SentinelOne (S)

SentinelOne is a compelling stock. Its ARR growth highlights the stickiness of its business model and suggests it’s winning market share.― StockStory Analyst Team

1. News

2. Summary

Why We Like SentinelOne

Built on the principle of "fighting machine with machine," SentinelOne (NYSE:S) provides an AI-powered cybersecurity platform that autonomously prevents, detects, and responds to threats across endpoints, cloud workloads, and identity systems.

- Impressive 60.8% annual revenue growth over the last five years indicates it’s winning market share

- ARR growth averaged 23.2% over the last year, showing customers are willing to take multi-year bets on its software

- Projected revenue growth of 20% for the next 12 months suggests its momentum from the last two years will persist

SentinelOne is a top-tier company. The valuation looks fair when considering its quality, so this might be a prudent time to buy some shares.

Why Is Now The Time To Buy SentinelOne?

SentinelOne is trading at $14.30 per share, or 3.8x forward price-to-sales. This multiple is cheap, and we think the stock is a bargain considering its quality characteristics.

A powerful double-play is a business that can both grow earnings and achieve a loftier multiple over time. Elite companies trading at meaningful discounts are good ways to set up this play.

3. SentinelOne (S) Research Report: Q4 CY2025 Update

Cybersecurity AI platform provider SentinelOne (NYSE:S) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 20.2% year on year to $271.2 million. The company expects next quarter’s revenue to be around $277 million, close to analysts’ estimates. Its non-GAAP profit of $0.07 per share was 19.1% above analysts’ consensus estimates.

SentinelOne (S) Q4 CY2025 Highlights:

- Revenue: $271.2 million vs analyst estimates of $271.1 million (20.2% year-on-year growth, in line)

- Adjusted EPS: $0.07 vs analyst estimates of $0.06 (19.1% beat)

- Adjusted Operating Income: $15.5 million vs analyst estimates of $13.64 million (5.7% margin, 13.7% beat)

- Revenue Guidance for Q1 CY2026 is $277 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2027 is $0.35 at the midpoint, beating analyst estimates by 17.5%

- Operating Margin: -29.5%, up from -35.6% in the same quarter last year

- Free Cash Flow was -$2.31 million, down from $15.9 million in the previous quarter

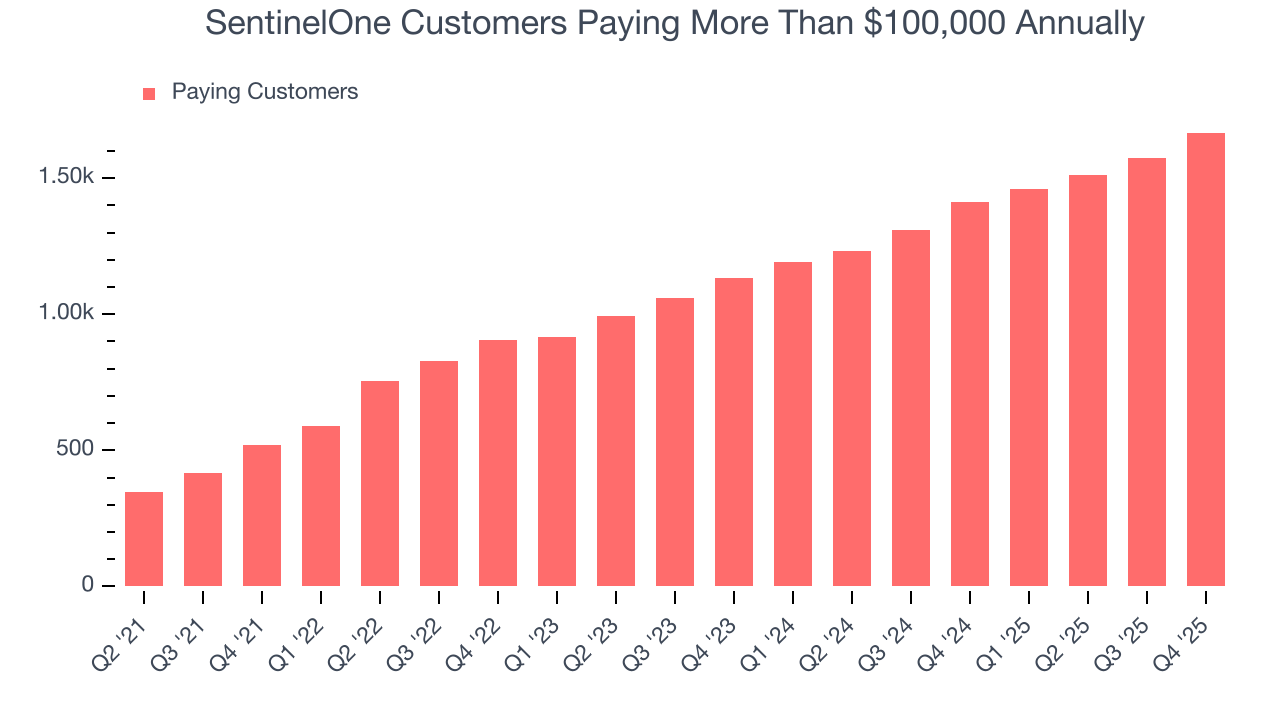

- Customers: 1,667 customers paying more than $100,000 annually

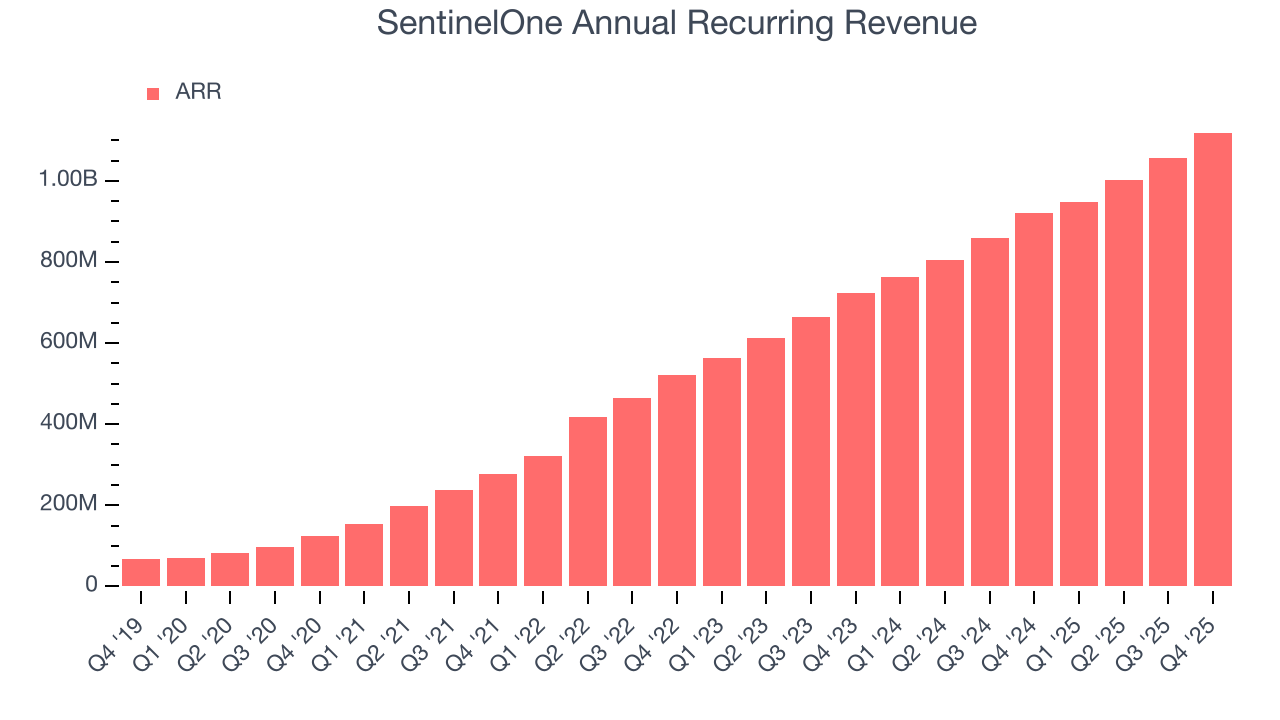

- Annual Recurring Revenue: $1.12 billion vs analyst estimates of $1.12 billion (21.6% year-on-year growth, in line)

- Market Capitalization: $4.81 billion

Company Overview

Built on the principle of "fighting machine with machine," SentinelOne (NYSE:S) provides an AI-powered cybersecurity platform that autonomously prevents, detects, and responds to threats across endpoints, cloud workloads, and identity systems.

SentinelOne's Singularity Platform represents a significant shift from traditional, human-dependent cybersecurity approaches to an AI-driven autonomous defense system. At its core, the platform employs three types of artificial intelligence: Static AI that identifies malicious files in milliseconds, Behavioral AI that monitors process activities for threats, and Streaming AI that correlates data across multiple sources to detect anomalies.

The platform creates detailed contextual narratives called "Storylines" for every protected device, enabling security teams to quickly investigate incidents across their digital environment. These Storylines track all events and behaviors occurring on endpoints, cloud workloads, and identity systems, providing analysts with the ability to trace attack progression and automatically remediate compromised systems.

SentinelOne generates revenue through subscription-based pricing tiers for its platform, with options ranging from basic endpoint protection (Singularity Core) to comprehensive enterprise security solutions (Singularity Enterprise). The company's customers span organizations of all sizes across approximately 80 countries, from small businesses to large global enterprises and government entities.

Beyond its core platform, SentinelOne offers additional services including Vigilance Managed Detection and Response (MDR), which provides 24/7 monitoring by the company's security analysts, and WatchTower, which delivers threat intelligence and proactive hunting capabilities. The company has built an extensive partner ecosystem that includes managed security service providers, incident response firms, and technology alliances, allowing SentinelOne to extend its reach and capabilities through integration with other security and IT systems.

4. Endpoint Security

Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks. As the volume of internet enabled devices grows, every device that employees use to connect to business networks represents a potential risk. Endpoint security software enables businesses to protect devices (endpoints) that employees use for work purposes either on a network or in the cloud from cyber threats.

SentinelOne competes with endpoint security providers like CrowdStrike Holdings, Inc. and VMware Carbon Black, legacy antivirus companies including Trellix (formerly McAfee), Symantec (owned by Broadcom), and Microsoft, as well as broader network security providers such as Palo Alto Networks who offer comprehensive security portfolios.

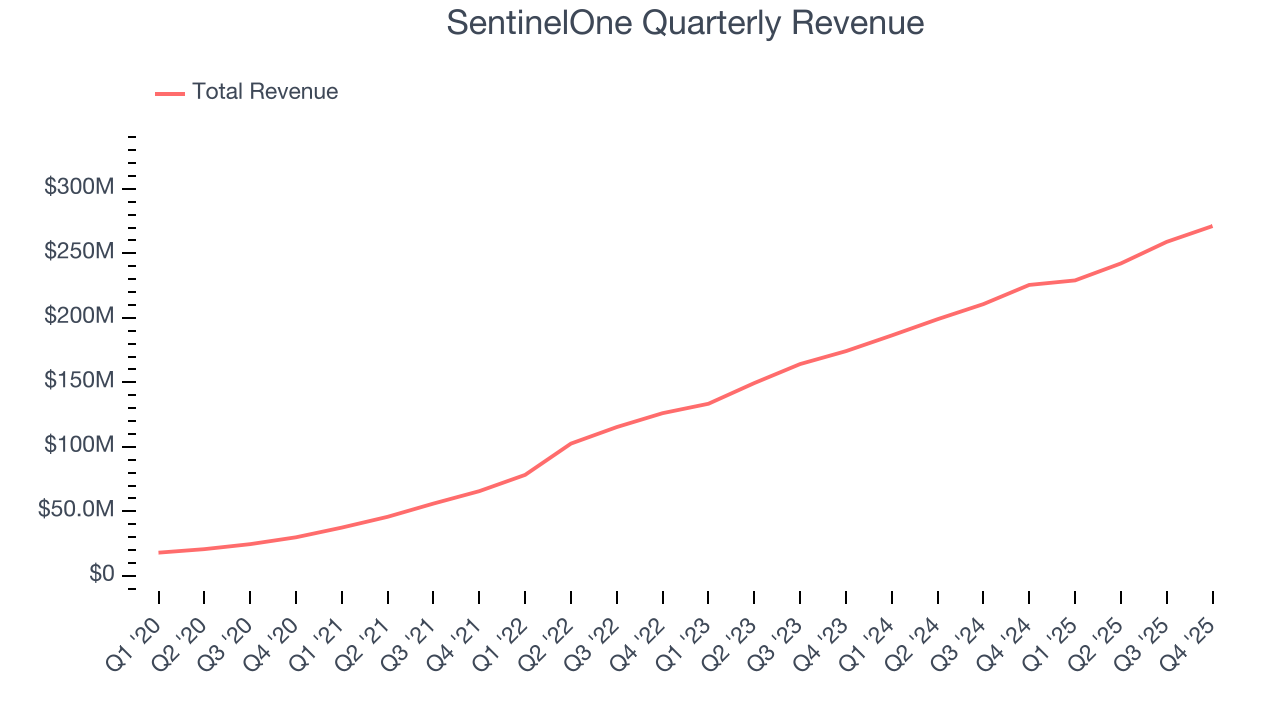

5. Revenue Growth

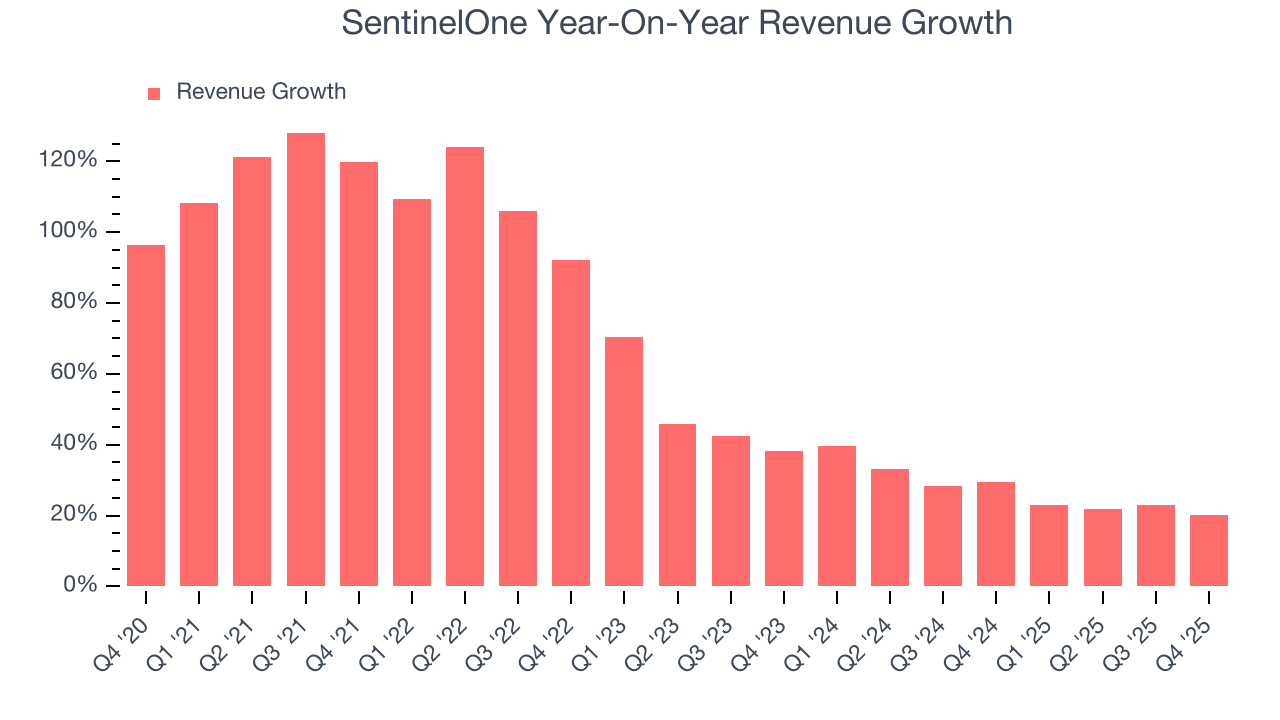

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, SentinelOne’s sales grew at an incredible 60.8% compounded annual growth rate over the last five years. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. SentinelOne’s annualized revenue growth of 27% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, SentinelOne’s year-on-year revenue growth of 20.2% was excellent, and its $271.2 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 20.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 19.8% over the next 12 months, a deceleration versus the last two years. Still, this projection is noteworthy and suggests the market sees success for its products and services.

6. Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

SentinelOne’s ARR punched in at $1.12 billion in Q4, and over the last four quarters, its growth was fantastic as it averaged 23.2% year-on-year increases. This performance aligned with its total sales growth and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes SentinelOne a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

7. Enterprise Customer Base

This quarter, SentinelOne reported 1,667 enterprise customers paying more than $100,000 annually, an increase of 95 from the previous quarter. That’s quite a bit more contract wins than last quarter and quite a bit above what we’ve observed over the previous year. Shareholders should take this as an indication that SentinelOne’s go-to-market strategy is working well.

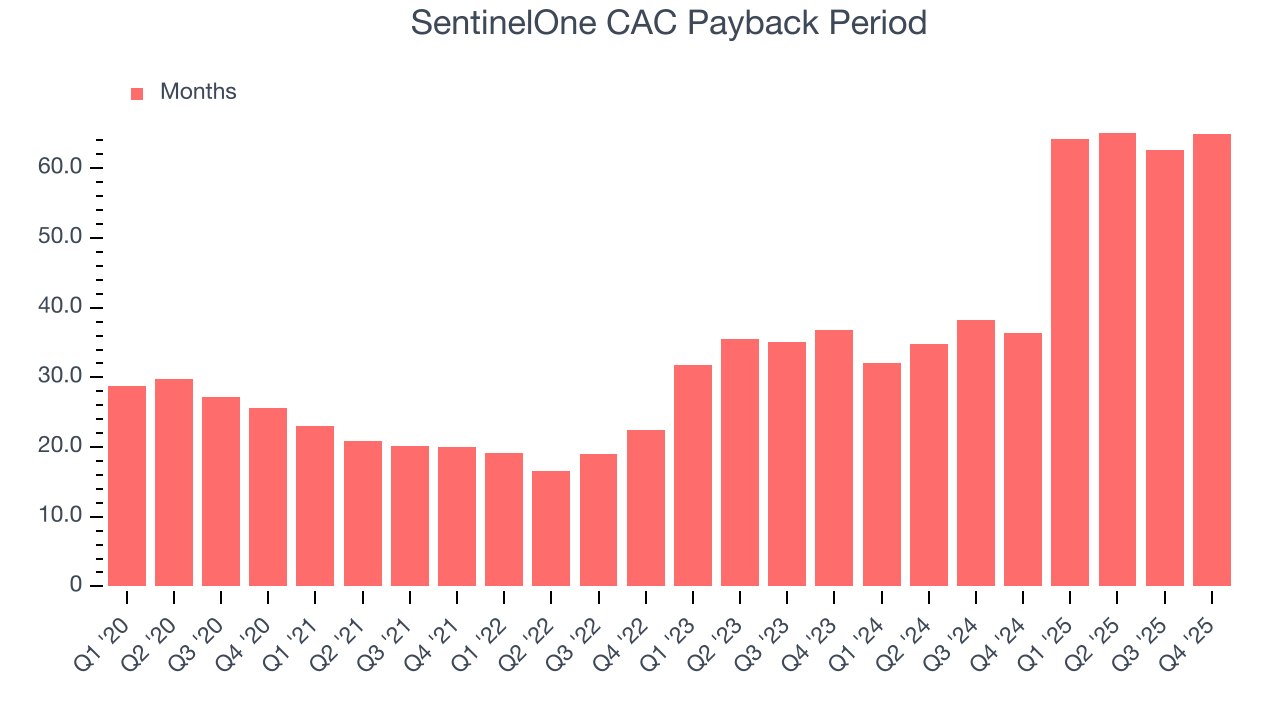

8. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

It’s relatively expensive for SentinelOne to acquire new customers as its CAC payback period checked in at 65 months this quarter. The company’s drawn-out sales cycles partly stem from its focus on enterprise clients who require some degree of customization, resulting in long onboarding periods. The complex integrations are a double-edged sword - while SentinelOne may not see immediate returns from its sales and marketing investments, it is rewarded with higher switching costs and lifetime value if it can continue meeting its customer’s needs.

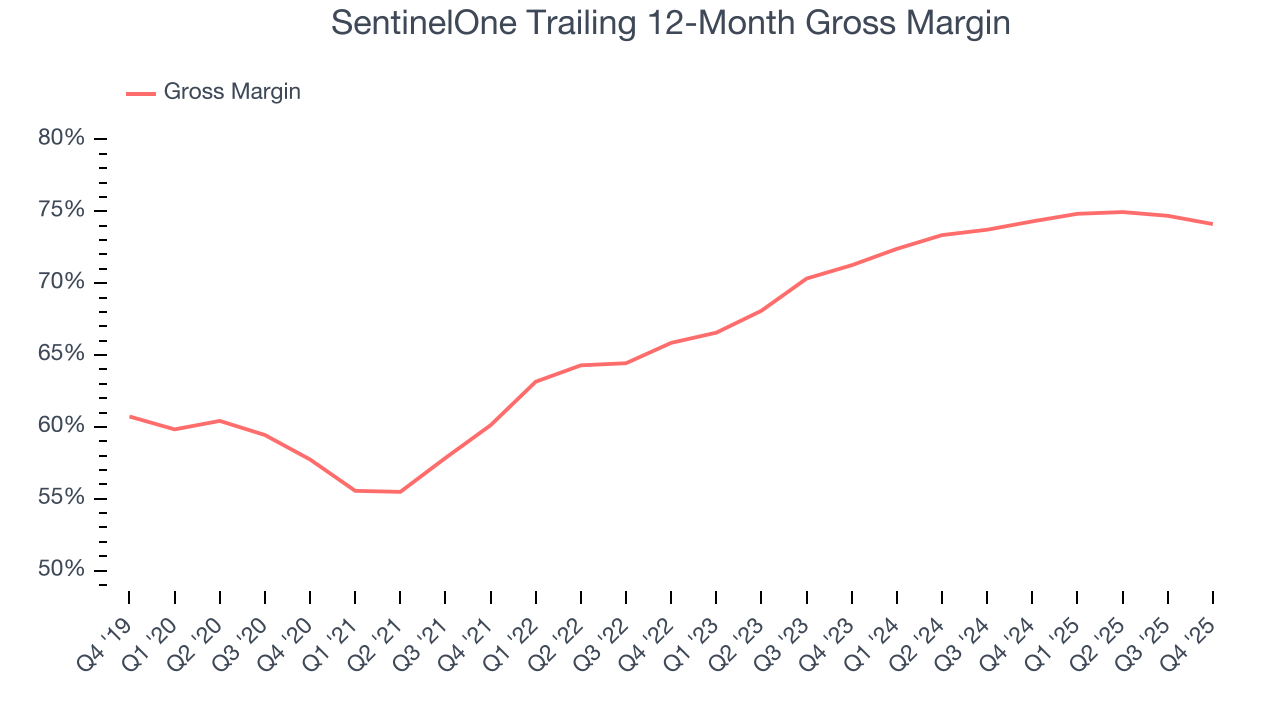

9. Gross Margin & Pricing Power

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

SentinelOne’s gross margin is better than the broader software industry and signals it has solid unit economics and competitive products. As you can see below, it averaged a decent 74.1% gross margin over the last year. That means for every $100 in revenue, roughly $74.12 was left to spend on selling, marketing, and R&D.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. SentinelOne has seen gross margins improve by 2.9 percentage points over the last 2 year, which is very good in the software space.

In Q4, SentinelOne produced a 72.6% gross profit margin, down 2.1 percentage points year on year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

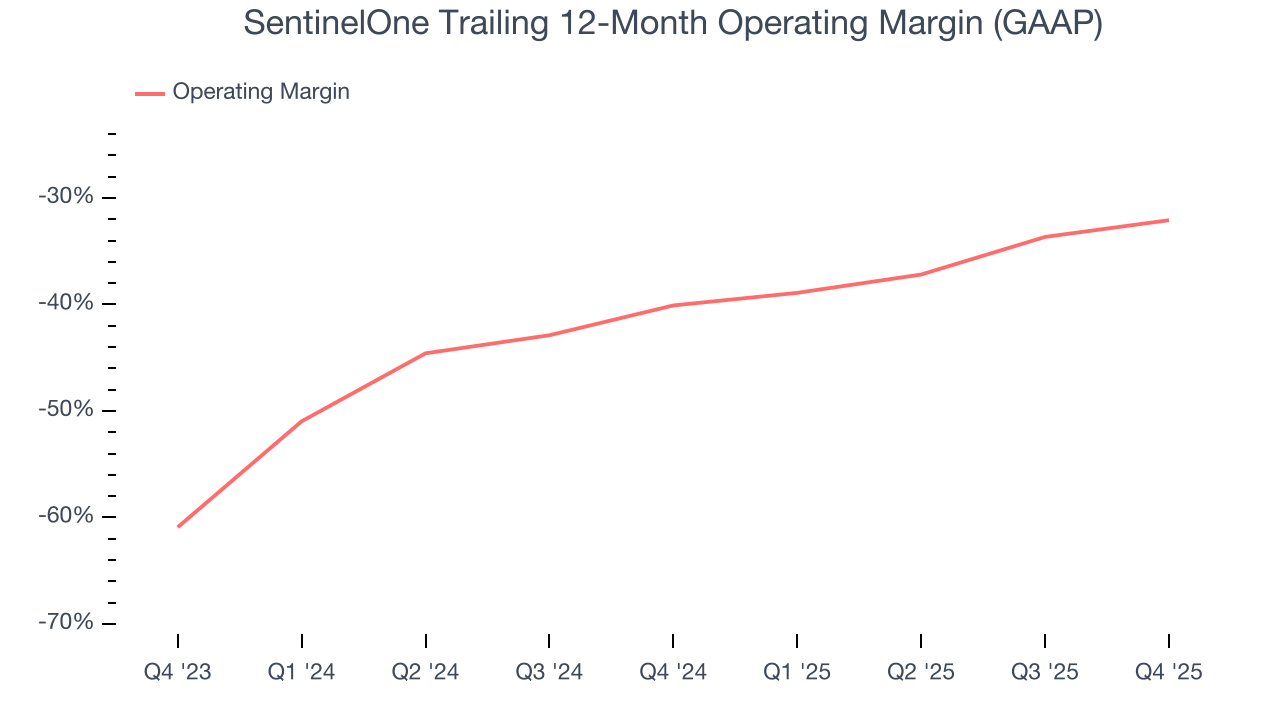

10. Operating Margin

SentinelOne’s expensive cost structure has contributed to an average operating margin of negative 32.1% over the last year. This happened because the company spent loads of money to capture market share. As seen in its fast revenue growth, the aggressive strategy has paid off so far, and Wall Street’s estimates suggest the party will continue. We tend to agree and believe the business has a good chance of reaching profitability upon scale.

Over the last two years, SentinelOne’s expanding sales gave it operating leverage as its margin rose by 8 percentage points. Still, it will take much more for the company to reach long-term profitability.

SentinelOne’s operating margin was negative 29.5% this quarter.

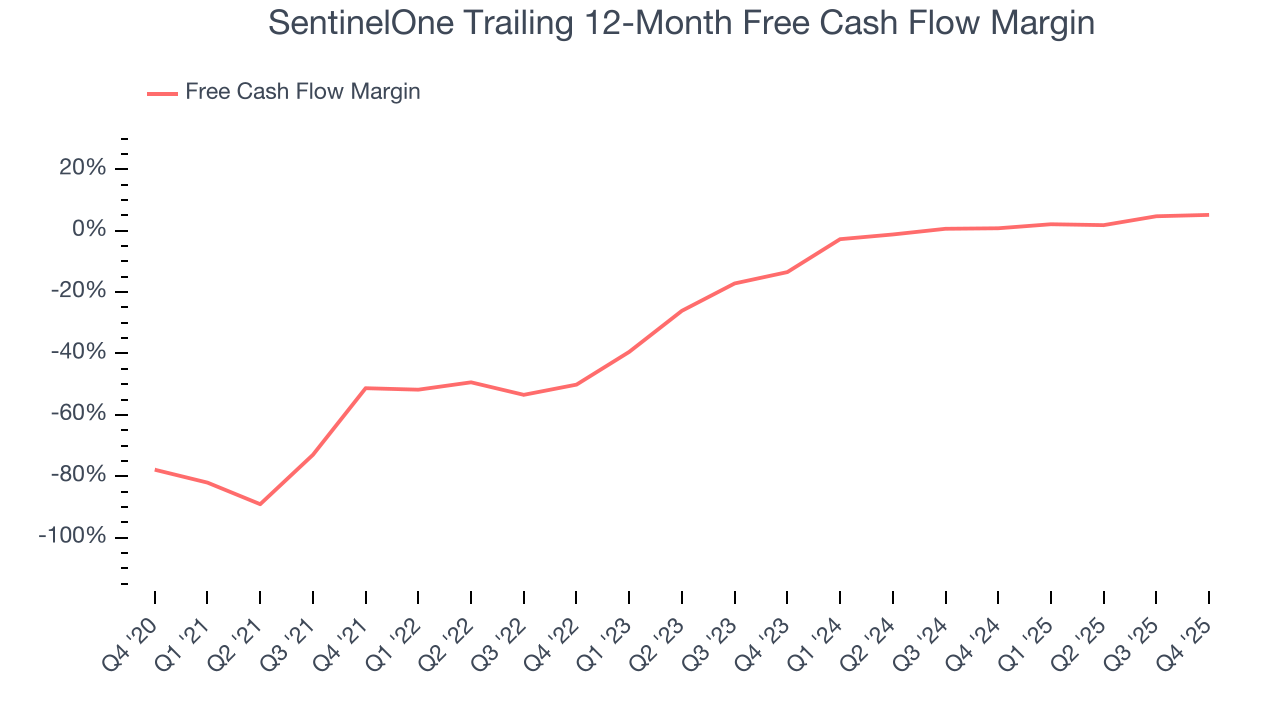

11. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

SentinelOne has shown weak cash profitability relative to peers over the last year, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 5.2%, below what we’d expect for a software business.

SentinelOne broke even from a free cash flow perspective in Q4. This result was good as its margin was 3.1 percentage points higher than in the same quarter last year, but we note it was lower than its one-year cash profitability. Nevertheless, we wouldn’t read too much into a single quarter because investment needs can be seasonal, causing short-term swings. Long-term trends trump temporary fluctuations.

Over the next year, analysts predict SentinelOne’s cash conversion will improve. Their consensus estimates imply its free cash flow margin of 5.2% for the last 12 months will increase to 13.2%, giving it more flexibility for investments, share buybacks, and dividends.

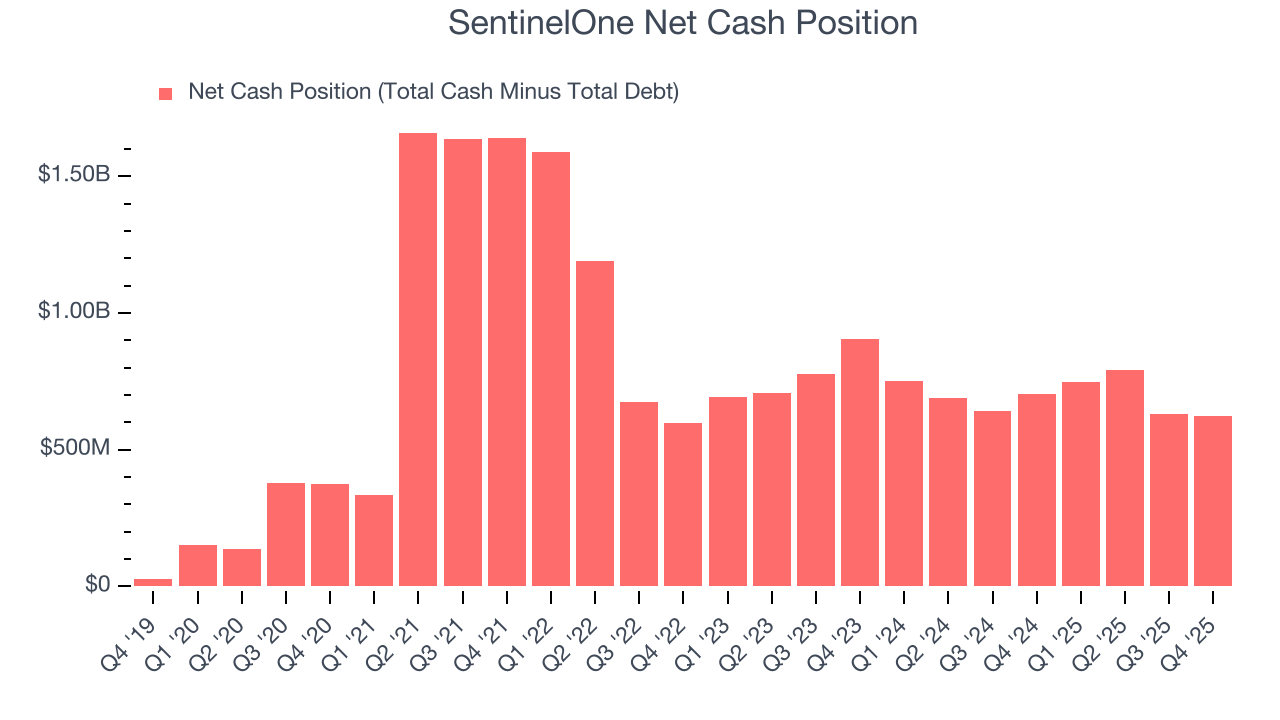

12. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

SentinelOne is a well-capitalized company with $628.7 million of cash and $5.12 million of debt on its balance sheet. This $623.5 million net cash position is 12.6% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from SentinelOne’s Q4 Results

We were impressed by SentinelOne’s optimistic full-year EPS guidance, which blew past analysts’ expectations. We were also happy with next year’s revenue guidance. On the other hand, its EPS guidance for next quarter missed and its revenue guidance for next quarter was in line with Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The market seemed to be hoping for more, and the stock traded down 4.3% to $13.25 immediately after reporting.

14. Is Now The Time To Buy SentinelOne?

Updated: March 16, 2026 at 10:15 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in SentinelOne.

SentinelOne possesses a number of positive attributes. First off, its revenue growth was exceptional over the last five years. And while its operating margins reveal poor profitability compared to other software companies, its surging ARR shows its fundamentals and revenue predictability are improving. On top of that, its gross margin suggests it can generate sustainable profits.

SentinelOne’s price-to-sales ratio based on the next 12 months is 4x. Looking at the software landscape right now, SentinelOne trades at a pretty interesting price. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $18.56 on the company (compared to the current share price of $14.27), implying they see 30.1% upside in buying SentinelOne in the short term.