Flowserve (FLS)

Flowserve is interesting. Its rising free cash flow margin gives it more chips to play with.― StockStory Analyst Team

1. News

2. Summary

Why Flowserve Is Interesting

Manufacturing the largest pump ever built for nuclear power generation, Flowserve (NYSE:FLS) manufactures and sells flow control equipment for various industries.

- Incremental sales over the last five years boosted profitability as its annual earnings per share growth of 10.5% outstripped its revenue performance

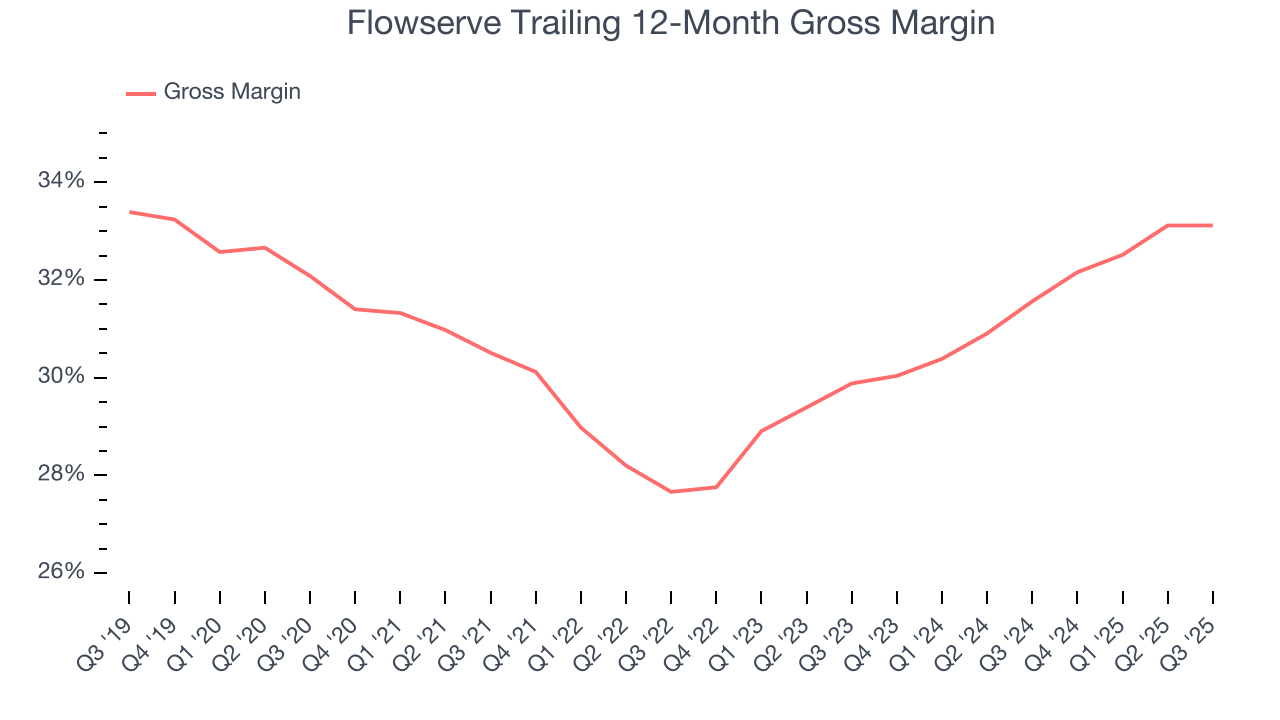

- Adequate gross margin of 30.8% gives it sufficient room to spend on marketing and product development

- One pitfall is its sales pipeline suggests its future revenue growth may not meet our standards as its average backlog growth of 1.2% for the past two years was weak

Flowserve has some noteworthy aspects. If you like the story, the price seems reasonable.

Why Is Now The Time To Buy Flowserve?

Flowserve is trading at $77.76 per share, or 20.2x forward P/E. The current valuation is below that of most industrials companies, but this isn’t a bargain. Instead, the price is appropriate for the quality you get.

If you think the market is undervaluing the company, now could be a good time to build a position.

3. Flowserve (FLS) Research Report: Q3 CY2025 Update

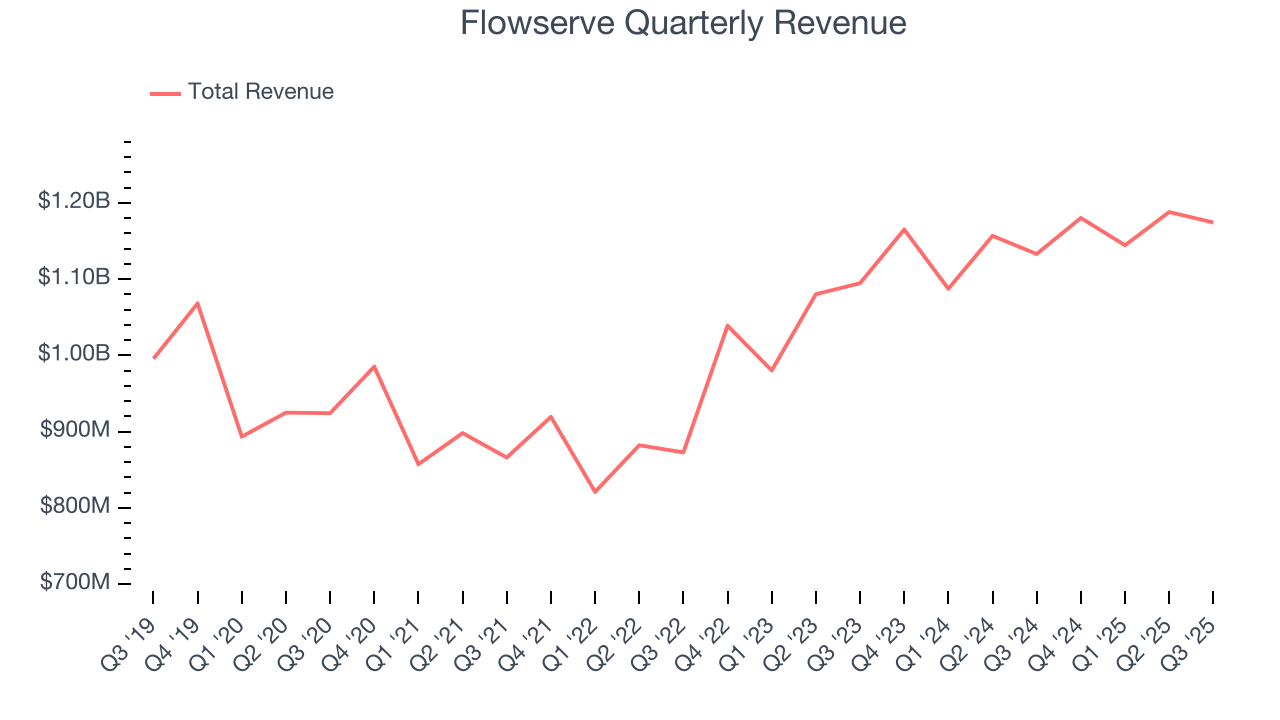

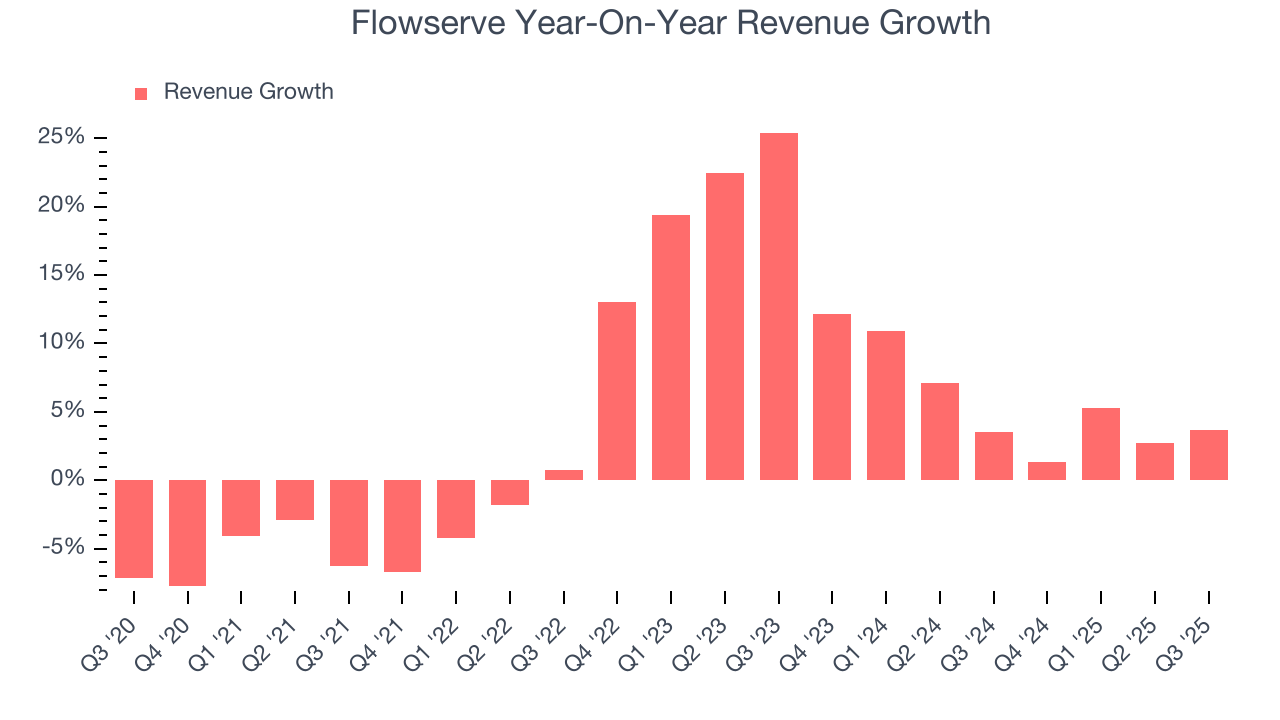

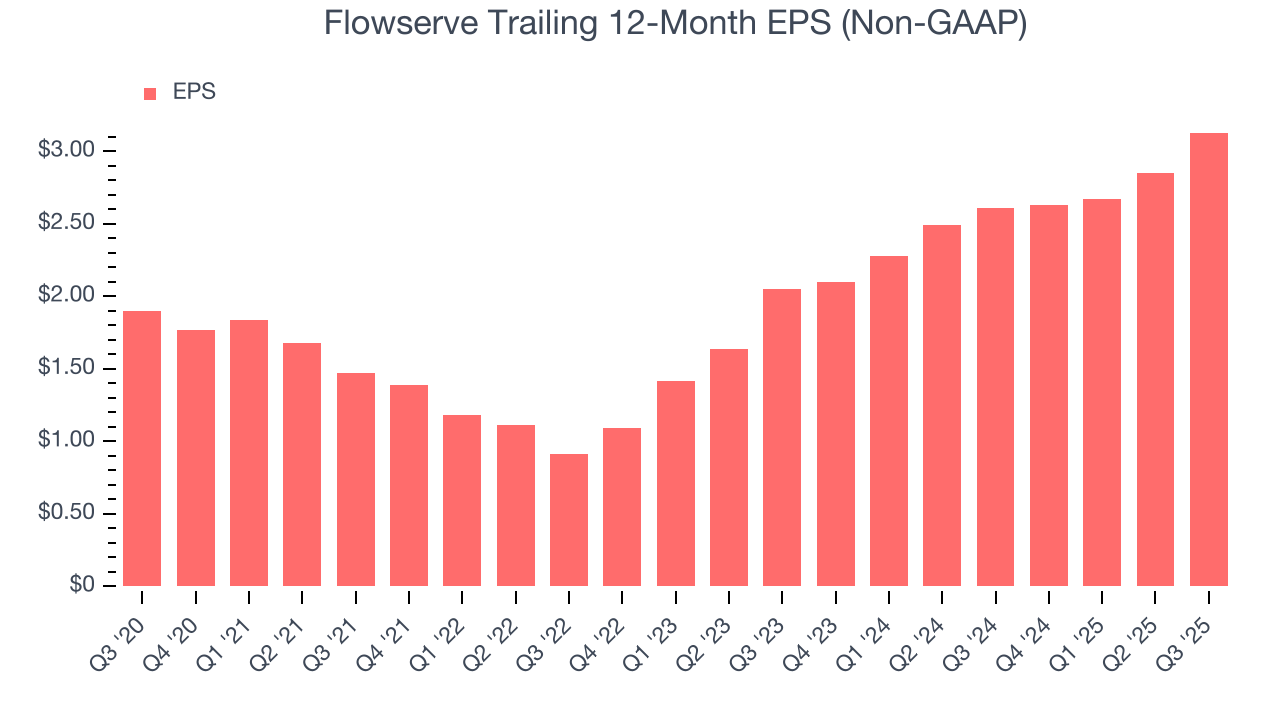

Flow control equipment manufacturer Flowserve (NYSE:FLS) missed Wall Street’s revenue expectations in Q3 CY2025 as sales rose 3.6% year on year to $1.17 billion. Its non-GAAP profit of $0.90 per share was 13.2% above analysts’ consensus estimates.

Flowserve (FLS) Q3 CY2025 Highlights:

- Revenue: $1.17 billion vs analyst estimates of $1.21 billion (3.6% year-on-year growth, 2.7% miss)

- Adjusted EPS: $0.90 vs analyst estimates of $0.80 (13.2% beat)

- Management raised its full-year Adjusted EPS guidance to $3.45 at the midpoint, a 3.8% increase

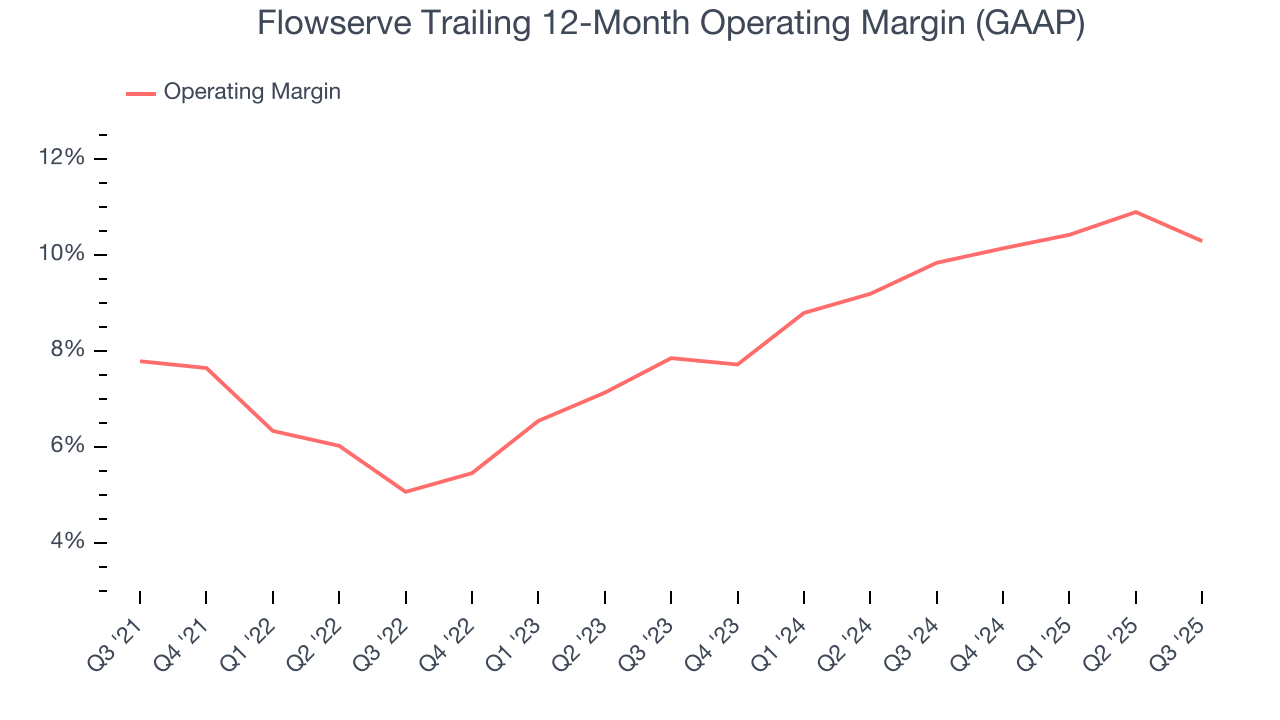

- Operating Margin: 6.7%, down from 9.1% in the same quarter last year

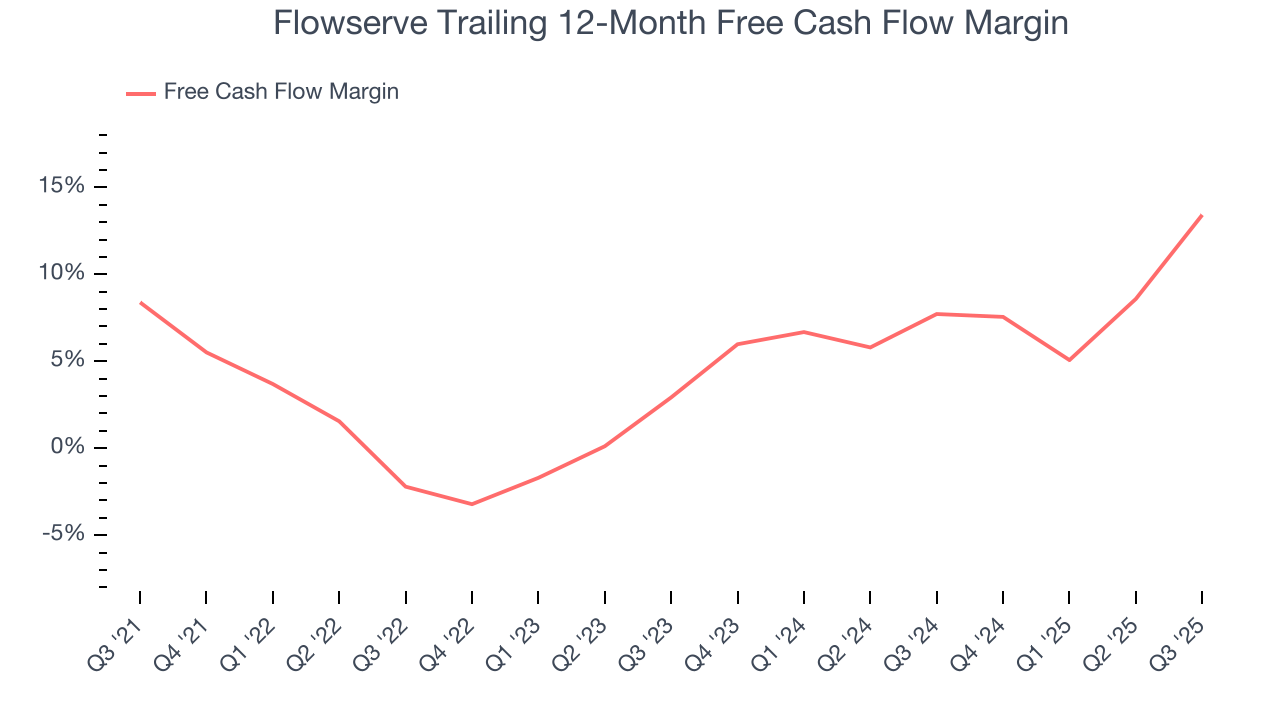

- Free Cash Flow Margin: 32.8%, up from 13.6% in the same quarter last year

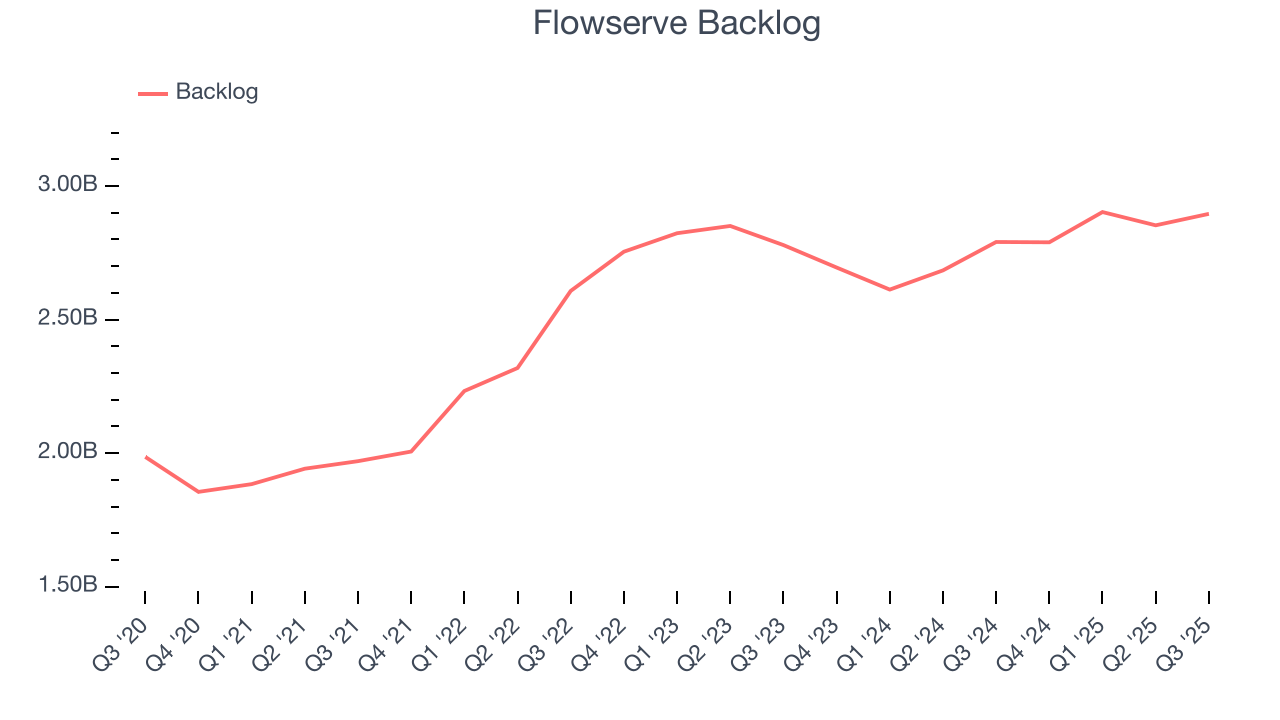

- Backlog: $2.9 billion at quarter end, up 3.8% year on year

- Market Capitalization: $6.91 billion

Company Overview

Manufacturing the largest pump ever built for nuclear power generation, Flowserve (NYSE:FLS) manufactures and sells flow control equipment for various industries.

Flowserve began as a manufacturer of pumps for the oil and gas industry but has evolved through acquisitions. In 2004 the company purchased SIHI, which expanded its presence internationally, and Lawrence Pumps in 2011, which strengthened its position in the chemical and general industries. Today, the company offers its products to oil refineries, chemical plants, power plants, and municipal water treatment facilities.

Flowserve’s product portfolio is made up of fluid control equipment which facilitate the movement, control, and protection of fluids in industrial processes. Specifically, its products include pumps, valves, seals, and automation technologies. It also offers services such as maintenance and repairs, which serve as a stream of recurring revenue.

Flowserve sells its products through direct sales, distribution channels, and online platforms. Its sales force engages directly with customers while distribution partners extend its reach. Furthermore, the company engages in contracts that vary in scope and duration, offering lower per-unit costs dependent on volume to incentivize larger purchases.

4. Gas and Liquid Handling

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Competitors offering similar products include Emerson Electric (NYSE:EMR), ITT (NYSE:ITT), and Grundfos (private).

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Flowserve grew its sales at a sluggish 4.2% compounded annual growth rate. This was below our standard for the industrials sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Flowserve’s annualized revenue growth of 5.7% over the last two years is above its five-year trend, but we were still disappointed by the results.

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Flowserve’s backlog reached $2.9 billion in the latest quarter and averaged 1.2% year-on-year growth over the last two years. Because this number is lower than its revenue growth, we can see the company hasn’t secured enough new orders to maintain its growth rate in the future.

This quarter, Flowserve’s revenue grew by 3.6% year on year to $1.17 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and implies its newer products and services will not lead to better top-line performance yet.

6. Gross Margin & Pricing Power

Flowserve’s unit economics are better than the typical industrials business, signaling its products are somewhat differentiated through quality or brand. As you can see below, it averaged a decent 30.7% gross margin over the last five years. That means for every $100 in revenue, roughly $30.73 was left to spend on selling, marketing, R&D, and general administrative overhead.

Flowserve produced a 32.4% gross profit margin in Q3, in line with the same quarter last year. On a wider time horizon, Flowserve’s full-year margin has been trending up over the past 12 months, increasing by 1.6 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Flowserve has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.4%, higher than the broader industrials sector.

Looking at the trend in its profitability, Flowserve’s operating margin rose by 2.5 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Flowserve generated an operating margin profit margin of 6.7%, down 2.4 percentage points year on year. Since Flowserve’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Flowserve’s EPS grew at a solid 10.5% compounded annual growth rate over the last five years, higher than its 4.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Flowserve’s earnings can give us a better understanding of its performance. As we mentioned earlier, Flowserve’s operating margin declined this quarter but expanded by 2.5 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Flowserve, its two-year annual EPS growth of 23.6% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q3, Flowserve reported adjusted EPS of $0.90, up from $0.62 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Flowserve’s full-year EPS of $3.13 to grow 16.5%.

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Flowserve has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.5% over the last five years, slightly better than the broader industrials sector.

Taking a step back, we can see that Flowserve’s margin expanded by 5 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Flowserve’s free cash flow clocked in at $384.7 million in Q3, equivalent to a 32.8% margin. This result was good as its margin was 19.1 percentage points higher than in the same quarter last year, building on its favorable historical trend.

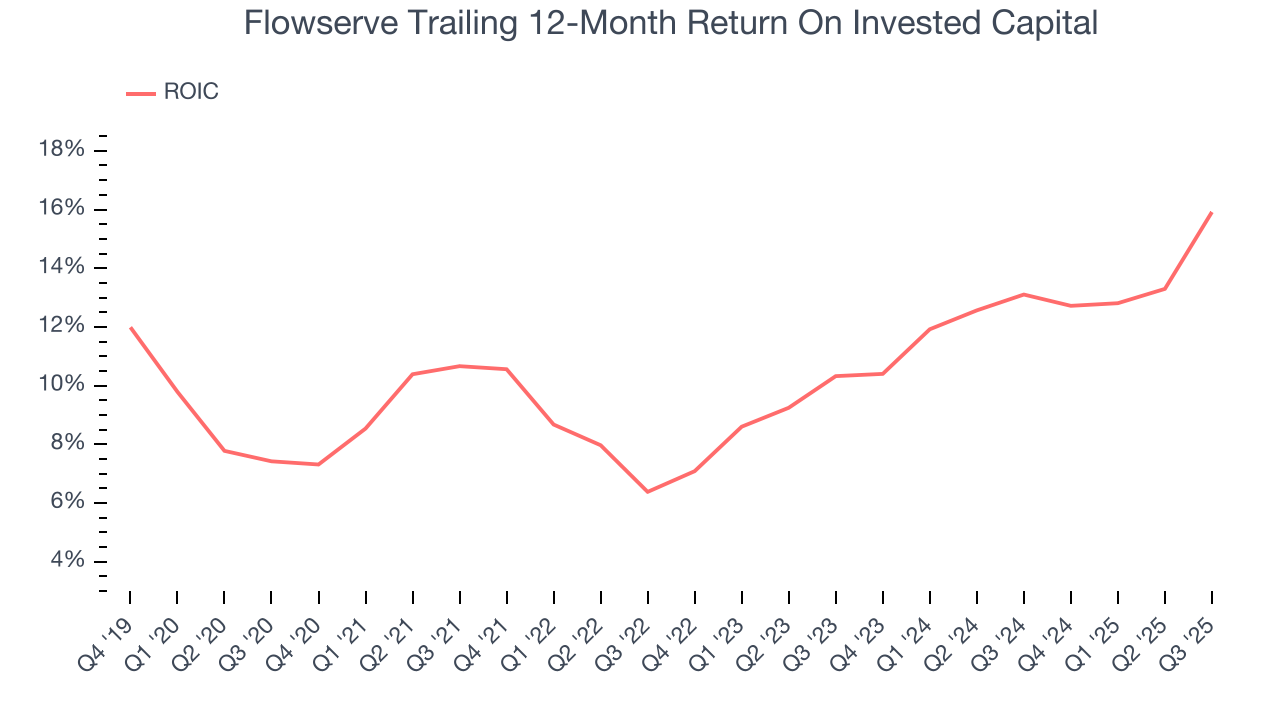

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Flowserve’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 11.3%, slightly better than typical industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Flowserve’s ROIC has increased. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

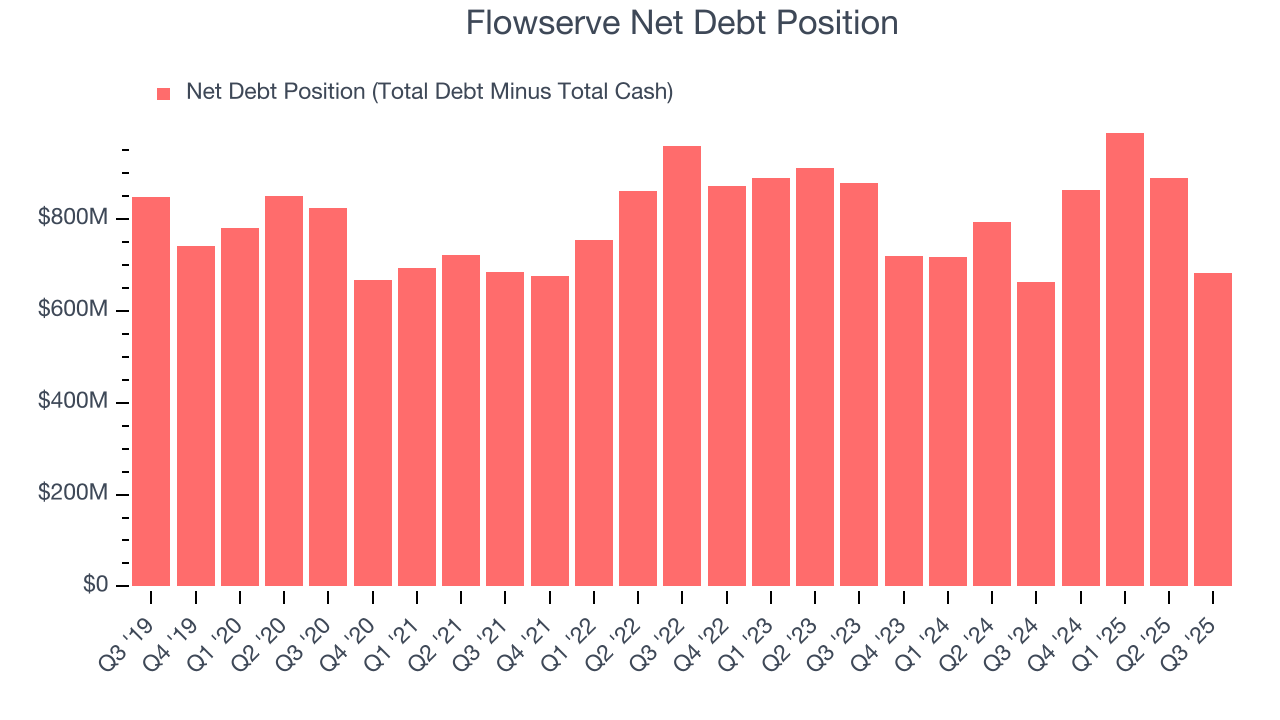

11. Balance Sheet Assessment

Flowserve reported $833.8 million of cash and $1.52 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $738.5 million of EBITDA over the last 12 months, we view Flowserve’s 0.9× net-debt-to-EBITDA ratio as safe. We also see its $71.96 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Flowserve’s Q3 Results

We were impressed by how significantly Flowserve blew past analysts’ backlog expectations this quarter. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. On the other hand, its revenue missed. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 6.4% to $56 immediately following the results.

13. Is Now The Time To Buy Flowserve?

Updated: January 24, 2026 at 10:02 PM EST

Before deciding whether to buy Flowserve or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

In our opinion, Flowserve is a good company. Although its revenue growth was uninspiring over the last five years, its rising cash profitability gives it more optionality. And while its backlog growth has disappointed, its projected EPS for the next year implies the company’s fundamentals will improve.

Flowserve’s P/E ratio based on the next 12 months is 20.2x. Looking at the industrials landscape right now, Flowserve trades at a pretty interesting price. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $80.80 on the company (compared to the current share price of $77.76), implying they see 3.9% upside in buying Flowserve in the short term.