Zscaler (ZS)

Zscaler is a compelling stock. Its financials show it’s a customer acquisition machine that can expand both quickly and organically.― StockStory Analyst Team

1. News

2. Summary

Why We Like Zscaler

Pioneering the "zero trust" approach that has fundamentally changed enterprise network security, Zscaler (NASDAQ:ZS) provides a cloud-based security platform that connects users, devices, and applications securely without traditional network-based security hardware.

- Annual revenue growth of 41.1% over the last five years was superb and indicates its market share is rising

- Impressive free cash flow profitability enables the company to fund new investments or reward investors with share buybacks/dividends

- Estimated revenue growth of 20.8% for the next 12 months implies its momentum over the last two years will continue

We expect great things from Zscaler. The valuation seems fair when considering its quality, so this might be a prudent time to buy some shares.

Why Is Now The Time To Buy Zscaler?

Zscaler’s stock price of $155.60 implies a valuation ratio of 6.9x forward price-to-sales. This valuation is fair - even cheap depending on how much you like the story - for the quality you get.

By definition, where you buy a stock impacts returns. Compared to entry price, business quality matters much more for long-term market outperformance. Buying in at a great price helps, nevertheless.

3. Zscaler (ZS) Research Report: Q4 CY2025 Update

Cloud security platform Zscaler (NASDAQ:ZS) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 25.9% year on year to $815.8 million. The company expects next quarter’s revenue to be around $835 million, close to analysts’ estimates. Its non-GAAP profit of $1.01 per share was 12.6% above analysts’ consensus estimates.

Zscaler (ZS) Q4 CY2025 Highlights:

- Revenue: $815.8 million vs analyst estimates of $798.8 million (25.9% year-on-year growth, 2.1% beat)

- Billings: $819.8 million vs analyst estimates of $892.8 million (10.4% year-on-year growth, 8.2% miss)

- Adjusted EPS: $1.01 vs analyst estimates of $0.90 (12.6% beat)

- Adjusted Operating Income: $181 million vs analyst estimates of $174.6 million (22.2% margin, 3.7% beat)

- The company slightly lifted its revenue guidance for the full year to $3.32 billion at the midpoint from $3.29 billion

- Management raised its full-year Adjusted EPS guidance to $4.01 at the midpoint, a 5.4% increase

- Operating Margin: -6.3%, in line with the same quarter last year

- Free Cash Flow Margin: 20.7%, down from 52.4% in the previous quarter

- Market Capitalization: $24.83 billion

Company Overview

Pioneering the "zero trust" approach that has fundamentally changed enterprise network security, Zscaler (NASDAQ:ZS) provides a cloud-based security platform that connects users, devices, and applications securely without traditional network-based security hardware.

The company's Zero Trust Exchange platform processes over 500 billion transactions daily through more than 160 data centers across 185 countries. This distributed cloud architecture eliminates the need for businesses to route traffic through central data centers for security scanning, instead functioning as an intelligent "switchboard" that uses business policies to securely connect users and applications regardless of location.

Zscaler offers three core products: Zscaler for Users enables secure access to internet and internal applications; Zscaler for Workloads secures cloud-based applications and data; and Zscaler for IoT/OT protects connected devices in industrial environments. These solutions incorporate capabilities like advanced threat protection, data loss prevention, cloud sandbox testing, and zero trust network access that would traditionally require multiple separate security appliances.

A typical enterprise might use Zscaler to allow employees to securely access cloud applications like Microsoft 365 or Salesforce from any location without compromising security, while simultaneously protecting sensitive corporate data. This enables companies to phase out expensive MPLS networks and VPN infrastructure while improving security posture. The platform also helps organizations migrate applications to public cloud environments by securing workload communications and identifying misconfigurations or vulnerabilities.

Zscaler operates on a subscription model, with pricing based on the number of users, applications, and specific services deployed. The company focuses primarily on larger enterprises, with approximately 35% of the Forbes Global 2000 among its customer base spanning industries like financial services, healthcare, manufacturing, and government.

4. Network Security

Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks. The migration of businesses to the cloud and employees working remotely in insecure environments is increasing demand modern cloud-based network security software, which offers better performance at lower cost than maintaining the traditional on-premise solutions, such as expensive specialized firewall hardware.

Zscaler competes with traditional network security vendors like Palo Alto Networks (NASDAQ:PANW), Cisco Systems (NASDAQ:CSCO), and Fortinet (NASDAQ:FTNT), as well as cloud security specialists such as Cloudflare (NYSE:NET) and CrowdStrike (NASDAQ:CRWD). Microsoft (NASDAQ:MSFT) also offers competing capabilities through its Defender platform.

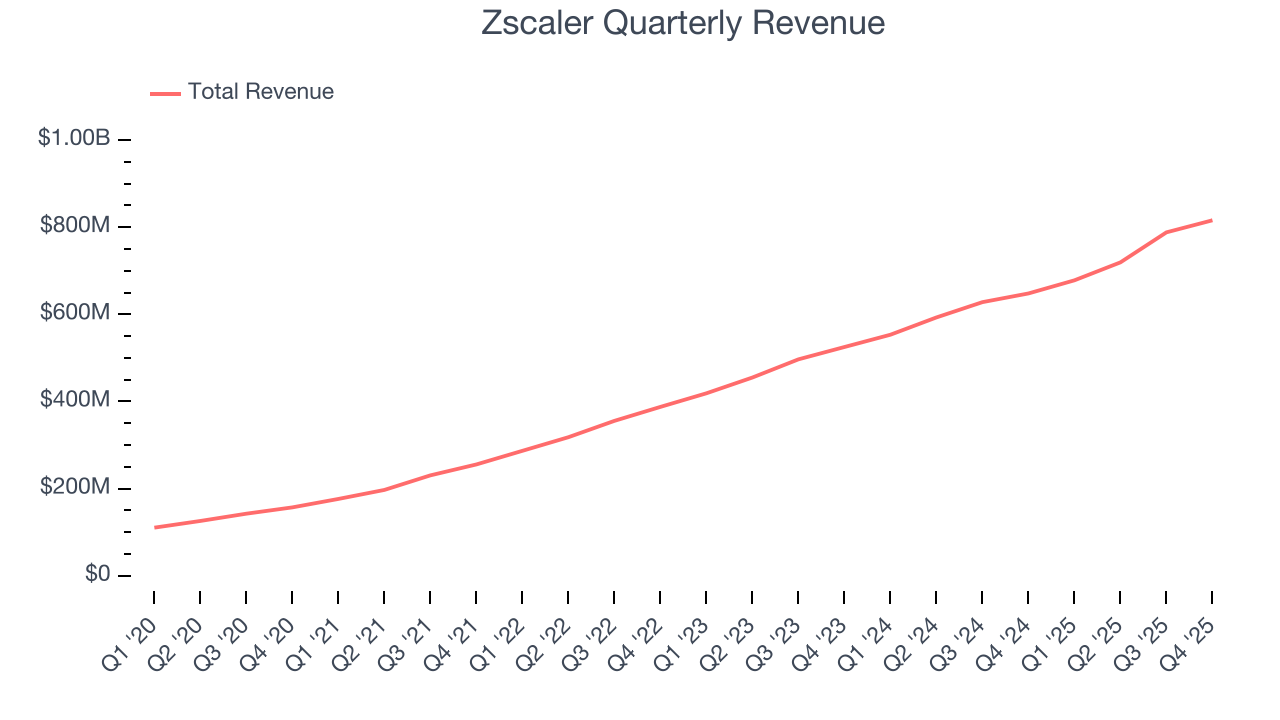

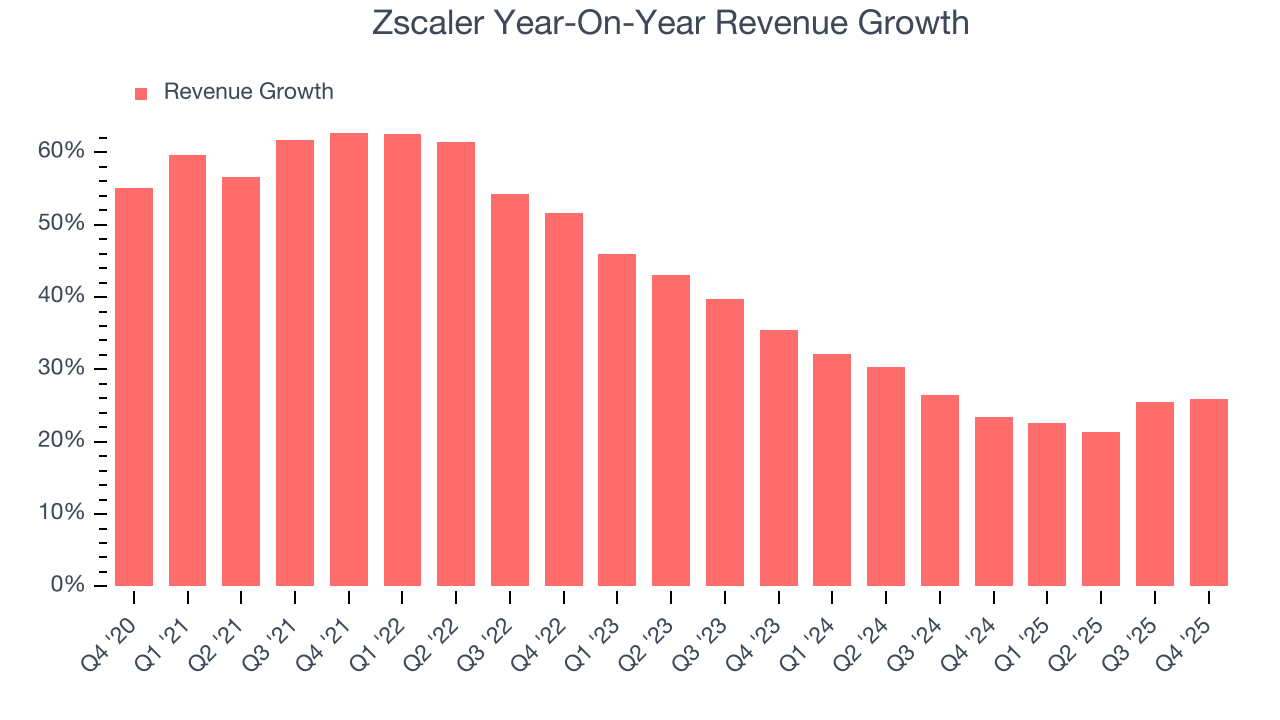

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Zscaler’s 41.1% annualized revenue growth over the last five years was incredible. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Zscaler’s annualized revenue growth of 25.8% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Zscaler reported robust year-on-year revenue growth of 25.9%, and its $815.8 million of revenue topped Wall Street estimates by 2.1%. Company management is currently guiding for a 23.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 20.2% over the next 12 months, a deceleration versus the last two years. Still, this projection is noteworthy and implies the market is forecasting success for its products and services.

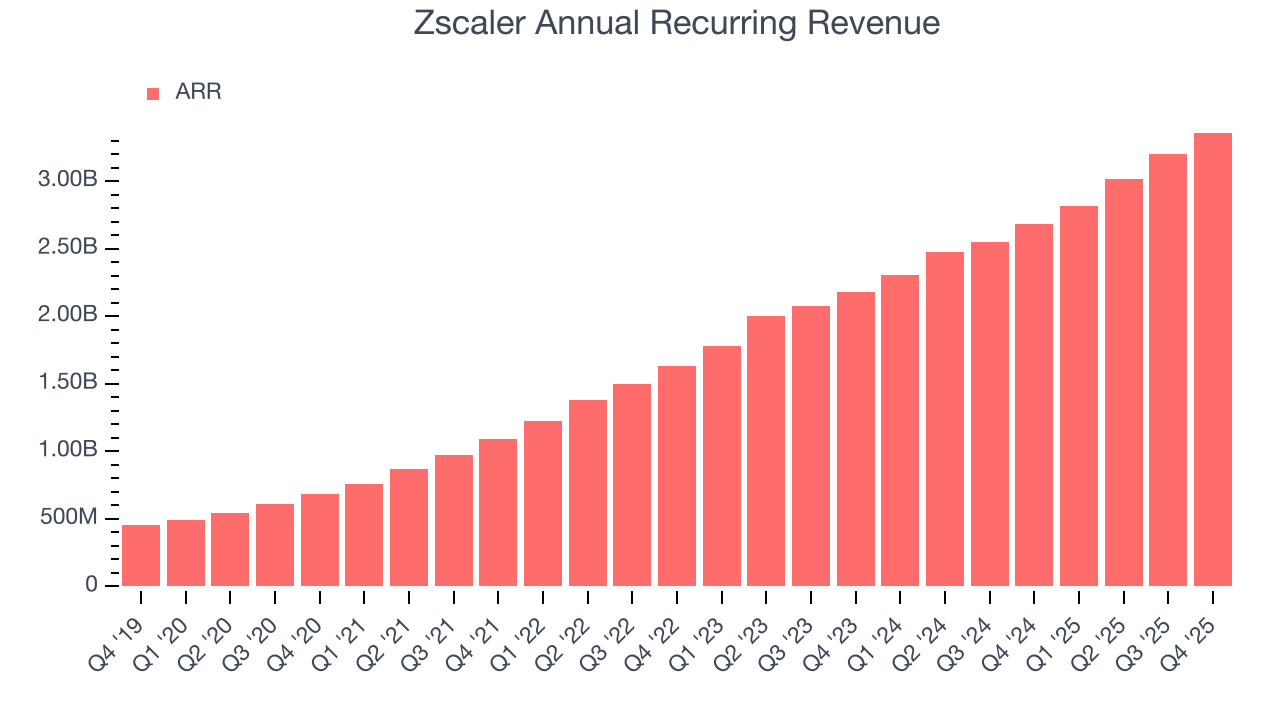

6. Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Zscaler’s ARR punched in at $3.36 billion in Q4, and over the last four quarters, its growth was fantastic as it averaged 23.7% year-on-year increases. This performance aligned with its total sales growth and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes Zscaler a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

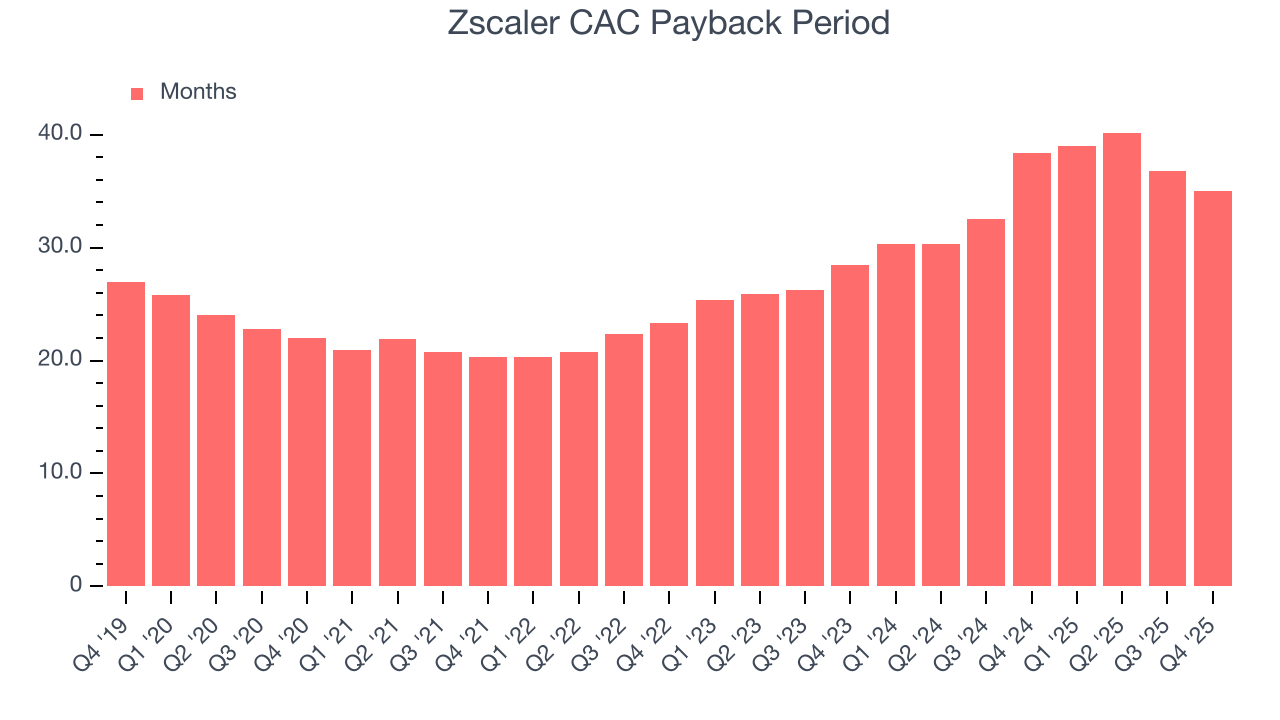

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Zscaler is quite efficient at acquiring new customers, and its CAC payback period checked in at 35 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a strong brand reputation, giving it more resources pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

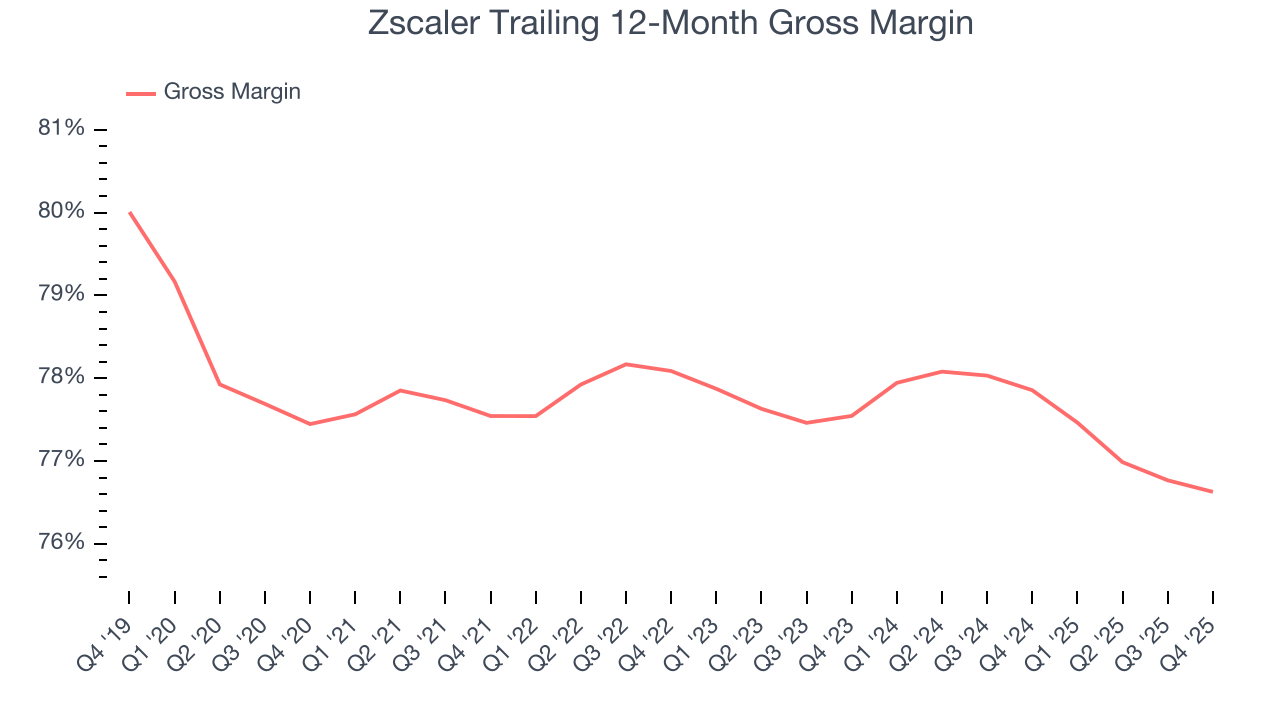

8. Gross Margin & Pricing Power

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Zscaler’s gross margin is good for a software business and points to its solid unit economics, competitive products and services, and lack of meaningful pricing pressure. As you can see below, it averaged an impressive 76.6% gross margin over the last year. That means for every $100 in revenue, roughly $76.63 was left to spend on selling, marketing, and R&D.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Zscaler has seen gross margins decline by 0.9 percentage points over the last 2 year, which is poor compared to software peers.

In Q4, Zscaler produced a 76.6% gross profit margin, in line with the same quarter last year. Zooming out, Zscaler’s full-year margin has been trending down over the past 12 months, decreasing by 1.2 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs.

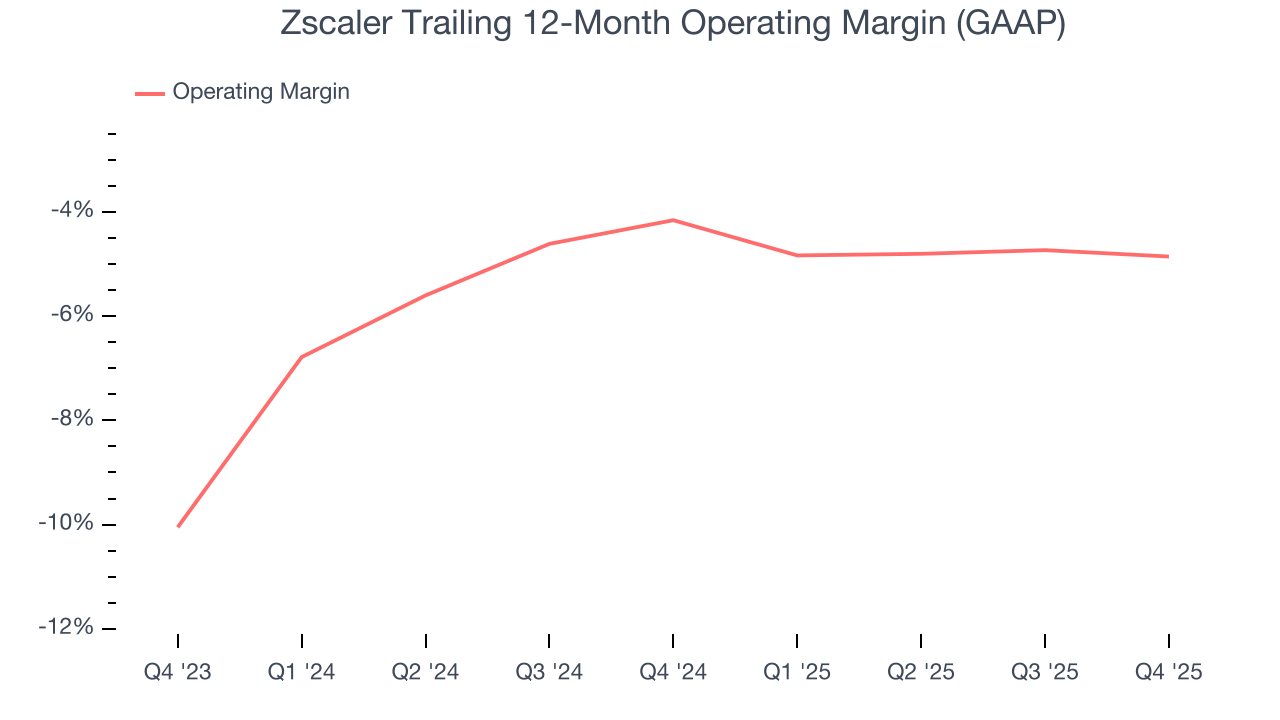

9. Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Zscaler’s expensive cost structure has contributed to an average operating margin of negative 4.9% over the last year. This happened because the company spent loads of money to capture market share. As seen in its fast revenue growth, the aggressive strategy has paid off so far, and Wall Street’s estimates suggest the party will continue. We tend to agree and believe the business has a good chance of reaching profitability upon scale.

Looking at the trend in its profitability, Zscaler’s operating margin might fluctuated slightly but has generally stayed the same over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Zscaler generated a negative 6.3% operating margin.

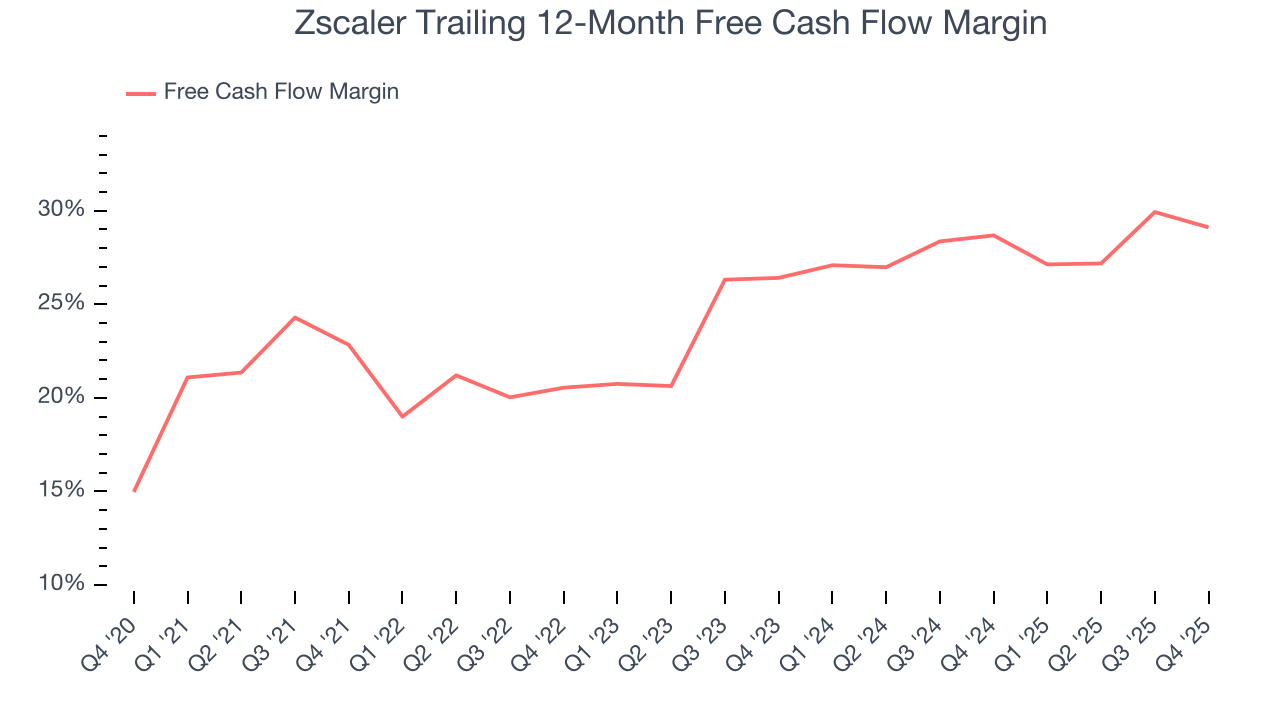

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Zscaler has shown robust cash profitability, driven by its attractive business model and cost-effective customer acquisition strategy that enable it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 29.1% over the last year, quite impressive for a software business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Zscaler’s free cash flow clocked in at $169.1 million in Q4, equivalent to a 20.7% margin. The company’s cash profitability regressed as it was 1.4 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

Over the next year, analysts predict Zscaler’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 29.1% for the last 12 months will decrease to 27.2%.

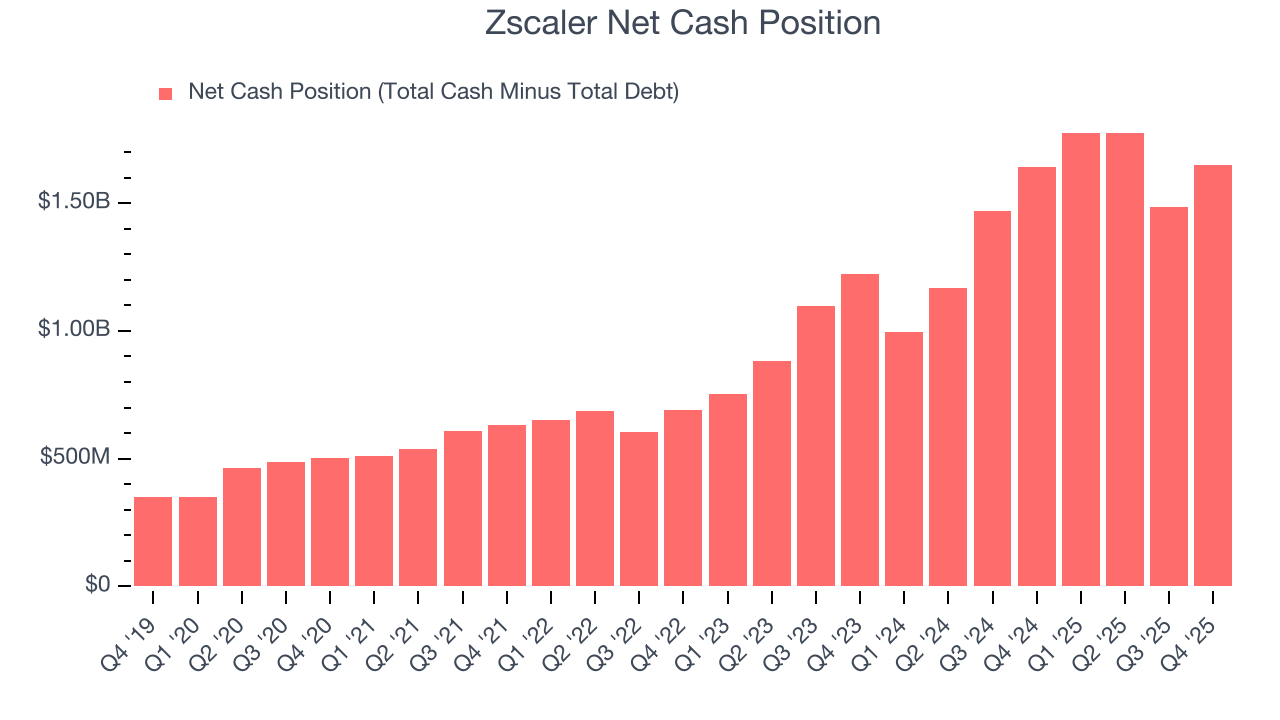

11. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Zscaler is a well-capitalized company with $3.51 billion of cash and $1.86 billion of debt on its balance sheet. This $1.65 billion net cash position is 7% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Zscaler’s Q4 Results

We were impressed by Zscaler’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its full-year EPS guidance trumped Wall Street’s estimates. On the other hand, all-important billings (sometimes referred to as cash revenue) missed fairly significantly. This is weighing on shares, and the stock traded down 7.4% to $155.00 immediately after reporting.

13. Is Now The Time To Buy Zscaler?

Updated: March 18, 2026 at 10:15 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Zscaler.

There are several reasons why we think Zscaler is a great business. For starters, its revenue growth was exceptional over the last five years. And while its operating margin hasn't moved over the last year, its surging ARR shows its fundamentals and revenue predictability are improving. On top of that, Zscaler’s bountiful generation of free cash flow empowers it to invest in growth initiatives.

Zscaler’s price-to-sales ratio based on the next 12 months is 6.9x. Looking across the spectrum of software companies today, Zscaler’s fundamentals shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $234.79 on the company (compared to the current share price of $155.60), implying they see 50.9% upside in buying Zscaler in the short term.