Sprinklr (CXM)

Sprinklr is in for a bumpy ride. Its weak revenue growth and gross margin show it not only lacks demand but also decent unit economics.― StockStory Analyst Team

1. News

2. Summary

Why We Think Sprinklr Will Underperform

With a proprietary AI engine processing 450 million data points daily across 30+ digital channels, Sprinklr (NYSE:CXM) provides cloud-based software that helps large enterprises manage customer experiences across social, messaging, chat, and voice channels.

- Estimated sales growth of 1.5% for the next 12 months implies demand will slow from its two-year trend

- Customers had second thoughts about committing to its platform over the last year as its average billings growth of 6% underwhelmed

- Operating profits increased over the last year as the company gained some leverage on its fixed costs and became more efficient

Sprinklr’s quality is lacking. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than Sprinklr

At $5.85 per share, Sprinklr trades at 1.7x forward price-to-sales. Sprinklr’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Sprinklr (CXM) Research Report: Q4 CY2025 Update

Customer experience management platform Sprinklr (NYSE:CXM) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 8.9% year on year to $220.6 million. The company expects next quarter’s revenue to be around $216 million, close to analysts’ estimates. Its non-GAAP profit of $0.13 per share was 34.7% above analysts’ consensus estimates.

Sprinklr (CXM) Q4 CY2025 Highlights:

- Revenue: $220.6 million vs analyst estimates of $216.9 million (8.9% year-on-year growth, 1.7% beat)

- Adjusted EPS: $0.13 vs analyst estimates of $0.10 (34.7% beat)

- Adjusted Operating Income: $37.73 million vs analyst estimates of $28.99 million (17.1% margin, 30.1% beat)

- Revenue Guidance for Q1 CY2026 is $216 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2027 is $0.48 at the midpoint, in line with analyst estimates

- Operating Margin: 6.4%, up from 5.2% in the same quarter last year

- Free Cash Flow Margin: 7.2%, similar to the previous quarter

- Market Capitalization: $1.39 billion

Company Overview

With a proprietary AI engine processing 450 million data points daily across 30+ digital channels, Sprinklr (NYSE:CXM) provides cloud-based software that helps large enterprises manage customer experiences across social, messaging, chat, and voice channels.

Sprinklr's unified platform is organized into four main product suites: Service, Social, Insights, and Marketing. The Service suite enables businesses to provide omnichannel customer support across voice, digital, and social channels. The Social suite helps manage social media publishing and engagement with governance controls. The Insights suite offers AI-powered analytics to track customer sentiment, brand reputation, and competitive benchmarking. The Marketing suite streamlines campaign planning, content creation, and social advertising.

What differentiates Sprinklr is its AI technology, which processes unstructured data like text, images, and video from digital channels. For example, a global hotel chain might use Sprinklr to monitor guest comments across review sites, respond to social media inquiries, analyze sentiment trends, and deliver personalized marketing—all within one platform instead of using multiple point solutions.

Sprinklr primarily targets large enterprises, with more than 60% of Fortune 100 companies among its customer base. The company monetizes through subscription-based pricing, with larger clients typically paying $1 million or more annually. Beyond software, Sprinklr offers professional services including implementation, training, and managed services to help customers maximize their platform investment.

The company has expanded internationally to serve customers in over 80 countries and supports more than 150 languages, making it suitable for global enterprises with complex, multi-market operations.

4. Customer Experience Software

The Internet has given customers more choice on whom to conduct business with and has also given them the power to easily share their experiences with other customers. These twin dynamics effectively have increased pressure on companies to both improve their customer service and also monitor their brand reputation online, driving the need for customer experience software offerings.

Sprinklr's competitors include customer experience platforms like Adobe Experience Cloud (NASDAQ: ADBE), Salesforce Service Cloud (NYSE: CRM), and Zendesk (private). In social media management, it competes with Hootsuite (private) and Khoros (private), while in contact center solutions, it faces competition from NICE (NASDAQ: NICE) and Genesys (private).

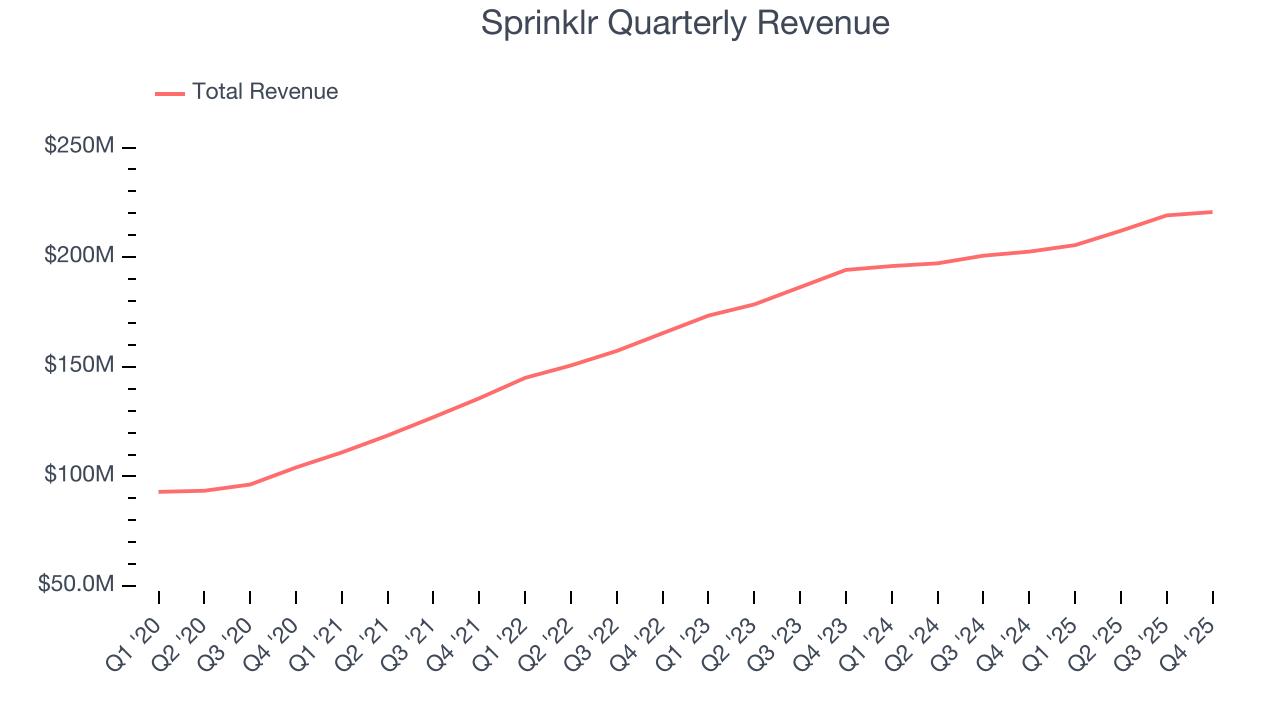

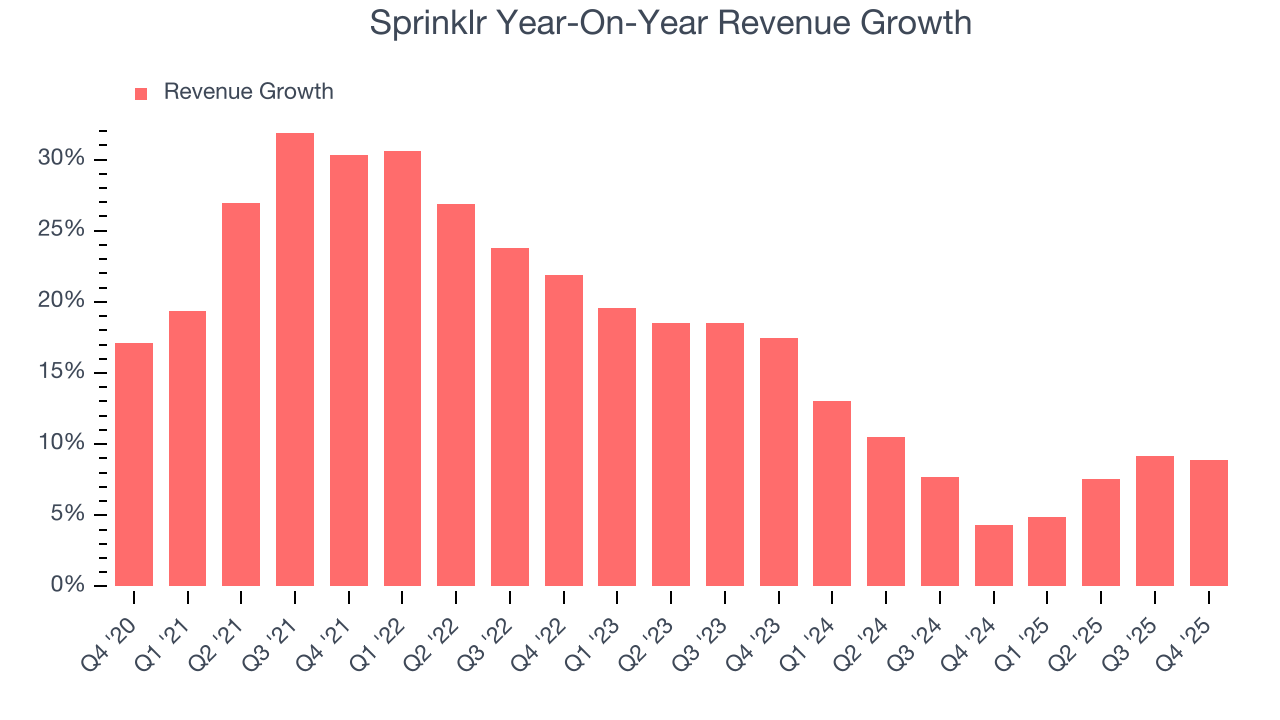

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Sprinklr grew its sales at a 17.2% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Sprinklr’s recent performance shows its demand has slowed as its annualized revenue growth of 8.2% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Sprinklr reported year-on-year revenue growth of 8.9%, and its $220.6 million of revenue exceeded Wall Street’s estimates by 1.7%. Company management is currently guiding for a 5.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.8% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

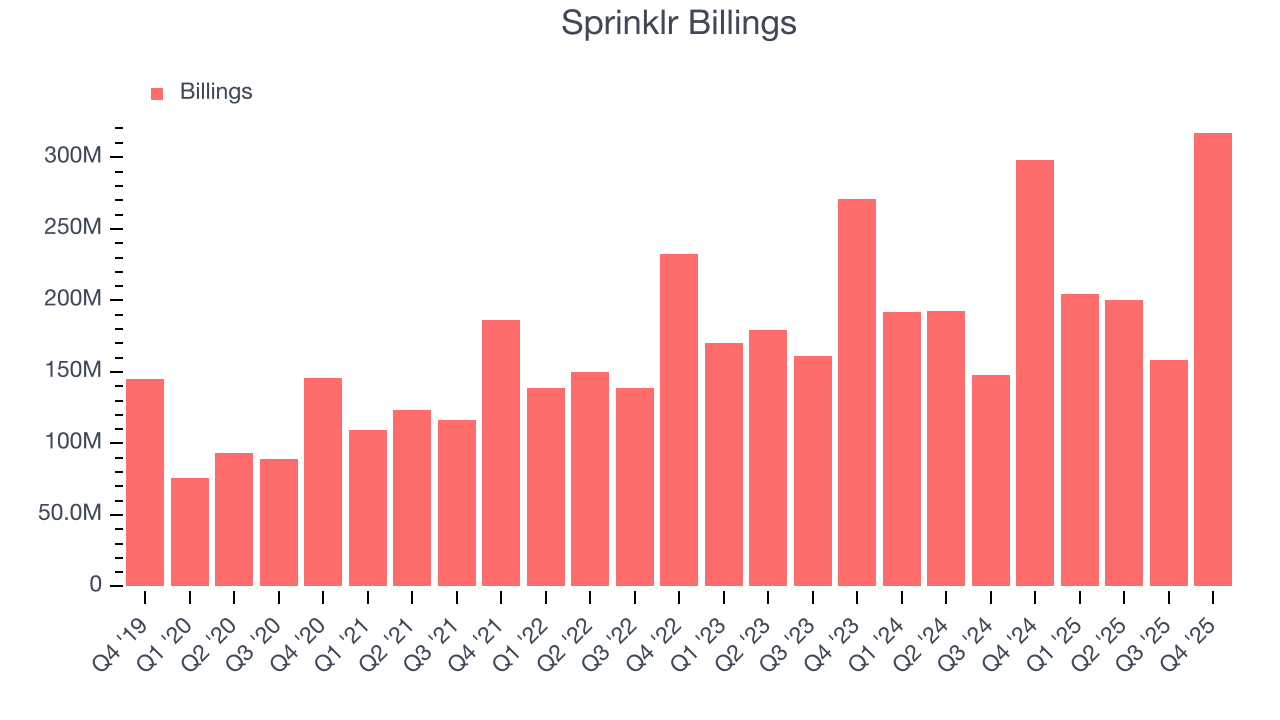

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Sprinklr’s billings came in at $317.4 million in Q4, and over the last four quarters, its growth was underwhelming as it averaged 6% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in acquiring/retaining customers.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for Sprinklr to acquire new customers as its CAC payback period checked in at 107.3 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

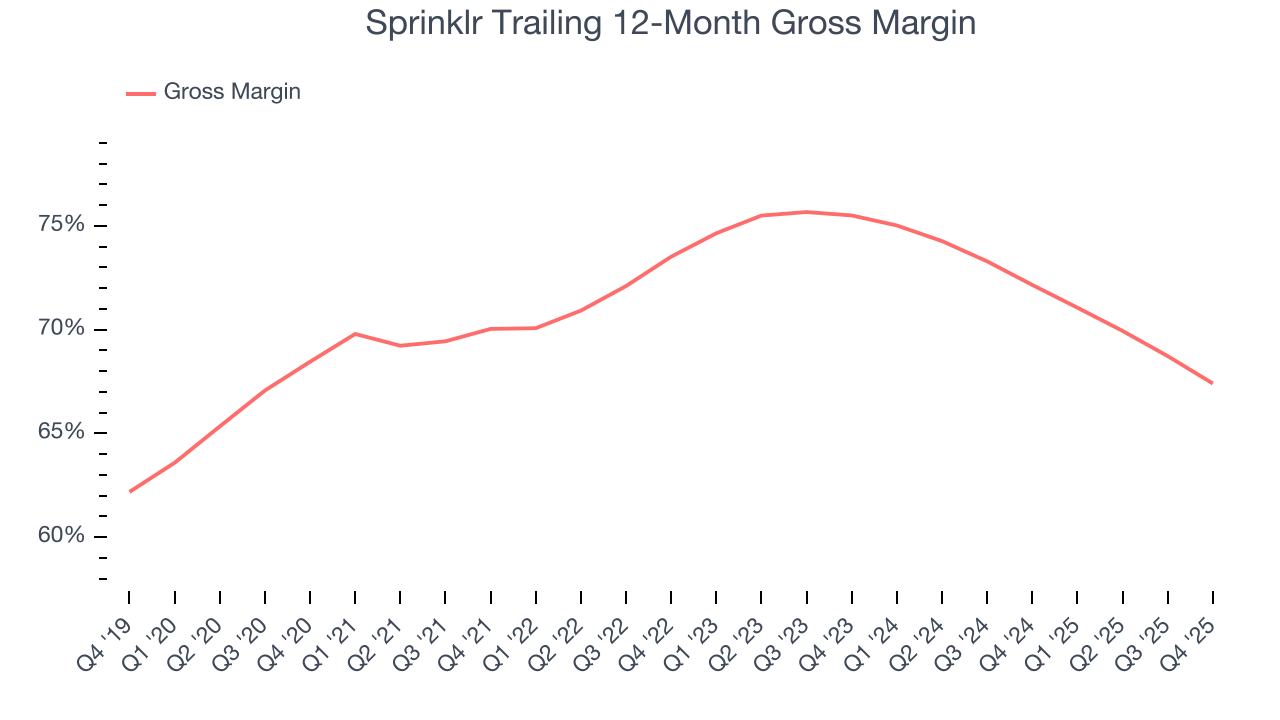

8. Gross Margin & Pricing Power

For software companies like Sprinklr, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Sprinklr’s gross margin is worse than the software industry average, giving it less room than its competitors to hire new talent that can expand its products and services. As you can see below, it averaged a 67.4% gross margin over the last year. Said differently, Sprinklr had to pay a chunky $32.60 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Sprinklr has seen gross margins decline by 8.1 percentage points over the last 2 year, which is among the worst in the software space.

This quarter, Sprinklr’s gross profit margin was 65.7% , marking a 5.3 percentage point decrease from 71% in the same quarter last year. Sprinklr’s full-year margin has also been trending down over the past 12 months, decreasing by 4.8 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs.

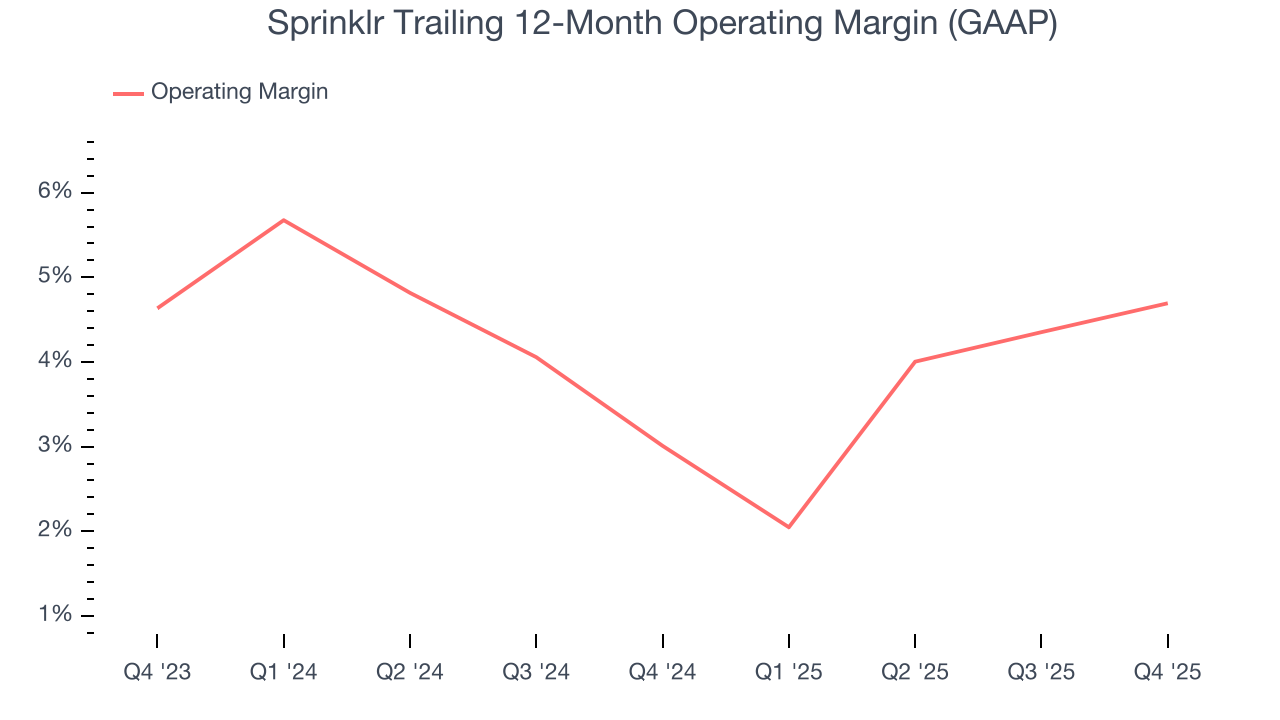

9. Operating Margin

Sprinklr has managed its cost base well over the last year. It demonstrated solid profitability for a software business, producing an average operating margin of 4.7%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Sprinklr’s operating margin rose by 1.7 percentage points over the last two years, as its sales growth gave it operating leverage.

This quarter, Sprinklr generated an operating margin profit margin of 6.4%, up 1.3 percentage points year on year. The increase was encouraging, and because its gross margin actually decreased, we can assume it was more efficient because its operating expenses like marketing, R&D, and administrative overhead grew slower than its revenue.

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

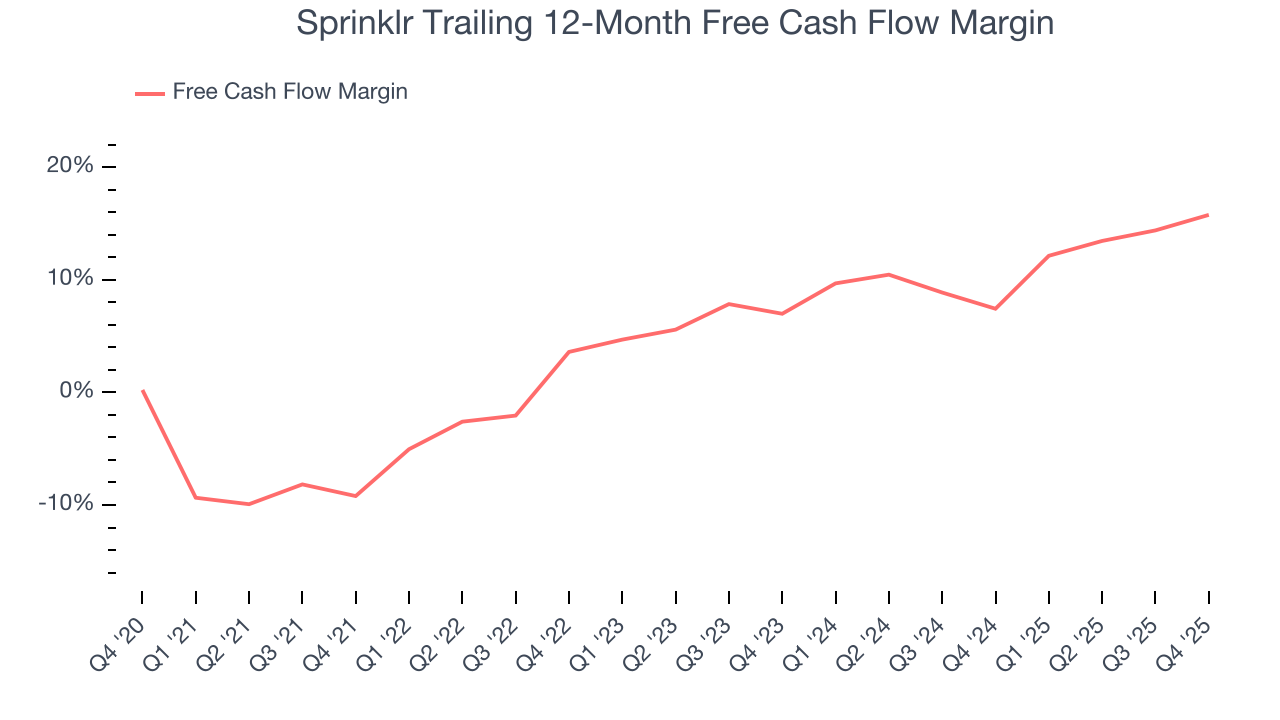

Sprinklr has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 15.8% over the last year, slightly better than the broader software sector.

Sprinklr’s free cash flow clocked in at $15.93 million in Q4, equivalent to a 7.2% margin. This result was good as its margin was 6.5 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Over the next year, analysts predict Sprinklr’s cash conversion will slightly improve. Their consensus estimates imply its free cash flow margin of 15.8% for the last 12 months will increase to 13.8%, giving it more flexibility for investments, share buybacks, and dividends.

11. Balance Sheet Assessment

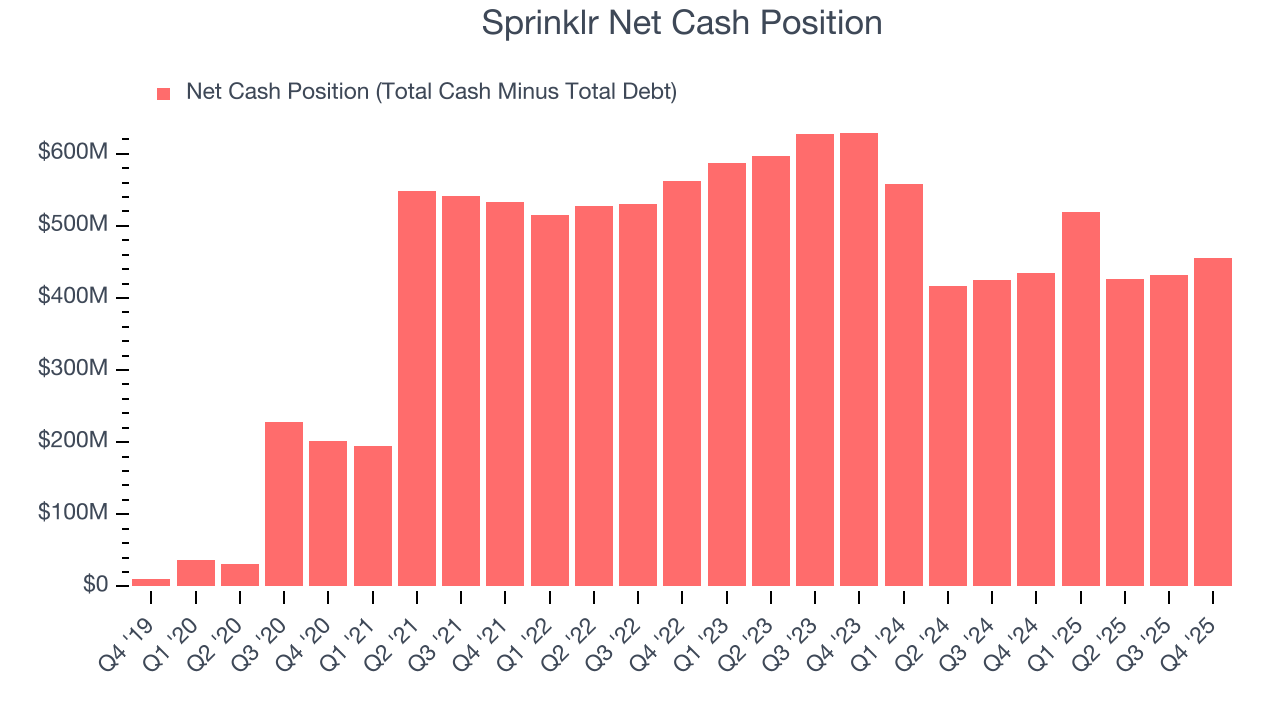

Companies with more cash than debt have lower bankruptcy risk.

Sprinklr is a profitable, well-capitalized company with $502.5 million of cash and $46.73 million of debt on its balance sheet. This $455.8 million net cash position is 31% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Sprinklr’s Q4 Results

It was encouraging to see Sprinklr beat analysts’ revenue expectations this quarter. Adjusted operating also nicely exceeded expectations. Looking ahead, Q1 revenue guidance and full-year EPS guidance were both roughly in line with Wall Street’s estimates. Overall, this was a decent quarter. The stock traded up 4.6% to $5.88 immediately following the results.

13. Is Now The Time To Buy Sprinklr?

Updated: March 14, 2026 at 10:31 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Sprinklr.

Sprinklr falls short of our quality standards. To kick things off, its revenue growth was mediocre over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its operating margins are in line with the overall software sector, the downside is its expanding operating margin shows it’s becoming more efficient at building and selling its software. On top of that, its gross margins show its business model is much less lucrative than other companies.

Sprinklr’s price-to-sales ratio based on the next 12 months is 1.7x. This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $8.88 on the company (compared to the current share price of $5.85).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.