Brady (BRC)

Brady catches our eye. It consistently invests in attractive growth opportunities, generating substantial cash flows and returns.― StockStory Analyst Team

1. News

2. Summary

Why Brady Is Interesting

Founded in 1914 and evolving through more than a century of industrial innovation, Brady (NYSE:BRC) manufactures and supplies identification solutions and workplace safety products that help companies identify and protect their premises, products, and people.

- Earnings per share have massively outperformed its peers over the last five years, increasing by 15.7% annually

- Disciplined cost controls and effective management have materialized in a strong operating margin

- On the other hand, its absence of organic revenue growth over the past two years suggests it may have to lean into acquisitions to drive its expansion

Brady is close to becoming a high-quality business. If you believe in the company, the price looks reasonable.

Why Is Now The Time To Buy Brady?

At $84.34 per share, Brady trades at 16.6x forward P/E. Brady’s valuation is lower than that of many in the business services space. Even so, we think it is justified for the revenue growth characteristics.

It could be a good time to invest if you see something the market doesn’t.

3. Brady (BRC) Research Report: Q3 CY2025 Update

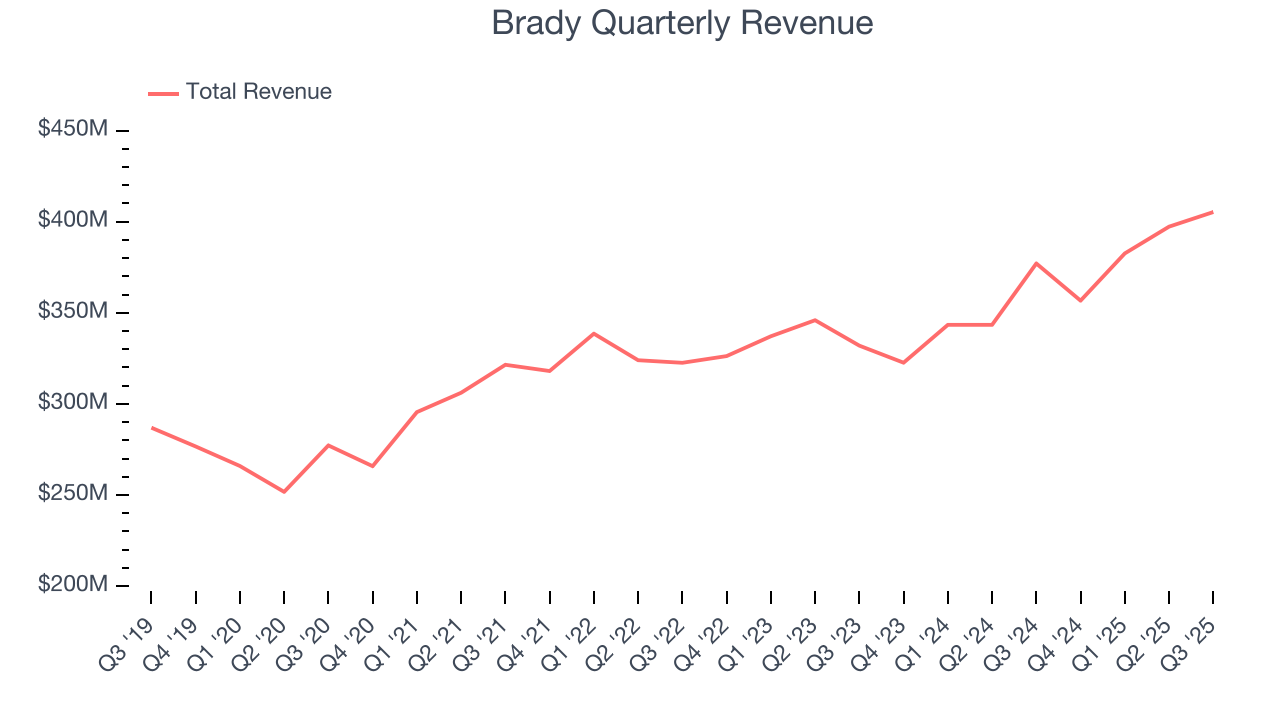

Identification solutions manufacturer Brady (NYSE:BRC) reported Q3 CY2025 results beating Wall Street’s revenue expectations, with sales up 7.5% year on year to $405.3 million. Its non-GAAP profit of $1.21 per share was 1.7% above analysts’ consensus estimates.

Brady (BRC) Q3 CY2025 Highlights:

- Revenue: $405.3 million vs analyst estimates of $395 million (7.5% year-on-year growth, 2.6% beat)

- Adjusted EPS: $1.21 vs analyst estimates of $1.19 (1.7% beat)

- Adjusted EBITDA: $85.73 million vs analyst estimates of $80.1 million (21.2% margin, 7% beat)

- Management slightly raised its full-year Adjusted EPS guidance to $5.03 at the midpoint

- Operating Margin: 16.8%, up from 15.6% in the same quarter last year

- Free Cash Flow Margin: 5.5%, up from 4.3% in the same quarter last year

- Market Capitalization: $3.53 billion

Company Overview

Founded in 1914 and evolving through more than a century of industrial innovation, Brady (NYSE:BRC) manufactures and supplies identification solutions and workplace safety products that help companies identify and protect their premises, products, and people.

Brady's product portfolio spans several categories designed to meet critical workplace needs. The company's safety and facility identification products include safety signs, floor-marking tape, pipe markers, lockout/tagout devices, and spill control products that help businesses maintain compliant and hazard-free environments. Its product identification solutions feature materials, printing systems, and RFID technology that enable manufacturers to track assets and label finished products. Wire identification products help electricians and engineers properly mark electrical components, while healthcare identification solutions assist hospitals in tracking patients and specimens.

The company operates through two geographic segments: Americas & Asia and Europe & Australia. This regional structure allows Brady to tailor its offerings to local market needs while maintaining global manufacturing standards. Brady's products reach customers through multiple channels, including distributors, a direct sales force, and digital platforms, with the company maintaining long-standing relationships with electrical, safety, and industrial distributors worldwide.

A manufacturing company at its core, Brady produces most of its proprietary products in-house. Its manufacturing processes involve precision techniques like compounding, coating, converting, and melt-blown operations. For example, a manufacturing plant might use Brady's lockout/tagout devices to prevent accidental equipment startups during maintenance, while simultaneously using Brady's floor-marking tape to designate safe walking paths and its identification labels to track inventory.

Brady serves diverse industries including industrial manufacturing, healthcare, chemical, oil and gas, automotive, aerospace, construction, and utilities. The company generates revenue by selling its physical products and related software solutions, with ongoing innovation driven by its research and development team that focuses on creating new products that solve customer problems and improve environmental sustainability.

4. Safety & Security Services

Rising concerns over physical security, cybersecurity threats, and workplace safety regulations will present opportunities for companies in this sector. AI and digitization will enhance surveillance, access control, and threat detection, which could benefit key players in Safety & Security Services. These trends could also introduce ethical and regulatory concerns over data privacy and automated decision-making in security operations, giving rise to headline risks. Finally, increasing scrutiny on private security practices and evolving criminal justice policies again mean that companies in the space need to operate with the utmost care or risk being the poster child of abuse of power.

Brady's competitors include 3M (NYSE: MMM) in safety and identification products, Avery Dennison (NYSE: AVY) in labeling and identification solutions, and Honeywell (NASDAQ: HON) in workplace safety equipment, along with regional players in specific market segments.

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $1.54 billion in revenue over the past 12 months, Brady is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

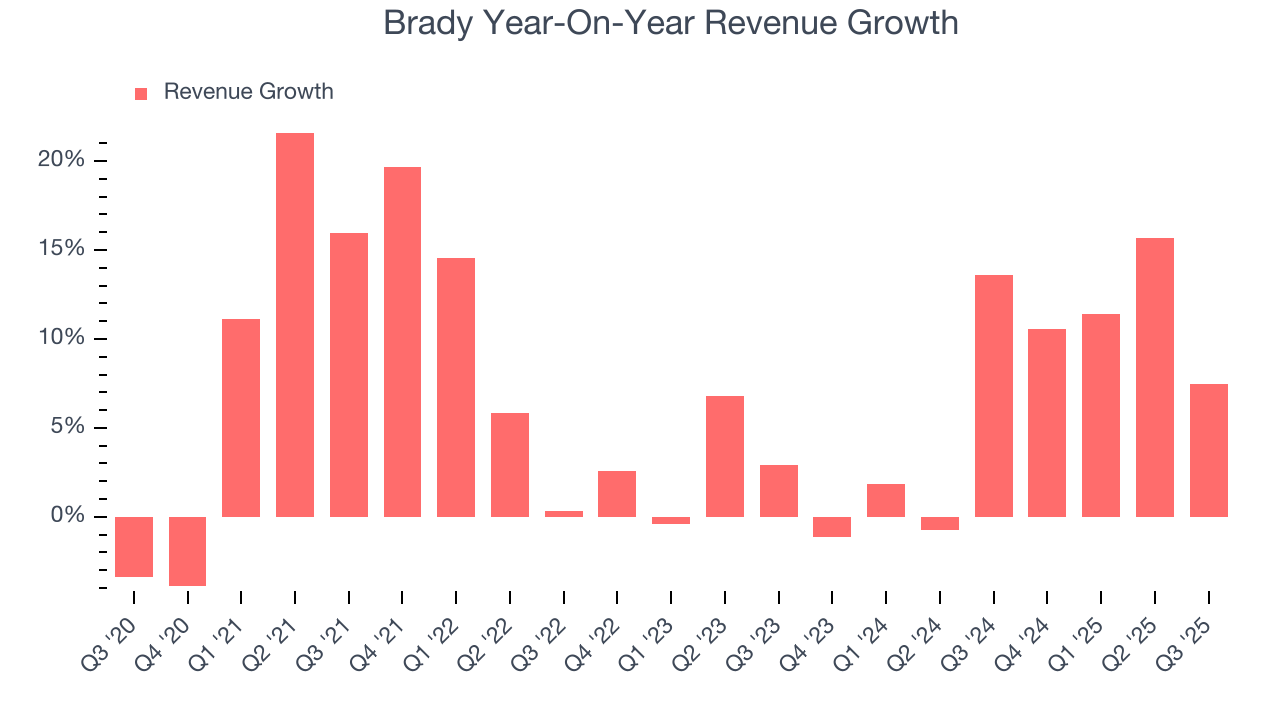

As you can see below, Brady grew its sales at a solid 7.5% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Brady’s annualized revenue growth of 7.2% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, Brady reported year-on-year revenue growth of 7.5%, and its $405.3 million of revenue exceeded Wall Street’s estimates by 2.6%.

Looking ahead, sell-side analysts expect revenue to grow 4% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges.

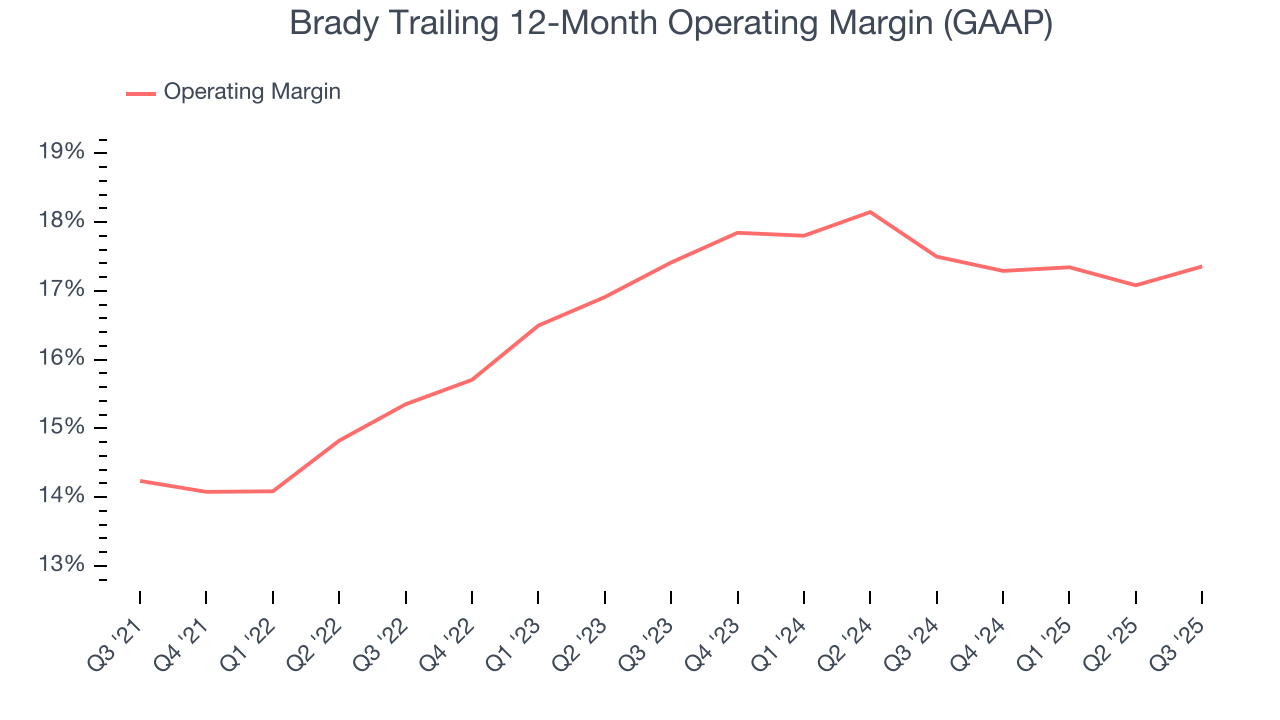

6. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Brady has been an efficient company over the last five years. It was one of the more profitable businesses in the business services sector, boasting an average operating margin of 16.5%.

Looking at the trend in its profitability, Brady’s operating margin rose by 3.1 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q3, Brady generated an operating margin profit margin of 16.8%, up 1.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

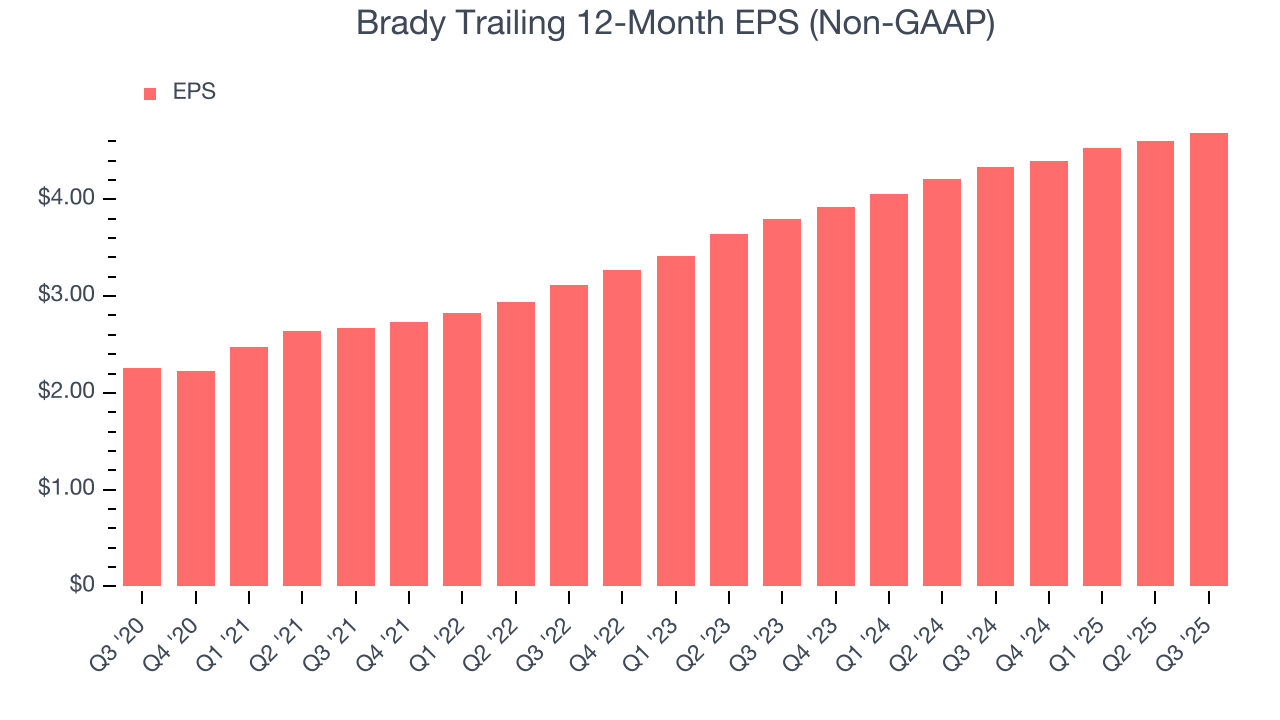

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Brady’s EPS grew at an astounding 15.7% compounded annual growth rate over the last five years, higher than its 7.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

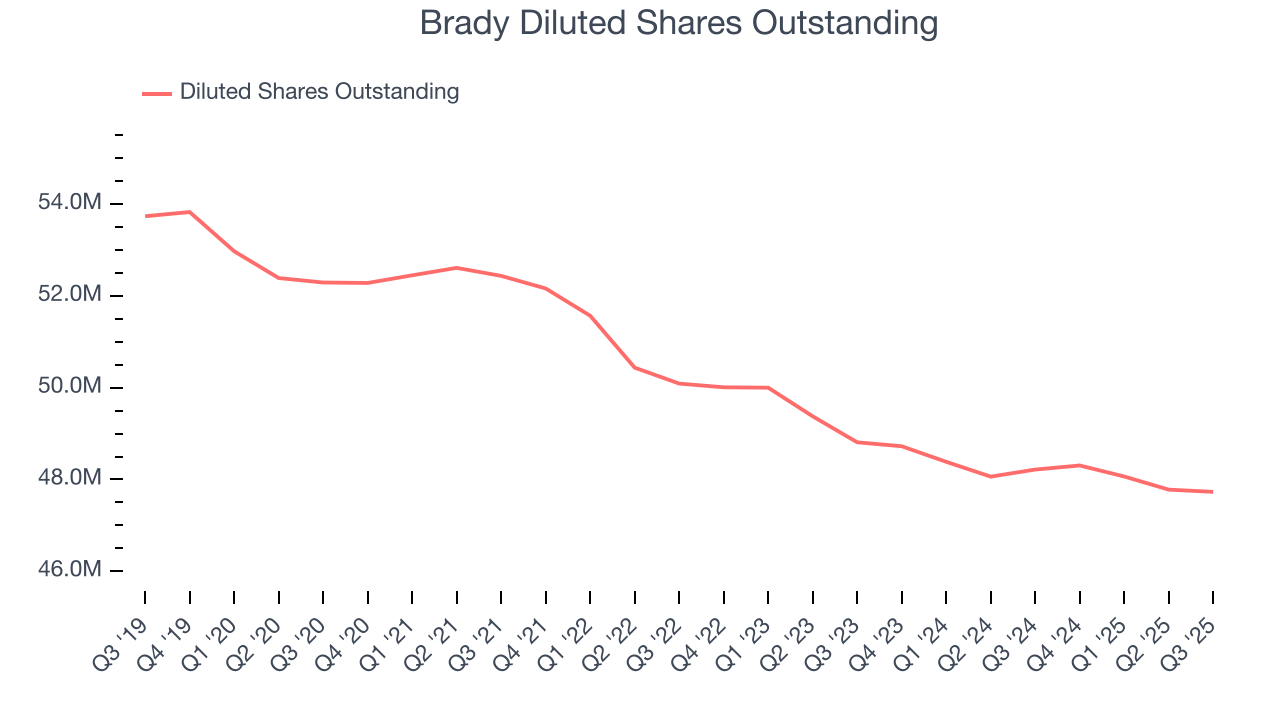

Diving into Brady’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Brady’s operating margin expanded by 3.1 percentage points over the last five years. On top of that, its share count shrank by 8.7%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Brady, its two-year annual EPS growth of 11.1% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q3, Brady reported adjusted EPS of $1.21, up from $1.12 in the same quarter last year. This print beat analysts’ estimates by 1.7%. Over the next 12 months, Wall Street expects Brady’s full-year EPS of $4.69 to grow 9.3%.

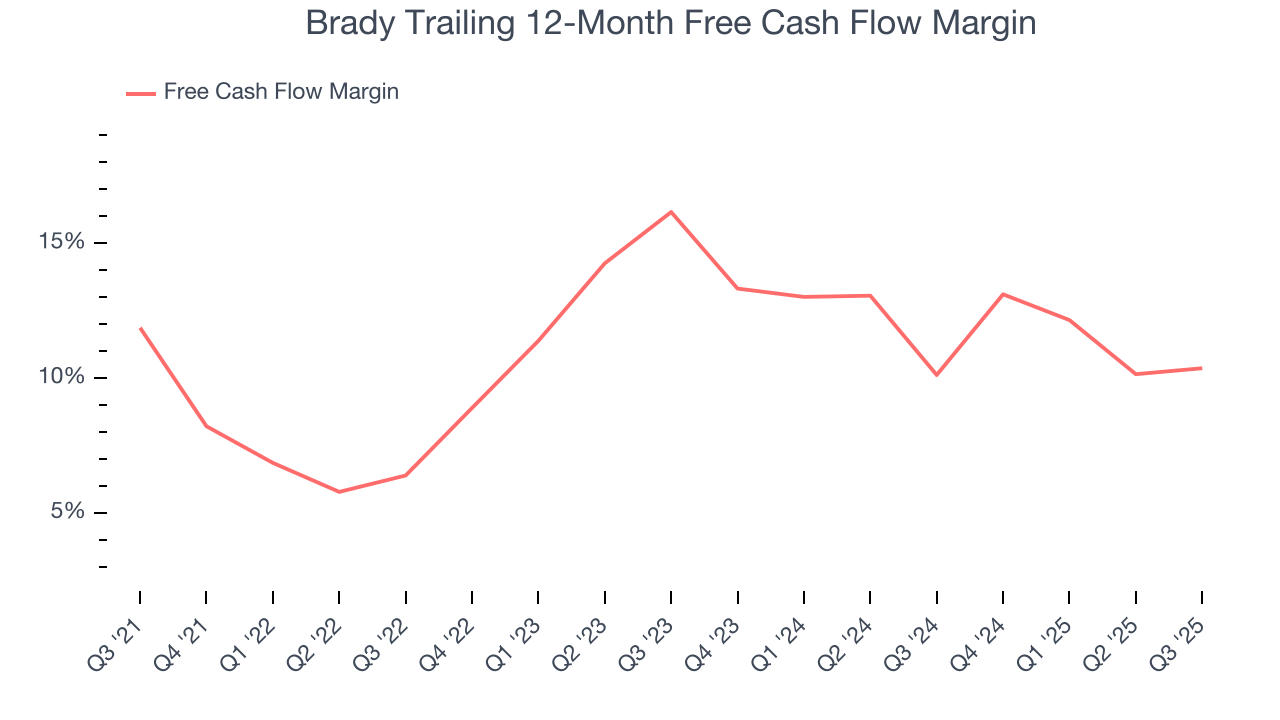

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Brady has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 11% over the last five years, quite impressive for a business services business.

Taking a step back, we can see that Brady’s margin dropped by 1.5 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Brady’s free cash flow clocked in at $22.38 million in Q3, equivalent to a 5.5% margin. This result was good as its margin was 1.2 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

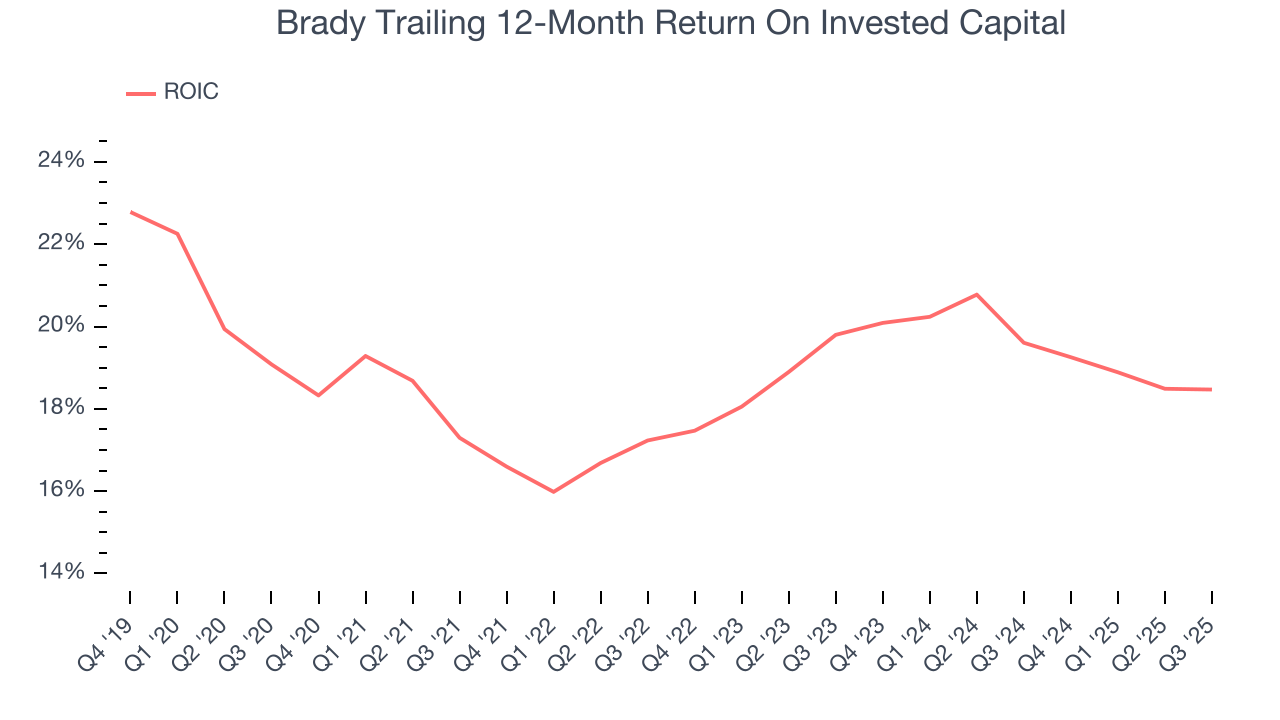

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Brady hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked. Its five-year average ROIC was 18.5%, higher than most business services businesses.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Brady’s ROIC increased by 1.8 percentage points annually over the last few years. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

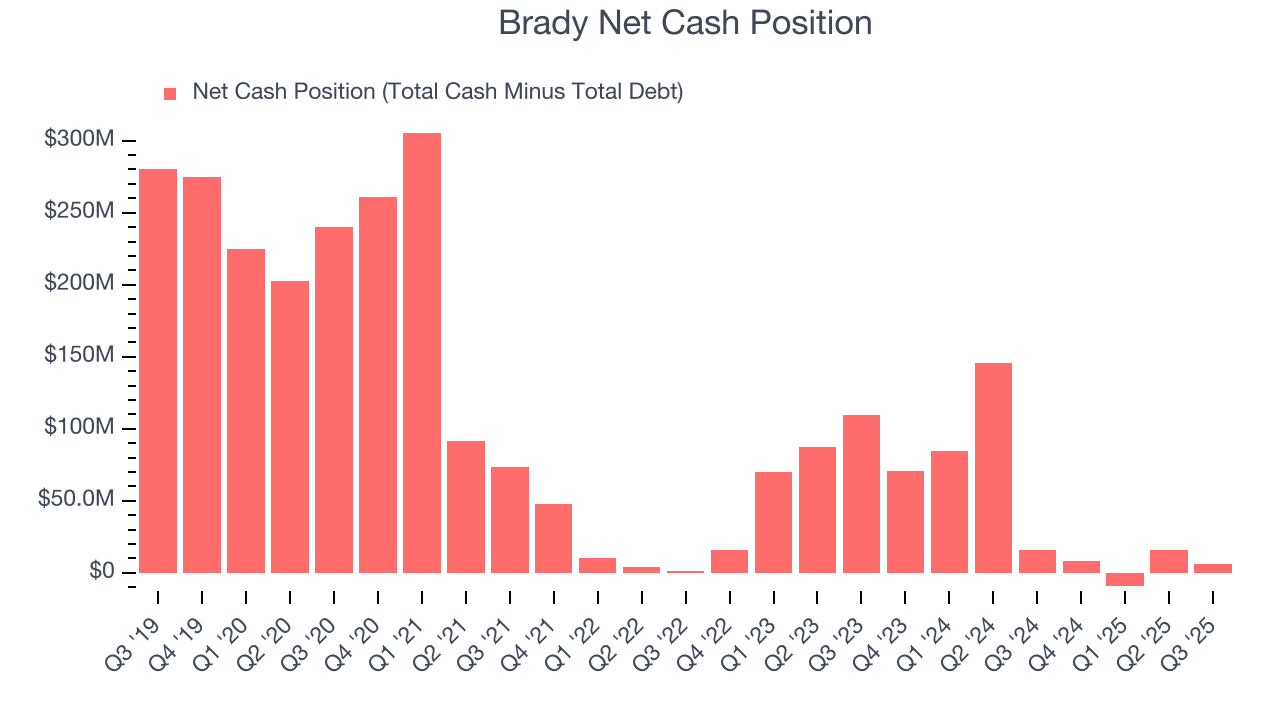

10. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Brady is a profitable, well-capitalized company with $182.7 million of cash and $176.8 million of debt on its balance sheet. This $5.9 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Brady’s Q3 Results

We enjoyed seeing Brady beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $75 immediately after reporting.

12. Is Now The Time To Buy Brady?

Updated: January 24, 2026 at 9:06 PM EST

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Brady, you should also grasp the company’s longer-term business quality and valuation.

There are some positives when it comes to Brady’s fundamentals. To kick things off, its revenue growth was solid over the last five years. And while its organic revenue growth has disappointed, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders. On top of that, its strong operating margins show it’s a well-run business.

Brady’s P/E ratio based on the next 12 months is 16.6x. Looking at the business services space right now, Brady trades at a compelling valuation. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $96 on the company (compared to the current share price of $84.34), implying they see 13.8% upside in buying Brady in the short term.