Essent Group (ESNT)

We’re skeptical of Essent Group. Its sluggish sales growth shows demand is soft, a worrisome sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why We Think Essent Group Will Underperform

Serving as a crucial bridge between homebuyers and the American dream of homeownership, Essent Group (NYSE:ESNT) provides private mortgage insurance and title services that enable lenders to offer home loans with down payments of less than 20%.

- 2.7% annualized net premiums earned growth over the last five years lagged behind its insurance peers

- Estimated sales growth of 2.2% for the next 12 months implies demand will slow from its two-year trend

- One positive is that its pre-tax profits increased over the last five years as the company gained some leverage on its fixed costs and became more efficient

Essent Group’s quality is not up to our standards. We’re hunting for superior stocks elsewhere.

Why There Are Better Opportunities Than Essent Group

At $57.73 per share, Essent Group trades at 0.9x forward P/B. This multiple is lower than most insurance companies, but for good reason.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Essent Group (ESNT) Research Report: Q4 CY2025 Update

Mortgage insurance provider Essent Group (NYSE:ESNT) met Wall Street’s revenue expectations in Q4 CY2025, but sales were flat year on year at $312.4 million. Its GAAP profit of $1.60 per share was 8% below analysts’ consensus estimates.

Essent Group (ESNT) Q4 CY2025 Highlights:

- Net Premiums Earned: $212.7 million (13% year-on-year decline)

- Revenue: $312.4 million vs analyst estimates of $311.6 million (flat year on year, in line)

- Pre-tax Profit: $184.5 million (59.1% margin)

- EPS (GAAP): $1.60 vs analyst expectations of $1.74 (8% miss)

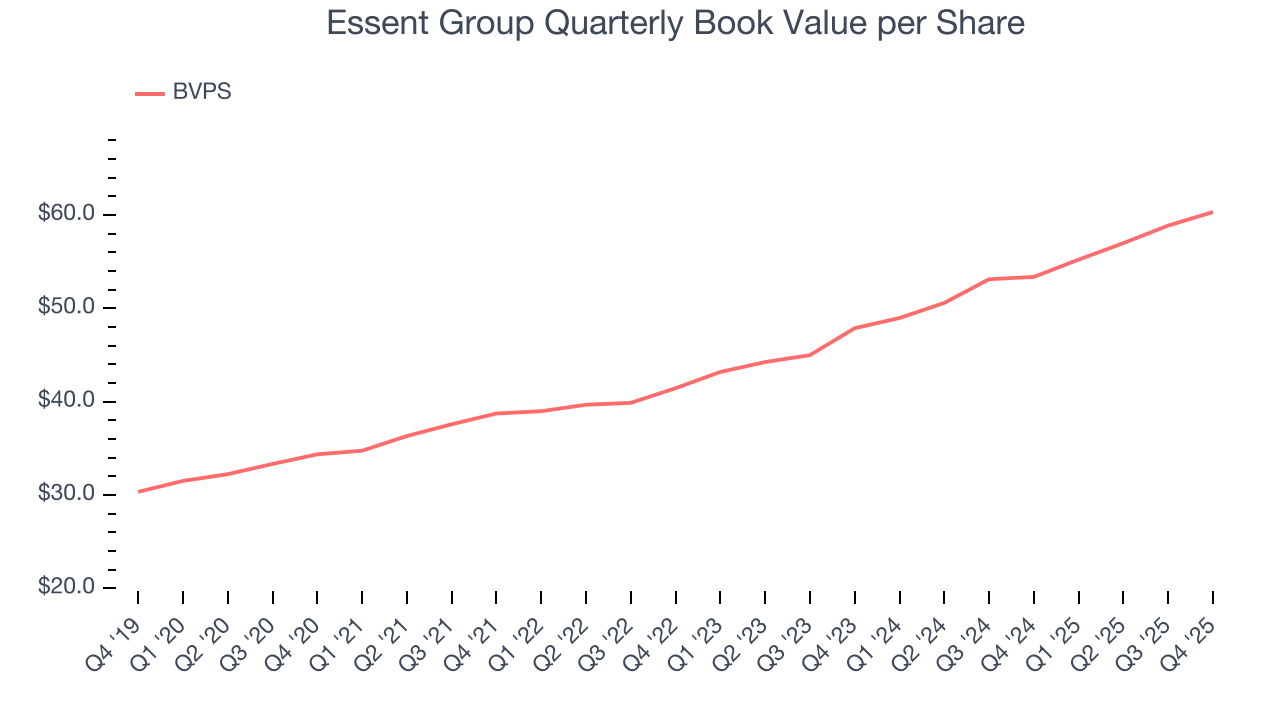

- Book Value per Share: $60.31 (13% year-on-year growth)

- Market Capitalization: $6.35 billion

Company Overview

Serving as a crucial bridge between homebuyers and the American dream of homeownership, Essent Group (NYSE:ESNT) provides private mortgage insurance and title services that enable lenders to offer home loans with down payments of less than 20%.

Essent's primary business revolves around protecting mortgage lenders against losses when borrowers default on loans with low down payments. When a homebuyer puts down less than 20% on a property, Fannie Mae and Freddie Mac (government-sponsored enterprises that purchase mortgages from lenders) require private mortgage insurance as protection. This insurance allows lenders to extend financing to borrowers who might otherwise be unable to purchase homes, while transferring a portion of the default risk to Essent.

The company offers several types of mortgage insurance products. Its main offering is primary mortgage insurance, which protects individual loans at specified coverage percentages determined by the lender or required by government-sponsored enterprises. Essent also provides pool insurance that offers additional credit enhancement for certain secondary market transactions by covering losses that exceed primary coverage limits.

Through its Bermuda-based subsidiary, Essent Reinsurance Ltd., the company participates in risk-sharing arrangements with government-sponsored enterprises and provides reinsurance services to other insurers. Following its 2023 acquisition of Agents National Title Insurance Company and Boston National Title, Essent expanded into title insurance and settlement services, which facilitate real estate transactions by ensuring clear property ownership.

Essent generates revenue primarily through insurance premiums, which can be structured as monthly payments or single upfront payments. The company maintains relationships with mortgage originators including banks, credit unions, and mortgage companies who integrate Essent's insurance into their lending processes.

4. Property & Casualty Insurance

Property & Casualty (P&C) insurers protect individuals and businesses against financial loss from damage to property or from legal liability. This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. On the other hand, P&C insurers face a major secular headwind from the increasing frequency and severity of catastrophe losses due to climate change. Furthermore, the liability side of the business is pressured by 'social inflation'—the trend of rising litigation costs and larger jury awards.

Essent Group competes with other private mortgage insurers such as MGIC Investment Corporation (NYSE:MTG), Radian Group (NYSE:RDN), and Enact Holdings (NASDAQ:ACT), as well as with government agencies like the Federal Housing Administration (FHA) that also provide mortgage insurance.

5. Revenue Growth

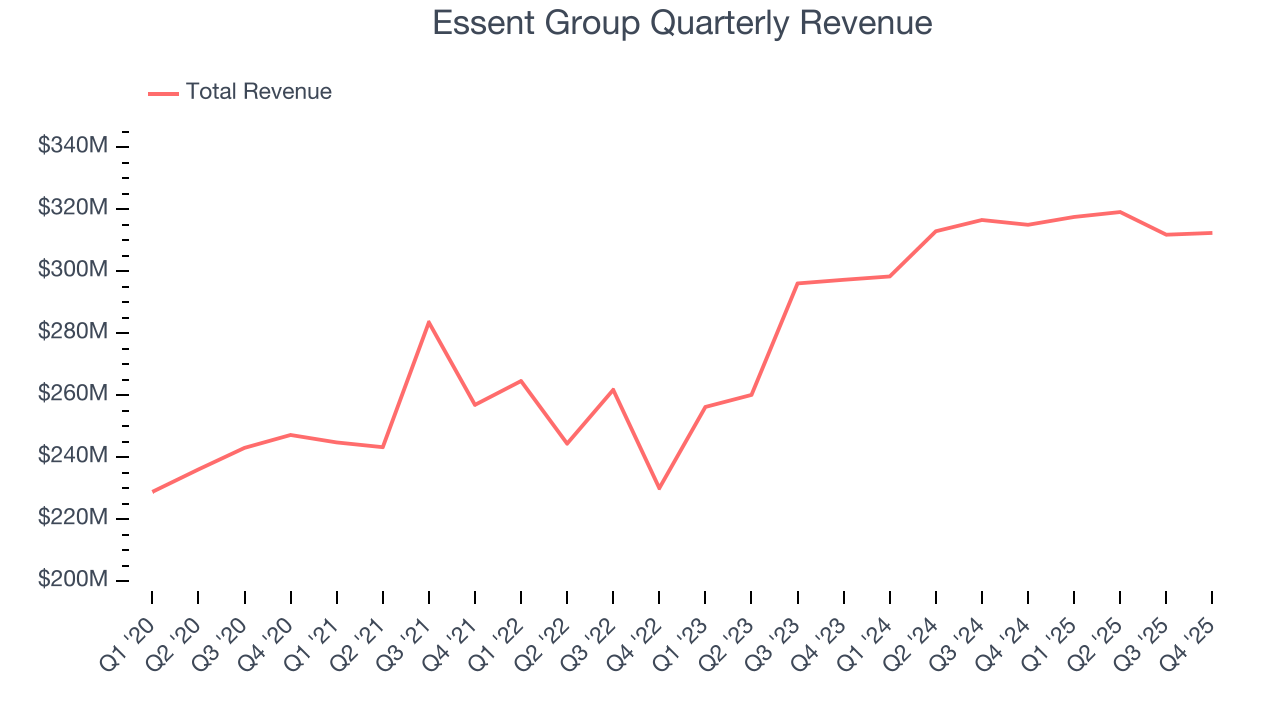

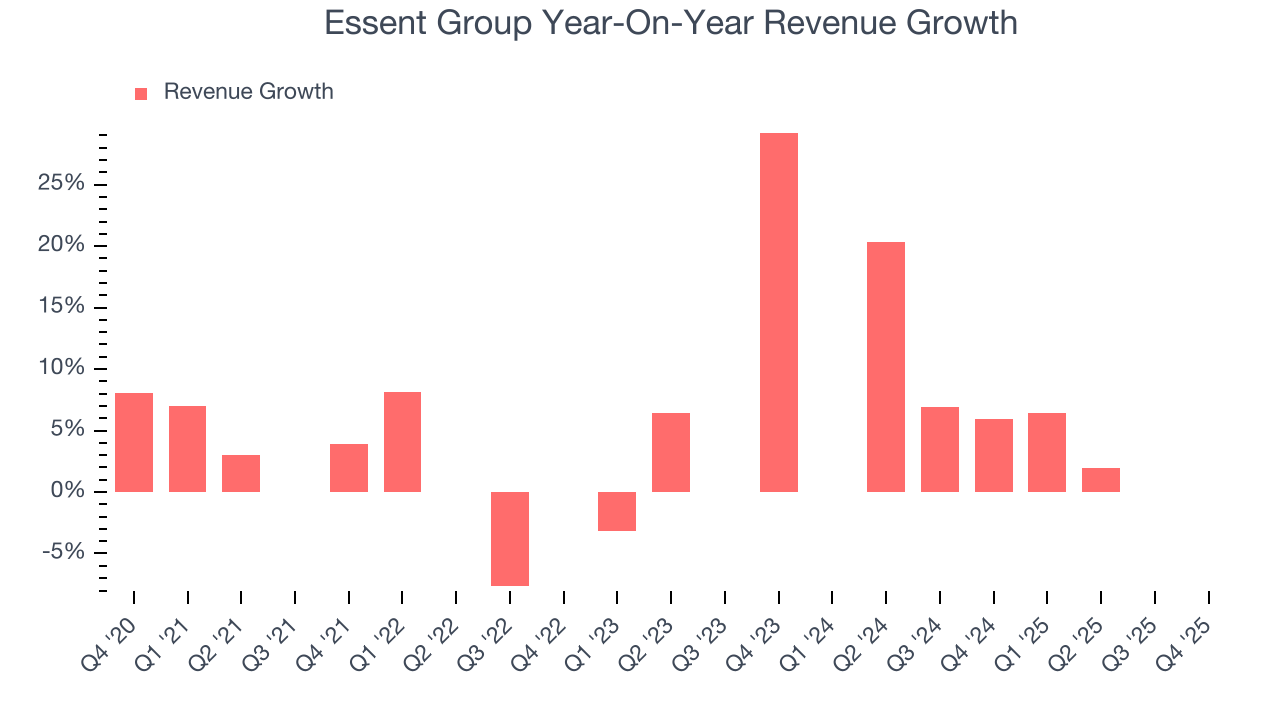

Insurers earn revenue three ways. The core insurance business itself, often called underwriting and represented in the income statement as premiums earned, is one way. Investment income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities is the second way. Fees from various sources such as policy administration, annuities, or other value-added services is the third. Unfortunately, Essent Group’s 5.7% annualized revenue growth over the last five years was tepid. This was below our standard for the insurance sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Essent Group’s annualized revenue growth of 6.6% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Essent Group’s $312.4 million of revenue was flat year on year and in line with Wall Street’s estimates.

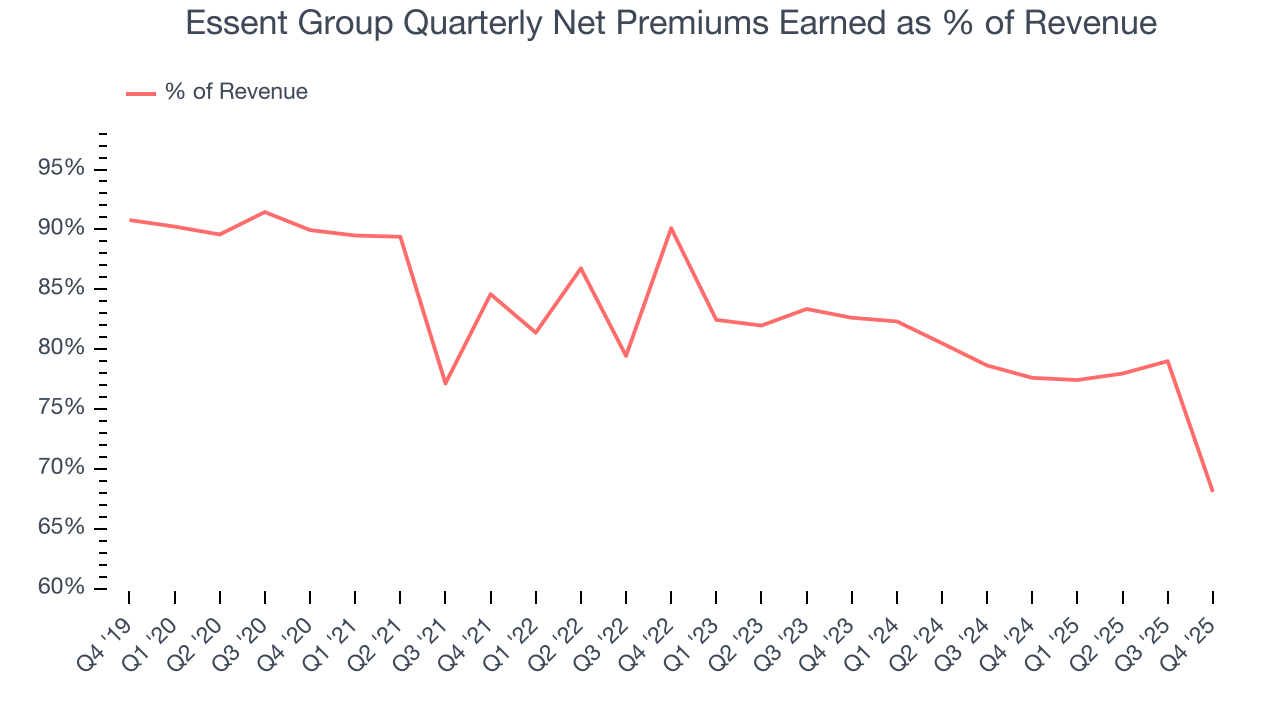

Net premiums earned made up 81.1% of the company’s total revenue during the last five years, meaning Essent Group barely relies on non-insurance activities to drive its overall growth.

Net premiums earned commands greater market attention due to its reliability and consistency, whereas investment and fee income are often seen as more volatile revenue streams that fluctuate with market conditions.

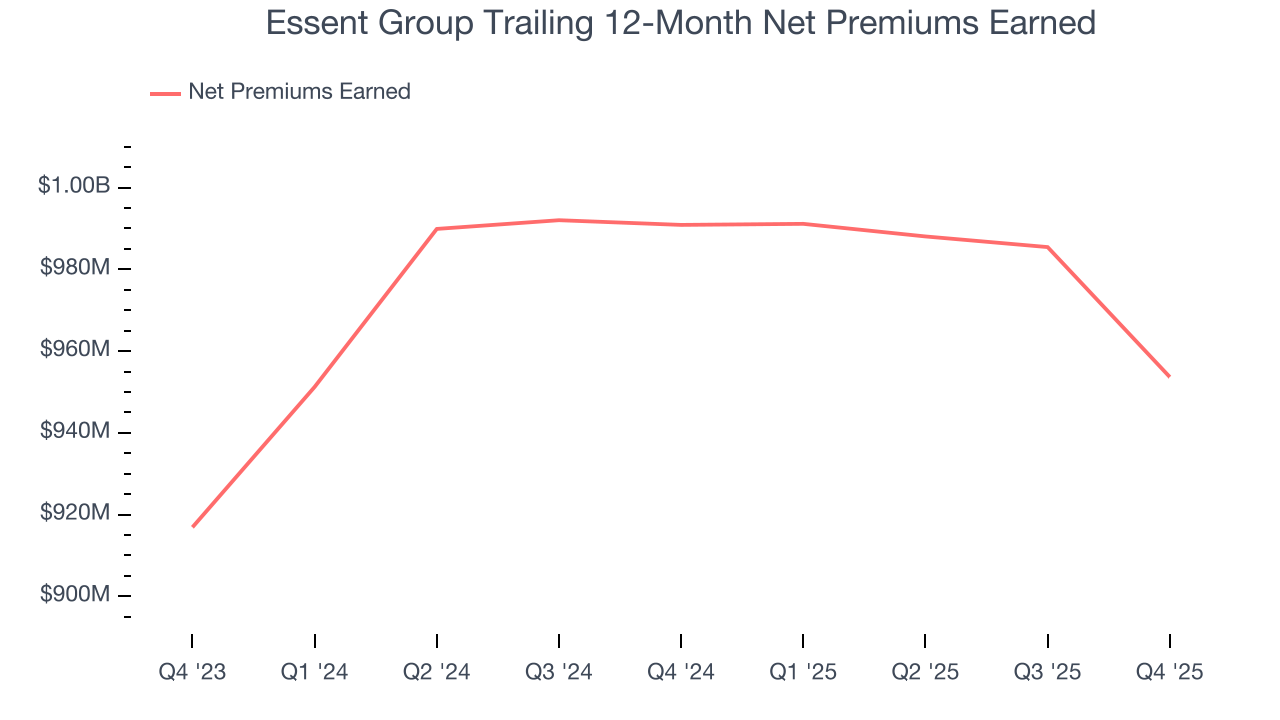

6. Net Premiums Earned

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are:

- Gross premiums - what’s ceded to reinsurers as a risk mitigation and transfer strategy

Essent Group’s net premiums earned has grown at a 2% annualized rate over the last five years, much worse than the broader insurance industry and slower than its total revenue.

When analyzing Essent Group’s net premiums earned over the last two years, we can paint a similar picture as it recorded an annual growth rate of 2%. Since two-year net premiums earned grew slower than total revenue over this period, it’s implied that other line items such as investment income grew at a faster rate. These extra revenue streams are important to the bottom line, yet their performance can be inconsistent. Some firms have been more successful and consistent in managing their float, but sharp fluctuations in the fixed income and equity markets can dramatically affect short-term results.

Essent Group’s net premiums earned came in at $212.7 million this quarter, down 13% year on year.

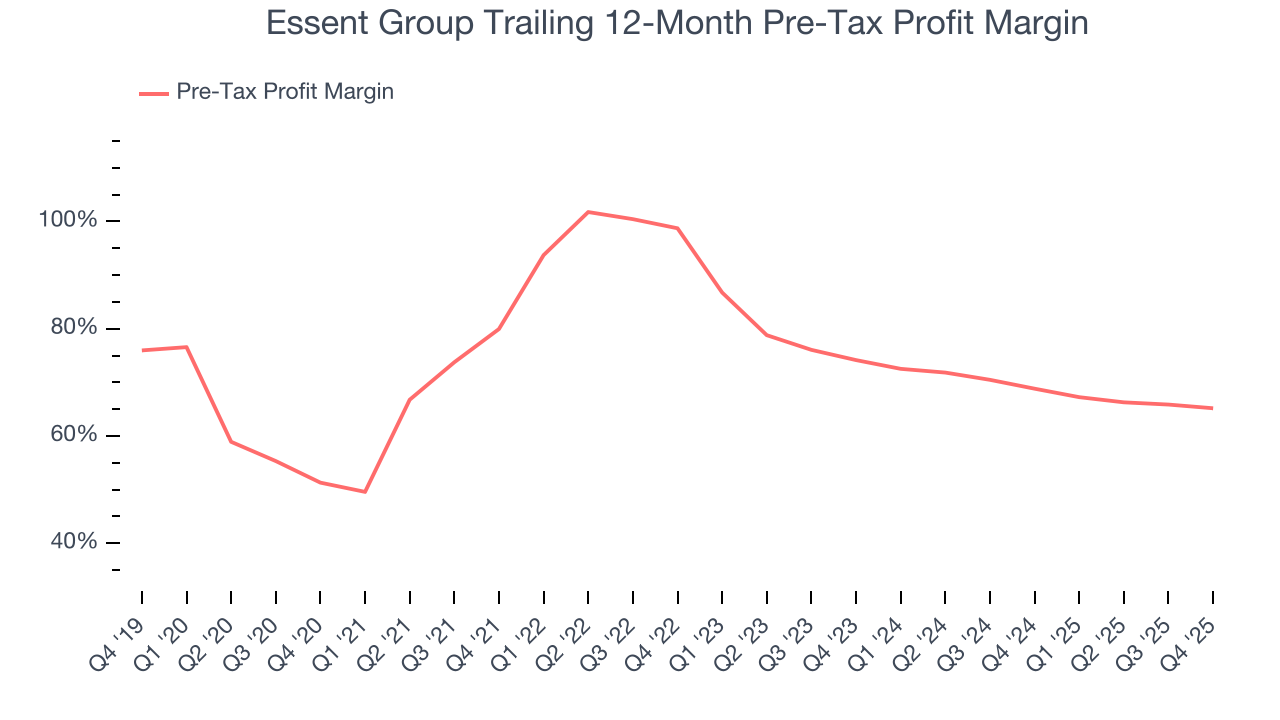

7. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

The economics of insurers are driven by their balance sheets, where assets (investing the float + premiums receivable) and liabilities (claims to pay) define the fundamentals. Interest income and expense should therefore be factored into the definition of profit but taxes - which are largely out of a company’s control - should not.

Over the last five years, Essent Group’s pre-tax profit margin has fallen by 13.9 percentage points, going from 80% to 65.2%. However, the company gave back some of its expense savings as its pre-tax profit margin declined by 9 percentage points on a two-year basis.

Essent Group’s pre-tax profit margin came in at 59.1% this quarter. This result was 2.8 percentage points worse than the same quarter last year.

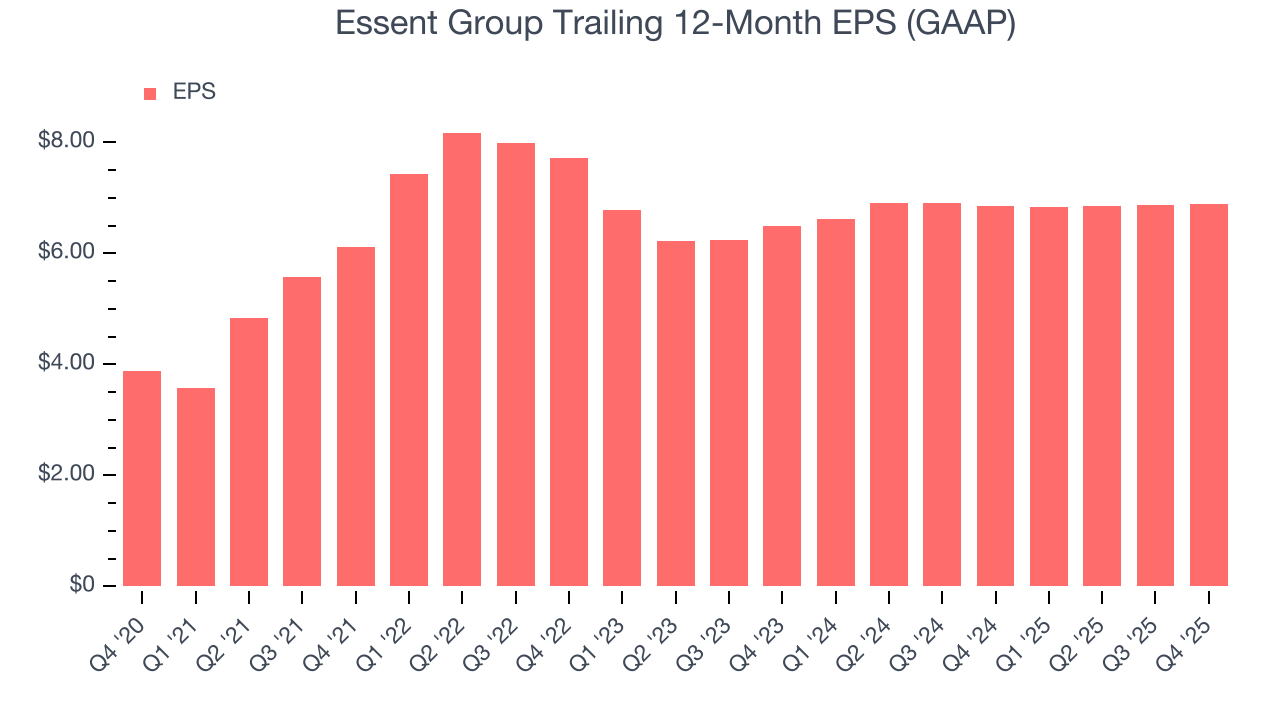

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Essent Group’s EPS grew at a decent 12.2% compounded annual growth rate over the last five years, higher than its 5.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

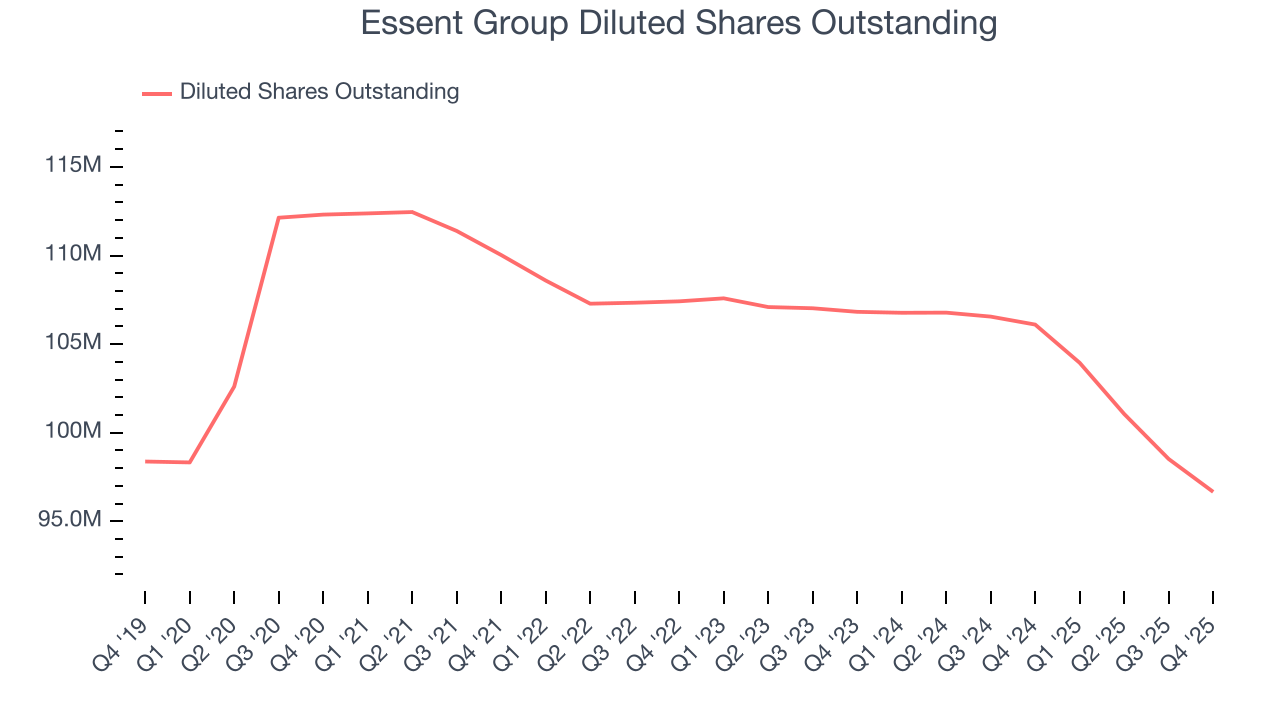

Diving into Essent Group’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Essent Group’s pre-tax profit margin declined this quarter but expanded by 13.9 percentage points over the last five years. Its share count also shrank by 13.9%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Essent Group, its two-year annual EPS growth of 2.9% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q4, Essent Group reported EPS of $1.60, up from $1.58 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Essent Group’s full-year EPS of $6.89 to grow 5.3%.

9. Book Value Per Share (BVPS)

Insurers are balance sheet businesses, collecting premiums upfront and paying out claims over time. Premiums collected but not yet paid out, often referred to as the float, are invested and create an asset base supported by a liability structure. Book value per share (BVPS) captures this dynamic by measuring these assets (investment portfolio, cash, reinsurance recoverables) less liabilities (claim reserves, debt, future policy benefits). BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality. While other (and more commonly known) per-share metrics like EPS can sometimes be lumpy due to reserve releases or one-time items and can be managed or skewed while still following accounting rules, BVPS reflects long-term capital growth and is harder to manipulate.

Essent Group’s BVPS grew at an impressive 11.9% annual clip over the last five years. The last two years show a similar trajectory as BVPS grew by 12.2% annually from $47.87 to $60.31 per share.

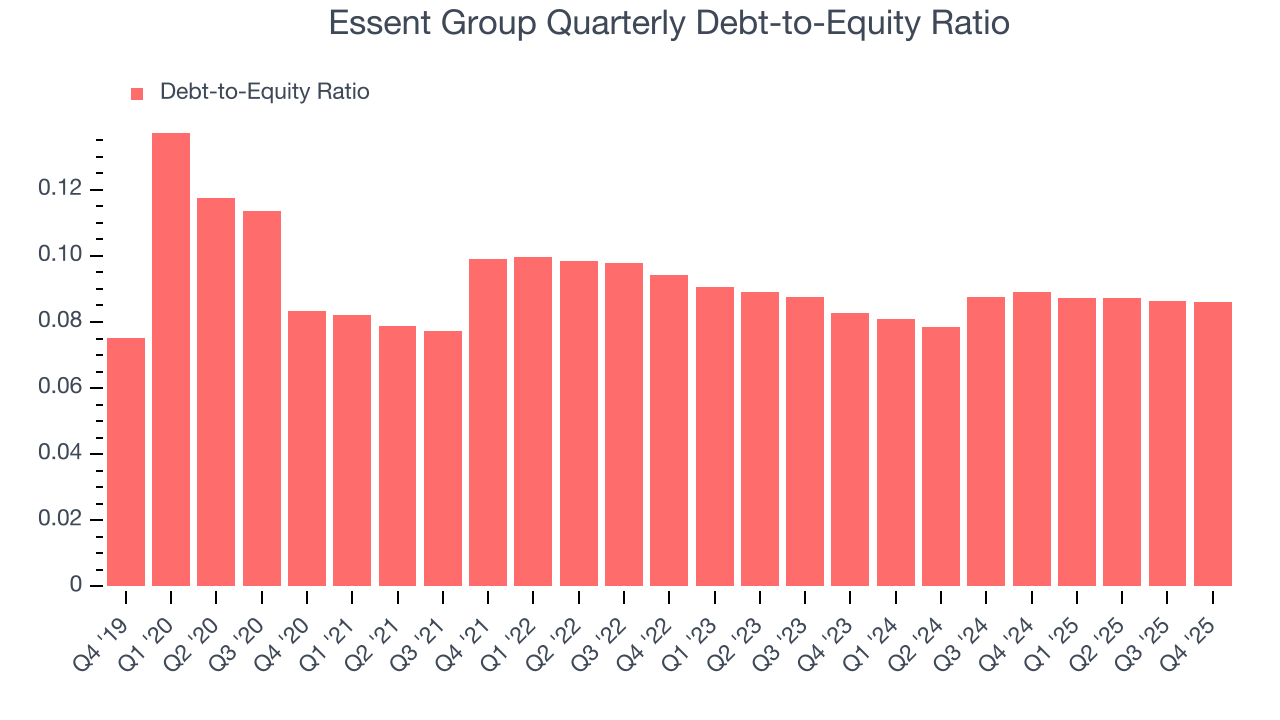

10. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Essent Group currently has $495.3 million of debt and $5.76 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0.1×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 1.0× for an insurance business. Anything below 0.5× is a bonus.

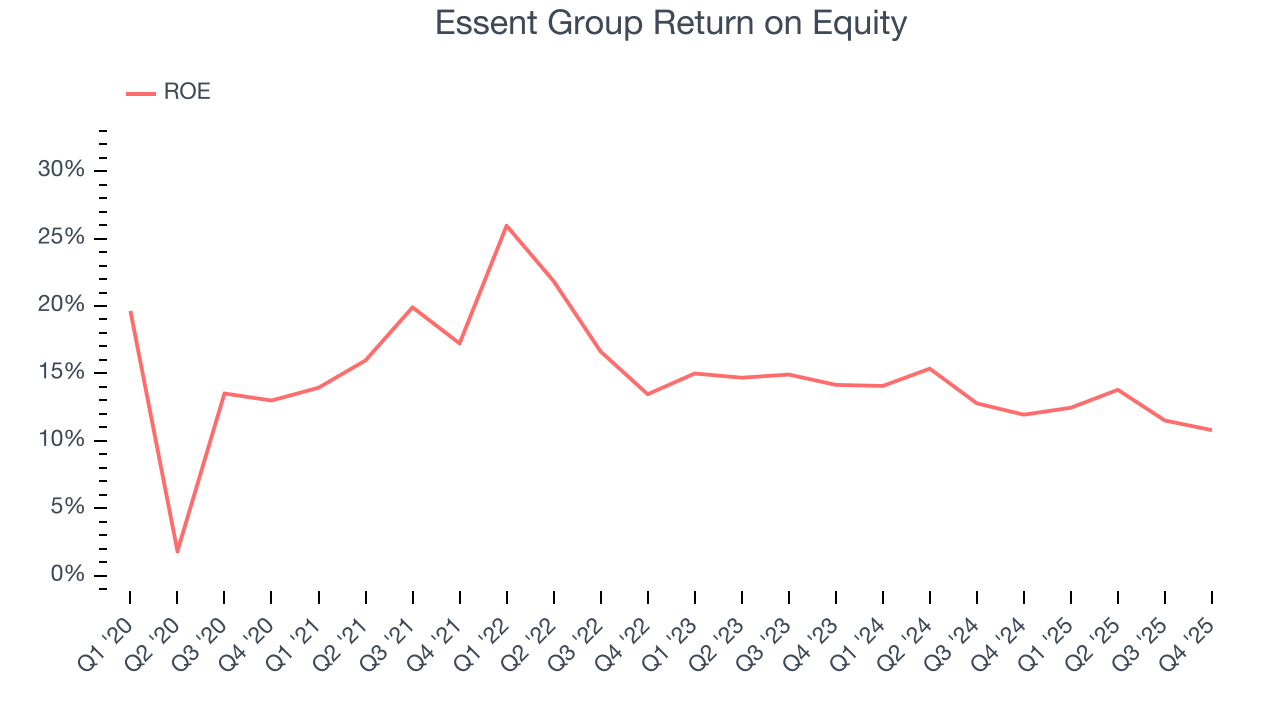

11. Return on Equity

Return on equity (ROE) is a crucial yardstick for insurance companies, measuring their ability to generate returns on the capital provided by shareholders. Insurers that consistently deliver superior ROE tend to create more value for their investors over time through strategic capital allocation and shareholder-friendly policies.

Over the last five years, Essent Group has averaged an ROE of 15.3%, healthy for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This is a bright spot for Essent Group.

12. Key Takeaways from Essent Group’s Q4 Results

We struggled to find many positives in these results. Overall, this was a softer quarter. The stock remained flat at $65.64 immediately following the results.

13. Is Now The Time To Buy Essent Group?

Updated: March 30, 2026 at 12:17 AM EDT

Are you wondering whether to buy Essent Group or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Essent Group isn’t a terrible business, but it isn’t one of our picks. To begin with, its revenue growth was uninspiring over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its expanding pre-tax profit margin shows the business has become more efficient, the downside is its net premiums earned growth was weak over the last five years. On top of that, its projected EPS for the next year is lacking.

Essent Group’s P/B ratio based on the next 12 months is 0.9x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $68.06 on the company (compared to the current share price of $57.73).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.