C3.ai (AI)

C3.ai keeps us up at night. Its poor revenue growth shows demand is soft and its cash burn makes us question its business model.― StockStory Analyst Team

1. News

2. Summary

Why We Think C3.ai Will Underperform

Named after the three Cs of its original focus—carbon, cloud computing, and customer relationship management—C3.ai (NYSE:AI) provides enterprise AI software that helps organizations develop, deploy, and operate large-scale artificial intelligence applications across various industries.

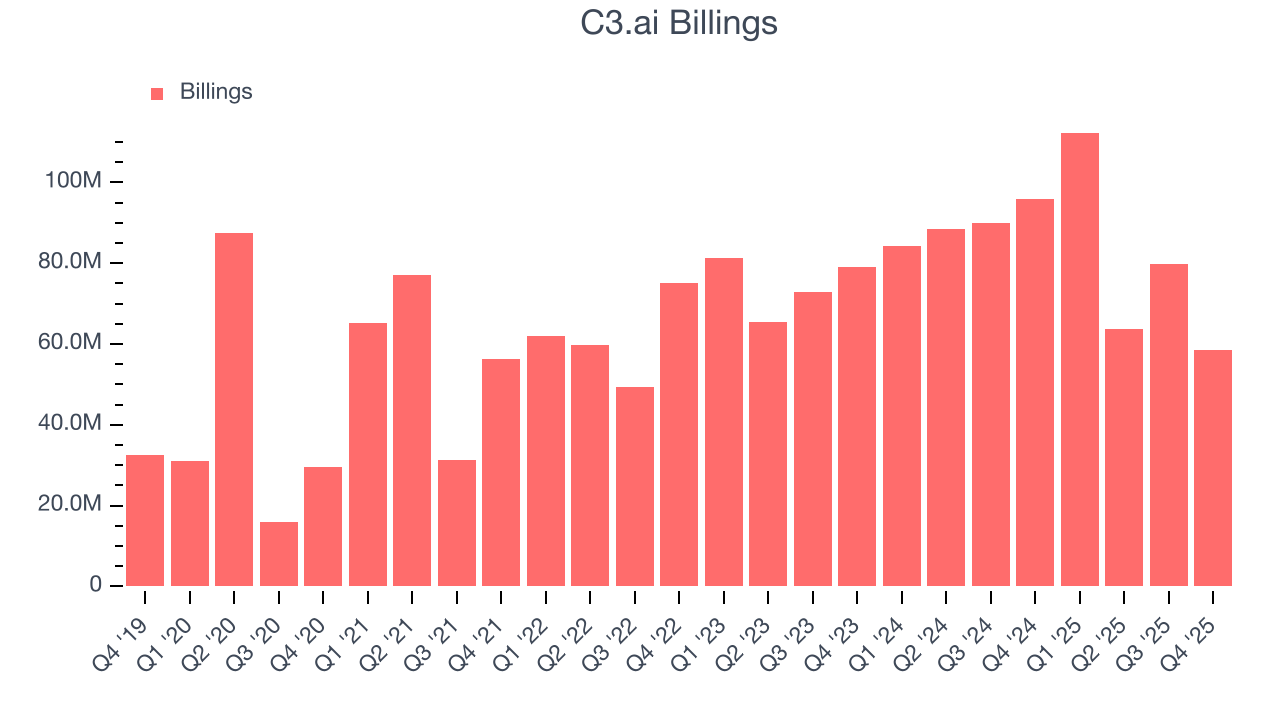

- Billings have dropped by 11.2% over the last year, suggesting it might have to lower prices to stimulate growth

- Projected sales decline of 31.9% for the next 12 months points to a tough demand environment ahead

- Sky-high servicing costs result in an inferior gross margin of 43.5% that must be offset through increased usage

C3.ai falls short of our quality standards. You should search for better opportunities.

Why There Are Better Opportunities Than C3.ai

C3.ai’s stock price of $8.67 implies a valuation ratio of 5.8x forward price-to-sales. This multiple expensive for its subpar fundamentals.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. C3.ai (AI) Research Report: Q4 CY2025 Update

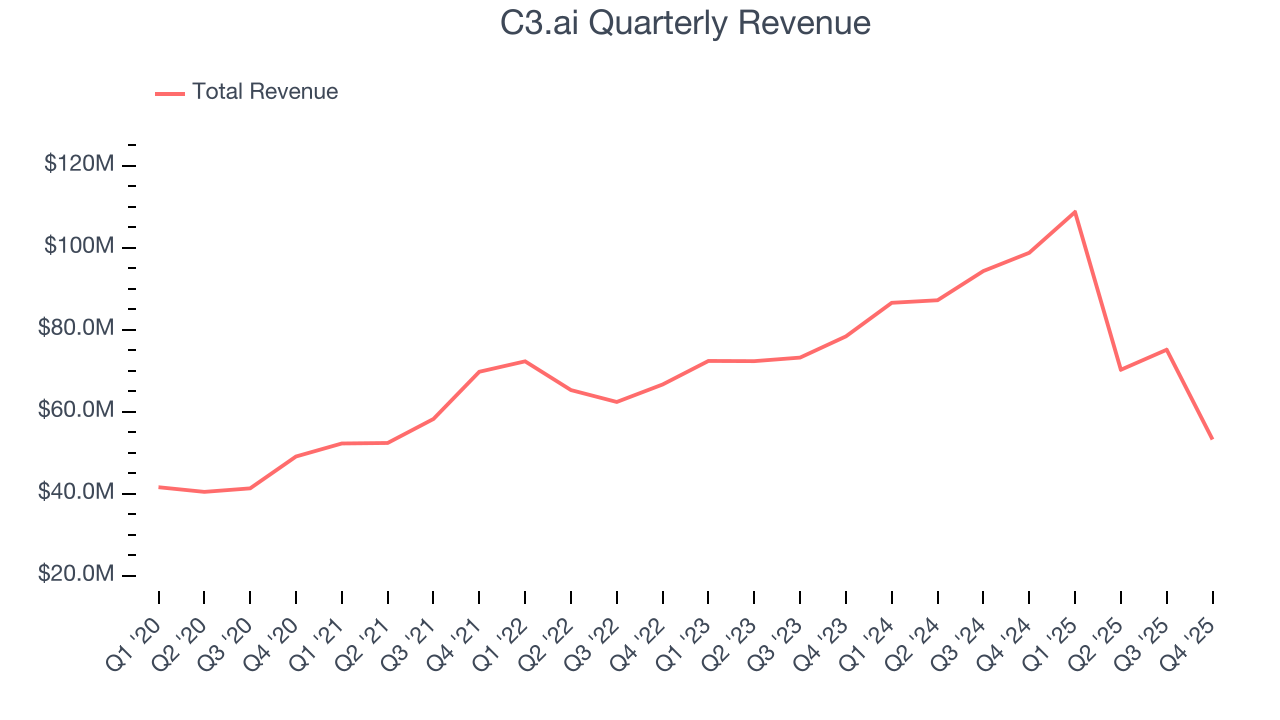

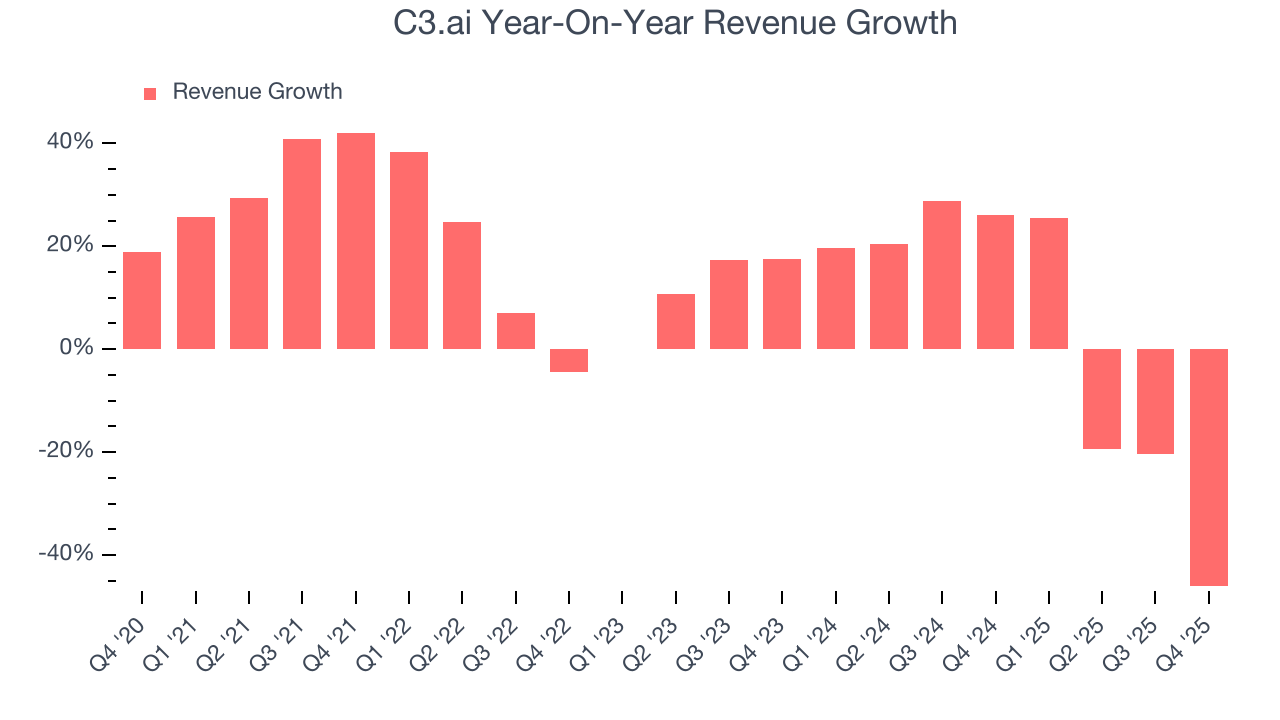

Enterprise AI software company C3.ai (NYSE:AI) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 46.1% year on year to $53.26 million. Next quarter’s revenue guidance of $50 million underwhelmed, coming in 35.9% below analysts’ estimates. Its GAAP loss of $0.94 per share was 24% below analysts’ consensus estimates.

C3.ai (AI) Q4 CY2025 Highlights:

- Revenue: $53.26 million vs analyst estimates of $75.66 million (46.1% year-on-year decline, 29.6% miss)

- EPS (GAAP): -$0.94 vs analyst expectations of -$0.76 (24% miss)

- Revenue Guidance for Q1 CY2026 is $50 million at the midpoint, below analyst estimates of $78.01 million

- Operating Margin: -264%, down from -88.7% in the same quarter last year

- Free Cash Flow was -$56.2 million compared to -$46.88 million in the previous quarter

- Billings: $58.57 million at quarter end, down 39% year on year

- Market Capitalization: $1.42 billion

Company Overview

Named after the three Cs of its original focus—carbon, cloud computing, and customer relationship management—C3.ai (NYSE:AI) provides enterprise AI software that helps organizations develop, deploy, and operate large-scale artificial intelligence applications across various industries.

The company's offerings are organized into three main product families: the C3 AI Platform, C3 AI Applications, and C3 Generative AI. The C3 AI Platform serves as the foundation for all the company's solutions, utilizing a model-driven architecture that enables customers to build AI applications without writing extensive code. This approach significantly reduces development time and complexity, allowing organizations to deploy enterprise-scale AI applications in as little as four weeks.

C3 AI Applications comprises a suite of pre-built, industry-specific AI solutions targeting high-value use cases across sectors like manufacturing, energy, financial services, defense, and supply chain management. Each application is designed to address specific business challenges, such as predictive maintenance, inventory optimization, fraud detection, or emissions management.

With its most recent addition, C3 Generative AI, the company has expanded its capabilities to include large language models and generative AI technologies. This solution allows users to access enterprise data through natural language interfaces while maintaining security controls and reducing the risk of AI "hallucinations" by connecting responses to verified data sources.

The company employs a consumption-based pricing model where customers either pay monthly fees based on computing resources used or enter into multi-period commitments. Its go-to-market strategy involves strategic partnerships with major technology providers like Google Cloud, AWS, Microsoft Azure, and industry specialists like Baker Hughes in the oil and gas sector, allowing C3.ai to extend its reach across global markets.

4. Data Infrastructure

Generating insights from system level data is an increasing priority for most businesses, but to do so requires connecting and analyzing piles of data stored and siloed in separate databases. This is the demand driver for cloud based data infrastructure software providers, who can more readily integrate, distribute and process information vs. legacy on-premise software providers.

C3.ai competes with large enterprise software providers like Microsoft (NASDAQ:MSFT), IBM (NYSE:IBM), and Oracle (NYSE:ORCL), cloud service providers offering AI platforms including Google (NASDAQ:GOOGL), Amazon (NASDAQ:AMZN), and specialized AI companies such as Palantir Technologies (NYSE:PLTR) and DataRobot.

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, C3.ai grew its sales at a 12.2% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. C3.ai’s recent performance shows its demand has slowed as its annualized revenue growth of 1.8% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, C3.ai missed Wall Street’s estimates and reported a rather uninspiring 46.1% year-on-year revenue decline, generating $53.26 million of revenue. Company management is currently guiding for a 54% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.3% over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

C3.ai’s billings came in at $58.57 million in Q4, and it averaged 11.2% year-on-year declines over the last four quarters. However, this alternate topline metric outperformed its total sales, meaning the company collects cash upfront and then recognizes the revenue over the length of its contracts - a boost for its liquidity and future revenue prospects.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

C3.ai is extremely efficient at acquiring new customers, and its CAC payback period checked in at 16 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

8. Gross Margin & Pricing Power

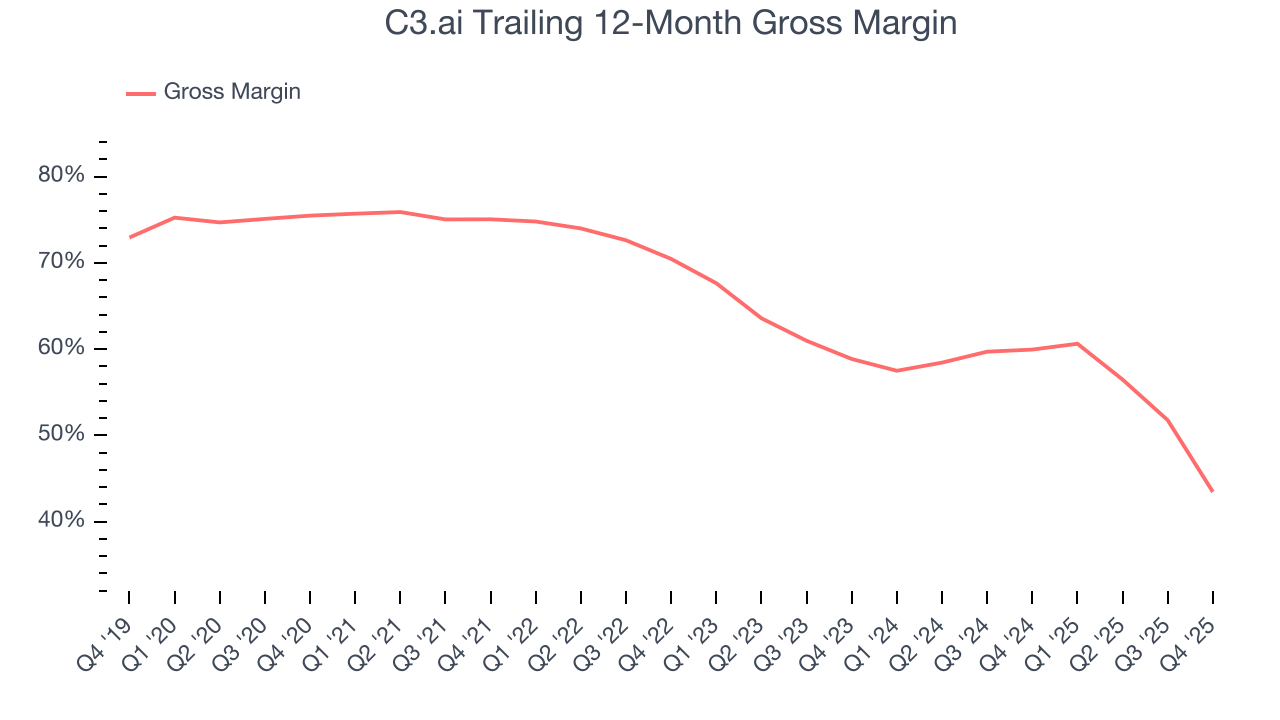

For software companies like C3.ai, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

C3.ai’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 43.5% gross margin over the last year. That means C3.ai paid its providers a lot of money ($56.55 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. C3.ai has seen gross margins decline by 15.4 percentage points over the last 2 year, which is among the worst in the software space.

In Q4, C3.ai produced a 17.3% gross profit margin, down 41.7 percentage points year on year. C3.ai’s full-year margin has also been trending down over the past 12 months, decreasing by 16.5 percentage points. If this move continues, it could suggest deteriorating pricing power and higher input costs.

9. Operating Margin

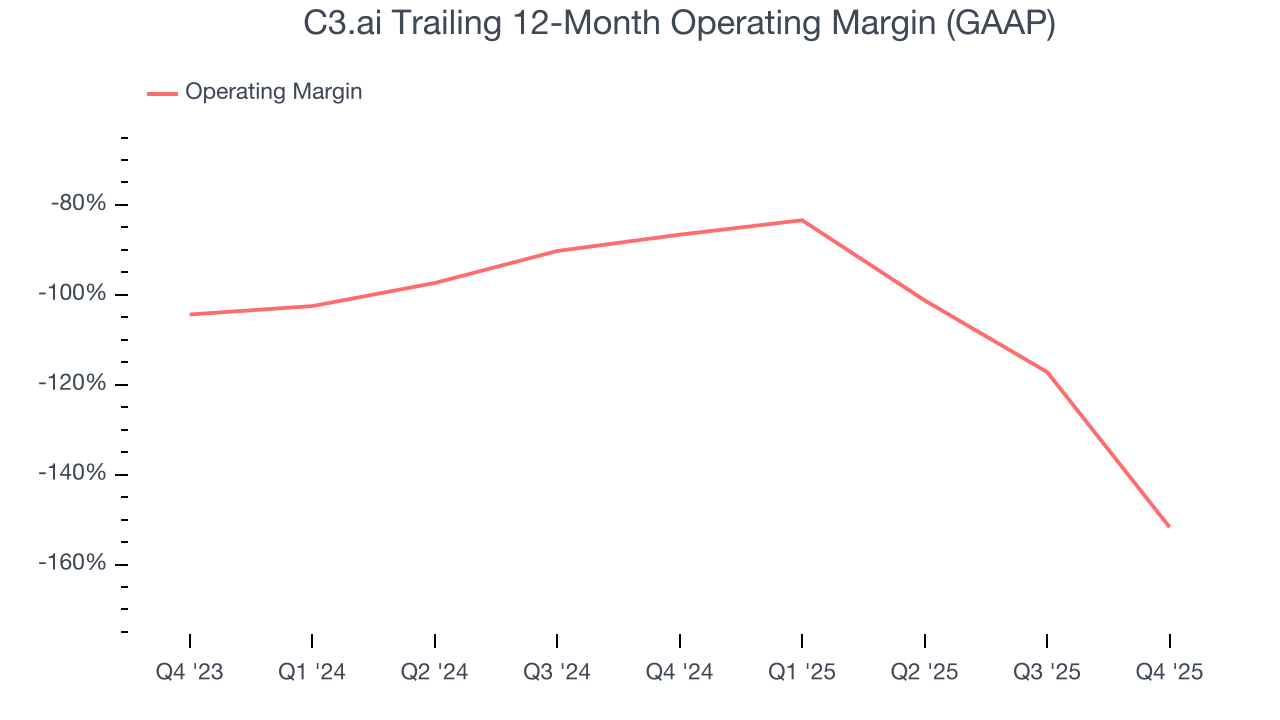

C3.ai’s expensive cost structure has contributed to an average operating margin of negative 152% over the last year. Unprofitable software companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if C3.ai reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

Analyzing the trend in its profitability, C3.ai’s operating margin decreased by 65.1 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. C3.ai’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, C3.ai generated a negative 264% operating margin. The company's consistent lack of profits raise a flag.

10. Cash Is King

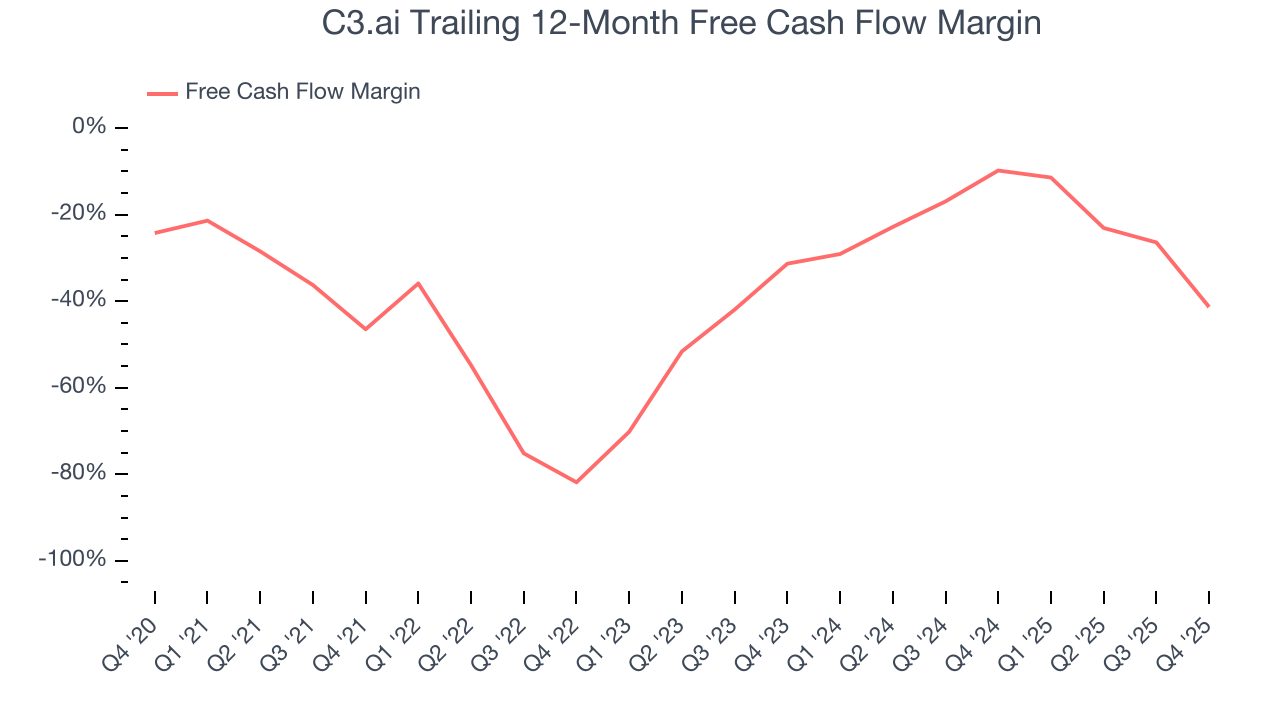

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

C3.ai’s demanding reinvestments have drained its resources over the last year, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 41.3%, meaning it lit $41.33 of cash on fire for every $100 in revenue.

C3.ai burned through $56.2 million of cash in Q4, equivalent to a negative 106% margin. The company’s cash burn increased from $22.38 million of lost cash in the same quarter last year.

Over the next year, analysts predict C3.ai will continue burning cash, albeit to a lesser extent. Their consensus estimates imply its free cash flow margin of negative 41.3% for the last 12 months will increase to negative 38%.

11. Balance Sheet Assessment

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

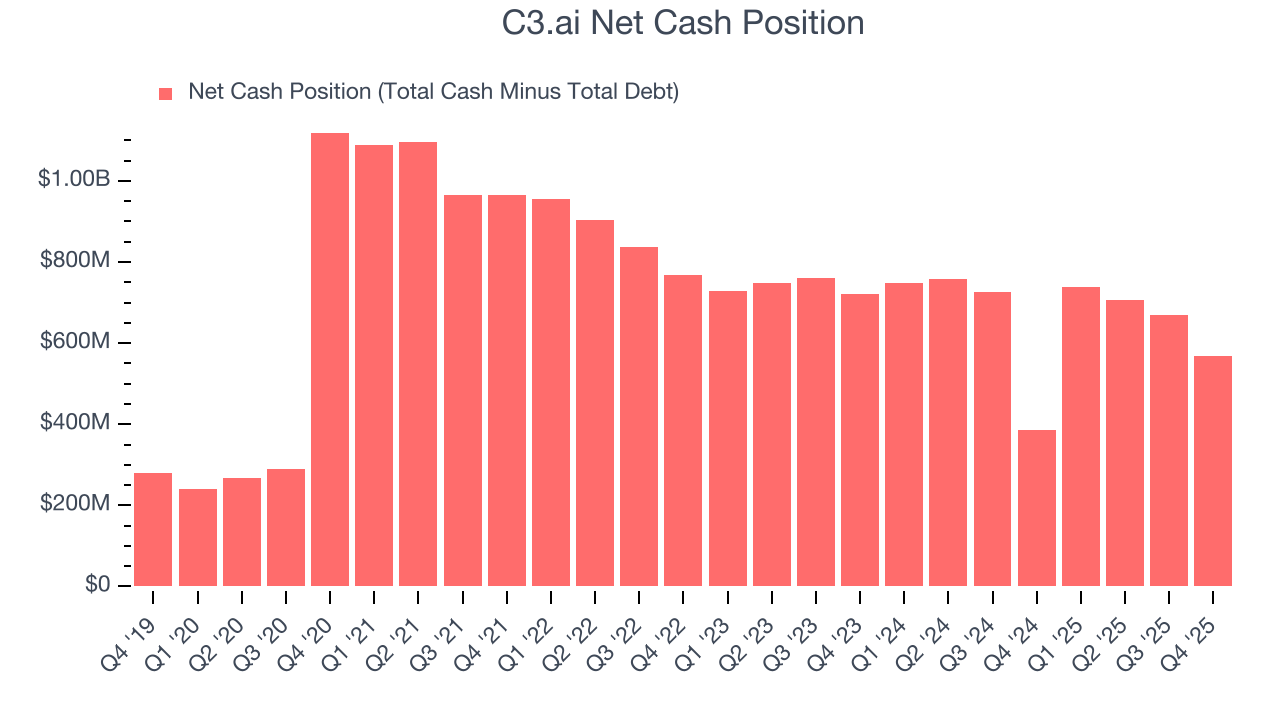

C3.ai burned through $127 million of cash over the last year. Although the company has $54.88 million of debt on its balance sheet, we think its $621.9 million of cash gives it enough runway (we typically look for at least two years) to prioritize growth over profitability.

12. Key Takeaways from C3.ai’s Q4 Results

We struggled to find many positives in these results. Its full-year revenue guidance missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter was quite bad. The stock traded down 20.8% to $8.18 immediately after reporting.

13. Is Now The Time To Buy C3.ai?

Updated: March 19, 2026 at 10:20 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in C3.ai.

C3.ai falls short of our quality standards. For starters, its revenue growth was uninspiring over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its efficient sales strategy allows it to target and onboard new users at scale, the downside is its declining operating margin shows it’s becoming less efficient at building and selling its software. On top of that, its operating margins reveal poor profitability compared to other software companies.

C3.ai’s price-to-sales ratio based on the next 12 months is 5.8x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $8.82 on the company (compared to the current share price of $8.67).