Ellington Financial (EFC)

Ellington Financial is up against the odds. Its weak returns on capital suggest it doesn’t generate sufficient profits, a sign of value destruction.― StockStory Analyst Team

1. News

2. Summary

Why We Think Ellington Financial Will Underperform

Operating under the guidance of Ellington Management Group, a respected name in structured credit markets, Ellington Financial (NYSE:EFC) acquires and manages a diverse portfolio of mortgage-related, consumer-related, and other financial assets to generate returns for investors.

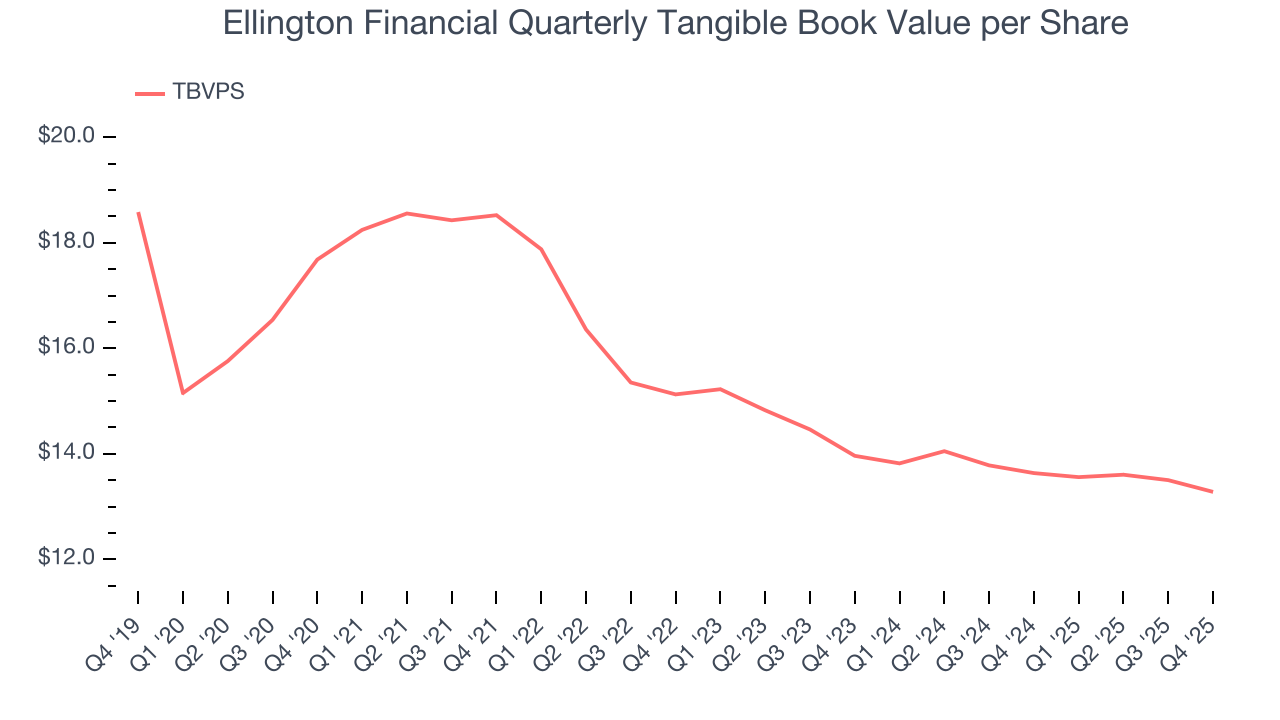

- Tangible book value per share tumbled by 5.6% annually over the last five years, showing banking sector trends are working against its favor during this cycle

- Annual earnings per share growth of 2.7% underperformed its revenue over the last five years, showing its incremental sales were less profitable

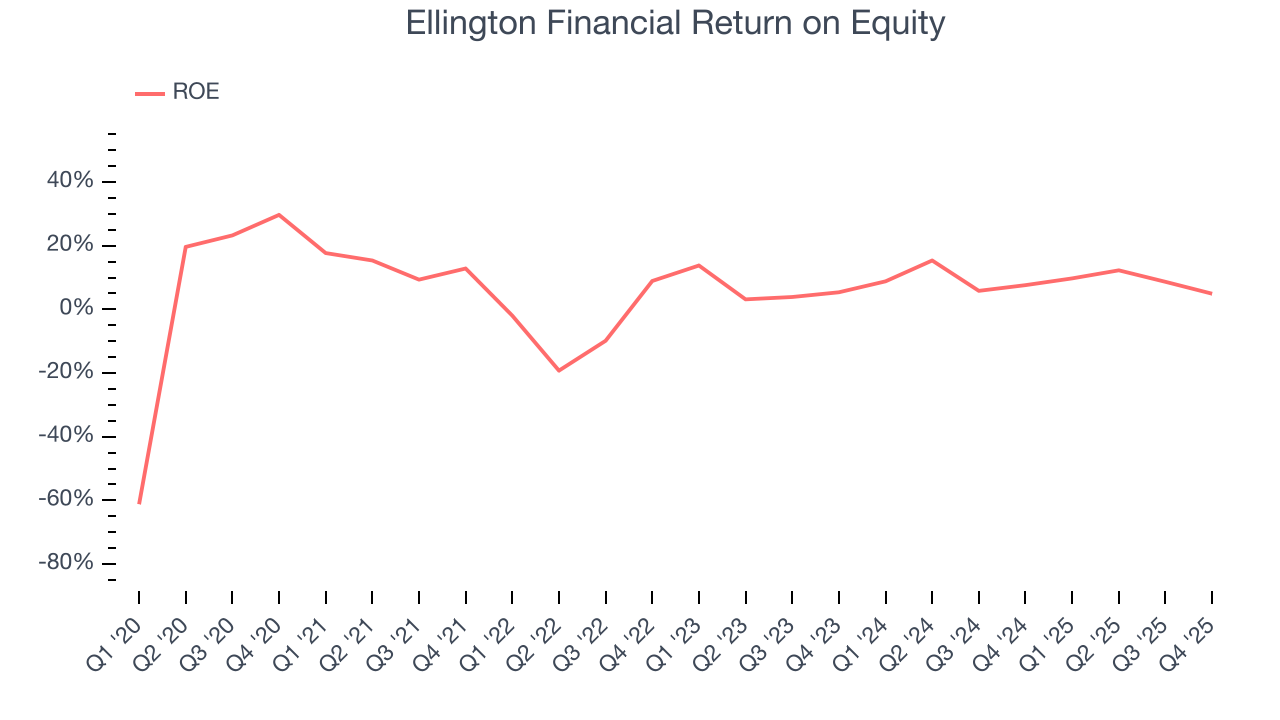

- Underwhelming 6.6% return on equity reflects management’s difficulties in finding profitable growth opportunities

Ellington Financial doesn’t fulfill our quality requirements. We’ve identified better opportunities elsewhere.

Why There Are Better Opportunities Than Ellington Financial

Ellington Financial’s stock price of $11.99 implies a valuation ratio of 0.9x forward P/B. Ellington Financial’s valuation may seem like a bargain, especially when stacked up against other banking companies. We remind you that you often get what you pay for, though.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Ellington Financial (EFC) Research Report: Q4 CY2025 Update

Mortgage investment firm Ellington Financial (NYSE:EFC) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 8.6% year on year to $65.81 million. Its non-GAAP profit of $0.47 per share was 2.4% above analysts’ consensus estimates.

Ellington Financial (EFC) Q4 CY2025 Highlights:

- Net Interest Income: $53.64 million vs analyst estimates of $56.26 million (13.7% year-on-year decline, 4.7% miss)

- Net Interest Margin: 3.4% vs analyst estimates of 1.2% (220 basis point beat)

- Revenue: $65.81 million vs analyst estimates of $90.74 million (8.6% year-on-year decline, 27.5% miss)

- Adjusted EPS: $0.47 vs analyst estimates of $0.46 (2.4% beat)

- Tangible Book Value per Share: $13.28 (2.6% year-on-year decline)

- Market Capitalization: $1.56 billion

Company Overview

Operating under the guidance of Ellington Management Group, a respected name in structured credit markets, Ellington Financial (NYSE:EFC) acquires and manages a diverse portfolio of mortgage-related, consumer-related, and other financial assets to generate returns for investors.

Ellington Financial operates through two main segments: the Investment Portfolio Segment and the Longbridge Segment. The Investment Portfolio Segment focuses on acquiring various types of loans and securities, including residential and commercial mortgage loans, mortgage-backed securities, consumer loans, and corporate debt. The company targets both government-guaranteed assets (like Agency RMBS) and non-guaranteed investments (such as non-QM loans and non-Agency RMBS), allowing it to diversify across risk profiles.

The Longbridge Segment, which became part of Ellington Financial through a controlling stake acquisition in 2022, specializes in reverse mortgages. Longbridge originates, purchases, sells, and services Home Equity Conversion Mortgage (HECM) loans, which are FHA-insured reverse mortgages designed for seniors. It also offers proprietary jumbo reverse mortgage products for high-value properties exceeding FHA limits. As an approved issuer of HMBS (HECM Mortgage-Backed Securities), Longbridge can securitize these loans, creating additional revenue streams.

Ellington Financial's business model involves identifying value opportunities across various asset classes. For example, the company might purchase non-performing residential mortgage loans at a discount, work to resolve them through modification or foreclosure, and then either sell the performing loans or foreclosed properties. Similarly, with consumer loans, Ellington might invest in tranches of securitizations backed by these assets, earning income from the interest payments while managing the associated risks.

The company is externally managed by Ellington Financial Management LLC, giving it access to Ellington Management Group's expertise in mortgage securities and structured products. This external management structure is common among mortgage REITs and provides the company with specialized investment capabilities.

4. Thrifts & Mortgage Finance

Thrifts & Mortgage Finance institutions operate by accepting deposits and extending loans primarily for residential mortgages, earning revenue through interest rate spreads (difference between lending rates and borrowing costs) and origination fees. The industry benefits from demographic tailwinds as millennials enter prime homebuying age, technological advancements streamlining the loan approval process, and potential interest rate stabilization improving affordability. However, significant headwinds include net interest margin compression during rate volatility, increased competition from fintech disruptors offering digital-first experiences, mounting regulatory compliance costs, and potential housing market corrections that could impact loan portfolios and default rates.

Ellington Financial competes with other mortgage REITs such as Annaly Capital Management (NYSE:NLY), AGNC Investment Corp. (NASDAQ:AGNC), New Residential Investment Corp. (NYSE:NRZ), and PennyMac Mortgage Investment Trust (NYSE:PMT), as well as with broader financial institutions that invest in mortgage-related assets.

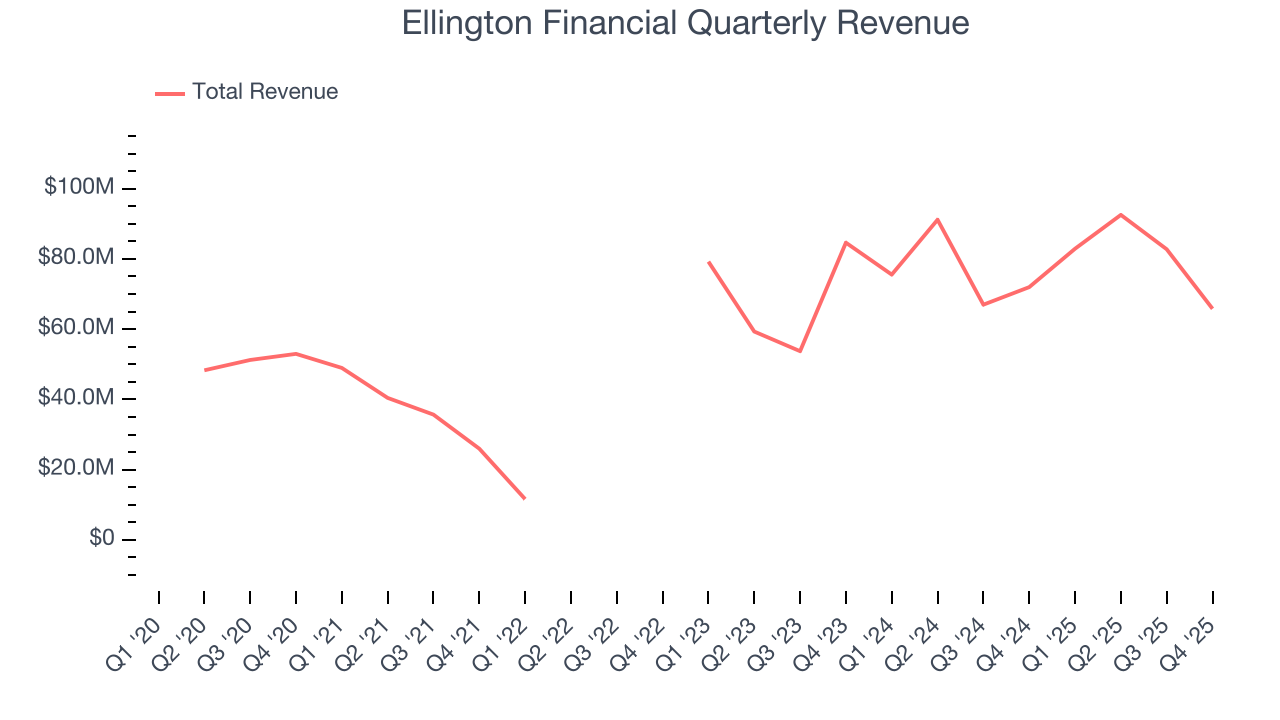

5. Sales Growth

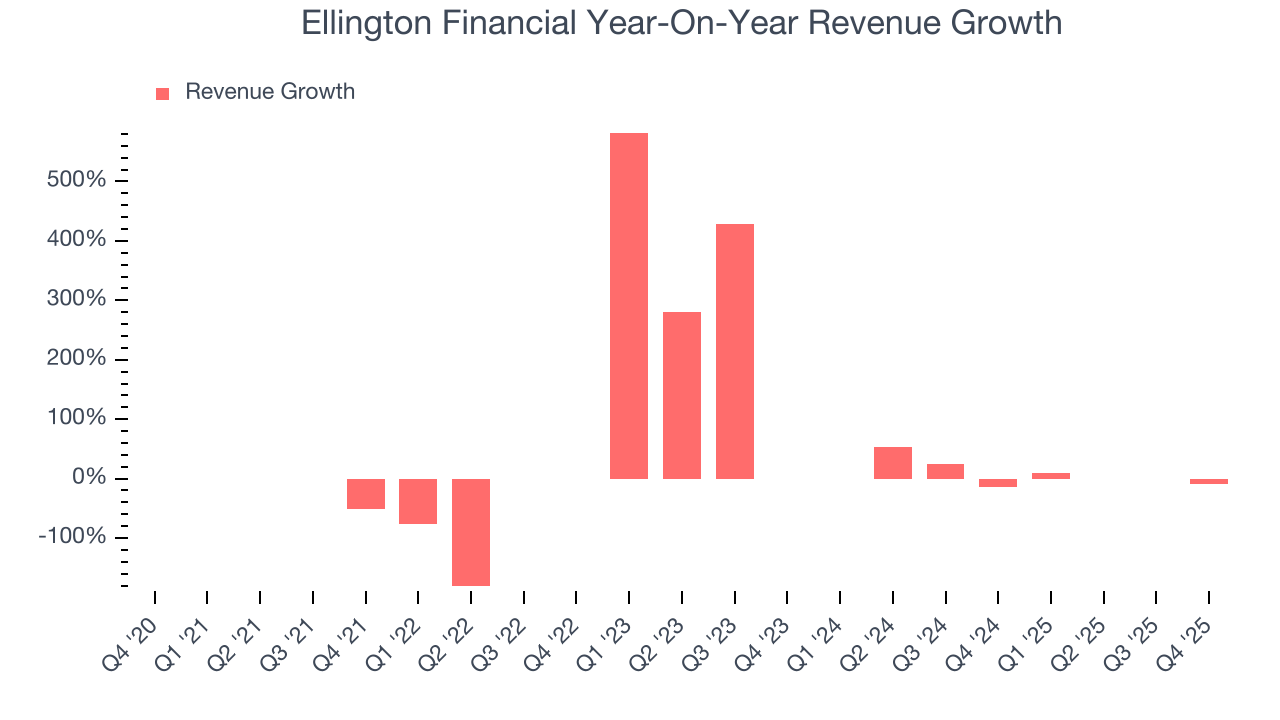

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Unfortunately, Ellington Financial’s 9.6% annualized revenue growth over the last five years was mediocre. This wasn’t a great result compared to the rest of the banking sector, but there are still things to like about Ellington Financial.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Ellington Financial’s recent performance shows its demand has slowed as its annualized revenue growth of 8.2% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Ellington Financial missed Wall Street’s estimates and reported a rather uninspiring 8.6% year-on-year revenue decline, generating $65.81 million of revenue.

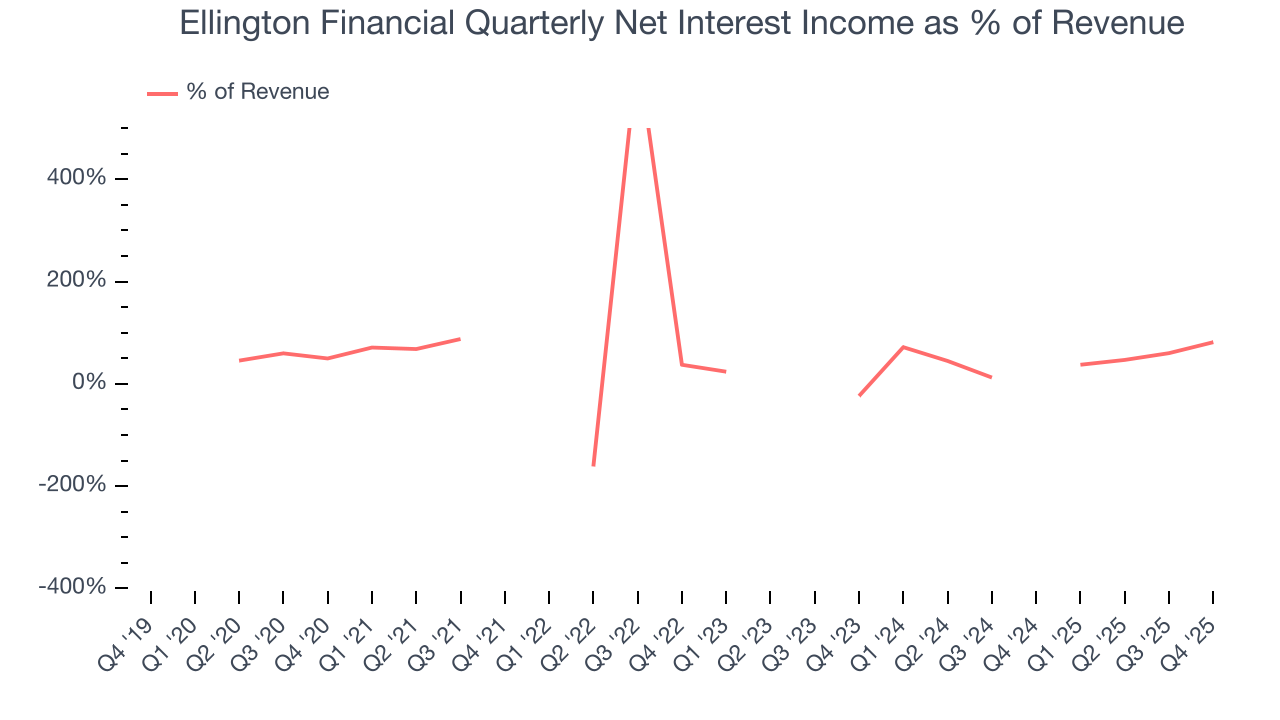

Since the company recorded losses on certain securities, it generated more net interest income than revenue (a 1.1x multiple of its revenue to be exact) during the last five years, meaning Ellington Financial lives and dies by its lending activities because non-interest income barely moves the needle.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Markets consistently prioritize net interest income growth over fee-based revenue, recognizing its superior quality and recurring nature compared to the more unpredictable non-interest income streams.

6. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

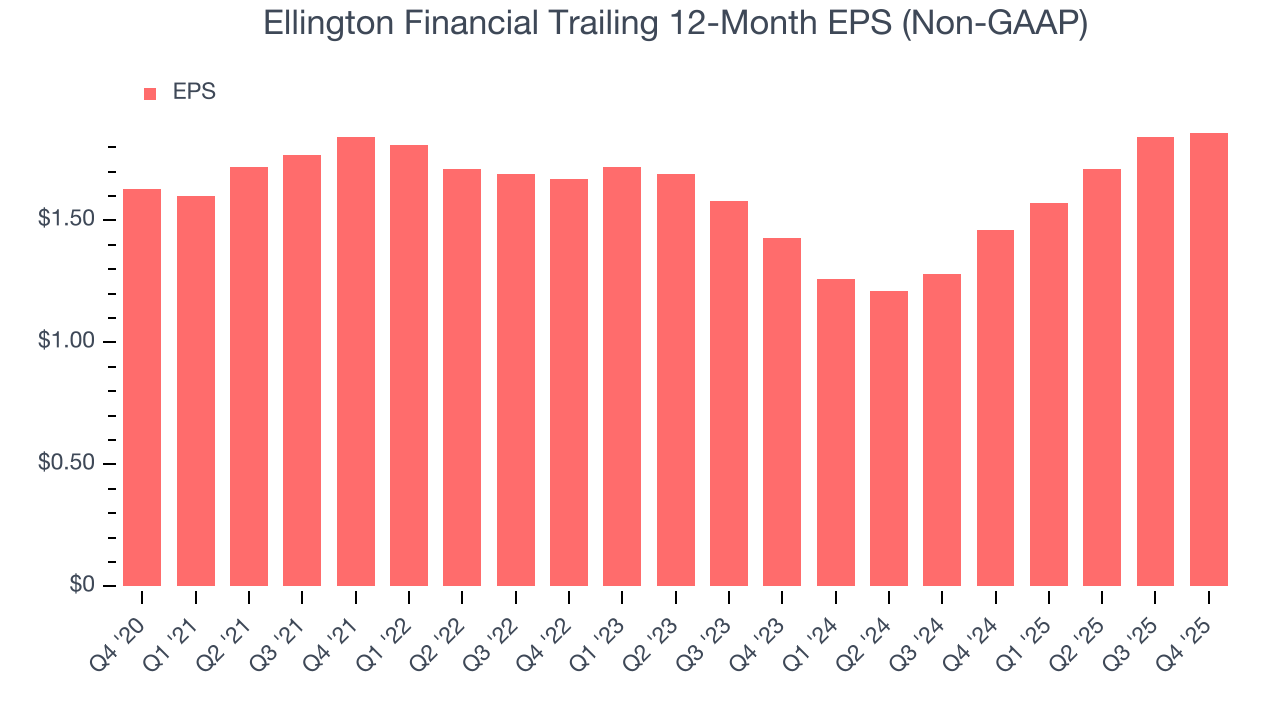

Ellington Financial’s EPS grew at a weak 2.7% compounded annual growth rate over the last five years, lower than its 9.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Ellington Financial, its two-year annual EPS growth of 14% was higher than its five-year trend. Accelerating earnings growth is almost always a great sign.

In Q4, Ellington Financial reported adjusted EPS of $0.47, up from $0.45 in the same quarter last year. This print beat analysts’ estimates by 2.4%. Over the next 12 months, Wall Street expects Ellington Financial’s full-year EPS of $1.86 to shrink by 2%.

7. Tangible Book Value Per Share (TBVPS)

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark. By excluding intangible assets with uncertain liquidation values, this metric captures real, liquid net worth per share. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to M&A or accounting rules allowing for loan losses to be spread out.

Ellington Financial’s TBVPS declined at a 5.6% annual clip over the last five years. On a two-year basis, TBVPS fell at a slower pace, dropping by 2.5% annually from $13.96 to $13.28 per share.

8. Return on Equity

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Ellington Financial has averaged an ROE of 6.6%, uninspiring for a company operating in a sector where the average shakes out around 7.5%. We’re optimistic Ellington Financial can turn the ship around given its success in other measures of financial health.

9. Key Takeaways from Ellington Financial’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its net interest income fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $12.50 immediately after reporting.

10. Is Now The Time To Buy Ellington Financial?

Updated: March 18, 2026 at 1:08 AM EDT

When considering an investment in Ellington Financial, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Ellington Financial falls short of our quality standards. Although its revenue growth was decent over the last five years and is expected to accelerate over the next 12 months, its TBVPS has declined over the last five years. And while the company’s estimated net interest income growth for the next 12 months is great, the downside is its weak EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders.

Ellington Financial’s P/B ratio based on the next 12 months is 0.9x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $14.63 on the company (compared to the current share price of $11.99).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.