris’s free cash flow clocked in at $619.3 million in Q4, equivalent to a 16.7% margin. This result was good as its margin was 7 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends trump fluctuations.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

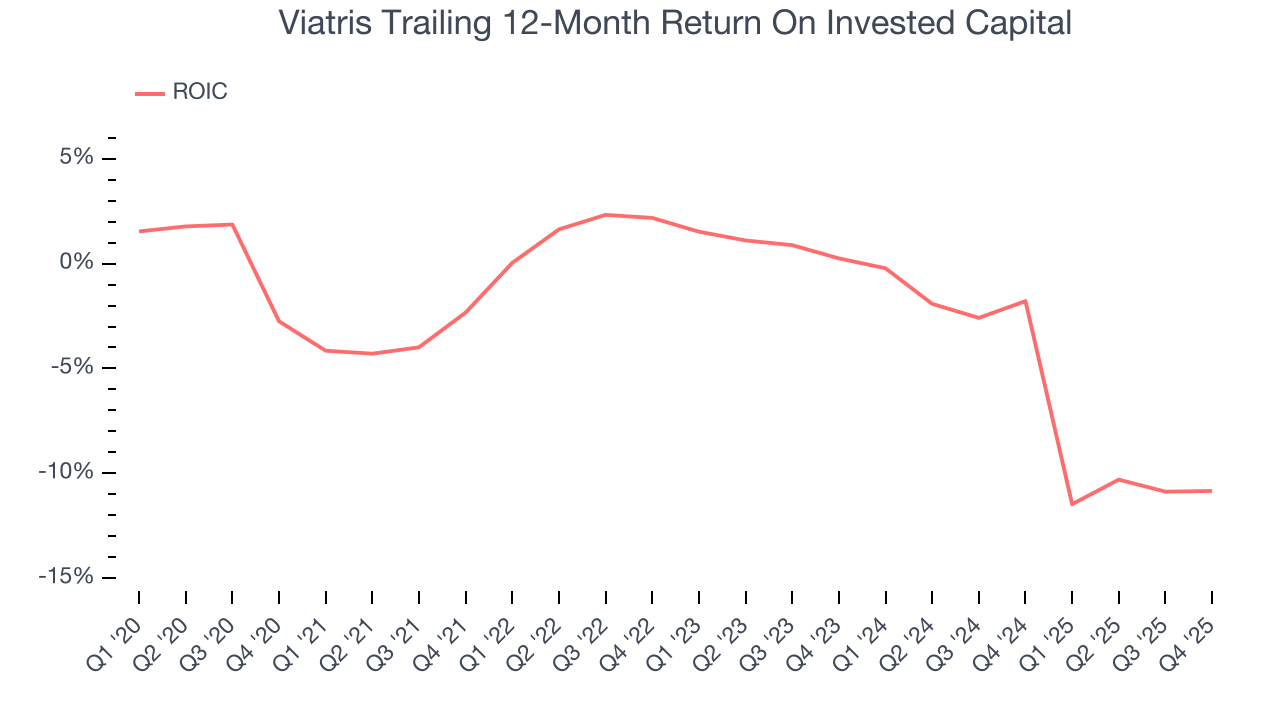

Viatris’s five-year average ROIC was negative 2.5%, meaning management lost money while trying to expand the business. Its returns were among the worst in the healthcare sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Viatris’s ROIC has decreased over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Assessment

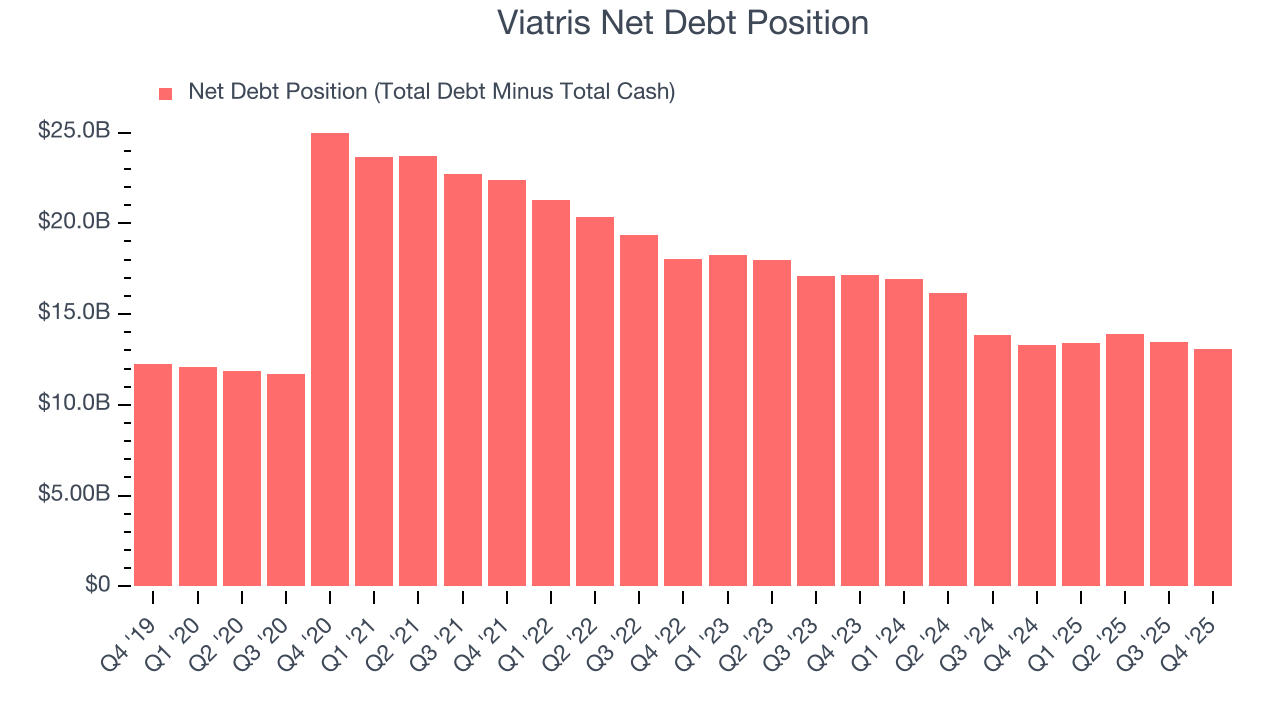

Viatris reported $1.32 billion of cash and $14.41 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $4.16 billion of EBITDA over the last 12 months, we view Viatris’s 3.1× net-debt-to-EBITDA ratio as safe. We also see its $232.1 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Viatris’s Q4 Results

We were impressed by how significantly Viatris blew past analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance exceeded Wall Street’s estimates. On the other hand, its full-year EPS guidance missed. Overall, this print was mixed. The stock remained flat at $15.93 immediately following the results.

13. Is Now The Time To Buy Viatris?

Updated: March 16, 2026 at 12:32 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Viatris.

We see the value of companies making people healthier, but in the case of Viatris, we’re out. To begin with, its revenue growth was uninspiring over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its impressive operating margins show it has a highly efficient business model, the downside is its declining EPS over the last five years makes it a less attractive asset to the public markets. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Viatris’s P/E ratio based on the next 12 months is 5.6x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $15.50 on the company (compared to the current share price of $13.48).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.